6 companies

Pleo

Payments🇩🇰 Denmark

Pleo is a corporate expense management platform that treats company spending like a personal finance problem solved through software. Rather than the tedious reimbursement cycles and spreadsheet chaos of traditional corporate cards, Pleo gives employees physical and virtual cards coupled with real-time expense categorization and approval workflows that happen at the speed of a Slack message.

The company positions itself as the antidote to finance teams drowning in manual reconciliation. Employees get instant card access, automatic receipt capture via smartphone, and intelligent categorization that learns spending patterns. Meanwhile, finance teams gain real-time visibility into company spending without the usual lag and friction.

Pleo operates in a market where most companies still rely on legacy corporate card providers or outdated expense management software that feels bolted together from the 1990s. The Danish fintech has expanded across Europe, building a platform that combines the convenience of consumer fintech with the compliance and control requirements of enterprise finance.

It's become a reference point for how embedded finance and B2B SaaS can simplify workflows that enterprises have tolerated as painful for decades. The company sits comfortably at the intersection of business banking, card issuing, and expense automation—categories that individually are crowded but rarely integrated as seamlessly.

Tradeshift

Financial Infrastructure🇩🇰 Denmark

Tradeshift runs the operating system for global commerce—a cloud platform that lets businesses transact with each other in real time, from purchase orders to invoices to payments. It's built for a world where finance teams spend less time on manual reconciliation and more time on strategy, where supply chain visibility is instant, and where cash flow stops being a guessing game.

The company sits at the intersection of procurement, invoice management, and working capital, connecting enterprises with their supplier networks. Rather than forcing companies to adopt yet another SaaS tool, Tradeshift embeds itself into the workflows that already exist—automating the grunt work of B2B commerce that still happens through email, spreadsheets, and PDF attachments.

Trodeshift's positioning is distinctly European: it understands the complexity of multi-regional supply chains, VAT compliance, and the regulatory layers that global companies navigate daily. While American fintech still obsesses over consumer-facing dashboards, Tradeshift has spent years building the unglamorous but essential plumbing that keeps enterprise trading flowing.

In an era where digital transformation is finally table stakes for large corporates, Tradeshift has become infrastructure—the kind that companies discover they can't function without. It's not the flashiest story in fintech, but it's one of the most resilient.

Kompas Bank

Digital Banking🇩🇰 Denmark

Kompas Bank is a Danish digital banking platform built for the modern customer who finds traditional banking unnecessarily complicated. Rather than forcing users through dense interfaces and archaic processes, Kompas strips away the friction and delivers straightforward account management, payments, and savings tools through a clean mobile app. The bank operates with a refreshingly direct approach: no unnecessary fees, transparent pricing, and the kind of speed you'd expect from a fintech rather than a legacy institution. It positions itself as an alternative to Denmark's established banking hierarchy, appealing to younger professionals and those frustrated by the status quo. Kompas combines the regulatory credibility of a licensed bank with the user experience sensibilities of a modern fintech, making it a genuinely different proposition in the Nordic market. The platform handles everyday banking—payments, transfers, account management—with the kind of simplicity that makes you wonder why other banks make things so hard. In the broader European digital banking landscape, Kompas represents the quiet professionalization of challenger banking in Scandinavia, where competition has shifted from novelty to genuine customer preference.

Anyday

Real Estate Finance🇩🇰 Denmark

Anyday is a Danish digital mortgage platform that strips away the tedium from home financing. Instead of bouncing between bank advisors and spreadsheets, borrowers get a transparent, mobile-first experience where they can compare rates, model different scenarios, and close deals without the usual friction. The company operates as a fintech-powered mortgage broker, aggregating products from multiple lenders and presenting them side by side with clear terms.

What sets Anyday apart in the Nordics is its refusal to pretend mortgages are simple. The platform acknowledges the complexity but designs around it, letting customers understand exactly what they're paying and why. While traditional banks still guard their mortgage offerings behind appointment-only processes, Anyday treats the entire journey as a digital product.

The company positions itself firmly against the status quo of Scandinavian mortgage banking, where rates are opaque and switching costs are high. By aggregating supply and making comparison effortless, Anyday creates pressure on incumbents while capturing switching demand from customers tired of legacy processes. It's a model that works particularly well in the Nordics, where regulatory clarity and digital adoption are already high.

Anyday represents the emerging class of fintech infrastructure plays that don't replace banks but make them more competitive by forcing transparency and speed into categories that have resisted both.

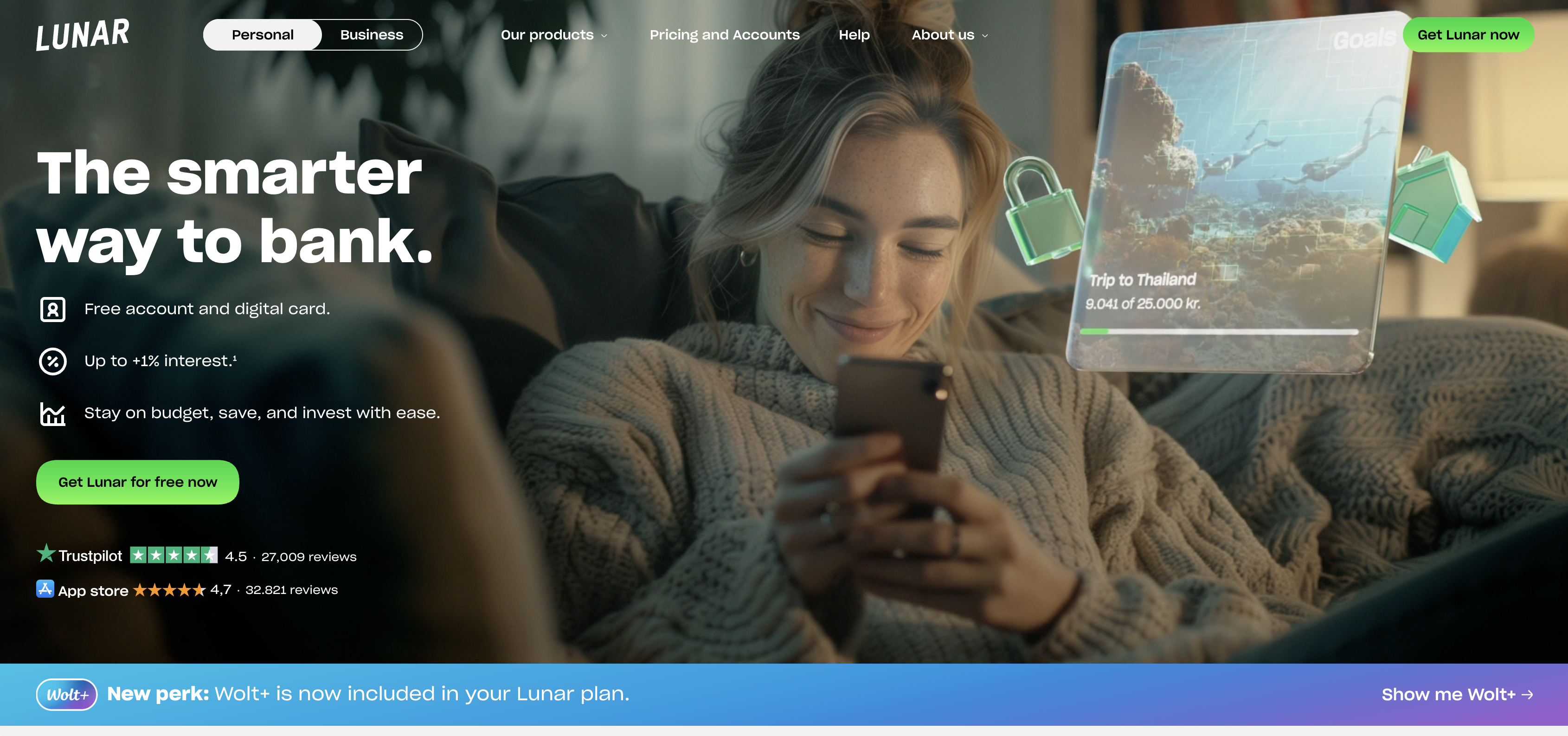

Lunar

Payments🇩🇰 Denmark

Lunar is a mobile-first banking app that strips away the complexity of traditional finance and replaces it with something radically simpler. Rather than pretending to be a full-service bank, Lunar focuses obsessively on what mobile banking actually needs to be: fast, borderless, and genuinely user-friendly.

The product itself is deliberately minimal. You get a digital account, a card, and payment tools that work seamlessly across Europe without the friction of legacy systems. There's no theatre, no unnecessary features, no pretence. What you see is what you get.

Lunar sits in a crowded space of European neobanks, but it's differentiated by an almost Nordic clarity of purpose. While competitors chase feature parity with legacy banks, Lunar has chosen constraint. The app does payments, spending insights, and cross-border transfers exceptionally well, then stops. That discipline feels rare in fintech, where bloat is often mistaken for progress.

The company operates across multiple European markets and has built a genuine community of users who value simplicity over complexity. For the generation that doesn't want to step foot in a physical bank but also doesn't want cryptocurrency jargon or gamified investing, Lunar fills a specific and growing need. It's the kind of fintech that understands that sometimes the most powerful feature is knowing what to leave out.

Spiir

Open Banking🇩🇰 Denmark

Personal finance app helping users manage money and spending.