104 companies

Wise

Payments🇬🇧 United Kingdom

Taavet Hinrikus had a problem that was embarrassingly simple to describe and maddeningly hard to solve. He was one of Skype's first employees, living in London and getting paid in euros while his bills were in pounds. Every month he was losing money to bank fees and exchange rate markups that his bank never disclosed upfront. Kristo Käärmann, a Deloitte consultant, had the same problem in reverse. In 2011 they sat down, compared rates, and started swapping money directly between each other's bank accounts — bypassing the banks entirely. Then they thought: what if anyone could do this?

That informal arrangement became TransferWise, launched in London in January 2011 with a straightforward promise that banks had been making impossible for decades: the real exchange rate, with fees shown upfront before you commit to a transfer. The early pitch was almost deliberately confrontational — the founders publicly compared bank exchange rate markups to theft, took out billboard ads outside banks, and built a campaign around showing customers exactly how much they were being overcharged. It worked.

TransferWise rebranded to Wise in 2021, the same year it listed directly on the London Stock Exchange — bypassing the traditional IPO process in a move consistent with a company that had spent a decade bypassing traditional financial processes. The listing valued the business at around £9 billion and gave it public-company discipline without the fanfare of a conventional float.

The product has expanded well beyond the original currency transfer use case. Wise now offers multi-currency accounts supporting over 40 currencies, a debit card, a business product for SMEs and freelancers managing cross-border payments, and a platform business that lets banks and other fintechs embed Wise's infrastructure into their own products. By June 2025, the platform had 15.6 million active customers processing £145 billion in cross-border volume annually — up 23% year on year. Revenue crossed £1 billion in 2024, with profit of £354 million.

The most significant recent development is structural: shareholders voted in July 2025 to move Wise's primary listing from London to a US exchange, with the transfer expected by early 2026. It's a pragmatic decision — the US is a large and growing market, the company has money-transmission licences in 48 states, and American institutional investors have historically valued fintech companies at higher multiples than London's market has.

Wise employs around 5,500 people and operates across more than 70 countries. Both founders remain involved — Käärmann as CEO, Hinrikus having stepped back from the board in recent years.

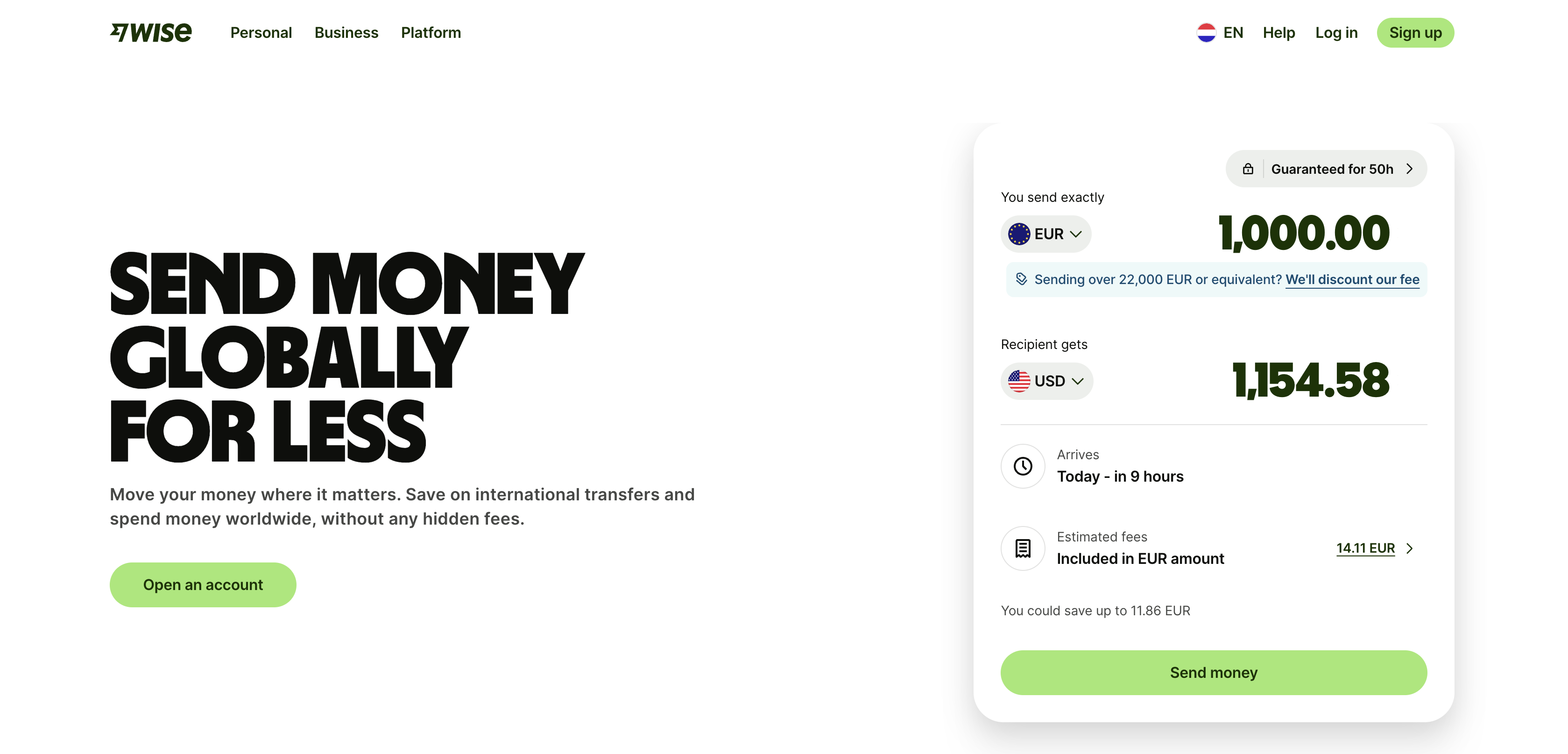

The core offer is deceptively simple. Wise operates its own network rather than renting access to SWIFT, which means it can cut out the middlemen taking cuts at every stage. You send pounds, it converts at the mid-market rate (the one you see on Google), and your recipient gets euros without the usual 3-5% tax that banks quietly extract. The company issues multi-currency accounts and cards that work globally, positioning itself as infrastructure for anyone whose life doesn't fit neatly into a single currency zone.

In the European market, Wise has become synonymous with cross-border reality. While traditional banks still talk about "international banking solutions," Wise customers are already sending money to fifteen countries from their phone without a second thought. The company went public in 2021, which paradoxically made it less of a fintech insurgent and more of an established player—but the underlying model hasn't changed: transparency and efficiency where opacity used to be profitable.

Wise represents a particular kind of fintech maturity: the startup that solved a specific, universal problem well enough that it became essential infrastructure for millions of people operating across borders. Its role in the European landscape is that of the pragmatist, proving that you don't need regulatory capture or cross-subsidization to build a sustainable business in payments.

MonzoFeatured

Wealth🇬🇧 United Kingdom

The founding team that built Monzo had all worked together before — at Starling Bank, another challenger bank startup that didn't survive its internal conflicts. Tom Blomfield, Gary Dolman, Jonas Huckestein, Jason Bates, and Paul Rippon left Starling together in 2015 and started again. The product they built was initially a prepaid card — a coral-coloured piece of plastic that became one of the most recognisable objects in British fintech — before becoming a fully licensed current account in 2017.

The early user community was unusual for a bank. Monzo ran community forums, published public blog posts about its engineering decisions, and invited customers into beta programmes for new features. When it broke the world record for the fastest crowdfunding raise in 2016 — £1 million in 96 seconds — it wasn't just raising money; it was building an identity. People felt ownership of the product in a way that no high street bank had ever managed to create. That emotional connection became a genuine competitive advantage.

The product has matured considerably since then. Monzo now offers current accounts, joint accounts, savings pots, personal loans, overdrafts, and investment products, all wrapped in the real-time notification experience and transaction categorisation that made its early reputation. Revenue reached £1.23 billion in 2024, up 40% year on year, with net income of £95 million — the second consecutive year of profitability after years of growth-first losses. The customer base reached 12.1 million by end of 2024, making Monzo the UK's largest digital bank by customer count. Customer deposits stood at £16.6 billion.

The business is still private — the much-discussed IPO has not yet happened, and internal disagreements about where to list (the former CEO TS Anil favoured the US, the board preferred London) contributed to Anil's departure in October 2025. Diana Layfield took over as CEO with a mandate focused on international expansion before any public listing. The company is valued at approximately $5.9 billion following a 2024 secondary sale backed by Alphabet's GIC and StepStone.

In December 2025 Monzo announced it had agreed to acquire Habito, the digital mortgage broker, pending regulatory approval — a move that extends the product into one of the last major financial products it didn't yet offer. With 3,821 employees and a loan book growing rapidly, Monzo has evolved from a prepaid card experiment into a bank with genuine scale and a growing claim on being the primary financial account for a generation of UK consumers.

Starling Bank

Digital Banking🇬🇧 United Kingdom

Starling Bank is a British challenger bank that stripped away the friction of traditional banking and rebuilt it around what modern customers actually need: instant notifications, real-time spending insights, and accounts you can open in minutes without stepping into a branch. Founded in 2014, it operates as a fully regulated bank with its own banking license, not just a wrapper around legacy infrastructure.

The platform serves both consumers and SMEs, offering straightforward current accounts, savings pots, and increasingly sophisticated business banking tools. Unlike neobanks reliant on partnerships, Starling owns its core infrastructure, which means faster iteration and tighter product control. The company has built a reputation for no-nonsense transparency: no hidden fees, no overdraft tricks, and clear communication about what you're getting.

In the crowded UK digital banking space, Starling stands apart through consistent execution and a focus on solving real problems rather than chasing hype. It's profitable, self-sufficient, and treated by legacy banks as a genuine competitor rather than a novelty. For European fintechs, Starling represents the successful blueprint: regulated, capital-efficient, and genuinely preferred by millions of users who value simplicity over flashiness.

As the fintech landscape matures, Starling exemplifies the shift from disruption theater to sustainable banking infrastructure—a reminder that the most radical innovation often looks deceptively simple.

Pockit

Digital Banking🇬🇧 United Kingdom

Pockit is a mobile-first financial platform designed for people who've been locked out of traditional banking. Rather than chasing the affluent, Pockit focuses on the underbanked—those without access to a current account, credit history, or the documentation banks demand. The app serves as a genuine alternative to brick-and-mortar banking, offering digital accounts, card payments, and money management tools entirely through your phone.

What sets Pockit apart is its commitment to financial inclusion without the gatekeeping. You don't need a credit score or payslip to open an account. Instead, the platform builds trust through usage patterns and behavioral data, creating pathways for people traditionally rejected by high street banks. This shifts the relationship from one of suspicion to one of genuine access.

The company operates across the UK and Europe, proving that underserved segments aren't just a niche—they're a substantial market. Pockit's mission is radical in its simplicity: banking shouldn't require jumping through hoops or having the right background. It's a challenger in the truest sense, not because it offers flashy features, but because it solves a real problem for millions of people who simply want to participate in the financial system.

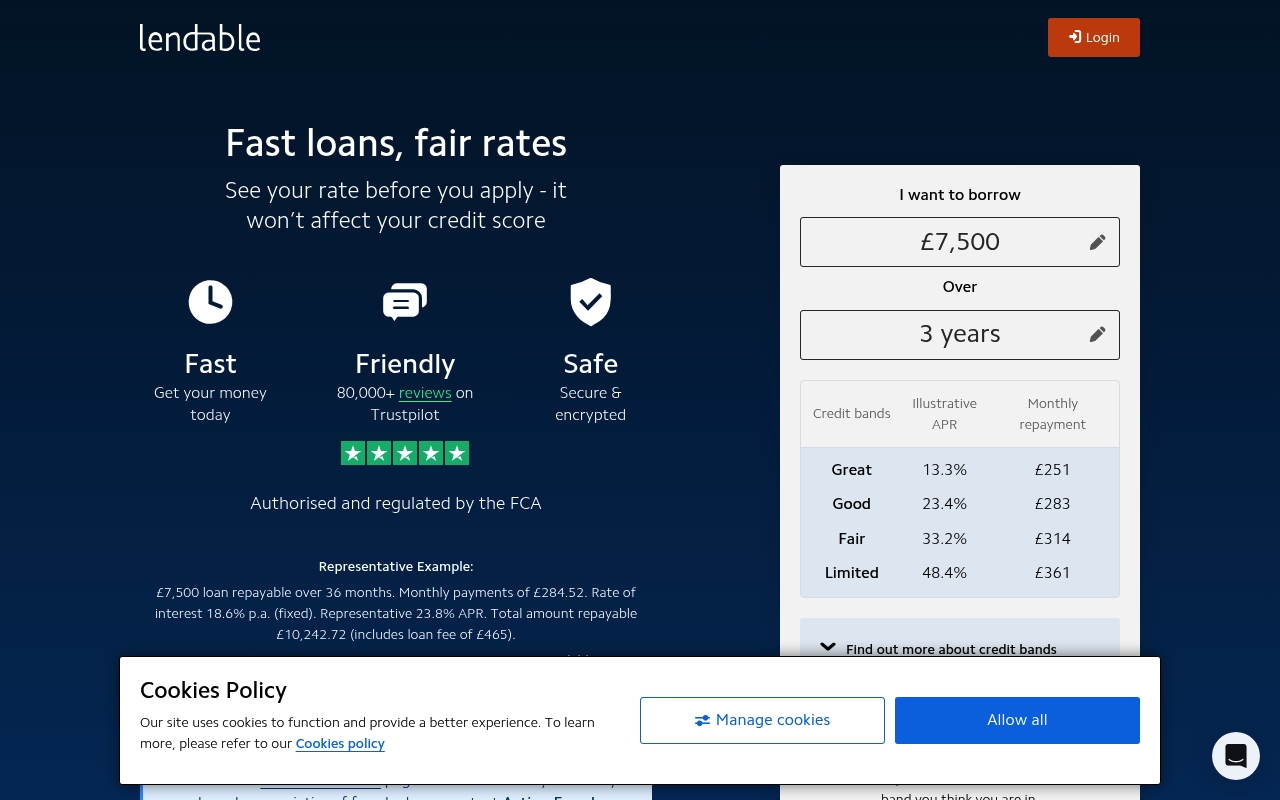

Lendable

Financial Infrastructure🇬🇧 United Kingdom

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates.

The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets.

In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names.

Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

GoHenry

Payments🇬🇧 United Kingdom

GoHenry gives children and teens prepaid cards with parental controls.

Zepz

Payments🇬🇧 United Kingdom

Zepz powers international money transfers through WorldRemit and Sendwave.

LemFi

Payments🇬🇧 United Kingdom

LemFi provides money accounts and remittances for immigrant communities.

Checkout.comFeatured

Embedded Finance🇬🇧 United Kingdom

Checkout.com is a global payments infrastructure company that builds the plumbing beneath the surface of e-commerce. While most payment processors still operate like legacy banking rails, Checkout.com has constructed a single API that connects directly to card networks, acquiring banks, and alternative payment methods—eliminating the middlemen that slow everything down. The platform processes payments in over 150 currencies across 195 countries, handling everything from straightforward card transactions to complex multi-currency settlements for merchants operating at scale.

What sets it apart in Europe and beyond is its refusal to be a typical payment gateway: instead of asking merchants to adapt to the network, Checkout.com adapts the network to the merchant. Founded in 2012 by Guillermo Gutiérrez García-Ceballos, the company has grown from a London-based startup into a critical piece of infrastructure for enterprises, fintechs, and marketplaces that need orchestration at the transaction level. It competes with traditional acquirers and modern payment platforms by combining the reliability of legacy banking with the speed and flexibility developers expect.

In the fragmented European payments landscape, Checkout.com has become indispensable for companies that refuse to compromise on latency, coverage, or control. The company represents a fundamental shift in how payments should work: less about choosing between payment methods and more about making payments invisible.

Funding Circle

Lending🇬🇧 United Kingdom

Funding Circle sits at the intersection of institutional capital and small business ambition. The platform connects SMEs with investors—funds, banks, and individuals—who want returns tied to real economic activity rather than abstract asset classes. It's fundamentally a marketplace, but one that's spent years learning how to assess credit risk at scale, price loans competitively, and move money across borders without the friction traditional finance demands.

The company operates across multiple geographies, though Europe remains central to its strategy. It handles everything from loan origination and underwriting through to servicing and portfolio management, meaning it's built real infrastructure rather than just matching borrowers to lenders. This matters because it allows institutional investors to actually understand what they're funding.

Funding Circle competes in a space where traditional banks have historically been absent—the mid-market lending gap where a £50,000 loan isn't big enough for a relationship manager but too important for a business to ignore. Alternative lenders have crowded this space, but Funding Circle's institutional backing and regulatory maturity give it a structural advantage. It's moved from pure peer-to-peer model toward a more hybrid approach, partnering with regulated lenders to expand reach while maintaining its marketplace credibility.

The company represents a fundamental rethinking of how capital reaches productive SMEs—not through gatekeepers, but through platforms that make risk transparent and pricing efficient.