← Back to Friday

Alternatives

Alternatives to Friday

Explore 8 European fintech companies similar to Friday — operating in InsurTech.

8 alternatives to Friday

Sorted by similarity and popularitywefox

InsurTech

🇨🇭 Switzerland

Wefox is a digital insurance broker that cuts through the noise of traditional insurance shopping. Rather than piecing together quotes from multiple providers, customers get personalized coverage recommendations through a streamlined mobile-first platform. The company bundles home, auto, and pet insurance into a single digital experience, handling everything from comparison to claims—no brokers in grey suits required.

What sets wefox apart in Europe's insurance landscape is its focus on simplicity. While legacy brokers still rely on phone calls and paperwork, wefox does the legwork algorithmically, comparing hundreds of policies in seconds and presenting only the relevant options. The interface feels less like insurance shopping and more like opening a fintech app.

The company operates across multiple European markets, building a tech-forward alternative to the tired insurance broker model. It's positioned as insurance for people who'd rather not think about insurance—until they need to claim. In the broader fintech ecosystem, wefox represents a straightforward play on distribution innovation: taking an opaque, offline-first industry and making it transparent, fast, and mobile-native.

Founded 2015

View profile →

Coverflex

Digital BankingInsurTechSME Finance

🇵🇹 Portugal

Coverflex is rewriting how freelancers and gig workers access financial security in Europe. Instead of the traditional employment model, the platform bundles flexible work with genuine benefits—health insurance, pension contributions, and paid leave—creating a middle path between employment and total independence.

The company essentially flips the script on gig economy precarity. Workers stay independent contractors but gain access to protections that were previously locked behind 9-to-5 employment. Employers get a simpler way to hire flexible talent without managing traditional payroll complexity. It's a fundamentally different architecture for modern work.

Coverflex operates across multiple European markets and has built a B2B2C model where companies use the platform to offer benefits to their contractor workforce. The business combines insurance brokerage, financial services coordination, and workplace infrastructure into one interface.

In a landscape where gig work remains fragmented and precarious, Coverflex sits at the intersection of fintech and HR tech, solving a genuine gap in how Europe's growing contingent workforce accesses security and stability.

Founded 2020

View profile →

Zego

InsurTech

🇬🇧 United Kingdom

Zego sells insurance built for the gig economy—a category that barely existed five years ago and now moves faster than traditional underwriting can handle. The London-based insurtech operates in a space where traditional insurers still treat gig workers as afterthoughts, bundling them into outdated categories. Zego flips this. It offers flexible, pay-as-you-go coverage for delivery riders, couriers, and other flexible workers across Europe, with pricing that reflects actual usage rather than punishing people for working on their own terms.

The product feels native to how gig workers actually live. Rather than forcing annual commitments or minimum coverage periods, Zego lets users activate insurance by the hour or day, paying only for what they use. The claims process is digital and friction-light—something traditional insurers have promised but rarely delivered. Behind the interface sits real underwriting AI that prices risk dynamically, allowing Zego to write policies that make sense for both the worker and the business.

In Europe's fragmented insurance market, Zego stands apart from pure distribution plays and legacy brokers by owning the underwriting function. It's not an aggregator slapping a UI on existing products; it's a real insurer rethinking the fundamentals. The company has grown quickly because it identified a timing mismatch: millions of people already working in the gig economy waiting for insurance that matched their reality, not their employment status.

Zego represents the emerging pattern in European insurtech: not trying to replace all insurance, but dominating one slice deeply and building unit economics that work. It's carved out a defensible position in a category that traditional players still don't quite understand.

Founded 2016

View profile →

Teylor

InsurTech

🇩🇪 Germany

Teylor is building the infrastructure layer for European insurers who've spent decades trapped in legacy systems. Rather than asking them to rip and replace everything, Teylor plugs into their existing architecture as an API-first, cloud-native alternative—handling policy administration, billing, and customer management with the speed and flexibility that modern insurance demands.

The company targets mid-market and larger insurers across Europe who need to move faster but can't afford the operational risk of wholesale transformation. Teylor's approach is pragmatic: you don't need to become a fintech startup to compete like one. Instead, you layer in modern tools where they matter most and keep your proven processes intact.

In a market where InsurTech typically means either a scrappy direct-to-consumer challenger or a consulting-heavy legacy modernization play, Teylor sits in a more interesting middle ground—enterprise-grade software that actually feels like it was built in the last decade. For traditional insurers tired of vendor lock-in and staggering implementation timelines, it represents a credible path to digital without the existential risk.

Founded 2019

View profile →

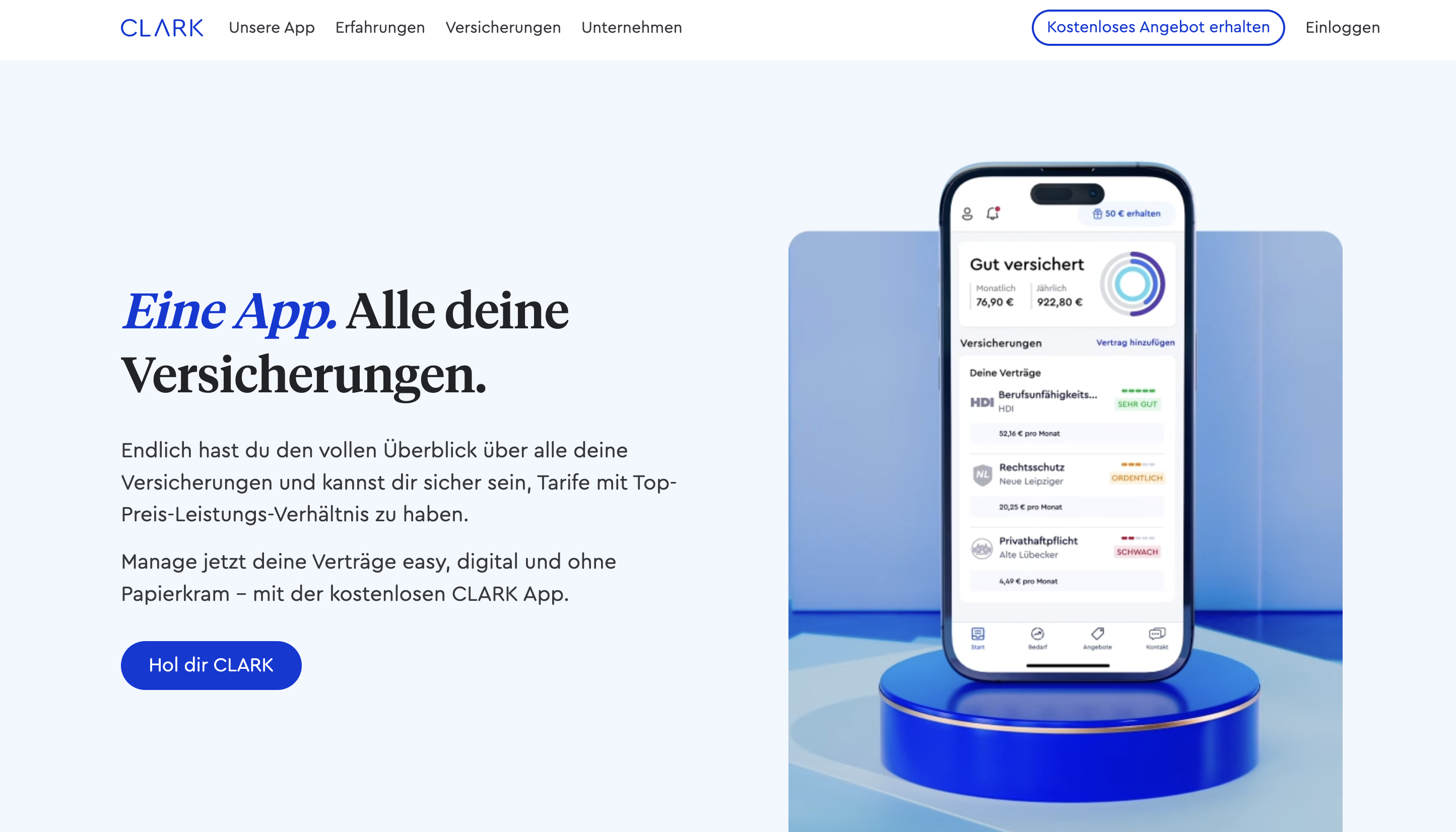

Clark

InsurTech

🇩🇪 Germany

Clark is disrupting the messy business of insurance administration in Germany, Austria, and Switzerland by giving customers a single digital interface to manage all their policies—regardless of which insurer they're with. Rather than forcing people to juggle multiple providers and renewal notices, Clark aggregates everything into one place and handles the administrative grunt work: comparing coverage, finding better deals, and switching policies when it makes sense.

The app has become the go-to way for tens of thousands of Europeans to actually understand what they're paying for and stop overpaying. What sets Clark apart is that it doesn't just manage policies after you buy them—it actively renegotiates on your behalf, leveraging collective bargaining power to find cheaper rates across competitors. You authorize the switch, Clark handles the paperwork. Most insurance platforms either sell you products or help you compare; Clark does neither. Instead, it sits between you and the entire market, keeping your interests first and taking a commission only when it saves you money. The company has essentially made insurance administration feel like it's from the 2020s rather than the 1990s. For millions of Europeans stuck with scattered policies, outdated coverage, and premium shock every renewal cycle, Clark has become infrastructure.

Founded 2015

View profile →

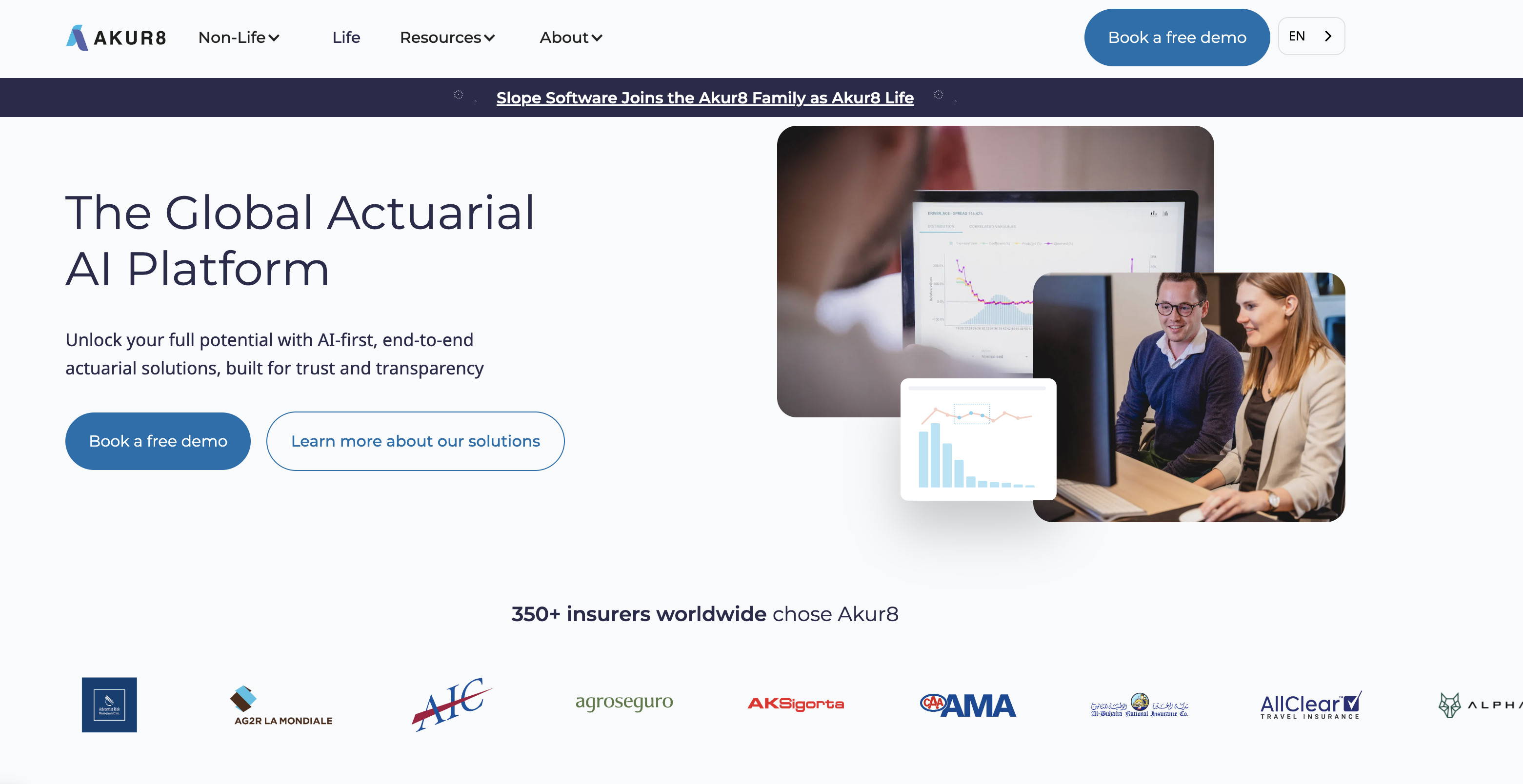

Akur8

InsurTech

🇫🇷 France

Akur8 is an AI-powered insurance underwriting platform that automates and accelerates pricing decisions for insurers. Rather than relying on traditional actuarial models that can take months to build and update, Akur8 uses machine learning to rapidly discover optimal pricing strategies from historical claims data, enabling insurers to compete faster and adapt to market shifts in weeks rather than quarters.

The platform is built for underwriters and actuaries who are tired of being bottlenecked by legacy systems. Akur8 sits between an insurer's data warehouse and their pricing engine, learning patterns that humans might miss and generating transparent, explainable models that regulators will actually approve. The company positions itself as the bridge between insurance's analog past and a data-driven future.

In the European insurance market, where digitalization remains patchy and many carriers still rely on spreadsheet-heavy workflows, Akur8 stands out by being genuinely usable—not just technically sophisticated, but designed for the reality of how insurance actually operates. Its customers include major European insurers looking to modernize underwriting without dismantling their entire infrastructure.

The company represents a broader shift toward embedded AI in financial services, where the technology doesn't replace humans but makes them exponentially more effective at their core job: pricing risk accurately.

Founded 2016

View profile →

Alan

InsurTech

🇫🇷 France

Alan is rewriting health insurance for the digital age, stripping away the bureaucratic drag that makes traditional coverage feel like a relic.

The Paris-based insurtech startup treats health protection as something that should integrate seamlessly into daily life rather than a quarterly bill you dread opening. Using AI and real-time data, Alan automates claims processing, cuts administrative friction, and lets users manage their coverage through a clean mobile app. What sets Alan apart is its focus on speed and transparency. Most European health insurers still operate like they're managing paper files; Alan processes claims in days, not months, and explains costs upfront instead of hiding them in fine print.

The company serves both individuals and SMEs across France, Belgium, Spain, and beyond, positioning itself as the insurance provider for people who actually understand technology. In a market where health insurance feels synonymous with frustration, Alan's role is to prove that coverage can be simple, fast, and genuinely customer-centric.

Founded 2016

View profile →

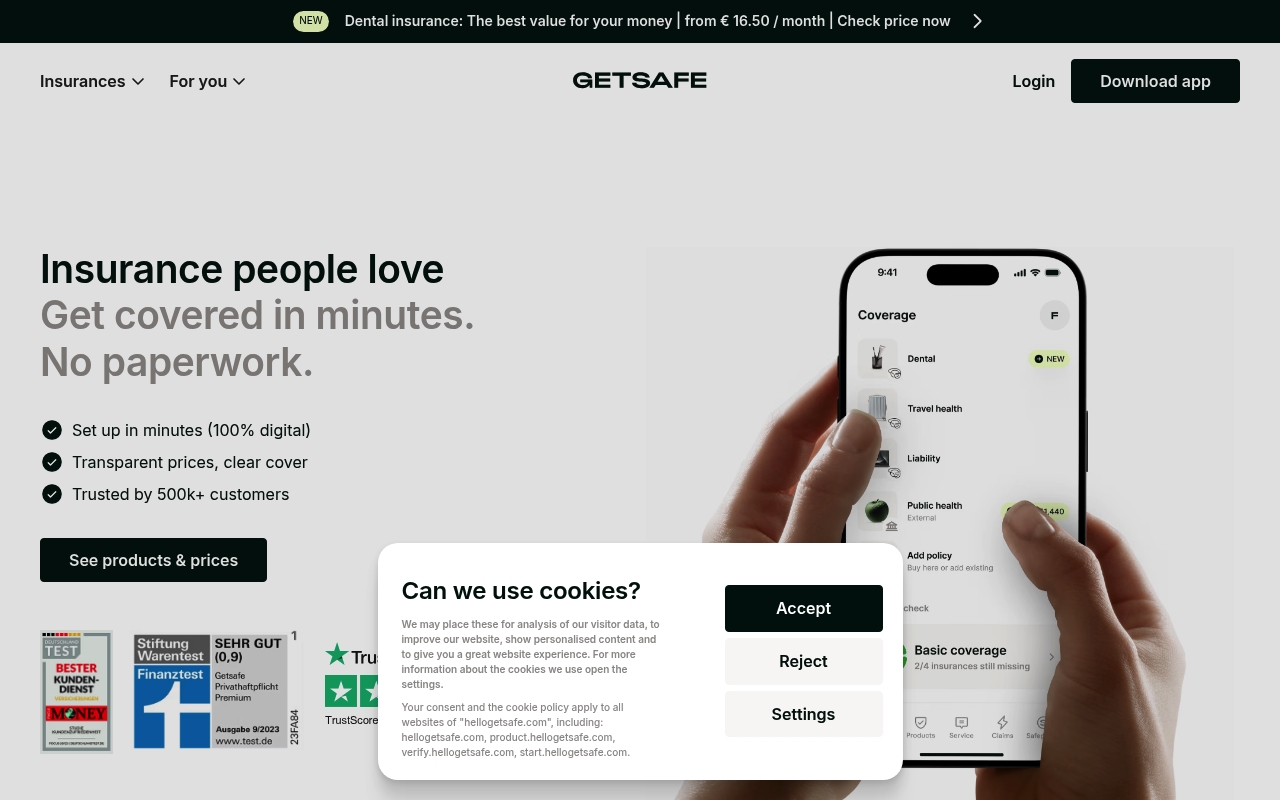

Getsafe

InsurTech

🇩🇪 Germany

Getsafe is building insurance for the digital age, stripping away the complexity and paperwork that make traditional coverage feel like a relic. Founded on the premise that buying insurance shouldn't require a PhD in fine print, the Berlin-based insurtech has made it possible to buy, manage, and claim on policies entirely through a smartphone app. The company doesn't issue policies itself—it partners with licensed insurers—but it's reimagined every touchpoint of the experience, from onboarding (minutes, not hours) to claims (AI-powered and often resolved instantly). Where legacy insurers still operate like bureaucracies, Getsafe feels like a consumer product.

The startup has quietly built a loyal user base across Germany, France, Spain, and Austria by targeting younger, digitally-native consumers who would rather avoid call centres altogether. Its approach is deliberately inclusive: pricing is transparent, policies are customizable, and the app handles everything from renewal reminders to claims documentation in a friction-free way. Unlike traditional insurance companies that treat digital as an afterthought, Getsafe is built digital-first from the ground up. The company generates revenue through commission-based partnerships with insurers and through incremental service fees.

In a category historically dominated by incumbents and tied to physical distribution, Getsafe represents a quiet but meaningful shift toward consumer-centric insurance platforms. It's not disrupting the regulatory infrastructure of insurance, but it's successfully disrupting how people interact with it—proving that a better app can win even in one of Europe's most conservative financial sectors.

Founded 2015

View profile →