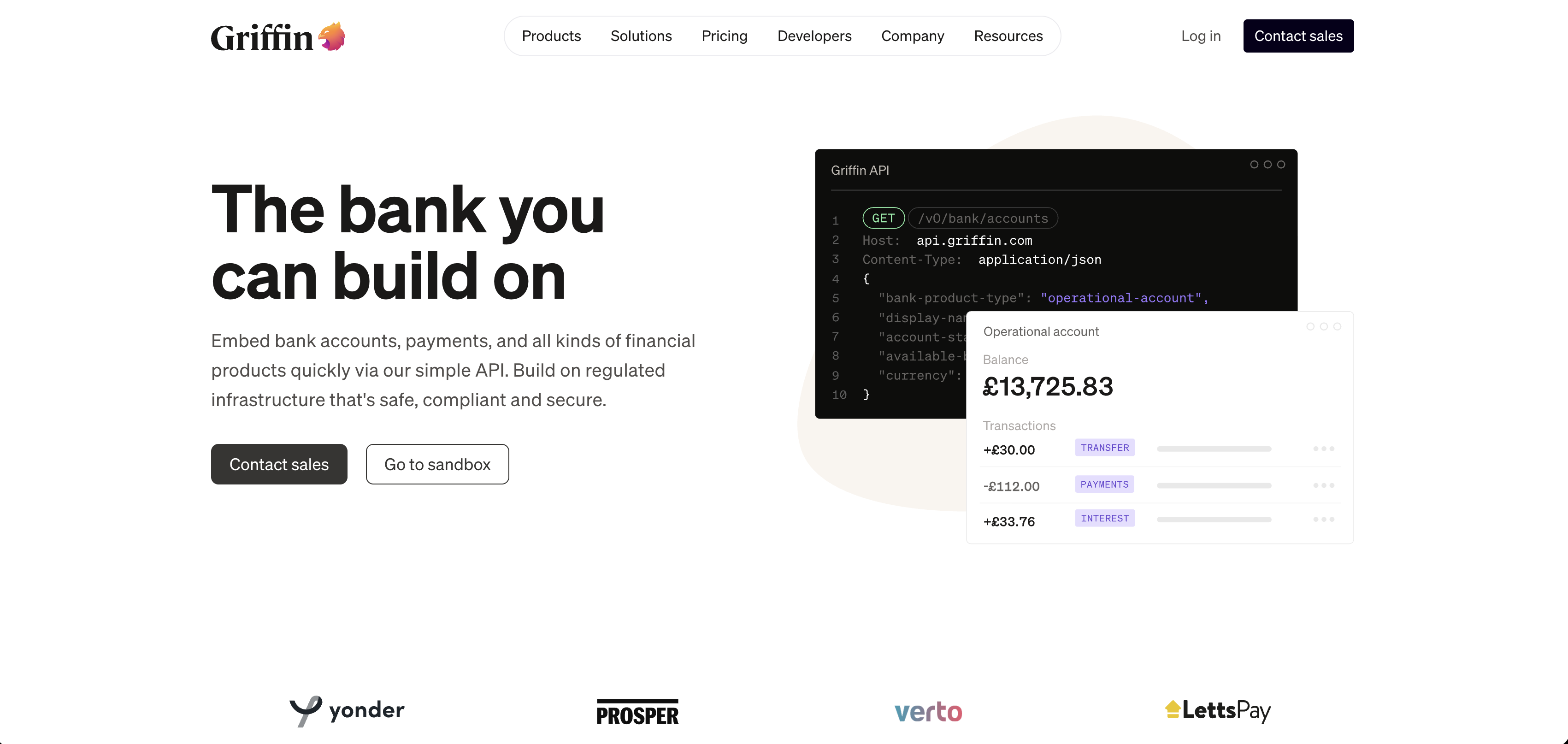

Griffin sits at the intersection of banking infrastructure and regulatory compliance, offering a modern approach to the unglamorous work of moving money safely. The London-based company builds banking-as-a-service platforms and payment rails designed for fintechs and regulated institutions that need to move fast without cutting corners on compliance. Rather than forcing customers to navigate the labyrinth of legacy banking systems, Griffin abstracts away the complexity, offering API-first access to real-time payments, account management, and embedded compliance tooling. It's the plumbing that lets newer financial services companies focus on their customers instead of wrestling with outdated bank infrastructure. In a market flooded with point solutions, Griffin's bet is that the future belongs to platforms that integrate banking, payments, and compliance from the ground up. The company operates quietly compared to flashier consumer fintech brands, but its impact ripples through the European fintech ecosystem where speed and regulatory certainty are non-negotiable. Griffin represents a shift toward infrastructure-first thinking: the recognition that solid banking foundations, not clever marketing, separate winners from regulatory casualties. Its position in the stack means it works with both institutional players and next-generation fintechs, each seeking to either modernize their operations or bypass legacy constraints entirely.