42 companies

TinkFeatured

Embedded Finance🇸🇪 Sweden

Daniel Kjellén and Fredrik Hedberg didn't set out to build infrastructure. Tink started in Stockholm in 2012 as a consumer personal finance app — an attempt to give Swedish bank customers a cleaner view of their money across multiple accounts. It was a reasonable idea that ran into an unreasonable obstacle: getting reliable, consistent data out of European banks was extraordinarily hard. The technical problem turned out to be more interesting than the consumer product. In 2018 they pivoted, shifted focus entirely to the B2B layer, and started selling the very infrastructure they'd been forced to build for themselves.

That pivot proved prescient. The EU's PSD2 directive, which came into full effect in 2019, legally required banks to open their data to authorised third parties — creating the regulatory foundation that open banking platforms needed to operate at scale. Tink had spent years building exactly those bank connections. When the regulation arrived, the company was ready.

The platform Kjellén and Hedberg built connects to more than 3,400 banks and financial institutions across Europe, reaching over 250 million bank customers. Through a single API integration, banks, fintechs, and merchants can access aggregated account data, initiate payments directly from customer bank accounts, verify account ownership, and enrich transaction data — without maintaining their own connections to hundreds of separate banking systems with different technical standards and update schedules. Clients include Klarna, PayPal, NatWest, ABN AMRO, and BNP Paribas Fortis.

In March 2022, Visa completed the acquisition of Tink for €1.8 billion — one of the largest European fintech acquisitions of that year, and a clear signal of how seriously the global payments industry had come to take open banking infrastructure. Visa's strategic rationale was straightforward: it had failed to acquire Plaid, the US equivalent, after an antitrust challenge, and needed a European open banking capability. Tink gave it 500 employees, 18 European markets, and relationships with over 300 banks and fintechs built over a decade.

The founders stayed on as CEO and CTO through the transition, continuing to run Tink as a standalone Visa subsidiary from Stockholm. Both departed in 2025 — Kjellén and Hedberg announced they were building Freda, a new AI-driven legal and compliance technology startup, with the pair describing Tink as "now in better hands than ever." Francois Tornier, Visa's VP of Open Banking, took over as CEO. The product roadmap has continued under Visa ownership, including a 2024 expansion of Tink's open banking platform into the US market.

Moneyhub

Wealth🇬🇧 United Kingdom

Open banking's promise — that financial data, properly used, can help people make better decisions — has been articulated by hundreds of companies. Moneyhub has spent longer than most actually delivering it. Founded in Bristol in 2014, it built one of the UK's first and most comprehensive open banking platforms, aggregating financial accounts, pension data, and property values into a unified financial picture that gives users — and the institutions serving them — a genuinely complete view of financial health. Its B2B platform powers the open banking and financial wellness features of major UK employers, financial advice firms, and pension providers, white-labelling its data aggregation and analytics capabilities under their brands. The pensions integration is particularly significant — Moneyhub connects to pension providers alongside bank accounts, giving users visibility into their retirement savings alongside their current financial position. That breadth of financial data coverage — beyond the current account focus of most open banking platforms — is a genuine differentiator. In the UK open banking ecosystem, where the FCA's consumer duty requirements are pushing financial institutions to demonstrate they understand their customers' broader financial circumstances, Moneyhub's comprehensive data view is becoming infrastructure rather than a nice-to-have.

Linxo

Open Banking🇫🇷 France

Linxo is a European personal finance platform that aggregates bank accounts, credit cards, and investments across multiple institutions into a single dashboard. Rather than asking users to switch banks entirely, the app pulls live data from existing accounts—a model that respects the European's pragmatic relationship with their primary bank while offering the insights and control they actually want. The company positions itself as the financial operating system for everyday money management, not a replacement for banking itself.

What sets Linxo apart in a crowded personal finance space is its focus on actionable intelligence. Beyond simple balance-checking, the platform categorizes spending automatically, alerts users to unusual transactions, and helps track progress toward financial goals—all without the paternalistic tone of many budgeting apps. It works across France, Spain, Germany, Italy, and Belgium, making it one of the few genuinely pan-European plays in a category often dominated by single-market apps.

Linxo has built its infrastructure on open banking standards, leveraging PSD2 APIs to connect securely to banking institutions rather than relying on screen-scraping. This approach gives it a technical moat while also keeping it aligned with regulatory trends. The company targets digitally-native adults who want visibility into their finances without the friction of traditional banking interfaces.

In the broader fintech landscape, Linxo represents a specific bet: that most people won't abandon their bank, but they will absolutely pay for—or accept advertising within—a tool that makes that bank easier to use. It's less disruptive than a neobank, more practical than an investment app, and more design-forward than legacy personal finance software.

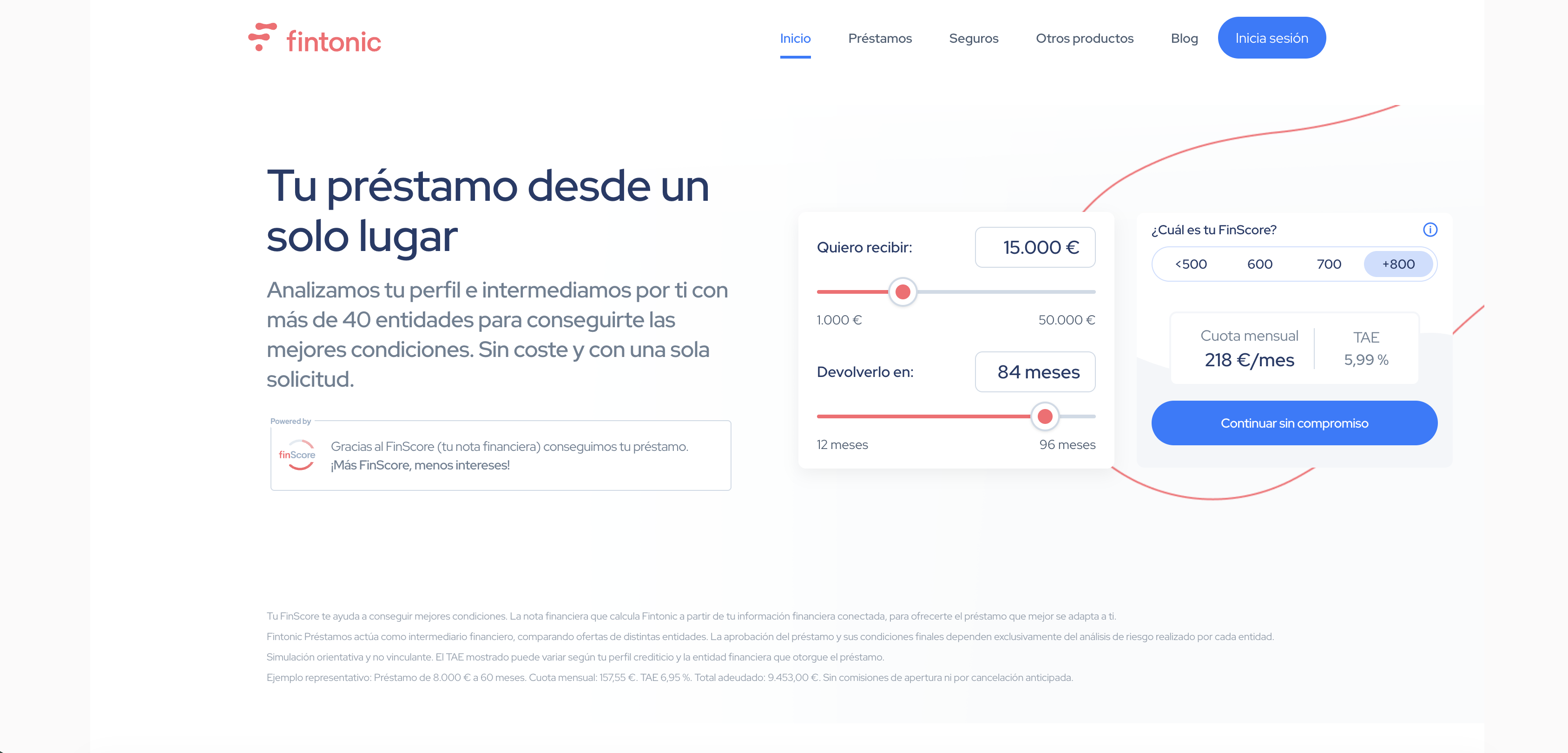

Fintonic

Open Banking🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

Trustly

Financial Infrastructure🇸🇪 Sweden

Trustly operates at the intersection of payment infrastructure and banking rails—a space where most European fintechs dabble, but few dominate. Founded on the premise that moving money across borders and between bank accounts shouldn't require three days and a legacy banking connection, Trustly has become the quiet backbone of European payments, handling transactions that power everything from e-commerce to iGaming to marketplace platforms.

The company's core insight is deceptively simple: why route payments through card networks when you can move money directly from bank account to bank account, in real time, across Europe? This approach—sometimes called account-to-account or bank-to-bank payments—eliminates the friction of card processing while delivering settlement speeds that card networks simply can't match. For merchants, it means lower costs and faster liquidity. For consumers, it means frictionless checkout experiences without the friction of entering card details.

Trustly's positioning is distinctly infrastructure-first. While competitors chase consumer-facing features or chase compliance nightmares in high-risk verticals, Trustly has built a modular, developer-friendly platform that lets businesses embed its payment rails directly into their own experiences. This B2B2C model—where Trustly powers payments for platforms that serve millions of end users—has become the company's superpower.

What sets Trustly apart in the European market is its breadth. The company isn't just a payments processor; it's a full-stack payments ecosystem. Cross-border transfers, open banking integrations, alternative payment methods, recurring billing—Trustly has layered these capabilities onto its core account-to-account infrastructure, creating something closer to a payments operating system than a single-use tool. In a landscape crowded with specialized point solutions, that generalist approach increasingly looks like prescience.

Trustly represents a fundamental shift in how European payments infrastructure is being rebuilt—one where bank integrations aren't a regulatory afterthought but the primary payment rail itself.

Eligma

Financial Infrastructure🇸🇮 Slovenia

Eligma is a cross-border payment and settlement infrastructure built for the digital economy. The company operates a network that simplifies how businesses and consumers move money across borders, stripping away the friction and opacity that characterizes traditional banking corridors. Rather than routing payments through legacy correspondent banking, Eligma connects participants directly, reducing settlement times from days to minutes while cutting costs substantially.

The platform bridges emerging markets with developed economies, focusing particularly on Southeast Asia and Europe. It's built for businesses that operate across jurisdictions—from e-commerce platforms to remittance providers to financial institutions themselves. Eligma abstracts away currency complexity and regulatory variance, presenting a single API that handles what would otherwise require juggling multiple banking relationships.

In a landscape crowded with neobanks and payment startups chasing domestic convenience, Eligma tackles the harder problem: the actual plumbing of international finance. It competes not on consumer interface but on network effects and operational resilience. The company positions itself as infrastructure for the fintech ecosystem itself, enabling other players to offer cross-border services without building the pipes from scratch.

Eligma represents a category increasingly important to European fintech: the B2B rails that sit beneath consumer-facing products, quietly moving capital where legacy banking leaves gaps. As European fintechs expand beyond their home markets, platforms like Eligma become critical dependencies rather than nice-to-have integrations.

Finary

Wealth🇫🇷 France

Wealthy individuals in France — and across Europe — tend to have their assets spread across multiple institutions: a current account here, a brokerage account there, real estate, a life insurance policy, perhaps some crypto. Getting a coherent picture of net worth across all of those positions has traditionally required either a private banker who charges for the privilege or a spreadsheet that goes out of date the moment you close it. Finary was founded in Paris in 2021 to solve that specific problem for the financially active generation that has moved beyond a single savings account. Its platform aggregates financial assets across banks, brokers, crypto exchanges, and real estate valuations into a single dashboard, providing net worth tracking, portfolio performance analysis, and asset allocation insights. The product is designed for the financially engaged user — someone who invests actively, owns multiple asset types, and wants the kind of portfolio view that was previously only available through private banking relationships. Finary has grown rapidly in the French market, tapping into a generation of investors who came of age during the low interest rate era and built diversified portfolios that their bank's app was never designed to show them clearly. In the European wealth tracking market, Finary represents the modern version of the portfolio management tool — mobile-first, multi-asset, and designed for self-directed investors.

Yapily

Embedded Finance🇬🇧 United Kingdom

Yapily sits at the intersection of open banking and embedded finance, building the plumbing that lets fintech companies and enterprises tap into banking data and payments without reinventing the wheel. Founded in 2016, the London-based company operates as an API infrastructure layer—connecting to banks across Europe and beyond to unlock account information, payment initiation, and consent management at scale.

What makes Yapily different is how it abstracts away the complexity of working with hundreds of banks and their inconsistent technical standards. Rather than forcing developers to build individual integrations for each bank's API, Yapily provides a unified interface that normalizes everything. It's the translator between your app and the messy reality of legacy banking infrastructure.

The company operates in the B2B2C space, partnering with fintechs, neobanks, and enterprise software providers who need banking connectivity but lack the resources to build it themselves. Their customer base spans lending platforms, wealth apps, accounting software, and payment orchestration layers—essentially anyone whose product benefits from real-time access to customer bank accounts or the ability to initiate payments.

Yapily's positioning is deliberately unsexy: they're infrastructure, not consumer-facing. But that's precisely the point. In a landscape crowded with consumer fintechs chasing headlines, Yapily has built a quiet, profitable business serving the builders themselves. They're to open banking what Stripe is to payments—the backbone that lets innovation happen faster.

Twikey

Financial Infrastructure🇧🇪 Belgium

Twikey sits at the intersection of payment orchestration and direct debit management, solving a problem most European fintechs have overlooked: how to automate recurring payments at scale. The platform enables businesses to collect payments via SEPA direct debit, card, and bank transfer—all orchestrated through a single API that feels less like legacy plumbing and more like modern infrastructure. Rather than forcing companies to juggle multiple payment rails and compliance frameworks, Twikey abstracts the complexity into intuitive workflows that handle mandate management, collections, and reconciliation with minimal friction. What sets Twikey apart is its obsession with the boring-but-critical work: ensuring compliance across jurisdictions, reducing failed payments through intelligent retry logic, and making recurring billing feel frictionless for both merchants and their customers. The company operates primarily in Western Europe but has built a platform designed to scale across the continent. In a landscape crowded with payment processors chasing flashy one-off transactions, Twikey has carved out territory in the unglamorous but lucrative recurring payment economy, where consistency and reliability matter far more than novelty. It's fintech infrastructure that doesn't try to be sexy—it just tries to work.

Spiir

Open Banking🇩🇰 Denmark

Personal finance app helping users manage money and spending.