91 companies

SumUp

Financial Infrastructure🇩🇪 Germany

SumUp is Europe's answer to the merchant services problem: a scrappy fintech that turned point-of-sale payments into something actually accessible. While legacy payment processors still treat small businesses like second-class customers, SumUp built hardware and software that work together seamlessly, letting anyone from a street vendor to a café owner accept cards in minutes, not months.

The company started by selling cheap card readers—simple, elegant devices that plugged into phones. But that was just the wedge. Today SumUp offers a stack: card readers, invoicing, basic accounting, and increasingly, working capital tools. It's the financial operating system for the SME who doesn't want to negotiate with a relationship manager.

What sets SumUp apart in Europe is its refusal to stay in the payments lane. Most competitors eventually build one feature and call it a day. SumUp keeps layering—acquiring merchant acquirer licenses, launching its own acquiring infrastructure in key markets, adding payment links and e-commerce solutions. The company operates across Western Europe and beyond, working with hundreds of thousands of merchants who are too small for traditional banking but too important to ignore.

SumUp represents the practical, unglamorous evolution of fintech: it's not trying to reinvent banking or blockchain. It's solving the cash flow problem for people who actually run businesses. That's a bigger opportunity than it sounds.

Starling Bank

Digital Banking🇬🇧 United Kingdom

Starling Bank is a British challenger bank that stripped away the friction of traditional banking and rebuilt it around what modern customers actually need: instant notifications, real-time spending insights, and accounts you can open in minutes without stepping into a branch. Founded in 2014, it operates as a fully regulated bank with its own banking license, not just a wrapper around legacy infrastructure.

The platform serves both consumers and SMEs, offering straightforward current accounts, savings pots, and increasingly sophisticated business banking tools. Unlike neobanks reliant on partnerships, Starling owns its core infrastructure, which means faster iteration and tighter product control. The company has built a reputation for no-nonsense transparency: no hidden fees, no overdraft tricks, and clear communication about what you're getting.

In the crowded UK digital banking space, Starling stands apart through consistent execution and a focus on solving real problems rather than chasing hype. It's profitable, self-sufficient, and treated by legacy banks as a genuine competitor rather than a novelty. For European fintechs, Starling represents the successful blueprint: regulated, capital-efficient, and genuinely preferred by millions of users who value simplicity over flashiness.

As the fintech landscape matures, Starling exemplifies the shift from disruption theater to sustainable banking infrastructure—a reminder that the most radical innovation often looks deceptively simple.

Indy

Digital Banking🇫🇷 France

Indy is a French fintech built for freelancers and self-employed workers who are tired of juggling accounting software, invoicing tools, and bank dashboards across a dozen different apps. The platform consolidates business banking, invoicing, expense tracking, and tax compliance into a single workspace designed specifically for French independent professionals and micro-entrepreneurs.

Unlike traditional accounting software that feels built for accountants, Indy puts the solopreneur first—automating routine tasks like categorizing expenses and calculating quarterly tax estimates while keeping the interface clean and approachable.

The company has become a go-to solution across France for freelancers managing both the creative and administrative sides of their business, from photographers to consultants to digital agencies. It's one of Europe's clearest examples of how fintech can solve a specific, underserved market by building exactly what that market actually needs rather than trying to be everything to everyone. In a landscape crowded with generic SME finance platforms, Indy's laser focus on French self-employed workers—and their particular regulatory requirements and pain points—has established it as a cultural fixture in the French freelance community.

Billie

Lending🇩🇪 Germany

Billie is a B2B payments platform built for small businesses and freelancers who are tired of chasing invoices. Instead of waiting 30, 60, or 90 days to get paid, users can access their outstanding invoices instantly through Billie's platform, converting them into immediate working capital without the traditional loan machinery.

The service works like this: businesses upload their invoices, Billie validates them, and funds arrive within hours. It's not a loan in the conventional sense—there's no credit scoring, no months of approval waiting, just a straightforward advance against money that's already owed. The economics are transparent: a small fee on the advance, nothing else.

Billie positions itself against the backdrop of Europe's slow payment culture, where SMEs are routinely starved of cash flow by larger clients who take their time settling bills. While traditional banks offer supply chain financing to enterprises, Billie democratizes this for the mid-market and smaller players who have real invoices but zero patience for bureaucracy.

In the broader fintech landscape, Billie sits at the intersection of lending, payments, and working capital—essentially making invoice financing frictionless for businesses that actually need it.

SeedLegals

RegTech🇬🇧 United Kingdom

Legal documents are one of the largest hidden costs of running a startup. Founders spend tens of thousands of pounds with law firms producing the term sheets, shareholder agreements, employee option schemes, and funding round paperwork that every growing company needs but few founders understand well enough to procure efficiently. SeedLegals was founded in London in 2016 to bring that legal infrastructure online. Its platform automates the creation of startup legal documents — fundraising agreements, employee equity, board resolutions, EMI option schemes — through a guided interface that produces lawyer-quality documents in hours rather than weeks, at a fraction of the cost. The product is grounded in genuine legal expertise — SeedLegals works with law firms and corporate lawyers to ensure the documents it produces meet the standards of the funds and investors that ultimately need to sign them. SeedLegals has become deeply embedded in the UK startup ecosystem, processing a significant share of EIS and SEIS funding rounds and supporting thousands of UK companies through their early-stage equity events. In the European startup infrastructure landscape, where regulatory and legal complexity varies significantly between markets, SeedLegals' UK depth represents the most mature example of legal automation for early-stage companies — a model that is gradually expanding to other European jurisdictions.

Capdesk

Capital Markets🇬🇧 United Kingdom

Equity management for private companies has historically been a mess of spreadsheets, lawyer markup, and reconciliation errors that compound silently until a fundraising round forces everyone to discover that the cap table reality differs from the cap table on file. Capdesk was founded in Copenhagen and grew up in London from 2015, building equity management software for private companies — a single source of truth for share allocations, option grants, vesting schedules, and shareholder communications. The product targets the gap between an Excel spreadsheet and a full-blown share registry: too small for the latter, too important to entrust to the former. Capdesk has built a strong client base across UK and European startups and scaleups, becoming one of the more trusted equity management platforms in Europe. The company was acquired by US-based Carta in 2023, consolidating the European equity management market under the umbrella of one of its largest global players. The acquisition reflects a broader pattern in private market infrastructure — the platforms that manage equity, fundraising, and investor relations are consolidating around a small number of comprehensive solutions. For European companies that built on Capdesk, the Carta acquisition brings them into a global platform with broader functionality at the cost of the local independence that some clients valued.

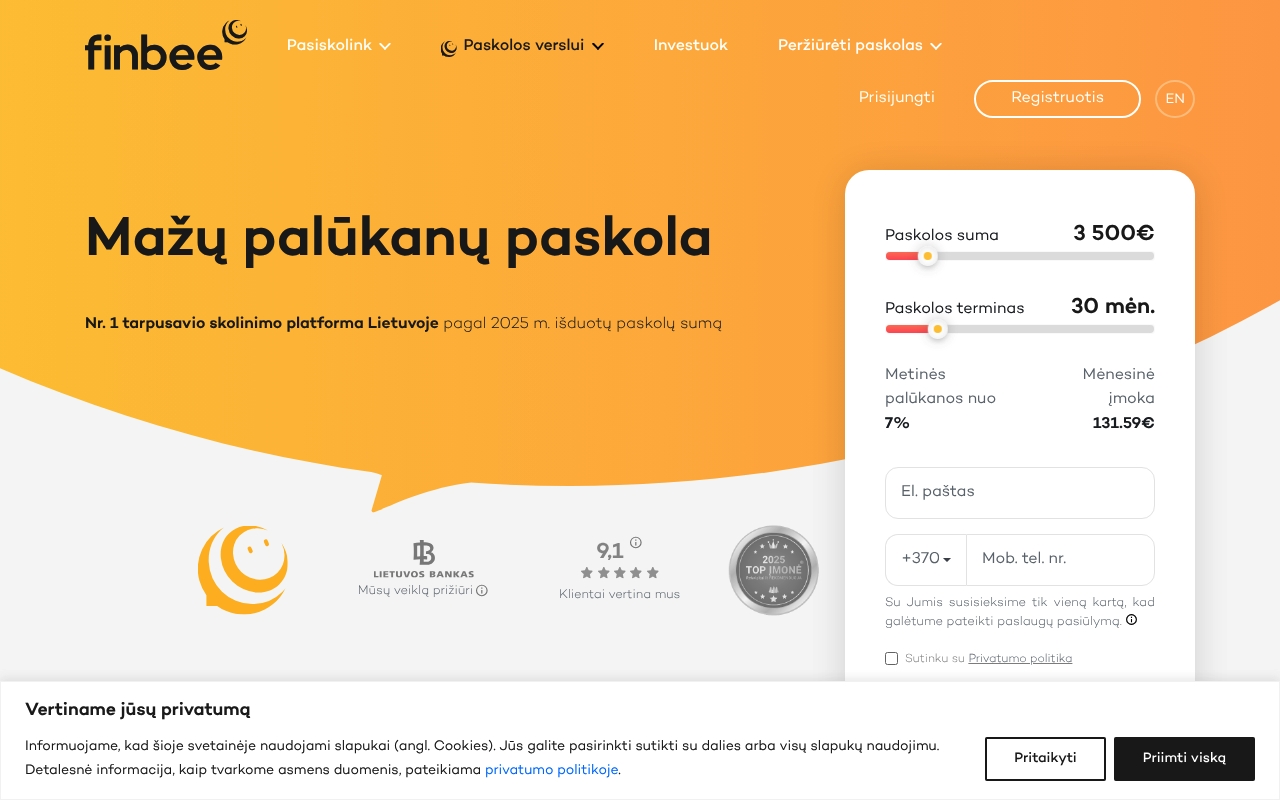

Finbee

Lending🇱🇹 Lithuania

Peer-to-peer business lending — connecting retail investors with creditworthy small businesses needing growth or working capital — represents a category within marketplace lending where the underwriting complexity is greater than consumer P2P but the credit characteristics are different. Finbee was founded in Vilnius in 2015 to build a Lithuanian platform offering both consumer and business P2P lending products, with an underwriting infrastructure designed to evaluate the specific risk characteristics of Lithuanian SMEs alongside individual borrowers. The platform has built a substantial domestic position in the Lithuanian marketplace lending segment, attracting both local and Pan-European investors looking for exposure to Lithuanian credit. Finbee's product range and operational depth reflect a decade of operating in a market that has been one of Europe's more active testbeds for P2P lending innovation — with multiple platforms, supportive regulation, and a retail investor base willing to engage with marketplace lending products. In the Baltic alternative lending landscape, Finbee represents the category of platform that has built durability through diversified product offerings and disciplined underwriting rather than aggressive growth — a positioning that has aged better than some of the more growth-focused models that dominated the early P2P era.

Finloup

Financial Infrastructure🇬🇷 Greece

Finloup is a European lending infrastructure platform that helps financial institutions and fintechs automate credit decisions and manage loan portfolios at scale. The company builds white-label software that sits between lenders and borrowers, handling everything from application to origination to ongoing portfolio management. Rather than reinventing the wheel for each lender, Finloup abstracts away the operational complexity of modern lending—think of it as the backstage machinery that lets banks and fintech lenders focus on distribution and customer experience instead of building lending systems from scratch. The platform works across consumer and SME lending, serving institutions across multiple European markets who need faster, smarter, more compliant ways to originate and manage credit. Where traditional core banking systems move slowly and cost millions to customize, Finloup offers speed and flexibility. It's built for a market where fintech lending has exploded but the infrastructure hasn't kept pace with demand. The company essentially democratizes access to institutional-grade lending technology, lowering the barriers for smaller players to compete with incumbents. Within the broader fintech ecosystem, Finloup represents a critical infrastructure layer—the unsexy but essential plumbing that makes modern lending possible at European scale.

Paysera

Financial Infrastructure🇱🇹 Lithuania

Paysera is a Lithuanian fintech company that has quietly built one of Europe's most comprehensive payment and banking platforms, serving millions of users across the continent. Rather than chasing hype, Paysera focuses on practical utility—combining payment processing, digital accounts, currency exchange, and invoicing tools into a single interface that works across borders and languages. The platform powers everything from freelancers managing invoices to SMEs handling payroll, while also offering consumer-facing services like multi-currency wallets and competitive exchange rates. What sets Paysera apart is its unglamorous pragmatism: it solves real friction in how Europeans move, spend, and manage money across different countries, without the startup theatrics. It's the kind of company that doesn't dominate headlines but has become indispensable infrastructure for a significant portion of the continent's digital economy. In the crowded European fintech landscape, where newer players chase consumer attention and legacy banks chase compliance, Paysera operates in the profitable middle—trusted by businesses and individuals who value reliability and cross-border simplicity over brand prestige.

Roger

Payments🇵🇱 Poland

Roger is a Polish fintech that strips away the friction from business payments. The platform lets SMEs and larger companies manage invoices, payroll, and cross-border transfers from a single dashboard, built on the conviction that corporate banking needn't be byzantine. Rather than forcing businesses through legacy bank portals, Roger delivers everything via mobile app and web interface—think Wise for corporate operations, but integrated with accounting systems and designed for the realities of mid-market firms. The company has built its reputation on speed and transparency, particularly around FX costs that traditional banks obscure. Roger handles both domestic and international payments with a focus on reducing the overhead that eats into margins. Positioned squarely in the European corridor where businesses actually move money, Roger competes by making the whole experience feel native and built for 2024, not inherited from 2004. Within the broader fintech landscape, Roger represents the quiet revolution of infrastructure modernization—not blockchain theatrics or retail disruption, but the unglamorous work of rebuilding how companies pay each other.