16 companies

Cobee

SME Finance🇪🇸 Spain

Cobee gives companies a platform for employee benefits and flexible compensation.

Ritmo

Digital Banking🇪🇸 Spain

Ritmo is a neobank built specifically for the gig economy—the millions of freelancers, contractors, and self-employed workers across Europe who operate outside traditional employment structures. Instead of forcing gig workers into standard business banking products, Ritmo designed from the ground up to understand the rhythms of irregular income, multiple clients, and the administrative burden that comes with self-employment.

The platform combines a business checking account with invoicing, expense tracking, and tax preparation tools, removing the friction between earning money and managing it. You get real-time visibility into cash flow, automated categorization of business expenses, and direct integration with tax authorities—so when it's time to file, the data is already organized.

What sets Ritmo apart isn't just its feature set. Most fintech players either chase the consumer market or build enterprise solutions for corporations. Ritmo recognized a gap: gig workers are economically significant but underserved by both traditional banks and most neobanks. The company speaks their language, understands their cash flow volatility, and builds products that actually reflect how they work.

In the broader European fintech landscape, Ritmo represents a growing trend of vertical-specific banking platforms. Rather than being all things to all people, it's solving a precise problem for a rapidly growing demographic. For the gig worker tired of explaining variable income to a bank manager or juggling multiple apps, Ritmo is the kind of focused, no-nonsense solution that defines modern fintech at its best.

Divilo

Financial Infrastructure🇪🇸 Spain

Divilo is building the infrastructure for European businesses to manage their international payroll at scale. Rather than juggling multiple vendors across different countries—payroll processors here, compliance specialists there, currency brokers elsewhere—Divilo consolidates the entire stack into one operating system. The platform handles everything from local employment law compliance to multi-currency payments, tax filing, and benefits administration across the continent. For HR teams and CFOs wrestling with the complexity of expanding internationally, it's a rare case of genuine consolidation rather than another bolted-on layer. The European payroll market remains fragmented by design—local rules, tax codes, and banking infrastructure mean there's no true continental standard. Divilo is attacking this head-on with a unified API and dashboard that speaks to both the technical and operational reality of cross-border employment. It's the kind of infrastructure play that sounds boring until you realize how much operational friction it removes for companies thinking beyond their home market.

Belvo

Embedded Finance🇪🇸 Spain

Belvo is a fintech infrastructure company that lets developers tap into Latin American banking data without building a single integration. The platform connects to thousands of banks and financial institutions across Mexico, Brazil, Colombia, and Peru, unlocking account balances, transaction histories, and identity information through a single API. Rather than forcing developers to chase down fragmented banking systems, Belvo standardizes chaotic regional financial infrastructure into clean, predictable data flows. Its core insight is simple: Latin American fintech is drowning in bank connectivity work when it should be building products. Belvo solves that. The platform serves fintechs, neobanks, and traditional financial institutions looking to modernize lending decisions, open banking integrations, and embedded finance experiences. Think of it as the connective tissue between fractured regional banking systems and the apps that need to run on top of them. By abstracting away the complexity of working with hundreds of different bank APIs and connection methods, Belvo has become the standard for financial data aggregation in a region where banking infrastructure is anything but standardized. It's the kind of boring-but-essential infrastructure that powers smarter lending, faster onboarding, and new financial products across Latin America.

Fintonic

Open Banking🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

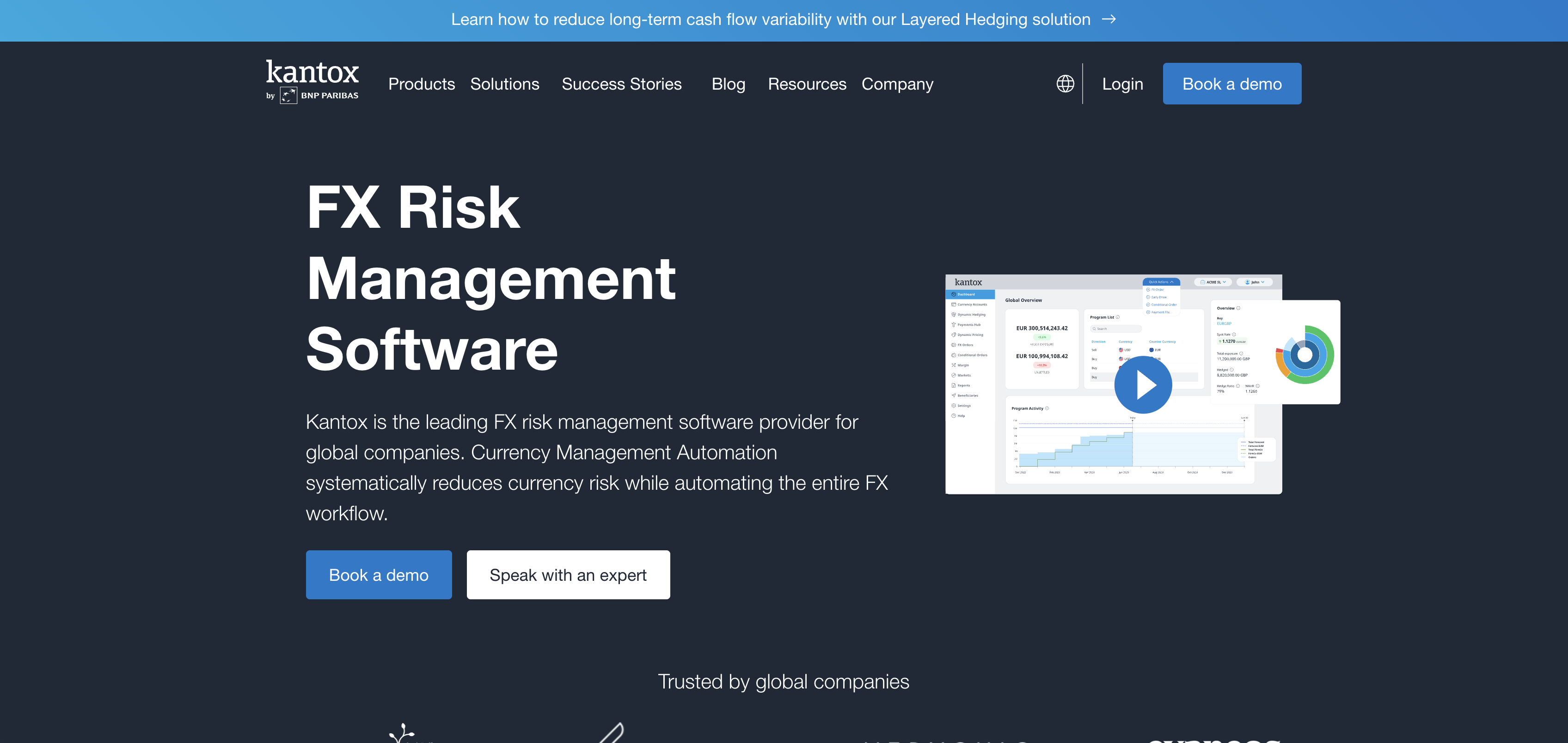

Kantox

Payments🇪🇸 Spain

Kantox sits at the intersection of corporate finance and fintech, solving a problem that has plagued treasurers and CFOs for decades: the cost and complexity of managing foreign exchange. Rather than forcing companies through the byzantine world of traditional banks or crude hedging tools, Kantox built a platform that lets businesses buy and sell currency with transparency, speed, and intelligence.

The platform aggregates liquidity from multiple sources—banks, non-bank liquidity providers, and peer matching—and surfaces the best rates in real time. No more vendor lock-in, no more opaque spreads, no more waiting. A mid-market company can execute a multi-million euro FX trade in minutes, seeing exactly what they're paying and why.

What sets Kantox apart in a crowded treasury tech space is its refusal to abstract away the mechanics. The platform shows you the market, then lets you trade. It's designed for finance professionals who know what they're doing and want control back from intermediaries. The company has built serious depth in emerging markets and supply chain currencies, which most legacy providers still treat as afterthoughts.

Kantox represents a broader shift in European fintech: the recognition that some of the most valuable problems live in the unglamorous corners of corporate finance, where even small improvements in execution cost save companies millions annually. In that sense, it's doing for FX what more visible fintechs have done for payments—stripping away friction and opacity from a process that should have been digital decades ago.

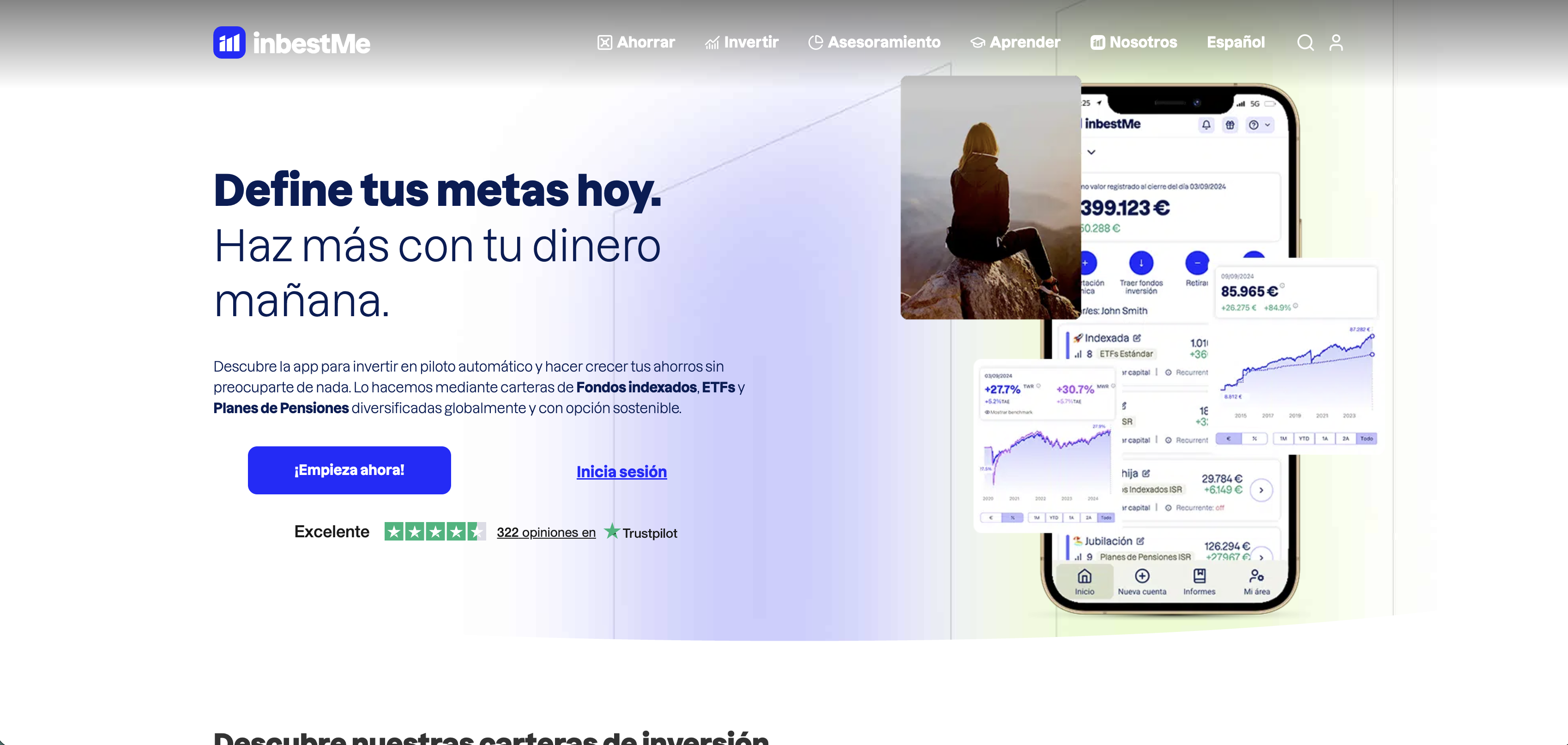

inbestMe

Wealth🇪🇸 Spain

Spain's investment culture has traditionally been more conservative than other major European markets — a population with high savings rates but low investment participation, and a financial advisory landscape dominated by banks that have not always had their clients' interests at the centre of their advice. inbestMe was founded in Barcelona in 2014 to bring transparent, low-cost robo-advisory to the Spanish market. Its platform offers diversified ETF portfolios with multiple risk profiles and specialised strategies including socially responsible investing — a category that has resonated particularly with the Spanish retail investor segment that values investment products with clear values alignment. The company has built a position in the Spanish wealth tech market alongside Indexa Capital and Finizens, the three companies that have effectively defined Spanish robo-advisory. In the Iberian market, where Indexa has built its position on aggressive cost minimisation and Finizens on automated saving habits, inbestMe has differentiated through SRI portfolios and a broader range of investment strategies. In the European robo-advisory landscape, the Spanish market has emerged as one of the more competitive — proof that consumer demand for low-cost diversified investing exists wherever transparent products are made available, even in markets that financial institutions have written off as resistant to change.

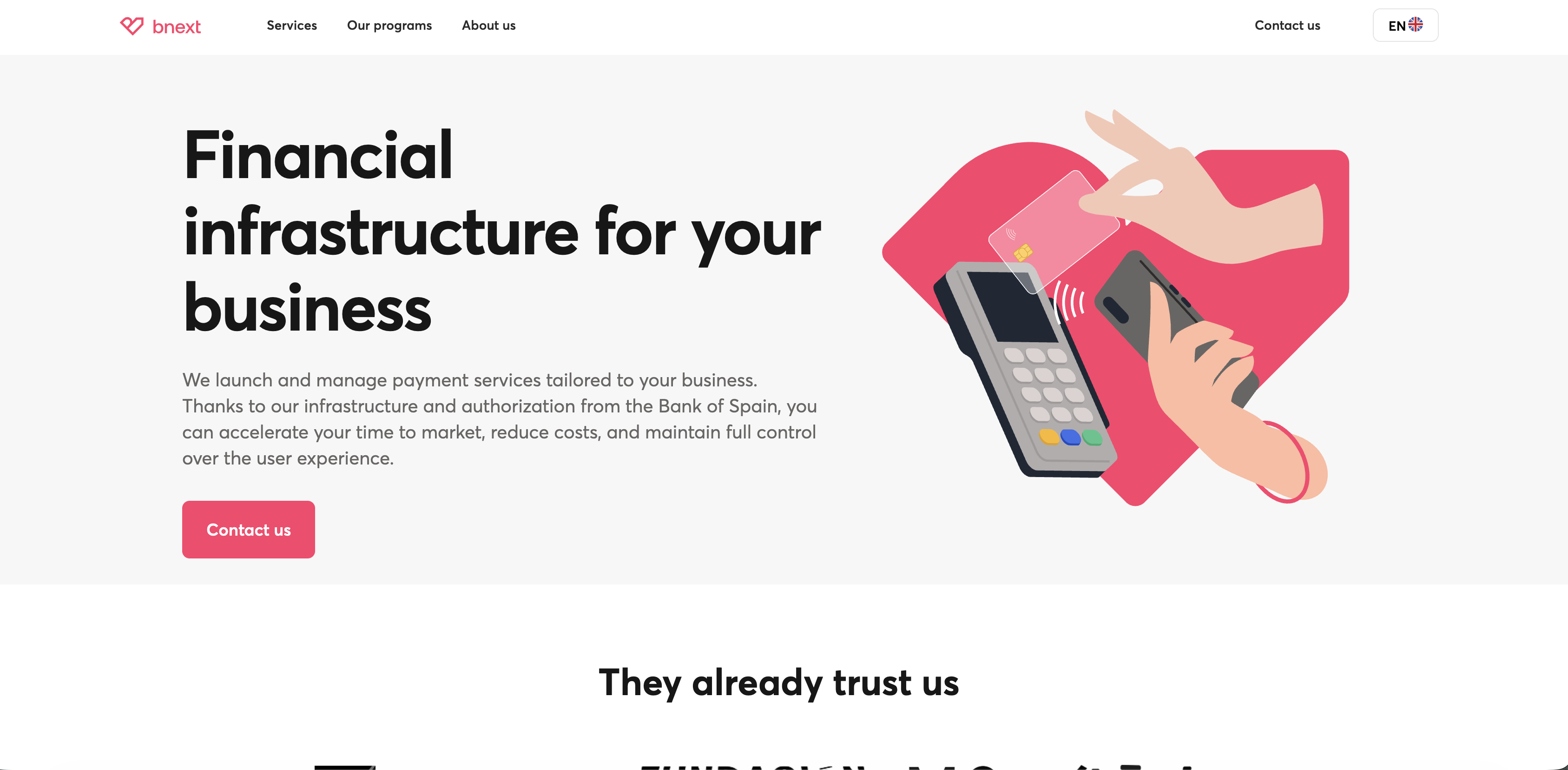

bnext

Payments🇪🇸 Spain

bnext is a Spanish neobank built for the self-employed and small business owners who've outgrown traditional banking but don't need enterprise complexity. It strips away the bloat of legacy banks and focuses on what actually matters: a mobile-first account, competitive forex rates, and transparent fees with no surprise charges. The platform handles invoicing, expense tracking, and basic bookkeeping alongside core banking, positioning itself as a unified workspace rather than just another digital bank. Where established institutions still treat SMEs as afterthoughts, bnext treats them as the primary customer. It's designed for the freelancer checking balances between client calls and the startup founder who wants one dashboard instead of five browser tabs. The company has carved out real traction in Spain and increasingly across Europe, proving there's genuine demand for banking that actually understands how modern small business works.

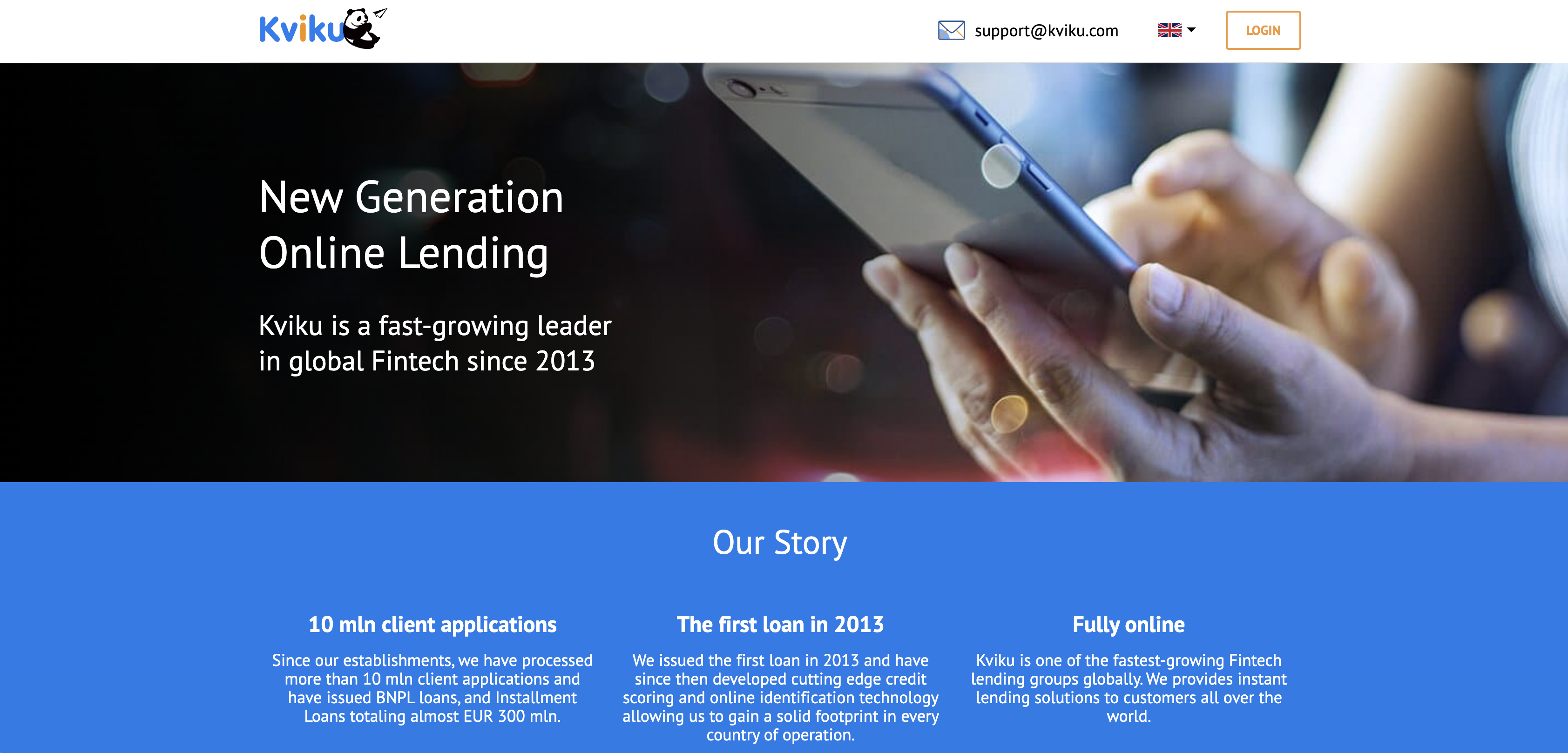

Kviku

Lending🇪🇸 Spain

Instant credit at the point of need — a small loan approved in seconds, disbursed before the moment of purchase passes — is one of the more powerful applications of modern credit technology. Kviku was founded in 2013 and operates as a digital consumer lender offering virtual credit cards and instalment loans across multiple markets including Spain, Poland, Kazakhstan, and the Philippines. Its model is built around speed and accessibility: a fully automated underwriting process that makes credit decisions in real time using alternative data, targeting the segment of consumers who need small amounts quickly and are underserved by traditional credit products. The virtual credit card format is particularly relevant in markets where physical card infrastructure is less developed but smartphone penetration is high. Kviku operates across a wide geographic footprint for a company of its size, reflecting the scalability of a model that is fundamentally about credit technology rather than physical distribution. In the embedded finance and BNPL context, Kviku represents the direct lending end of the spectrum — not a buy now pay later product embedded in a merchant checkout, but a digital credit line that consumers carry with them to any point of purchase.

Sequra

Embedded Finance🇪🇸 Spain

Sequra is a Spanish fintech that's quietly become one of Europe's most pragmatic buy-now-pay-later platforms. Rather than chasing the glossy consumer narrative, Sequra built itself as the infrastructure layer for merchants—retailers, e-commerce platforms, and marketplaces across Europe who need flexible payment options without the operational overhead.

The company operates a two-sided model: on one end, it handles merchant acquisiton and underwriting; on the other, it manages the consumer credit experience through instant decisioning and repayment flexibility. What sets Sequra apart is its merchant-first approach. It doesn't market directly to consumers. Instead, it embeds itself into checkout flows and relies on merchant partnerships to scale. This is embedded finance done deliberately.

Sequra's competitive positioning sits between pure BNPL platforms (Klarna, Clearpay) and traditional point-of-sale lending. It's more disciplined about credit risk than some BNPL peers, more tech-native than legacy installers. Across Spain, Italy, France, and Germany, it's become the quiet backbone for thousands of merchants who want flexible payment rails without the consumer brand overhead.

In a fintech landscape increasingly obsessed with consumer apps, Sequra represents a different thesis: sometimes the real value is in being invisible, reliable infrastructure.