181 companies

RevolutFeatured

Wealth🇱🇹 Lithuania

Nik Storonsky grew up moving between Russia and France before landing in London as a derivatives trader. Vlad Yatsenko was a software engineer who'd spent years building financial systems. In 2015 they sat down and asked a question that should have occurred to banks years earlier: why does spending money abroad still cost so much?

The answer they built was Revolut — initially a prepaid card with no foreign exchange fees, then a multi-currency account, then a trading platform, then an insurance product, then a business banking offering, then something that's increasingly hard to describe as anything other than a full financial operating system. Revolut didn't unbundle banking so much as rebuild it from scratch for people who found the existing version frustrating and expensive.

The numbers now are genuinely striking for a company that started with two people and a card. Revenue reached £4.5 billion in 2025, up 46% year on year, with net profit of £1.3 billion. The customer base grew to 68.3 million retail users — one in five working-age adults in Europe — plus 767,000 businesses. The company employs 12,200 people across more than 25 countries and was valued at $75 billion in a November 2025 secondary share sale, making it Europe's most valuable private technology company.

The milestone that mattered most, though, arrived in March 2026: a full UK banking licence from the Prudential Regulation Authority, ending a three-year application process that had become the most-watched regulatory saga in European fintech. The licence means Revolut can now protect UK deposits up to £120,000, offer authorised consumer credit, and compete directly with high street banks for mortgage and lending business. It's the piece that transforms Revolut from a very successful payments app into a regulated bank.

The company has also applied for a US banking charter and is expanding aggressively into Latin America, having opened its first bank outside Europe in Mexico. The original thesis — that banking could be cheaper, faster, and simpler — hasn't changed. The scale at which it's now being tested has.

AdyenFeatured

Embedded Finance🇳🇱 Netherlands

Pieter van der Does and Arnout Schuijff had already built and sold one payments company when they sat down in 2006 to start again. The result was Adyen — the name literally means "start over" in Surinamese — and the premise was simple: instead of stitching together the same fragmented payment infrastructure everyone else was using, they would build the whole thing themselves from scratch.

That decision, made in an Amsterdam office nearly two decades ago, is still the reason Adyen is different. Most payment companies are assemblers — they buy a gateway here, a processor there, bolt them together and hope for the best. Adyen owns its own technology stack end to end, which means a merchant integrating once gets access to card processing, local payment methods, point-of-sale terminals, and real-time settlement data through a single platform. No middle layers, no reconciliation headaches, no finger-pointing between vendors when something breaks.

The client list tells you everything about where Adyen sits in the market. McDonald's, Spotify, Microsoft, LVMH, H&M — these are companies with serious payment volumes and zero appetite for systems that don't work. Adyen became the default choice for enterprises that had outgrown the limitations of traditional payment stacks and needed something that could handle global scale without buckling.

Since going public on Euronext Amsterdam in 2018, Adyen has grown into one of Europe's most valuable technology companies, with around 4,300 employees across 23 countries and net revenue of just under €2 billion in 2024. It remains headquartered in Amsterdam and consistently profitable — a combination that's rarer in fintech than it should be.

For businesses that treat payments as infrastructure rather than an afterthought, Adyen is the benchmark everything else gets measured against.

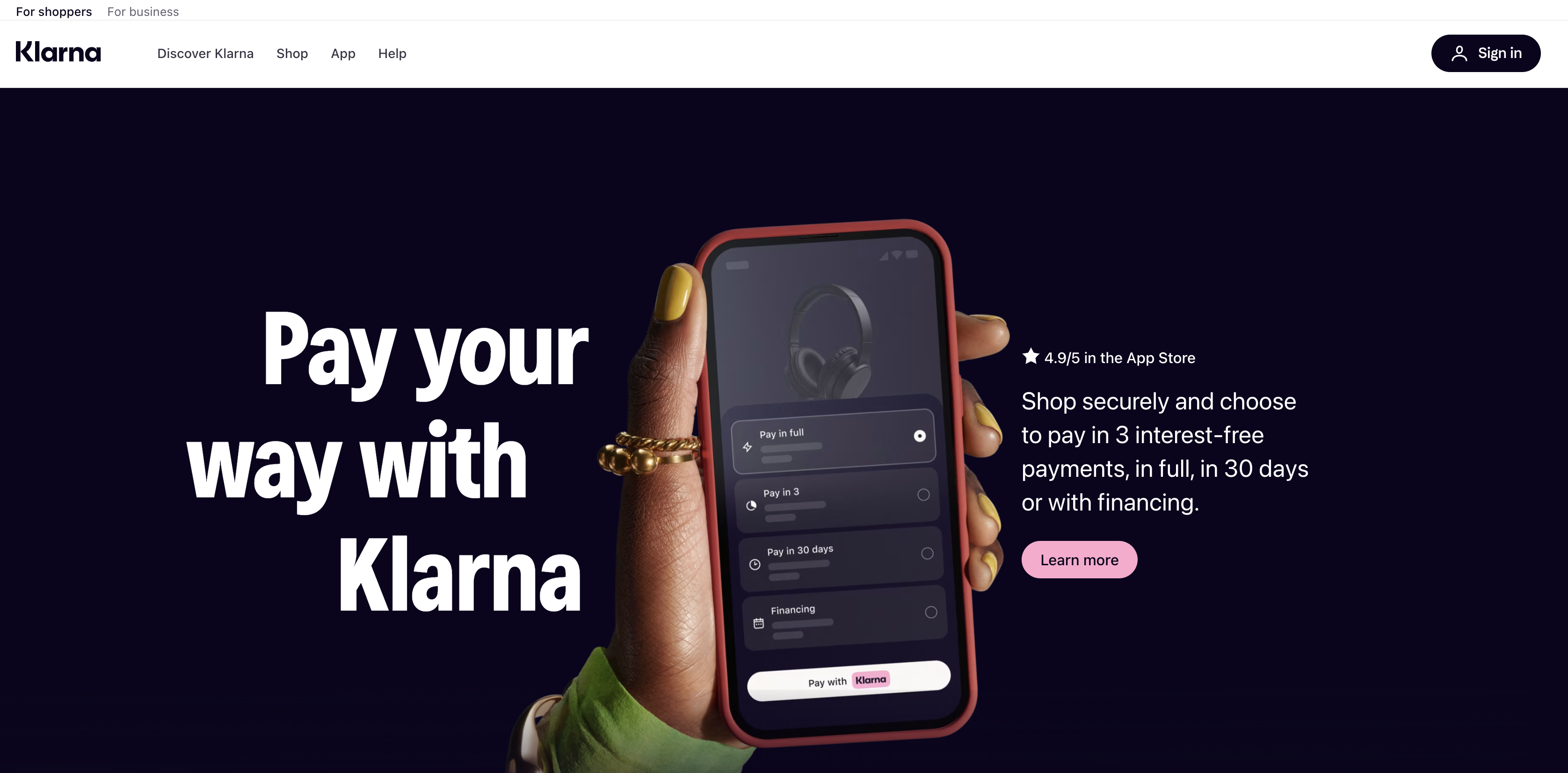

KlarnaFeatured

Embedded Finance🇸🇪 Sweden

Three Stockholm School of Economics students pitched an idea at a university entrepreneurship competition in 2005: let shoppers receive goods before they pay, and put the credit risk on the merchant side. The pitch finished last. They built it anyway.

Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson launched what was originally called Kreditor, later renamed Klarna, and spent the next two decades turning that rejected idea into one of Europe's most recognised fintech brands. The core insight held up: millions of people would rather split a purchase into three instalments than reach for a credit card, and merchants would pay for the privilege of offering that option because it reduces cart abandonment and increases average order values.

Klarna grew from a Swedish checkout button into something considerably more complex. It now holds a banking licence in Sweden, offers savings accounts, issues its own card, and operates across more than 45 markets with around 93 million active consumers and 675,000 merchant partners at the end of 2024. The US, which Klarna entered in 2015, has become its largest market by revenue, a fact the company underlined by listing on the New York Stock Exchange in September 2025 under the ticker KLAR, raising $1.37 billion at IPO.

The financial trajectory has been bumpy. Klarna reported net income of $21 million in 2024, a return to profitability after a bruising 2022 that included an 85% valuation cut and significant layoffs that reduced headcount from over 7,000 to around 3,400. What survived the restructuring was a leaner company with $2.81 billion in revenue and a clearer strategic direction: AI. Klarna's partnership with OpenAI produced a customer service assistant it claims handles the equivalent of 700 full-time agents, and generative AI now manages roughly two-thirds of customer chats.

The honest assessment of where Klarna sits today: it's no longer purely a BNPL provider and it's not quite a bank. It's somewhere in between, a consumer finance platform that knows more about your shopping behaviour than your bank does, and is betting that's worth a lot.

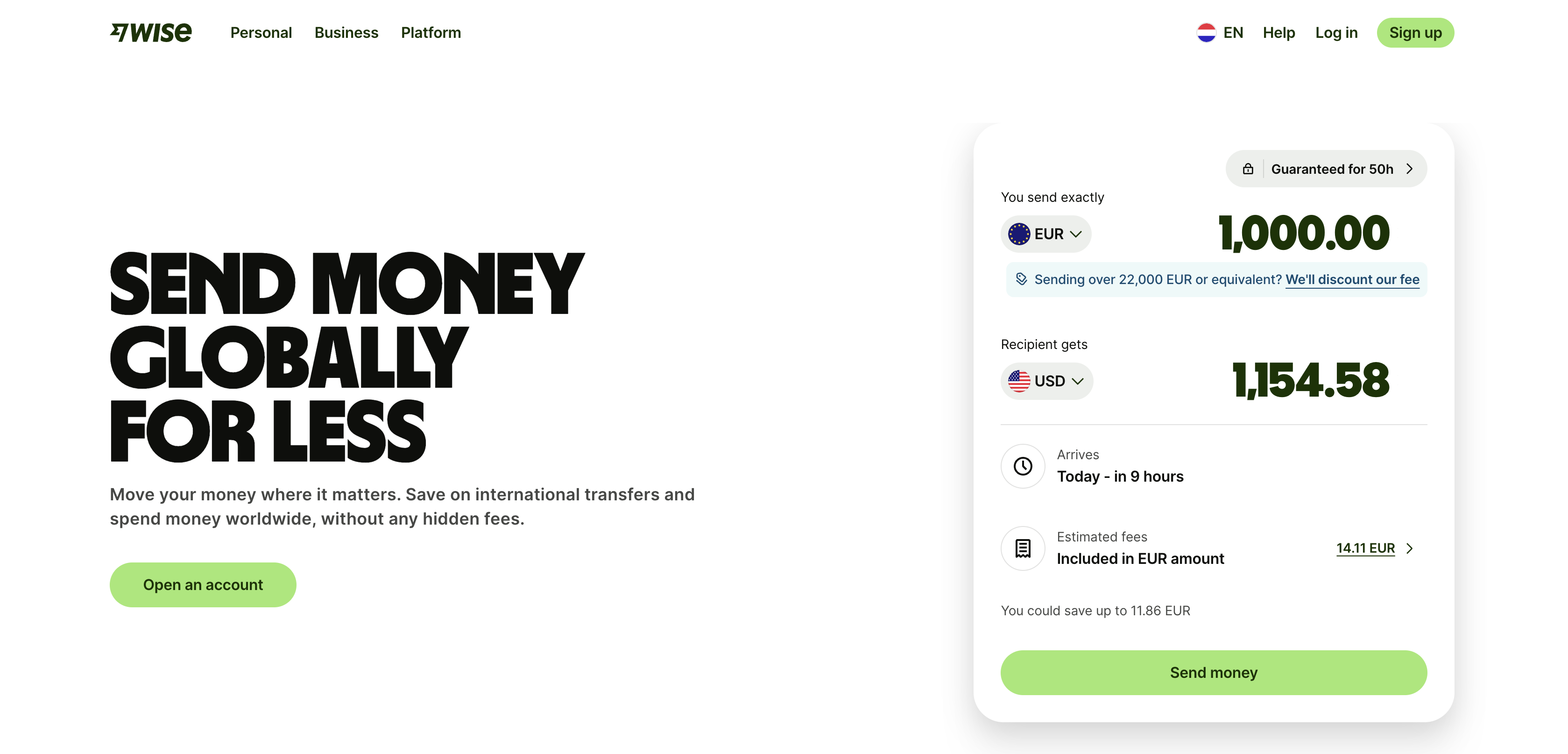

Wise

Payments🇬🇧 United Kingdom

Taavet Hinrikus had a problem that was embarrassingly simple to describe and maddeningly hard to solve. He was one of Skype's first employees, living in London and getting paid in euros while his bills were in pounds. Every month he was losing money to bank fees and exchange rate markups that his bank never disclosed upfront. Kristo Käärmann, a Deloitte consultant, had the same problem in reverse. In 2011 they sat down, compared rates, and started swapping money directly between each other's bank accounts — bypassing the banks entirely. Then they thought: what if anyone could do this?

That informal arrangement became TransferWise, launched in London in January 2011 with a straightforward promise that banks had been making impossible for decades: the real exchange rate, with fees shown upfront before you commit to a transfer. The early pitch was almost deliberately confrontational — the founders publicly compared bank exchange rate markups to theft, took out billboard ads outside banks, and built a campaign around showing customers exactly how much they were being overcharged. It worked.

TransferWise rebranded to Wise in 2021, the same year it listed directly on the London Stock Exchange — bypassing the traditional IPO process in a move consistent with a company that had spent a decade bypassing traditional financial processes. The listing valued the business at around £9 billion and gave it public-company discipline without the fanfare of a conventional float.

The product has expanded well beyond the original currency transfer use case. Wise now offers multi-currency accounts supporting over 40 currencies, a debit card, a business product for SMEs and freelancers managing cross-border payments, and a platform business that lets banks and other fintechs embed Wise's infrastructure into their own products. By June 2025, the platform had 15.6 million active customers processing £145 billion in cross-border volume annually — up 23% year on year. Revenue crossed £1 billion in 2024, with profit of £354 million.

The most significant recent development is structural: shareholders voted in July 2025 to move Wise's primary listing from London to a US exchange, with the transfer expected by early 2026. It's a pragmatic decision — the US is a large and growing market, the company has money-transmission licences in 48 states, and American institutional investors have historically valued fintech companies at higher multiples than London's market has.

Wise employs around 5,500 people and operates across more than 70 countries. Both founders remain involved — Käärmann as CEO, Hinrikus having stepped back from the board in recent years.

The core offer is deceptively simple. Wise operates its own network rather than renting access to SWIFT, which means it can cut out the middlemen taking cuts at every stage. You send pounds, it converts at the mid-market rate (the one you see on Google), and your recipient gets euros without the usual 3-5% tax that banks quietly extract. The company issues multi-currency accounts and cards that work globally, positioning itself as infrastructure for anyone whose life doesn't fit neatly into a single currency zone.

In the European market, Wise has become synonymous with cross-border reality. While traditional banks still talk about "international banking solutions," Wise customers are already sending money to fifteen countries from their phone without a second thought. The company went public in 2021, which paradoxically made it less of a fintech insurgent and more of an established player—but the underlying model hasn't changed: transparency and efficiency where opacity used to be profitable.

Wise represents a particular kind of fintech maturity: the startup that solved a specific, universal problem well enough that it became essential infrastructure for millions of people operating across borders. Its role in the European landscape is that of the pragmatist, proving that you don't need regulatory capture or cross-subsidization to build a sustainable business in payments.

N26Featured

Payments🇩🇪 Germany

Valentin Stalf and Maximilian Tayenthal were both Austrian, both based in Berlin, and both convinced in 2013 that retail banking was an unsolved problem disguised as a solved one. The branch network, the paper forms, the week-long account opening process — none of it was necessary. It was just the accumulated infrastructure of an industry that had never had to compete on user experience. They called their company Number26, after the number of cubes in a Rubik's cube, and set about building the bank they wished existed.

What launched in early 2015 was a current account with an app that didn't feel like it had been built by a committee of compliance officers. Real-time push notifications. A spending categorisation that actually worked. An account you could open in minutes on your phone. No branch visits, no signature cards, no waiting. N26 spread quickly across Germany and Austria, then into France, Spain, Italy, and eventually 24 European markets. At its 2021 peak, it was valued at $9 billion and widely cited as one of Europe's most important fintech companies.

The years since have been more complicated. Germany's financial regulator BaFin placed N26 under a customer growth cap from 2021, restricting new signups to 60,000 per month following concerns about anti-money laundering controls — a significant constraint for a company whose growth model depends on rapid user acquisition. In 2024, BaFin issued a €9.2 million fine for delayed suspicious transaction reports before lifting the growth cap entirely in June 2024 after N26 invested around €80 million overhauling its compliance infrastructure. The saga was expensive and reputationally bruising, but the outcome was a more robustly regulated company.

The financial trajectory since the cap was lifted has been encouraging. Revenue reached €440 million in 2024, up 40% year on year, and N26 recorded its first net-positive quarter in Q3 2024. Active customers reached 4.8 million by end of 2024. The product has expanded beyond basic current accounts into stock trading, ETFs, crypto via Bitpanda, and savings products — moves that increase revenue per user and reduce reliance on interchange fees.

The leadership picture changed substantially in late 2025. Stalf moved to the Supervisory Board in August, Tayenthal departed in December, and former UBS executive Mike Dargan was appointed CEO pending BaFin approval in April 2026. Both founders stepping back simultaneously — after more than a decade running the company they built — marks a genuine transition point, from founder-led startup to institutionally managed bank. Whether that changes the product culture is the question N26's 1,600 employees and 4.8 million customers are watching closely.

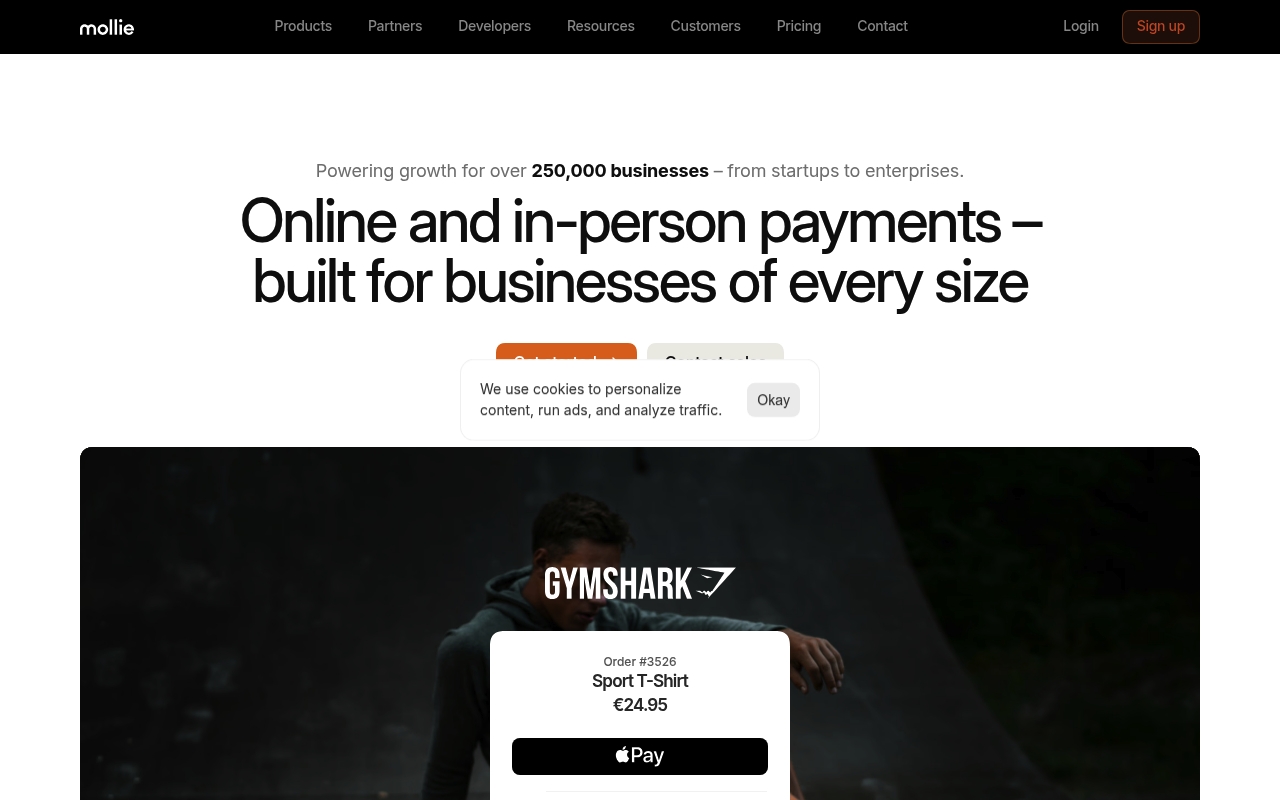

MollieFeatured

Financial Infrastructure🇳🇱 Netherlands

Adriaan Mol built Mollie's first backend while living with his parents in the Netherlands in 2004. No investors, no office, no team — just a founder and an idea that small businesses deserved a payment integration that didn't require a team of lawyers and a six-month setup process. He bootstrapped it for over fifteen years before taking outside funding in 2019. By then, Mollie had already grown into one of the most important payment platforms in European e-commerce, entirely on the back of a product that developers actually liked using.

The proposition is straightforward: one API, one dashboard, and access to the payment methods that actually matter across Europe. That means iDEAL in the Netherlands, Bancontact in Belgium, Klarna and SEPA Direct Debit everywhere, alongside cards, Apple Pay, and a growing list of local methods that would otherwise require separate integrations and separate acquirer relationships. Mollie handles the compliance, the fraud monitoring, and the settlement complexity. Merchants get a clean interface and a single invoice.

For the 250,000 businesses using Mollie today — ranging from Gymshark and Wild to local bakeries and market stalls, as CEO Koen Köppen regularly points out — the appeal is less about feature lists and more about what they don't have to think about. European payments are fragmented by design. Every country has its preferred methods, its own regulatory quirks, its own consumer habits. Mollie's job is to make that invisible.

The numbers from 2024 reflect a company that has found its model. Revenue reached €214 million, up 28% year on year, with gross profit growing 30% to €115 million and the company returning to positive EBITDA for the first time since 2018. Mollie raised a total of $940 million in funding and was valued at $6.5 billion following its 2021 Series C led by Blackstone.

The most significant recent development is the acquisition of GoCardless in December 2025 — bringing the UK-based direct debit specialist into the Mollie group and substantially expanding its recurring payments and bank transfer capabilities across Europe. Combined, the two companies cover a considerable share of European e-commerce payment infrastructure.

Mollie is still headquartered in Amsterdam, with around 900 employees across offices in Ghent, London, Lisbon, Munich, Milan, Paris, and beyond.

SumUp

Financial Infrastructure🇩🇪 Germany

SumUp is Europe's answer to the merchant services problem: a scrappy fintech that turned point-of-sale payments into something actually accessible. While legacy payment processors still treat small businesses like second-class customers, SumUp built hardware and software that work together seamlessly, letting anyone from a street vendor to a café owner accept cards in minutes, not months.

The company started by selling cheap card readers—simple, elegant devices that plugged into phones. But that was just the wedge. Today SumUp offers a stack: card readers, invoicing, basic accounting, and increasingly, working capital tools. It's the financial operating system for the SME who doesn't want to negotiate with a relationship manager.

What sets SumUp apart in Europe is its refusal to stay in the payments lane. Most competitors eventually build one feature and call it a day. SumUp keeps layering—acquiring merchant acquirer licenses, launching its own acquiring infrastructure in key markets, adding payment links and e-commerce solutions. The company operates across Western Europe and beyond, working with hundreds of thousands of merchants who are too small for traditional banking but too important to ignore.

SumUp represents the practical, unglamorous evolution of fintech: it's not trying to reinvent banking or blockchain. It's solving the cash flow problem for people who actually run businesses. That's a bigger opportunity than it sounds.

Payrexx

Embedded Finance🇨🇭 Switzerland

Payrexx is a Swiss payment processing platform that handles everything from card transactions to alternative payment methods through a single integration. Rather than juggling multiple providers, merchants get one dashboard, one API, and unified reporting—clean and straightforward.

The company built its infrastructure to serve small and medium-sized businesses across Europe who found traditional acquiring fragmented and expensive. Payrexx bundles payment gateway, merchant acquiring, and checkout orchestration into a single stack, letting SMEs accept payments without becoming payment infrastructure experts.

What separates Payrexx is its positioning as the pragmatic middle ground. It's not a heavyweight enterprise solution requiring months of integration, nor is it a bare-bones commodity service. The platform emphasizes ease of use alongside robust features—white-label checkout pages, recurring billing, instant settlement options, and granular reporting that actually tells you something useful about your business.

In the crowded European payments landscape, Payrexx occupies the space where regulation meets accessibility. It holds full payment institution licensing across multiple jurisdictions, meaning merchants don't have to worry about compliance theater. For growing businesses tired of piecing together payment solutions, Payrexx represents consolidation without compromise.

Computop

Financial Infrastructure🇩🇪 Germany

Computop is a German payment processor that handles the unglamorous but essential work of moving money across borders and payment systems for enterprises. The company sits at the infrastructure layer, offering payment gateway services, card processing, and merchant acquiring solutions to retailers, fintechs, and financial institutions across Europe and beyond. Rather than chasing consumer attention, Computop focuses on the operational backbone—enabling businesses to accept payments in multiple currencies, manage risk, and comply with shifting regulations without rebuilding their entire tech stack. It's the kind of company most consumers never hear about, but whose software touches thousands of transactions daily. In a market crowded with flashy payment startups, Computop represents the older, less visible tradition of fintech: solving concrete problems for enterprises at scale. The company's strength lies in its ability to integrate with existing banking and e-commerce systems rather than replacing them, making it a pragmatic choice for companies that value stability over disruption.

Paysera

Financial Infrastructure🇱🇹 Lithuania

Paysera is a Lithuanian fintech company that has quietly built one of Europe's most comprehensive payment and banking platforms, serving millions of users across the continent. Rather than chasing hype, Paysera focuses on practical utility—combining payment processing, digital accounts, currency exchange, and invoicing tools into a single interface that works across borders and languages. The platform powers everything from freelancers managing invoices to SMEs handling payroll, while also offering consumer-facing services like multi-currency wallets and competitive exchange rates. What sets Paysera apart is its unglamorous pragmatism: it solves real friction in how Europeans move, spend, and manage money across different countries, without the startup theatrics. It's the kind of company that doesn't dominate headlines but has become indispensable infrastructure for a significant portion of the continent's digital economy. In the crowded European fintech landscape, where newer players chase consumer attention and legacy banks chase compliance, Paysera operates in the profitable middle—trusted by businesses and individuals who value reliability and cross-border simplicity over brand prestige.