27 companies

AdyenFeatured

Embedded Finance🇳🇱 Netherlands

Pieter van der Does and Arnout Schuijff had already built and sold one payments company when they sat down in 2006 to start again. The result was Adyen — the name literally means "start over" in Surinamese — and the premise was simple: instead of stitching together the same fragmented payment infrastructure everyone else was using, they would build the whole thing themselves from scratch.

That decision, made in an Amsterdam office nearly two decades ago, is still the reason Adyen is different. Most payment companies are assemblers — they buy a gateway here, a processor there, bolt them together and hope for the best. Adyen owns its own technology stack end to end, which means a merchant integrating once gets access to card processing, local payment methods, point-of-sale terminals, and real-time settlement data through a single platform. No middle layers, no reconciliation headaches, no finger-pointing between vendors when something breaks.

The client list tells you everything about where Adyen sits in the market. McDonald's, Spotify, Microsoft, LVMH, H&M — these are companies with serious payment volumes and zero appetite for systems that don't work. Adyen became the default choice for enterprises that had outgrown the limitations of traditional payment stacks and needed something that could handle global scale without buckling.

Since going public on Euronext Amsterdam in 2018, Adyen has grown into one of Europe's most valuable technology companies, with around 4,300 employees across 23 countries and net revenue of just under €2 billion in 2024. It remains headquartered in Amsterdam and consistently profitable — a combination that's rarer in fintech than it should be.

For businesses that treat payments as infrastructure rather than an afterthought, Adyen is the benchmark everything else gets measured against.

MollieFeatured

Financial Infrastructure🇳🇱 Netherlands

Adriaan Mol built Mollie's first backend while living with his parents in the Netherlands in 2004. No investors, no office, no team — just a founder and an idea that small businesses deserved a payment integration that didn't require a team of lawyers and a six-month setup process. He bootstrapped it for over fifteen years before taking outside funding in 2019. By then, Mollie had already grown into one of the most important payment platforms in European e-commerce, entirely on the back of a product that developers actually liked using.

The proposition is straightforward: one API, one dashboard, and access to the payment methods that actually matter across Europe. That means iDEAL in the Netherlands, Bancontact in Belgium, Klarna and SEPA Direct Debit everywhere, alongside cards, Apple Pay, and a growing list of local methods that would otherwise require separate integrations and separate acquirer relationships. Mollie handles the compliance, the fraud monitoring, and the settlement complexity. Merchants get a clean interface and a single invoice.

For the 250,000 businesses using Mollie today — ranging from Gymshark and Wild to local bakeries and market stalls, as CEO Koen Köppen regularly points out — the appeal is less about feature lists and more about what they don't have to think about. European payments are fragmented by design. Every country has its preferred methods, its own regulatory quirks, its own consumer habits. Mollie's job is to make that invisible.

The numbers from 2024 reflect a company that has found its model. Revenue reached €214 million, up 28% year on year, with gross profit growing 30% to €115 million and the company returning to positive EBITDA for the first time since 2018. Mollie raised a total of $940 million in funding and was valued at $6.5 billion following its 2021 Series C led by Blackstone.

The most significant recent development is the acquisition of GoCardless in December 2025 — bringing the UK-based direct debit specialist into the Mollie group and substantially expanding its recurring payments and bank transfer capabilities across Europe. Combined, the two companies cover a considerable share of European e-commerce payment infrastructure.

Mollie is still headquartered in Amsterdam, with around 900 employees across offices in Ghent, London, Lisbon, Munich, Milan, Paris, and beyond.

FourthlineFeatured

Identity & KYC🇳🇱 Netherlands

Fourthline didn't start as a KYC company. It started as a payment institution. Krik Gunning and Chris van Straeten founded Safened in Amsterdam, licensed by the Dutch Central Bank as a regulated payment provider. As Safened onboarded its own customers, it built identity verification technology capable enough that other banks and fintechs started asking to use it directly. The demand was real and growing — digital financial services were expanding rapidly but compliance infrastructure hadn't kept pace. In 2019 Gunning and van Straeten spun the KYC operation out as a standalone company and renamed it Fourthline.

The name refers to compliance being the fourth line of defence in financial crime prevention — after business operations, risk management, and internal audit. It's a deliberately serious framing for a company that treats KYC not as a box to tick but as a technical problem worth solving properly. While many identity verification providers offer generic document checks, Fourthline built its platform around the regulatory requirements of Europe's strictest financial supervisors — the kind of compliance depth that a neobank launching in Germany or a broker entering the Netherlands actually needs to satisfy its regulator, not just its legal team.

The platform covers the full KYC and AML stack through a single API: document verification, biometric checks with liveness detection, AML and sanctions screening, risk scoring, proof of address, and ongoing customer monitoring throughout the customer lifecycle. The modular architecture means regulated institutions can pick the components they need rather than buying a fixed bundle — a practical advantage for fintechs that need identity verification at onboarding but different monitoring requirements at scale.

The client list is a reasonable proxy for the quality of the product. Fourthline verifies identities for N26, Qonto, Trade Republic, flatexDEGIRO, Scalapay, Shine, and Bitpanda — regulated financial businesses across Europe that operate under strict supervisory scrutiny and cannot afford onboarding failures. The company employs around 225 people and has raised approximately $70 million in funding, primarily from Finch Capital.

In March 2026 Fourthline appointed Paul Stoddart as CEO, replacing co-founder Krik Gunning who moved into an advisory role after leading the company since its founding. The timing coincides with a significant regulatory tailwind: the EU's new Anti-Money Laundering Regulation comes into force in July 2027, substantially raising compliance requirements for financial institutions across Europe and expanding the addressable market for precisely the kind of infrastructure Fourthline has spent six years building.

Knab

Digital Banking🇳🇱 Netherlands

Knab is a Dutch digital bank for consumers, freelancers, and small businesses.

Biller

Payments🇳🇱 Netherlands

Biller provides B2B buy-now-pay-later and invoice payment solutions.

Brand New Day

Wealth🇳🇱 Netherlands

Brand New Day provides online pensions, savings, and investment accounts in the Netherlands.

Credolab

Identity & KYC🇳🇱 Netherlands

Credit decisions in markets without comprehensive credit bureau coverage have always been hard. The traditional underwriting model relies on credit history, income verification, and identity documents that significant portions of the global population either don't have or can't easily produce. Credolab was founded in 2016 with operations across Asia and Europe to address that gap with an unconventional data source — smartphone metadata. Its platform analyses behavioural patterns from a mobile device — without accessing personal content — to generate credit scores for consumers who have no traditional credit history. The data points are surprisingly predictive: how someone manages their phone storage, the pattern of their app usage, the regularity of their device behaviour all correlate with credit risk in ways that traditional underwriting misses. Credolab serves lenders, telcos, and digital platforms across emerging markets where credit bureau coverage is thin and the demand for digital credit is growing rapidly. In the alternative credit data landscape, where companies are competing to find the data sources that will define the next generation of underwriting, Credolab's behavioural smartphone approach is one of the more distinctive — and one that addresses a genuinely large unmet need in markets where billions of people remain credit-invisible to traditional financial systems.

Pay.nl

Financial Infrastructure🇳🇱 Netherlands

Pay.nl is a Dutch payment processor built for the complexity of modern commerce. Rather than forcing merchants into a one-size-fits-all payment flow, it offers a modular approach where acquirers, payment methods, and risk tools snap together like building blocks. This flexibility appeals to mid-market retailers and platform operators who've outgrown off-the-shelf solutions but don't have the resources to build from scratch.

The company positions itself as the pragmatic middle ground in European payments. While fintechs chase consumer flashiness and traditional PSPs move at legacy speed, Pay.nl focuses on the unglamorous reality of merchant operations: payment routing, multi-currency settlement, real-time reconciliation, and developer experience. Its API-first architecture means integrations take weeks instead of quarters.

Pay.nl operates across the full payment stack—card acquiring, alternative payment methods, tokenization, subscription billing—but treats them as components rather than marketing bullets. This modular thinking extends to risk management and compliance, which the company bundles without overhead.

Within Europe's crowded payments landscape, Pay.nl competes less on consumer reach and more on merchant control. It's the choice for companies that care about payment economics and operational efficiency rather than brand building. Its role in the broader ecosystem is to mature the middle market, proving that European merchants don't need either a tech giant's infrastructure or a startup's rough edges.

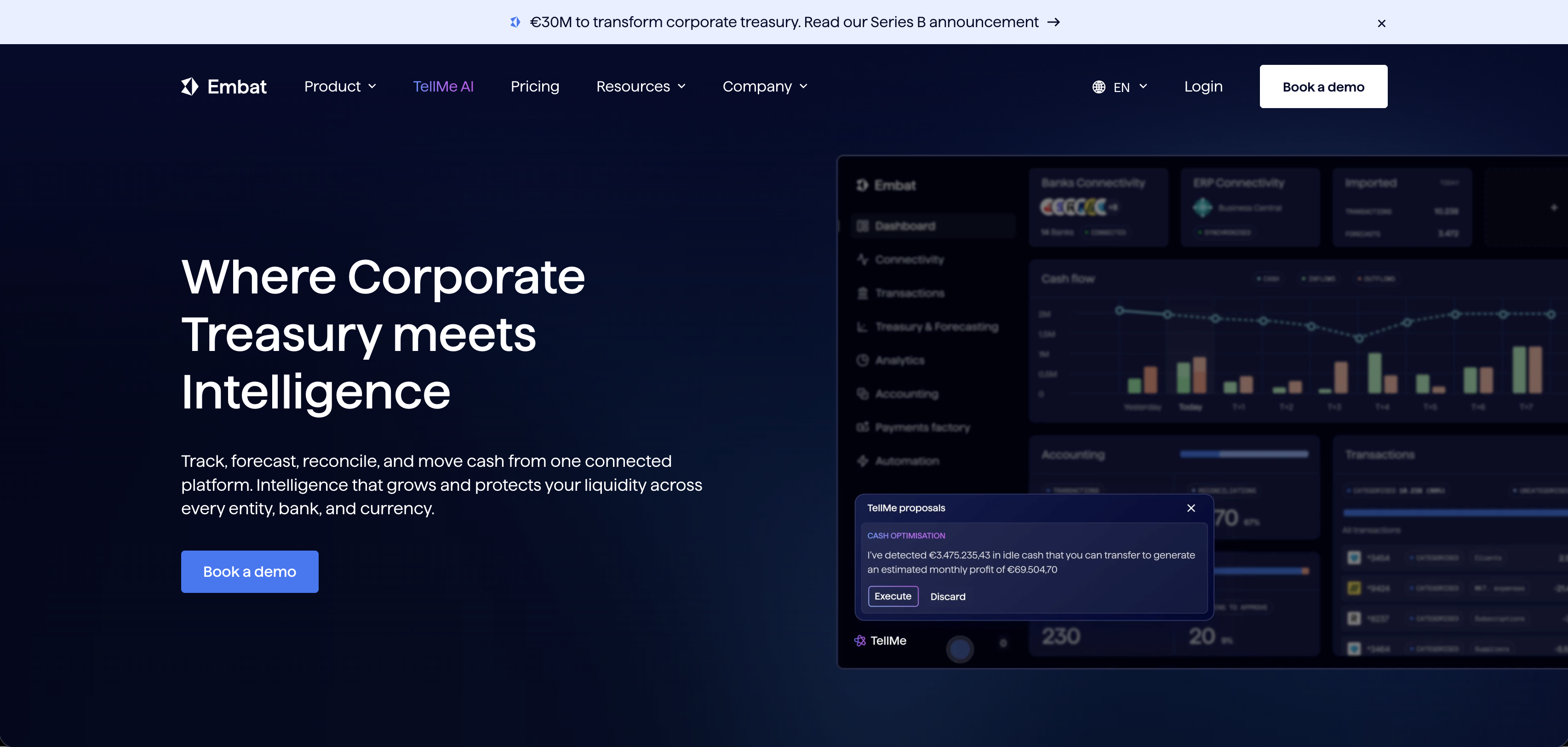

Embat

Financial Infrastructure🇳🇱 Netherlands

Embat is a European fintech platform built for the era when payments moved beyond the checkout. Founded on the principle that modern businesses need payment infrastructure that speaks their language—not the other way around—Embat offers a composable payments stack designed for developers and merchants who refuse to settle for legacy constraints.

The platform combines payment orchestration, processing, and settlement into a single, modular system. Rather than forcing clients into rigid vendor relationships, Embat lets companies plug in their preferred processors, acquirers, and gateway partners while maintaining unified visibility and control. This flexibility appeals to enterprises and merchants tired of vendor lock-in and technical debt.

What sets Embat apart in the crowded European payments landscape is its developer-first design philosophy. The company recognizes that payments sit at the intersection of multiple systems—loyalty, inventory, subscriptions, marketplaces—and builds its API architecture accordingly. This contrasts sharply with older payment solutions that treat payments as an isolated transaction layer rather than a core business platform.

Embat occupies a distinct position between monolithic payment processors and lightweight API providers. It's built for companies that have outgrown commodity payment gateways but don't want to stitch together five different vendors to get what they need. In the increasingly competitive European fintech market, Embat represents the modern infrastructure play: solving real operational complexity for merchants and enterprises through intelligent, flexible payment technology.

ICEPAY

Payments🇳🇱 Netherlands

ICEPAY is a Dutch payment processor that handles everything from card transactions to alternative payment methods across Europe. The company powers checkout experiences for thousands of merchants, managing the complex plumbing of converting customer intent into settled funds. What sets ICEPAY apart is its focus on European merchants—particularly mid-market businesses that need more than a one-size-fits-all gateway. The platform bundles payment processing with risk management, offering fraud detection and chargeback protection alongside the standard card rails. It's built for merchants who want flexibility without complexity, handling both online and in-store payments through a unified infrastructure. ICEPAY operates in a crowded space where most competitors either stay focused on pure payment processing or sprawl into adjacent services. The company positions itself as the European alternative to global juggernauts, with deeper understanding of regional payment preferences and compliance requirements. It's a pragmatic choice for businesses scaling across multiple European markets—less startup energy, more mature operational backbone. In the broader fintech ecosystem, ICEPAY represents the unglamorous but essential layer: the infrastructure that makes European commerce work behind the scenes.