20 companies

Additiv

Treasury🇨🇭 Switzerland

Additiv is a treasury and cash management platform built for the modern corporate finance team. It sits at the intersection of spreadsheets and enterprise software—companies spend billions managing liquidity across multiple banks, currencies, and counterparties, yet most still rely on fragmented manual processes. Additiv replaces that chaos with a unified workspace where teams can forecast cash flows, manage payments, and monitor FX exposure in real time.

The platform connects directly to a company's banking infrastructure, pulling live transaction data and balances across all their accounts. From there, teams can model scenarios, automate routine reconciliation, and execute payments without context-switching between tools. It's designed for finance managers and treasurers who've outgrown spreadsheets but don't want the bloat of legacy treasury systems.

In a market dominated by legacy players like Kyriba and FIS, Additiv positions itself as the cloud-native alternative—faster to implement, easier to use, and built for companies that actually want to control their cash position rather than just report on it. The company sits squarely in the corporate finance modernization wave that's reshaping how mid-market and enterprise companies think about liquidity. Unlike niche point solutions, Additiv attempts to be comprehensive enough to replace multiple tools while remaining nimble and intuitive.

Roger

Payments🇵🇱 Poland

Roger is a Polish fintech that strips away the friction from business payments. The platform lets SMEs and larger companies manage invoices, payroll, and cross-border transfers from a single dashboard, built on the conviction that corporate banking needn't be byzantine. Rather than forcing businesses through legacy bank portals, Roger delivers everything via mobile app and web interface—think Wise for corporate operations, but integrated with accounting systems and designed for the realities of mid-market firms. The company has built its reputation on speed and transparency, particularly around FX costs that traditional banks obscure. Roger handles both domestic and international payments with a focus on reducing the overhead that eats into margins. Positioned squarely in the European corridor where businesses actually move money, Roger competes by making the whole experience feel native and built for 2024, not inherited from 2004. Within the broader fintech landscape, Roger represents the quiet revolution of infrastructure modernization—not blockchain theatrics or retail disruption, but the unglamorous work of rebuilding how companies pay each other.

Finastra

Financial Infrastructure🇬🇧 United Kingdom

Finastra is a London-based financial software giant that powers the plumbing behind modern finance. Rather than chasing consumers with flashy apps, Finastra builds the invisible infrastructure that banks, investment firms, and capital markets players depend on to operate. Think of it as the operating system for institutional finance—the sort of company most people have never heard of but whose systems process trillions in transactions daily.

The company's portfolio spans core banking systems, treasury management platforms, capital markets solutions, and lending technology. Finastra operates at the intersection of legacy finance and digital transformation, helping traditional institutions modernize their backend without scrapping decades of accumulated complexity. For banks and brokers, Finastra's software is often indispensable—the kind of vendor you can't easily replace once integrated into your operations.

In the European market, Finastra competes with other heavyweight infrastructure players but stands out for its broad coverage across retail, corporate, and capital markets segments. The company has grown partly through acquisition, absorbing competitors and bolt-on technologies to expand its ecosystem. It's not the startup disrupting finance from the margins; it's the entrenched platform that established institutions lean on to survive and scale.

Ebury

Payments🇬🇧 United Kingdom

Ebury is a London-based fintech that's quietly become one of Europe's most ambitious cross-border payment platforms for small and mid-sized businesses. Built for founders and finance teams who spend too much time juggling currency conversions, hedging risk, and waiting days for international transfers, Ebury strips away the friction that traditional banks left behind.

The platform handles the full spectrum of what mid-market companies actually need: sending money across borders at better rates, managing foreign exchange exposure without needing a treasury team, collecting payments in dozens of currencies, and—increasingly—accessing working capital tied to those flows. It's not a flashy consumer app; it's infrastructure that makes international growth less exhausting.

Unlike the volume-chasing payment processors or the idealistic startups that oversimplified cross-border payments, Ebury positioned itself as the pragmatic middle ground. It embedded deep relationships with regional banks while building technology that works at scale. The company has expanded beyond its British roots into major European markets, growing a client base that ranges from e-commerce sellers to manufacturing firms that actually need sophisticated FX management, not just cheaper wires.

Ebury represents a maturing fintech category: the infrastructure play that's neither a bank nor a simple API, but rather a new kind of financial operating system for companies doing serious international business.

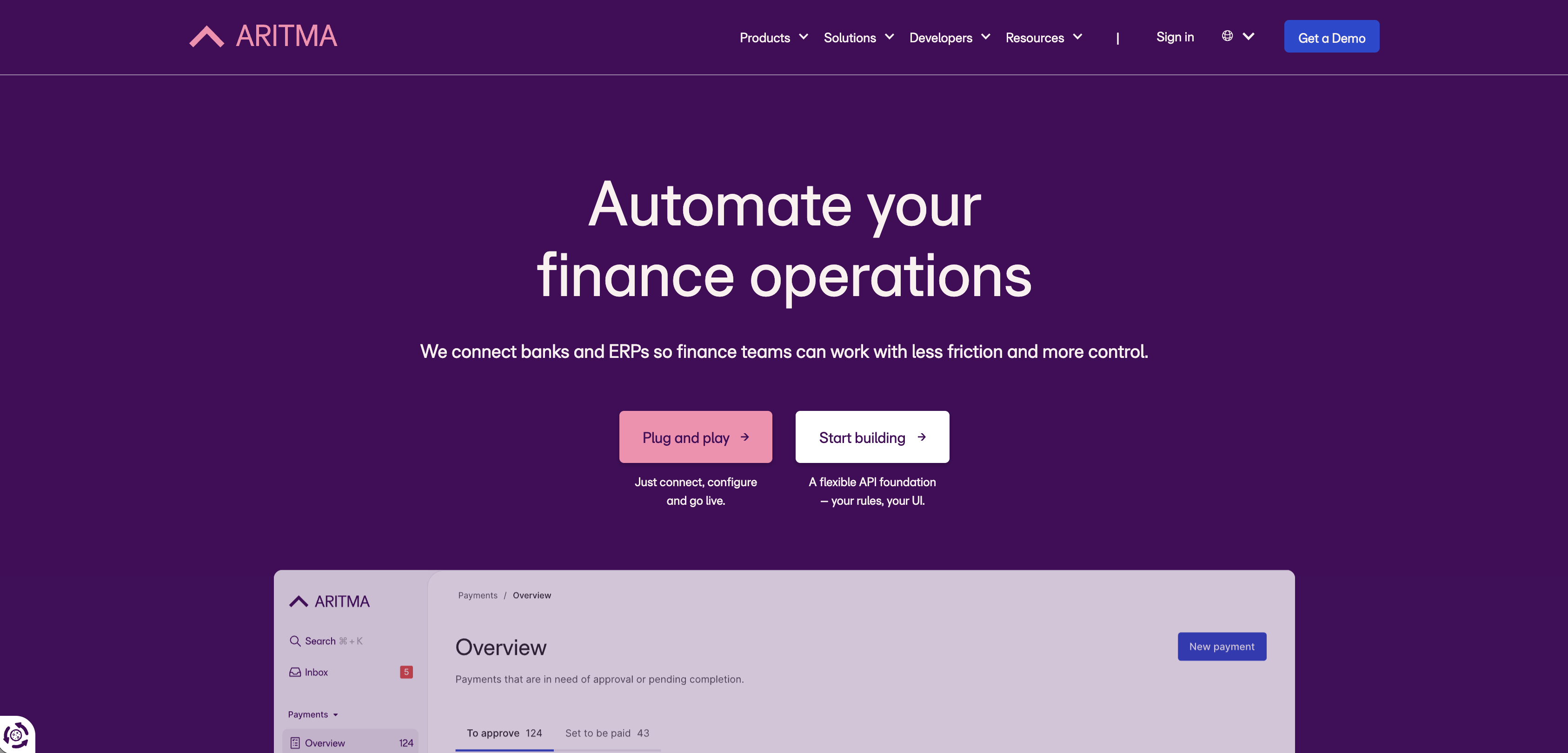

Aritma

Payments🇳🇴 Norway

Aritma is building the financial operating system for businesses that want to move beyond spreadsheets and legacy banking infrastructure. The platform consolidates cash management, payments, and accounting into a single workspace, letting companies see their full financial picture in real time rather than waiting for bank statements and reconciliation cycles. It's built for the EU market, where fragmented banking, multiple currencies, and regulatory complexity make finance operations unnecessarily complicated for growing businesses.

Instead of bolting together payment platforms, banking apps, and accounting tools, Aritma unifies them—automating reconciliation, tracking cash movements across accounts and currencies, and embedding compliance workflows from the start. The result feels less like traditional treasury software and more like financial infrastructure for the internet era: API-first, collaborative, and designed for businesses that actually move fast.

Most corporate finance tools are built for big enterprises with dedicated CFO teams and legacy bank relationships. Aritma positions itself as the alternative for mid-market and high-growth companies that need institutional financial controls without the institutional overhead. It's part of a broader shift toward embedded finance operations—the idea that cash management and payments shouldn't feel like a separate department, but integrated into how companies actually work.

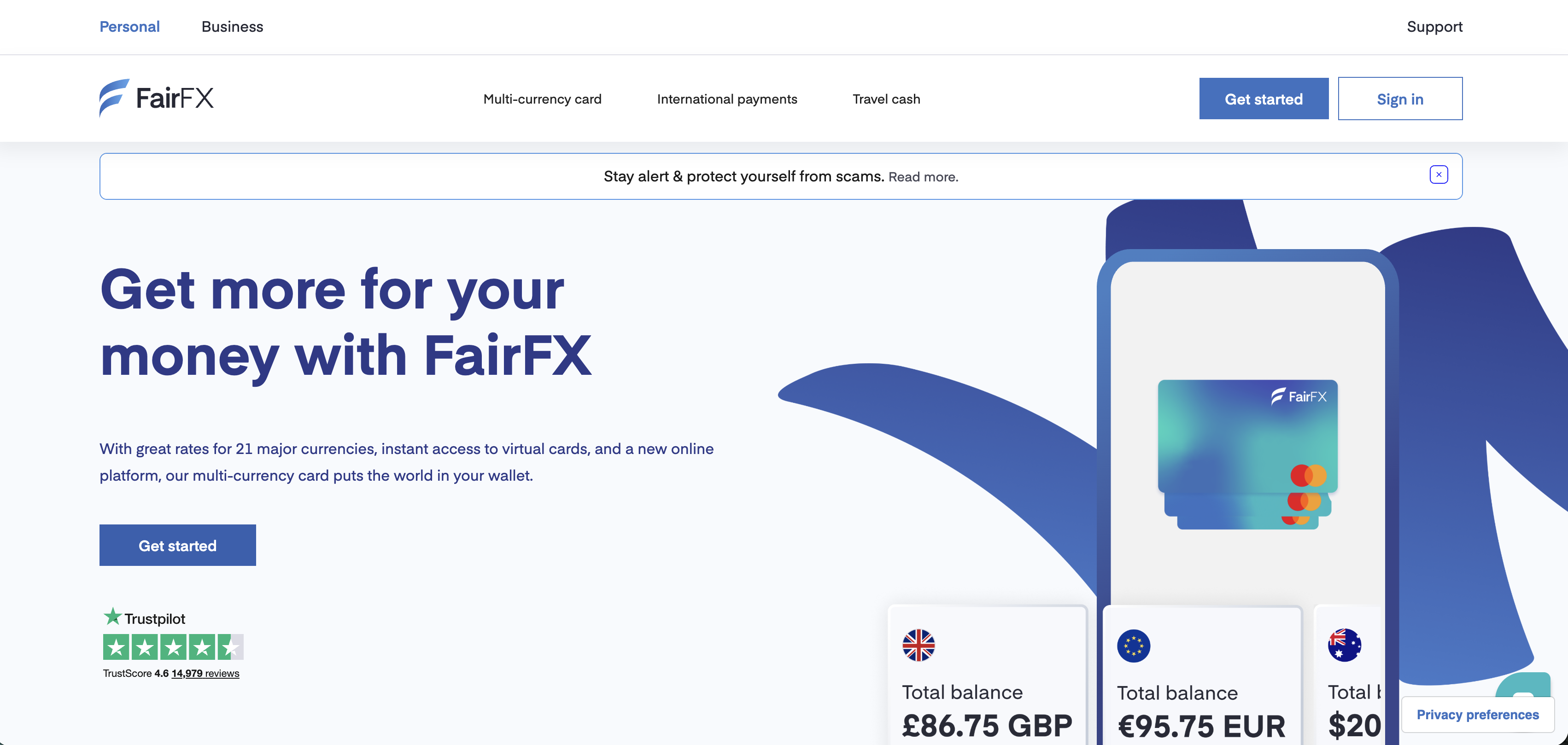

FairFX

Payments🇬🇧 United Kingdom

International money transfers and travel money used to be one of the most opaque and most expensive parts of consumer banking — bank exchange rates that included undisclosed margins, fees layered on fees, and a deliberate obscurity about how much consumers were actually paying to convert one currency to another. FairFX was founded in London in 2007 to bring transparency and competitive pricing to that market. Its multi-currency prepaid card and money transfer service let consumers and businesses lock in exchange rates and access foreign currency at significantly better rates than high street banks offered. The company expanded across consumer and business segments, building a particular following among UK consumers travelling internationally and SMEs making cross-border payments. FairFX became part of Equals Group, broadening into a wider international payments and corporate FX platform serving both retail and B2B customers. In the European consumer FX market, where Wise and Revolut have built dominant positions through better products and clearer pricing, FairFX represented an earlier wave of disruption — companies that proved consumers would switch from banks for FX if the alternative was meaningfully better. That proof of concept paved the way for the larger fintechs that followed.

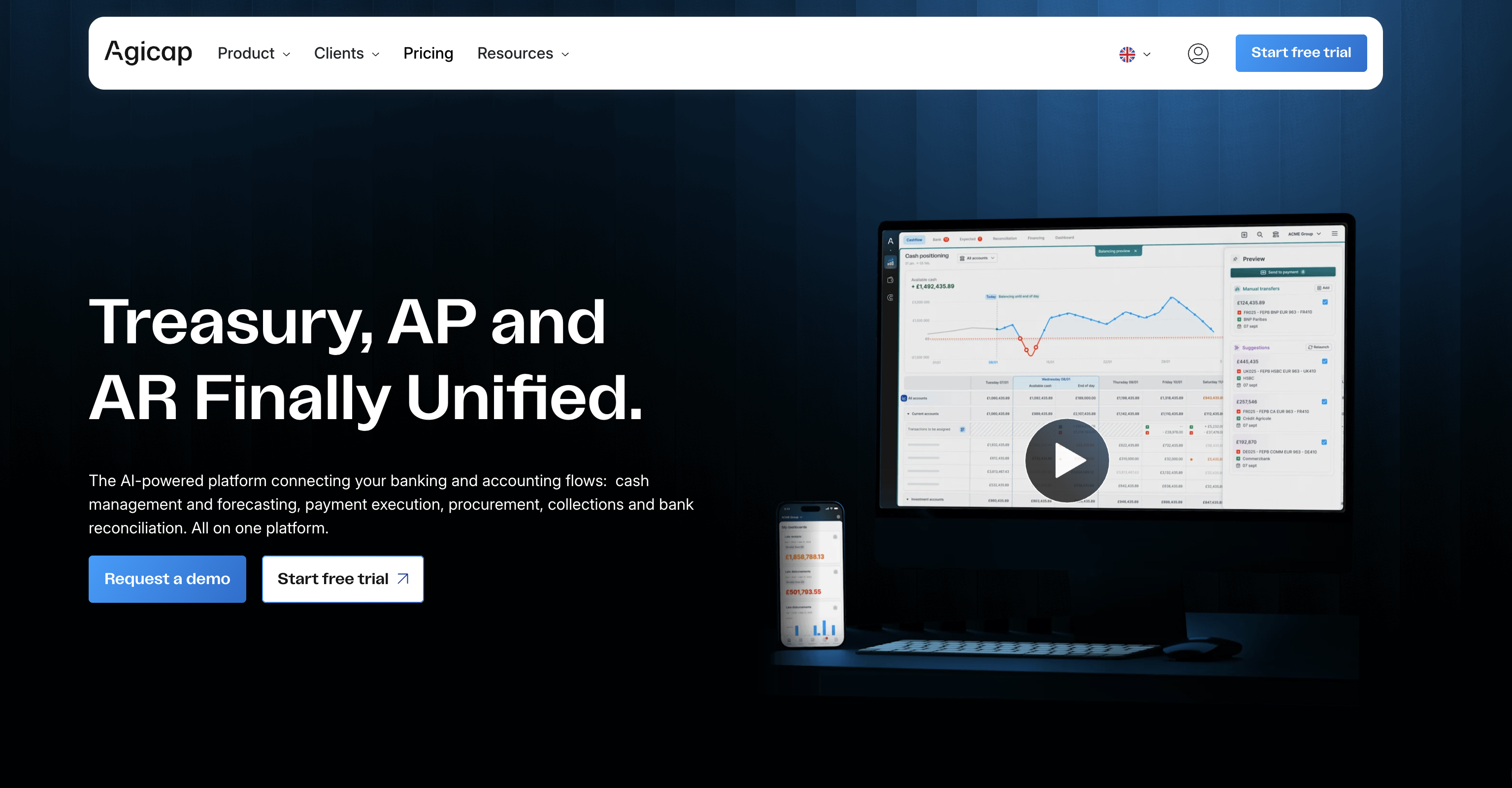

Agicap

SME Finance🇫🇷 France

Cash flow forecasting for mid-market companies is a constant headache. Finance teams spend weeks building Excel models, updating bank balances by hand, and scrambling when surprises hit. Agicap strips away the manual drudgery with a platform that pulls real-time bank data, forecasts cash positions, and alerts teams to shortfalls before they become crises.

The platform connects directly to corporate bank accounts across Europe, aggregating transactions and balances in a single dashboard. Finance teams can forecast weeks or months ahead, model different scenarios, and plan borrowing or investment with confidence. It's built for the CFO or finance manager at a growing company—someone managing millions but not yet running a treasury department.

In a crowded space of cash management tools, Agicap distinguishes itself through simplicity and breadth of bank connectivity. Where some competitors focus on large enterprises or niche workflows, Agicap targets the mid-market sweet spot: companies that have outgrown spreadsheets but aren't yet ready to deploy enterprise software. The platform's strength lies in its ease of setup and integration with French, German, and UK banking networks.

Agicap sits at the intersection of SME finance and treasury, filling a gap for companies that need working capital visibility without the complexity or cost of traditional corporate treasury platforms.

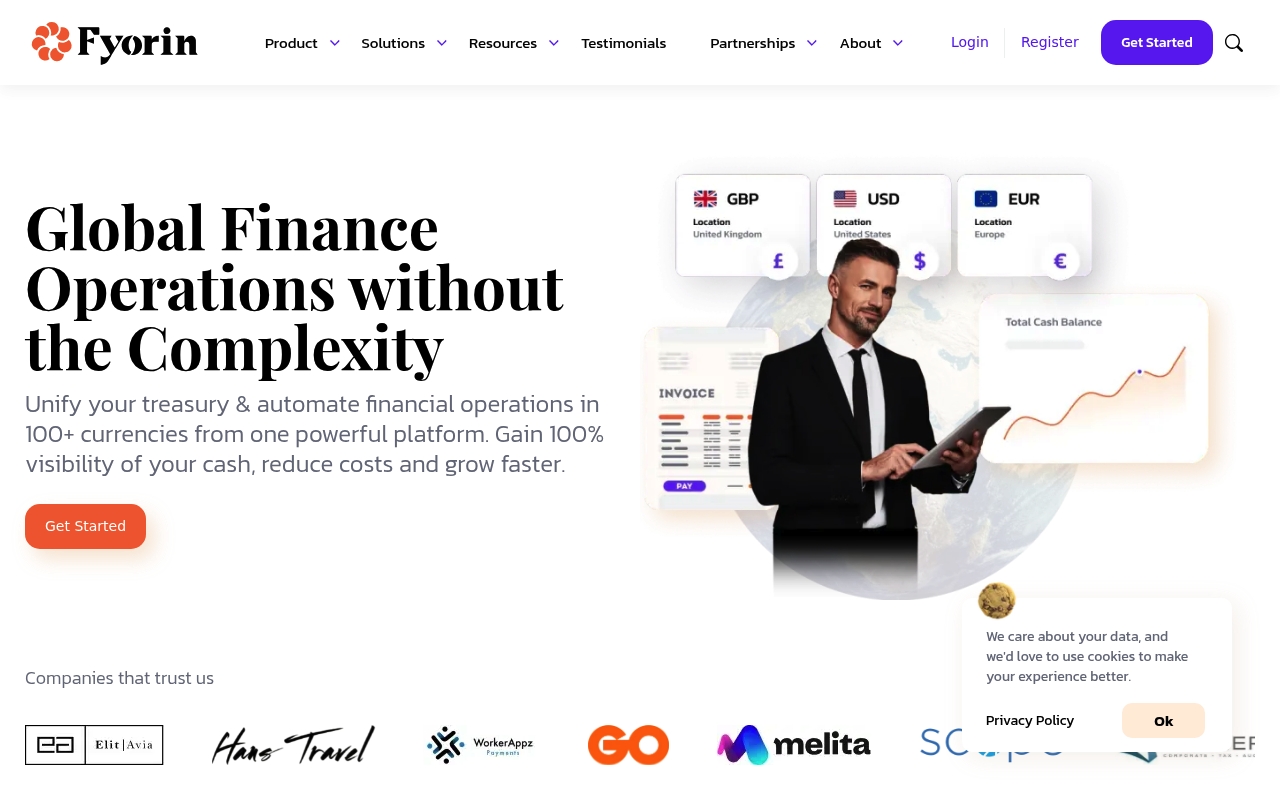

Fyorin

Financial Infrastructure🇲🇹 Malta

Fyorin is a European treasury and payments platform built for the modern corporate finance team. It bundles cash management, FX execution, and liquidity forecasting into a single interface—stripping away the complexity that haunts traditional treasury software. The platform connects directly to your banks and accounting systems, giving finance teams real-time visibility into cash positions across multiple accounts and currencies. Unlike legacy solutions that require armies of integrators and months of implementation, Fyorin is designed for immediate deployment, letting companies start optimizing cash flow within weeks rather than years. It appeals to mid-market and enterprise finance teams tired of spreadsheet-driven processes and fragmented point solutions. Fyorin sits squarely in the gap between enterprise banking software and modern fintech: it's professional enough for serious corporate finance, but built with the simplicity and speed that modern teams expect. The platform is particularly valuable for companies with multi-currency exposure or complex banking relationships, where manual cash management becomes a real drag on working capital efficiency. In a market crowded with legacy treasury vendors, Fyorin represents a cleaner, faster alternative that doesn't ask you to overhaul your entire finance stack.

ION Group

Financial Infrastructure🇬🇧 United Kingdom

ION Group is a sprawling financial software empire that has quietly become one of Europe's most comprehensive infrastructure plays. The company operates across trading, risk management, and post-trade processing—the unsexy but absolutely critical backbone that powers global capital markets. Unlike flashy fintech startups chasing consumer adoption, ION builds the invisible plumbing that institutional traders, hedge funds, and investment banks depend on every single day. Its portfolio spans front-office platforms, market data aggregation, clearing and settlement systems, and regulatory reporting tools. ION serves as a counterweight to the purely consumer-focused fintech narrative, proving there's enormous value in solving problems for professionals who move billions. The company's strength lies in its ability to connect disparate financial systems, providing what amounts to a unified operating system for institutional finance. For European financial institutions, ION represents a trusted partner in an increasingly complex regulatory landscape, offering solutions that integrate seamlessly with legacy infrastructure while modernizing workflows. Its acquisition-driven growth strategy—picking up niche specialists and consolidating them into a cohesive platform—mirrors the broader consolidation happening across enterprise fintech. ION's market position underscores a fundamental truth about fintech: the biggest opportunities often lie in B2B infrastructure rather than consumer apps.

Ophen Technologies

SME Finance🇩🇪 Germany

Most corporate treasuries are still wrestling with spreadsheets and manual workflows when it comes to managing liquidity and FX exposure. Ophen Technologies reimagines treasury management for mid-market companies by building a unified platform that turns fragmented banking relationships into a single source of truth. The platform aggregates real-time cash positions across multiple banks, surfaces FX exposure, and automates the mechanics of moving money and hedging risk. It sits between a company's existing bank accounts and ERP systems, orchestrating what should be simple but somehow remains chaotic. What sets Ophen apart is its refusal to force clients into rip-and-replace dynamics. Instead, it works with existing infrastructure, meaning finance teams get immediate value without betting the company on a migration. The platform speaks the language of CFOs and controllers, not engineers, which matters when the problem you're solving is as mission-critical as knowing where your cash actually is. In a market where treasury tech tends toward either complexity or oversimplification, Ophen occupies a pragmatic middle ground. For European mid-market companies managing multi-currency operations and the complexity that comes with it, the platform addresses a genuine pain point that traditional banking and generic ERP modules have consistently underserved.