95 companies

MonzoFeatured

Wealth🇬🇧 United Kingdom

The founding team that built Monzo had all worked together before — at Starling Bank, another challenger bank startup that didn't survive its internal conflicts. Tom Blomfield, Gary Dolman, Jonas Huckestein, Jason Bates, and Paul Rippon left Starling together in 2015 and started again. The product they built was initially a prepaid card — a coral-coloured piece of plastic that became one of the most recognisable objects in British fintech — before becoming a fully licensed current account in 2017.

The early user community was unusual for a bank. Monzo ran community forums, published public blog posts about its engineering decisions, and invited customers into beta programmes for new features. When it broke the world record for the fastest crowdfunding raise in 2016 — £1 million in 96 seconds — it wasn't just raising money; it was building an identity. People felt ownership of the product in a way that no high street bank had ever managed to create. That emotional connection became a genuine competitive advantage.

The product has matured considerably since then. Monzo now offers current accounts, joint accounts, savings pots, personal loans, overdrafts, and investment products, all wrapped in the real-time notification experience and transaction categorisation that made its early reputation. Revenue reached £1.23 billion in 2024, up 40% year on year, with net income of £95 million — the second consecutive year of profitability after years of growth-first losses. The customer base reached 12.1 million by end of 2024, making Monzo the UK's largest digital bank by customer count. Customer deposits stood at £16.6 billion.

The business is still private — the much-discussed IPO has not yet happened, and internal disagreements about where to list (the former CEO TS Anil favoured the US, the board preferred London) contributed to Anil's departure in October 2025. Diana Layfield took over as CEO with a mandate focused on international expansion before any public listing. The company is valued at approximately $5.9 billion following a 2024 secondary sale backed by Alphabet's GIC and StepStone.

In December 2025 Monzo announced it had agreed to acquire Habito, the digital mortgage broker, pending regulatory approval — a move that extends the product into one of the last major financial products it didn't yet offer. With 3,821 employees and a loan book growing rapidly, Monzo has evolved from a prepaid card experiment into a bank with genuine scale and a growing claim on being the primary financial account for a generation of UK consumers.

Flexfin

Lending🇬🇷 Greece

Flexfin provides invoice financing and working capital for Greek businesses.

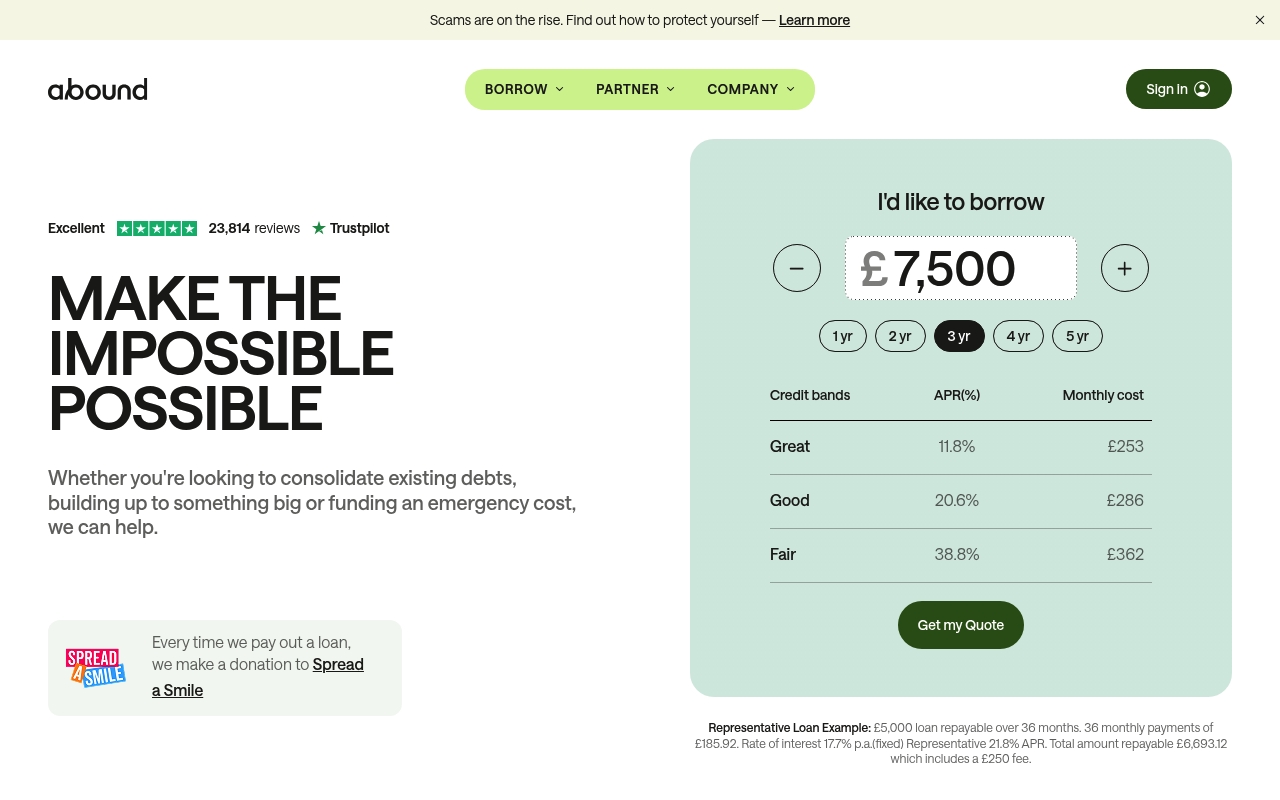

Abound

Open Banking🇬🇧 United Kingdom

Abound uses open banking data to make consumer lending decisions more personal.

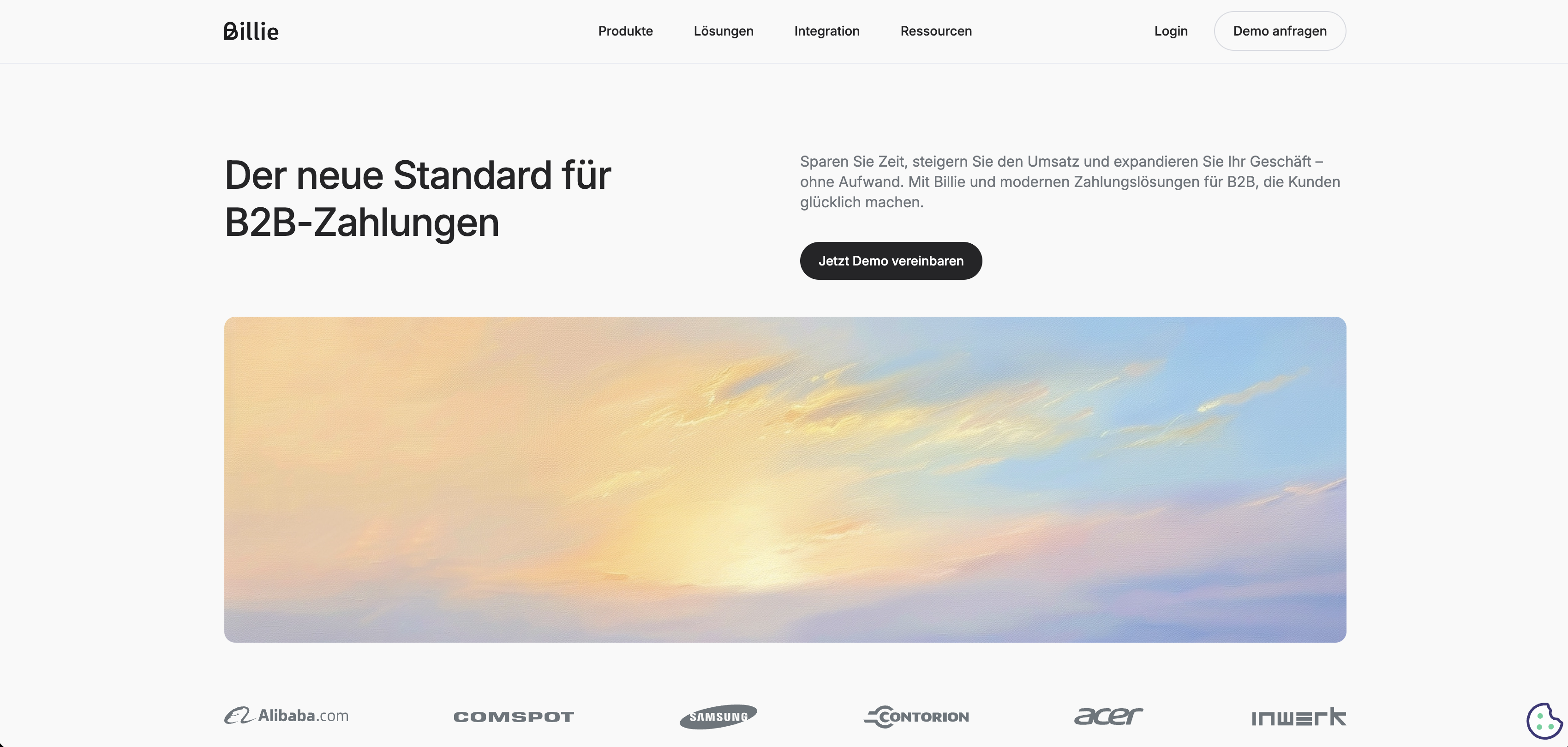

Billie

Lending🇩🇪 Germany

Billie is a B2B payments platform built for small businesses and freelancers who are tired of chasing invoices. Instead of waiting 30, 60, or 90 days to get paid, users can access their outstanding invoices instantly through Billie's platform, converting them into immediate working capital without the traditional loan machinery.

The service works like this: businesses upload their invoices, Billie validates them, and funds arrive within hours. It's not a loan in the conventional sense—there's no credit scoring, no months of approval waiting, just a straightforward advance against money that's already owed. The economics are transparent: a small fee on the advance, nothing else.

Billie positions itself against the backdrop of Europe's slow payment culture, where SMEs are routinely starved of cash flow by larger clients who take their time settling bills. While traditional banks offer supply chain financing to enterprises, Billie democratizes this for the mid-market and smaller players who have real invoices but zero patience for bureaucracy.

In the broader fintech landscape, Billie sits at the intersection of lending, payments, and working capital—essentially making invoice financing frictionless for businesses that actually need it.

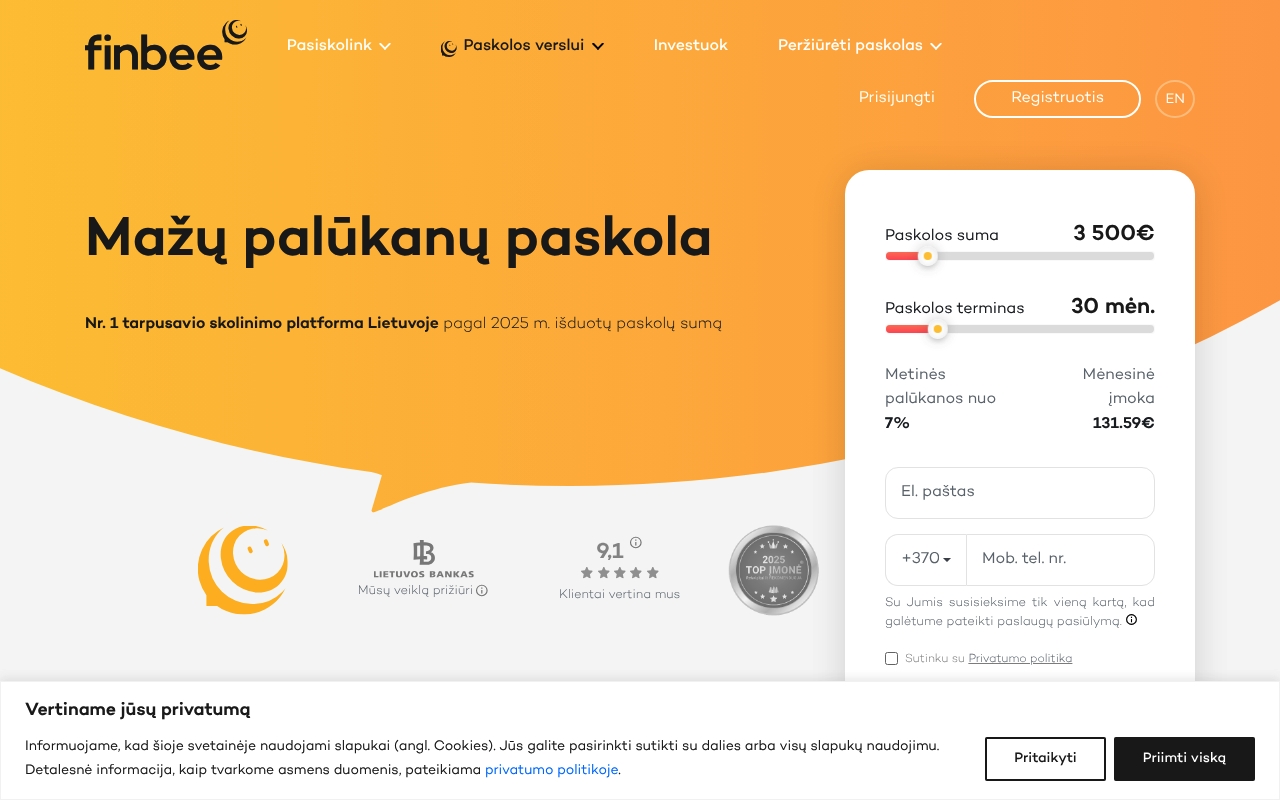

Finbee

Lending🇱🇹 Lithuania

Peer-to-peer business lending — connecting retail investors with creditworthy small businesses needing growth or working capital — represents a category within marketplace lending where the underwriting complexity is greater than consumer P2P but the credit characteristics are different. Finbee was founded in Vilnius in 2015 to build a Lithuanian platform offering both consumer and business P2P lending products, with an underwriting infrastructure designed to evaluate the specific risk characteristics of Lithuanian SMEs alongside individual borrowers. The platform has built a substantial domestic position in the Lithuanian marketplace lending segment, attracting both local and Pan-European investors looking for exposure to Lithuanian credit. Finbee's product range and operational depth reflect a decade of operating in a market that has been one of Europe's more active testbeds for P2P lending innovation — with multiple platforms, supportive regulation, and a retail investor base willing to engage with marketplace lending products. In the Baltic alternative lending landscape, Finbee represents the category of platform that has built durability through diversified product offerings and disciplined underwriting rather than aggressive growth — a positioning that has aged better than some of the more growth-focused models that dominated the early P2P era.

Avafin

Lending🇨🇿 Czech Republic

Consumer credit in Central and Eastern European markets continues to evolve through the slow process of digital infrastructure replacing the informal and bank-based credit options that previously dominated. Avafin operates in that evolving landscape, providing digital consumer loans across multiple CEE markets including the Czech Republic, Poland, Latvia, and Spain. The company offers short-term and instalment consumer credit through digital channels, with underwriting infrastructure that has been built around the specific credit data and regulatory environments of each market it operates in. Avafin's positioning emphasises responsible lending standards and regulatory compliance — a deliberately conservative posture in a sector where the line between accessible credit and exploitative credit is constantly contested by regulators and consumer protection organisations. The company is part of a broader portfolio of consumer credit operations that have been built around the operational depth required to lend across multiple CEE jurisdictions while maintaining consistent credit performance. In the broader European consumer credit landscape, the CEE digital lending segment has matured significantly over the past decade — moving from the early days of high-cost short-term lending toward a more diversified product range that increasingly resembles the consumer credit options available in Western European markets, just with different distribution and underwriting infrastructure underneath.

CashCredit

Lending🇧🇬 Bulgaria

CashCredit operates in Bulgaria's consumer lending space, offering quick cash loans through a digital interface designed for speed and accessibility. The platform targets individuals seeking fast credit decisions without the bureaucratic friction of traditional banking. In a market where many borrowers still face lengthy application processes, CashCredit compresses the timeline through online application and rapid underwriting. The company positions itself as a straightforward alternative for personal borrowing, emphasizing the simplicity of its loan products. As part of Bulgaria's emerging fintech lending ecosystem, CashCredit represents the shift toward digital-first credit provision in Central and Eastern Europe, where traditional banks remain slow to modernize their consumer lending operations. The company's core offering sits at the intersection of accessibility and speed—two factors that increasingly define competitive advantage in the consumer lending space across the region.

Finloup

Financial Infrastructure🇬🇷 Greece

Finloup is a European lending infrastructure platform that helps financial institutions and fintechs automate credit decisions and manage loan portfolios at scale. The company builds white-label software that sits between lenders and borrowers, handling everything from application to origination to ongoing portfolio management. Rather than reinventing the wheel for each lender, Finloup abstracts away the operational complexity of modern lending—think of it as the backstage machinery that lets banks and fintech lenders focus on distribution and customer experience instead of building lending systems from scratch. The platform works across consumer and SME lending, serving institutions across multiple European markets who need faster, smarter, more compliant ways to originate and manage credit. Where traditional core banking systems move slowly and cost millions to customize, Finloup offers speed and flexibility. It's built for a market where fintech lending has exploded but the infrastructure hasn't kept pace with demand. The company essentially democratizes access to institutional-grade lending technology, lowering the barriers for smaller players to compete with incumbents. Within the broader fintech ecosystem, Finloup represents a critical infrastructure layer—the unsexy but essential plumbing that makes modern lending possible at European scale.

Mambu

Financial Infrastructure🇩🇪 Germany

Mambu is a cloud-native banking software platform that lets financial institutions and fintechs launch and operate lending and deposit products without building from scratch. Rather than forcing customers into rigid legacy systems, Mambu provides composable banking infrastructure—modular APIs and pre-built components that work together or stand alone, depending on what you actually need.

The company sits at the intersection of two fintech realities: traditional banks are drowning in outdated core systems that can't keep pace with market demands, while new lenders and neobanks need speed without sacrificing compliance or scale. Mambu's approach is to be the operating system underneath, handling the heavy lifting of loan origination, deposit management, portfolio servicing, and regulatory reporting while letting clients focus on customer experience and product innovation.

What makes Mambu different from other core banking platforms is its emphasis on velocity. Institutions deploy in weeks rather than years. The platform is genuinely modular—you can pick the lending module, the deposit module, or both, and layer in third-party services through APIs. This flexibility has resonated with everyone from African microfinance networks to European challenger banks to enterprise lenders managing complex credit products.

Mambu is now a critical piece of infrastructure in the emerging markets fintech ecosystem, particularly across Africa and Asia, where it powers lending operations for hundreds of financial institutions. In Europe, it's carved out space among mid-market and challenger banks looking to avoid the capital expenditure and technical debt of legacy systems. The company represents a broader shift in fintech: away from end-to-end platforms that claim to do everything, toward specialized infrastructure that does one thing—backend financial operations—exceptionally well.

Credolab

Identity & KYC🇳🇱 Netherlands

Credit decisions in markets without comprehensive credit bureau coverage have always been hard. The traditional underwriting model relies on credit history, income verification, and identity documents that significant portions of the global population either don't have or can't easily produce. Credolab was founded in 2016 with operations across Asia and Europe to address that gap with an unconventional data source — smartphone metadata. Its platform analyses behavioural patterns from a mobile device — without accessing personal content — to generate credit scores for consumers who have no traditional credit history. The data points are surprisingly predictive: how someone manages their phone storage, the pattern of their app usage, the regularity of their device behaviour all correlate with credit risk in ways that traditional underwriting misses. Credolab serves lenders, telcos, and digital platforms across emerging markets where credit bureau coverage is thin and the demand for digital credit is growing rapidly. In the alternative credit data landscape, where companies are competing to find the data sources that will define the next generation of underwriting, Credolab's behavioural smartphone approach is one of the more distinctive — and one that addresses a genuinely large unmet need in markets where billions of people remain credit-invisible to traditional financial systems.