23 companies

Capdesk

Capital Markets🇬🇧 United Kingdom

Equity management for private companies has historically been a mess of spreadsheets, lawyer markup, and reconciliation errors that compound silently until a fundraising round forces everyone to discover that the cap table reality differs from the cap table on file. Capdesk was founded in Copenhagen and grew up in London from 2015, building equity management software for private companies — a single source of truth for share allocations, option grants, vesting schedules, and shareholder communications. The product targets the gap between an Excel spreadsheet and a full-blown share registry: too small for the latter, too important to entrust to the former. Capdesk has built a strong client base across UK and European startups and scaleups, becoming one of the more trusted equity management platforms in Europe. The company was acquired by US-based Carta in 2023, consolidating the European equity management market under the umbrella of one of its largest global players. The acquisition reflects a broader pattern in private market infrastructure — the platforms that manage equity, fundraising, and investor relations are consolidating around a small number of comprehensive solutions. For European companies that built on Capdesk, the Carta acquisition brings them into a global platform with broader functionality at the cost of the local independence that some clients valued.

Nordnet

Wealth🇸🇪 Sweden

Pan-Nordic retail investing requires more than translating a Swedish product into Norwegian, Danish, and Finnish. Each Nordic market has its own pension system, tax-advantaged investment accounts, regulatory framework, and consumer expectations — complexity that has kept many investment platforms confined to a single national market. Nordnet was founded in Stockholm in 1996 with the explicit ambition to build a genuinely Pan-Nordic investment platform, and has spent nearly three decades doing it. Its platform serves customers across Sweden, Norway, Denmark, and Finland, offering stocks, funds, ETFs, pensions, and savings products tailored to each market's specific tax-advantaged account structures. The cross-border depth is genuinely unusual — most Nordic financial services companies that operate internationally do so through separate national entities with separate products, rather than the integrated platform approach that Nordnet has built. The company is publicly listed on the Stockholm Stock Exchange and competes directly with Avanza in the Swedish market while occupying dominant positions in several other Nordic countries. In the European retail investment landscape, Nordnet's combination of cross-border integration and decades of operational depth makes it one of the most credible regional brokers in any European market — a model that the rest of Europe has been slower to replicate.

Primary Bid

Wealth🇬🇧 United Kingdom

Primary Bid sits at the intersection of investment access and market fairness. For years, retail investors have watched from the sidelines while institutional players get first crack at hot IPO allocations. Primary Bid flips that script, letting everyday people invest in initial public offerings directly, cutting out the traditional gatekeepers that have hoarded these opportunities.

The platform operates as a digital intermediary between retail investors and companies going public, democratizing access to what was once a VIP-only event. It's not just about fairness—it's about giving ordinary Europeans the chance to participate in wealth creation at the most exciting moment in a company's lifecycle.

Unlike traditional investment banks that cherry-pick their favored clients, Primary Bid opens the IPO window to anyone with a UK brokerage account. This challenges the old model where your wealth determined your access. The company essentially rebuilds the IPO process for the internet age, stripping away exclusivity and replacing it with transparency and scale.

In the broader fintech landscape, Primary Bid represents a quiet but powerful shift toward democratized capital markets—proving that retail investors aren't just traders chasing memes, but serious participants worthy of institutional-quality opportunities.

Raisin

Wealth🇩🇪 Germany

Raisin operates as Europe's leading savings marketplace, connecting millions of savers with competitive deposit and investment products across a fragmented banking landscape. Rather than building its own bank, Raisin has assembled a platform that lets customers shop for the best rates on savings accounts, fixed-rate deposits, and bonds from hundreds of partner institutions—cutting through the friction that keeps most European savers stuck with their hometown banks paying near-zero interest. The core insight is deceptively simple: most people never comparison shop for savings because it's tedious, so they leave money on the table. Raisin automated that tedium and standardized the onboarding, making it easy to move cash between institutions in search of yield. This positions it somewhere between a broker, a marketplace operator, and a fintech enabler. The platform operates across multiple European markets—Germany, Austria, Spain, France, and the UK—and has scaled to manage billions in deposits through its partner banks. By aggregating demand and making switching painless, Raisin has built a defensible moat in an industry where incumbents have historically relied on customer inertia. Unlike neobanks chasing transaction volume or fintechs building products for the already-engaged, Raisin targets the vast middle: ordinary savers who want better returns without complexity. Its expansion into investment products shows ambition to become the default platform for European retail savings and wealth building, operating as infrastructure for the continent's distributed banking system.

Finastra

Financial Infrastructure🇬🇧 United Kingdom

Finastra is a London-based financial software giant that powers the plumbing behind modern finance. Rather than chasing consumers with flashy apps, Finastra builds the invisible infrastructure that banks, investment firms, and capital markets players depend on to operate. Think of it as the operating system for institutional finance—the sort of company most people have never heard of but whose systems process trillions in transactions daily.

The company's portfolio spans core banking systems, treasury management platforms, capital markets solutions, and lending technology. Finastra operates at the intersection of legacy finance and digital transformation, helping traditional institutions modernize their backend without scrapping decades of accumulated complexity. For banks and brokers, Finastra's software is often indispensable—the kind of vendor you can't easily replace once integrated into your operations.

In the European market, Finastra competes with other heavyweight infrastructure players but stands out for its broad coverage across retail, corporate, and capital markets segments. The company has grown partly through acquisition, absorbing competitors and bolt-on technologies to expand its ecosystem. It's not the startup disrupting finance from the margins; it's the entrenched platform that established institutions lean on to survive and scale.

CRX Markets

Capital Markets🇩🇪 Germany

CRX Markets operates in the murky territory between traditional finance and crypto, building infrastructure for regulated digital asset trading. The London-based platform serves institutional players who need the guardrails of compliance alongside the speed and transparency that blockchain-native markets promise. Rather than choosing between TradFi rigor and crypto innovation, CRX sits in the middle—offering a regulated venue for tokenized assets and digital securities that feels more like a regulated exchange than a crypto casino. The firm works with brokers, asset managers, and custodians who want exposure to digital assets but can't afford the regulatory ambiguity. What sets CRX apart is its focus on institutional-grade infrastructure: proper settlement, custody integration, and regulatory transparency. While most crypto platforms chase retail volume and headline-grabbing token launches, CRX is quietly building the plumbing that makes institutional participation in digital markets actually viable. It's the kind of infrastructure play that doesn't get flashy media coverage but matters enormously for the evolution of finance. In a landscape where most platforms are either fully traditional or fully crypto, CRX represents the emerging middle ground where serious institutions are beginning to operate.

PlanDelta

Capital Markets🇩🇪 Germany

Private equity and corporate finance practitioners spend a remarkable share of their working time on financial modelling tasks that have not changed substantively in twenty years — building DCF models, LBO models, and scenario analyses in Excel templates that are passed between analysts, marked up by partners, and remain the lingua franca of deal evaluation despite the obvious limitations of the medium. PlanDelta was founded in Germany in 2019 to bring modern software approaches to that workflow. Its platform supports financial modelling, scenario planning, and deal evaluation for corporate finance teams and investment professionals, replacing or augmenting Excel-based processes with collaborative tools designed for the specific demands of transaction work. The product targets the gap between the spreadsheet world that defines most deal work and the enterprise FP&A platforms that serve very different use cases. In the European corporate finance technology landscape, the willingness of investment professionals to move workflows out of Excel has historically been limited — the medium is universal, the templates are inherited, and the switching costs are high. Companies building products in this space need to demonstrate that their tools genuinely improve the quality and speed of analysis rather than just changing the interface. PlanDelta is building toward that demonstration in a market where the resistance to new tools is real but the underlying need for better analytical infrastructure is genuine.

Kvika

Wealth🇮🇸 Iceland

Kvika is an Icelandic investment bank and fintech firm that has quietly built something rarely seen in Europe's crowded fintech space: a full-service wealth and capital markets platform designed for serious investors, not casual traders. Founded in the early 2000s, the company operates as a licensed bank rather than a scrappy startup, which gives it something most fintechs lack—direct access to markets, custody capabilities, and institutional credibility.

The platform combines retail investment tools with professional-grade execution and advisory services. You can trade equities, bonds, funds, and derivatives across multiple exchanges, but Kvika doesn't compete on flashiness. Instead, it positions itself as the thinking investor's choice in a market saturated with gamified trading apps and commission-free broker clones.

What sets Kvika apart in the Nordic and European context is its hybrid model. It serves both individual investors seeking serious portfolio management and corporate clients needing capital markets access. The company operates with the regulatory infrastructure and market relationships that pure fintechs spend years trying to replicate, yet it maintains the technology-first approach that defines modern finance.

Kvika represents a different kind of European fintech success—one built on institutional foundations rather than disruption narratives. It's the kind of player that rarely makes headlines but quietly captures the investor who wants depth over hype.

ION Group

Financial Infrastructure🇬🇧 United Kingdom

ION Group is a sprawling financial software empire that has quietly become one of Europe's most comprehensive infrastructure plays. The company operates across trading, risk management, and post-trade processing—the unsexy but absolutely critical backbone that powers global capital markets. Unlike flashy fintech startups chasing consumer adoption, ION builds the invisible plumbing that institutional traders, hedge funds, and investment banks depend on every single day. Its portfolio spans front-office platforms, market data aggregation, clearing and settlement systems, and regulatory reporting tools. ION serves as a counterweight to the purely consumer-focused fintech narrative, proving there's enormous value in solving problems for professionals who move billions. The company's strength lies in its ability to connect disparate financial systems, providing what amounts to a unified operating system for institutional finance. For European financial institutions, ION represents a trusted partner in an increasingly complex regulatory landscape, offering solutions that integrate seamlessly with legacy infrastructure while modernizing workflows. Its acquisition-driven growth strategy—picking up niche specialists and consolidating them into a cohesive platform—mirrors the broader consolidation happening across enterprise fintech. ION's market position underscores a fundamental truth about fintech: the biggest opportunities often lie in B2B infrastructure rather than consumer apps.

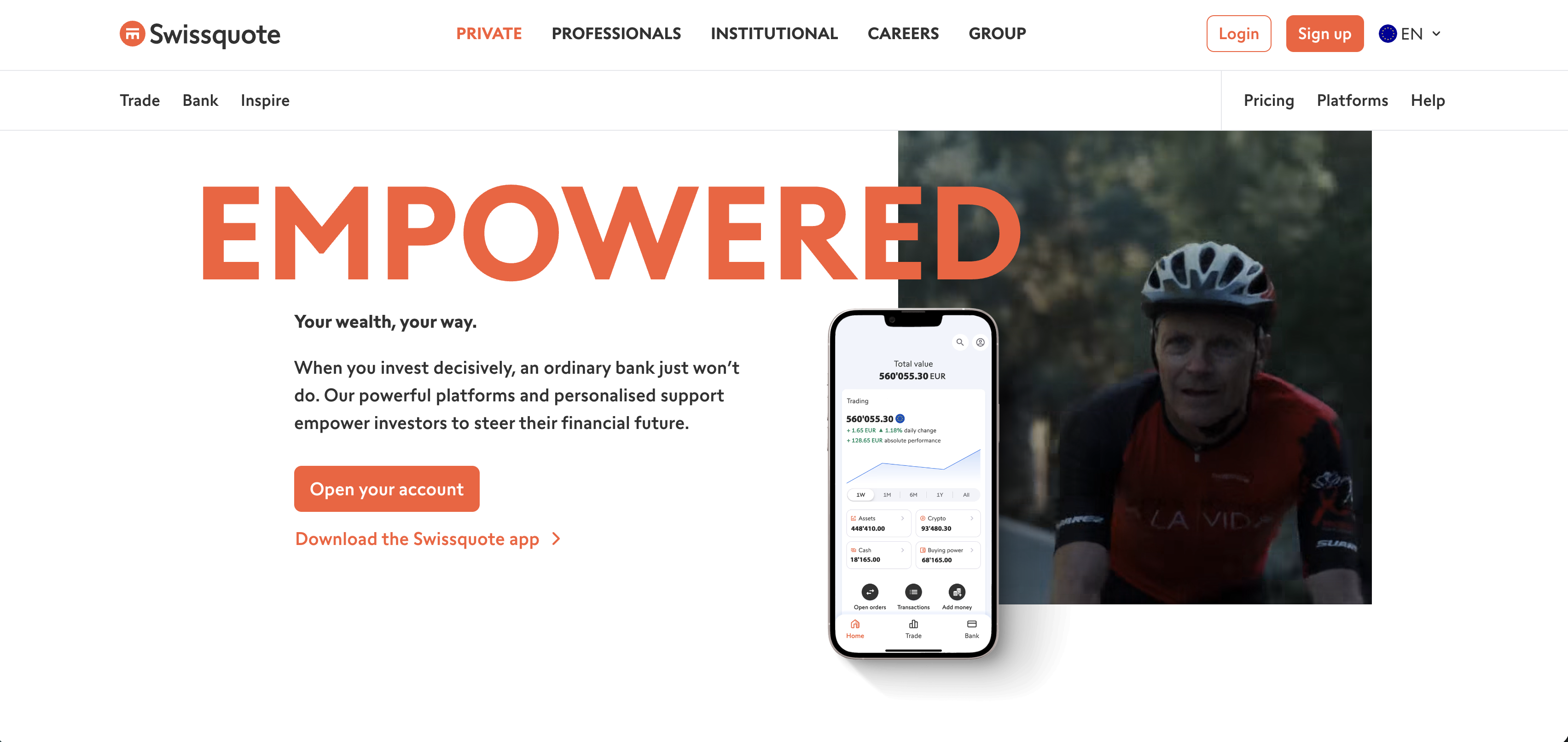

Swissquote

Wealth🇨🇭 Switzerland

Swissquote is a Swiss online banking and investment platform that democratised retail access to capital markets long before the term fintech became fashionable. Founded in 1996, it operates as a full-service digital broker, offering everything from currency trading and stocks to cryptocurrencies and structured products—all wrapped in the kind of regulated, institutional-grade infrastructure you'd expect from Switzerland.

The platform serves both everyday investors and active traders, positioning itself as a counterweight to traditional brokers by eliminating gatekeeping and offering direct market access. Its digital-first approach means clients manage portfolios through intuitive apps and web interfaces rather than dealing with relationship managers. Swissquote has progressively expanded into crypto custody and trading, recognizing early that digital assets would become table stakes in modern wealth management.

Within Europe's competitive fintech landscape, Swissquote occupies a middle ground between pure-play neobanks and heavyweight institutional players. It lacks the brand velocity of newer challengers but carries the regulatory credibility of its Swiss heritage and banking license. The company has built longevity by staying disciplined about what it does well—trading, investing, and increasingly, custodying digital assets—rather than chasing every trend.

Today, Swissquote represents a particular archetype in European fintech: the early mover that survived consolidation, scaled sustainably, and now competes by coupling digital experience with the trust premium of being rooted in one of the world's most regulated financial jurisdictions. It's neither disruptive in the startup sense nor stagnant—it's simply a mature digital-first investment platform that works.