← Back to Invesdor

Alternatives

Alternatives to Invesdor

Explore 12 European fintech companies similar to Invesdor — operating in Wealth and Capital Markets and SME Finance.

12 alternatives to Invesdor

Sorted by similarity and popularityCapdesk

Capital MarketsSME Finance

🇬🇧 United Kingdom

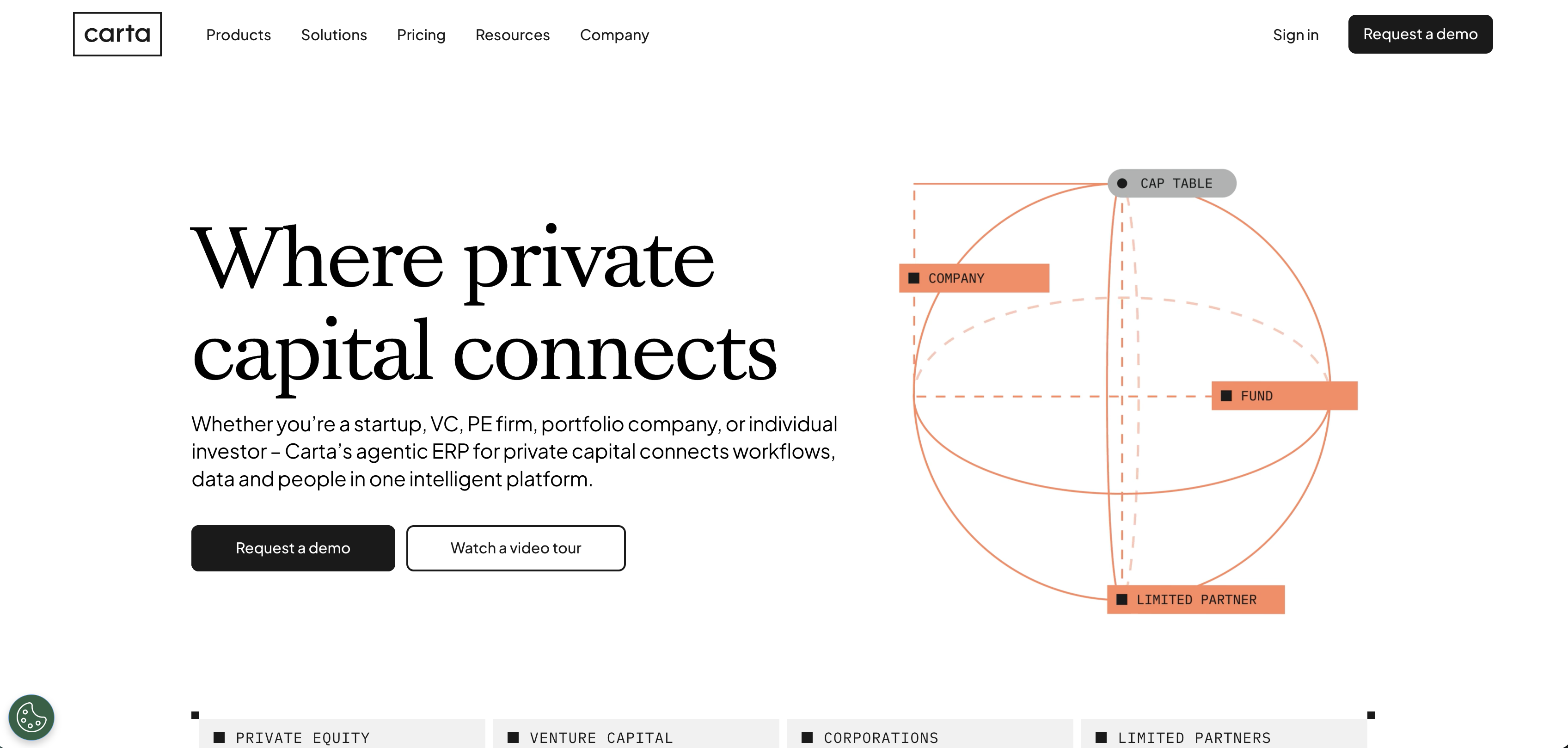

Equity management for private companies has historically been a mess of spreadsheets, lawyer markup, and reconciliation errors that compound silently until a fundraising round forces everyone to discover that the cap table reality differs from the cap table on file. Capdesk was founded in Copenhagen and grew up in London from 2015, building equity management software for private companies — a single source of truth for share allocations, option grants, vesting schedules, and shareholder communications. The product targets the gap between an Excel spreadsheet and a full-blown share registry: too small for the latter, too important to entrust to the former. Capdesk has built a strong client base across UK and European startups and scaleups, becoming one of the more trusted equity management platforms in Europe. The company was acquired by US-based Carta in 2023, consolidating the European equity management market under the umbrella of one of its largest global players. The acquisition reflects a broader pattern in private market infrastructure — the platforms that manage equity, fundraising, and investor relations are consolidating around a small number of comprehensive solutions. For European companies that built on Capdesk, the Carta acquisition brings them into a global platform with broader functionality at the cost of the local independence that some clients valued.

Founded 2015

View profile →

Revolut

WealthPaymentsDigital BankingCrypto & BlockchainPersonal Finance

🇱🇹 Lithuania

Nik Storonsky grew up moving between Russia and France before landing in London as a derivatives trader. Vlad Yatsenko was a software engineer who'd spent years building financial systems. In 2015 they sat down and asked a question that should have occurred to banks years earlier: why does spending money abroad still cost so much?

The answer they built was Revolut — initially a prepaid card with no foreign exchange fees, then a multi-currency account, then a trading platform, then an insurance product, then a business banking offering, then something that's increasingly hard to describe as anything other than a full financial operating system. Revolut didn't unbundle banking so much as rebuild it from scratch for people who found the existing version frustrating and expensive.

The numbers now are genuinely striking for a company that started with two people and a card. Revenue reached £4.5 billion in 2025, up 46% year on year, with net profit of £1.3 billion. The customer base grew to 68.3 million retail users — one in five working-age adults in Europe — plus 767,000 businesses. The company employs 12,200 people across more than 25 countries and was valued at $75 billion in a November 2025 secondary share sale, making it Europe's most valuable private technology company.

The milestone that mattered most, though, arrived in March 2026: a full UK banking licence from the Prudential Regulation Authority, ending a three-year application process that had become the most-watched regulatory saga in European fintech. The licence means Revolut can now protect UK deposits up to £120,000, offer authorised consumer credit, and compete directly with high street banks for mortgage and lending business. It's the piece that transforms Revolut from a very successful payments app into a regulated bank.

The company has also applied for a US banking charter and is expanding aggressively into Latin America, having opened its first bank outside Europe in Mexico. The original thesis — that banking could be cheaper, faster, and simpler — hasn't changed. The scale at which it's now being tested has.

Founded 2015

View profile →

Monzo

WealthDigital BankingLendingPersonal Finance

🇬🇧 United Kingdom

The founding team that built Monzo had all worked together before — at Starling Bank, another challenger bank startup that didn't survive its internal conflicts. Tom Blomfield, Gary Dolman, Jonas Huckestein, Jason Bates, and Paul Rippon left Starling together in 2015 and started again. The product they built was initially a prepaid card — a coral-coloured piece of plastic that became one of the most recognisable objects in British fintech — before becoming a fully licensed current account in 2017.

The early user community was unusual for a bank. Monzo ran community forums, published public blog posts about its engineering decisions, and invited customers into beta programmes for new features. When it broke the world record for the fastest crowdfunding raise in 2016 — £1 million in 96 seconds — it wasn't just raising money; it was building an identity. People felt ownership of the product in a way that no high street bank had ever managed to create. That emotional connection became a genuine competitive advantage.

The product has matured considerably since then. Monzo now offers current accounts, joint accounts, savings pots, personal loans, overdrafts, and investment products, all wrapped in the real-time notification experience and transaction categorisation that made its early reputation. Revenue reached £1.23 billion in 2024, up 40% year on year, with net income of £95 million — the second consecutive year of profitability after years of growth-first losses. The customer base reached 12.1 million by end of 2024, making Monzo the UK's largest digital bank by customer count. Customer deposits stood at £16.6 billion.

The business is still private — the much-discussed IPO has not yet happened, and internal disagreements about where to list (the former CEO TS Anil favoured the US, the board preferred London) contributed to Anil's departure in October 2025. Diana Layfield took over as CEO with a mandate focused on international expansion before any public listing. The company is valued at approximately $5.9 billion following a 2024 secondary sale backed by Alphabet's GIC and StepStone.

In December 2025 Monzo announced it had agreed to acquire Habito, the digital mortgage broker, pending regulatory approval — a move that extends the product into one of the last major financial products it didn't yet offer. With 3,821 employees and a loan book growing rapidly, Monzo has evolved from a prepaid card experiment into a bank with genuine scale and a growing claim on being the primary financial account for a generation of UK consumers.

Founded 2015

View profile →

SumUp

Financial InfrastructurePaymentsDigital BankingSME Finance

🇩🇪 Germany

SumUp is Europe's answer to the merchant services problem: a scrappy fintech that turned point-of-sale payments into something actually accessible. While legacy payment processors still treat small businesses like second-class customers, SumUp built hardware and software that work together seamlessly, letting anyone from a street vendor to a café owner accept cards in minutes, not months.

The company started by selling cheap card readers—simple, elegant devices that plugged into phones. But that was just the wedge. Today SumUp offers a stack: card readers, invoicing, basic accounting, and increasingly, working capital tools. It's the financial operating system for the SME who doesn't want to negotiate with a relationship manager.

What sets SumUp apart in Europe is its refusal to stay in the payments lane. Most competitors eventually build one feature and call it a day. SumUp keeps layering—acquiring merchant acquirer licenses, launching its own acquiring infrastructure in key markets, adding payment links and e-commerce solutions. The company operates across Western Europe and beyond, working with hundreds of thousands of merchants who are too small for traditional banking but too important to ignore.

SumUp represents the practical, unglamorous evolution of fintech: it's not trying to reinvent banking or blockchain. It's solving the cash flow problem for people who actually run businesses. That's a bigger opportunity than it sounds.

Founded 2012

View profile →

Starling Bank

Digital BankingSME FinancePersonal Finance

🇬🇧 United Kingdom

Starling Bank is a British challenger bank that stripped away the friction of traditional banking and rebuilt it around what modern customers actually need: instant notifications, real-time spending insights, and accounts you can open in minutes without stepping into a branch. Founded in 2014, it operates as a fully regulated bank with its own banking license, not just a wrapper around legacy infrastructure.

The platform serves both consumers and SMEs, offering straightforward current accounts, savings pots, and increasingly sophisticated business banking tools. Unlike neobanks reliant on partnerships, Starling owns its core infrastructure, which means faster iteration and tighter product control. The company has built a reputation for no-nonsense transparency: no hidden fees, no overdraft tricks, and clear communication about what you're getting.

In the crowded UK digital banking space, Starling stands apart through consistent execution and a focus on solving real problems rather than chasing hype. It's profitable, self-sufficient, and treated by legacy banks as a genuine competitor rather than a novelty. For European fintechs, Starling represents the successful blueprint: regulated, capital-efficient, and genuinely preferred by millions of users who value simplicity over flashiness.

As the fintech landscape matures, Starling exemplifies the shift from disruption theater to sustainable banking infrastructure—a reminder that the most radical innovation often looks deceptively simple.

Founded 2014

View profile →

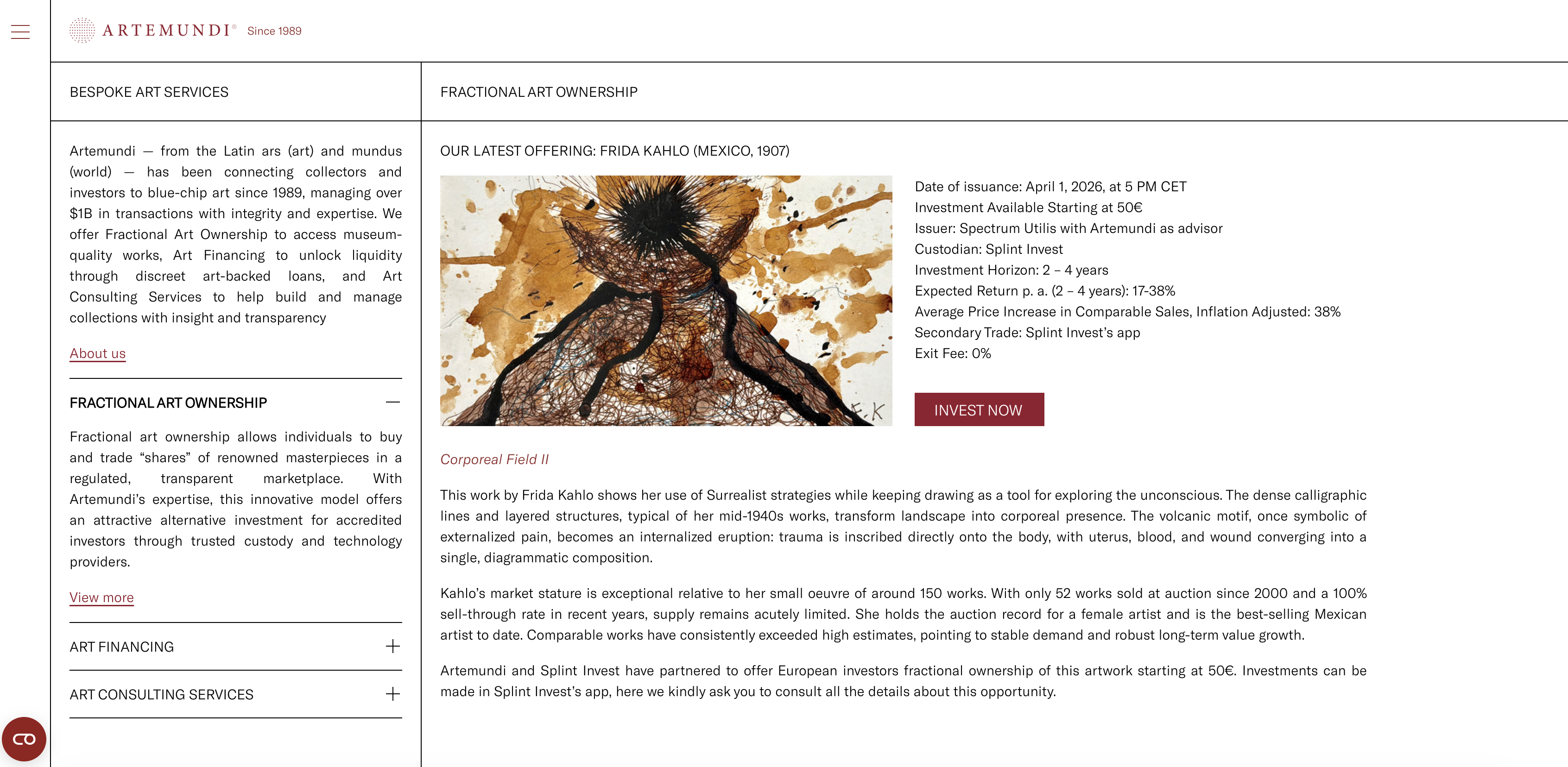

Artemundi

Wealth

🇩🇪 Germany

Artemundi is an alternative asset manager built for the modern wealth ecosystem. Rather than chasing traditional markets, the firm specializes in emerging market debt, private equity, and distressed assets—seeking returns where conventional investors see opacity. It's positioned at the intersection of hedge fund sophistication and institutional rigor, attracting wealth managers and sophisticated investors who understand that real returns often live outside the mainstream.

The company runs multiple investment vehicles targeting different risk appetites and timeframes, each managed with the discipline of a tier-one institutional shop. Their approach combines deep emerging market expertise with operational rigor, allowing them to navigate complexity that smaller competitors cannot. This isn't retail wealth management repackaged; it's institutional-grade alternative investing for those who can access it.

In the European wealth tech landscape, Artemundi represents the alternative asset class gatekeepers—firms that manage substantial capital across non-traditional strategies. While the fintech world obsesses over fractional shares and gamified trading, Artemundi operates in the space where serious capital allocation happens. They cater to family offices, pension funds, and institutional investors who view alternative assets as core portfolio components rather than exotic bets.

The firm embodies a particular European investment philosophy: skepticism of index-heavy approaches, appetite for frontier markets, and belief that skilled managers can exploit inefficiencies where passive strategies cannot. In an era of wealth fragmentation and advisor tech disruption, Artemundi remains a destination for institutional-grade alternative returns.

View profile →

Trade Republic

WealthDigital BankingPersonal Finance

🇩🇪 Germany

Trade Republic has fundamentally rewritten the script for European retail investing. Where traditional brokers demanded minimums, paperwork, and fees that could swallow returns, this Berlin-based neobroker arrived in 2015 with a smartphone app and a radical premise: investing should cost almost nothing and take seconds.

The platform trades stocks, ETFs, and fractional shares across multiple European exchanges with zero commissions. Its core strength is simplicity—the interface strips away complexity while maintaining the depth serious investors expect. Execution is fast, the fee structure is transparent (mostly subscription-based rather than per-trade), and the onboarding process reflects modern expectations around speed and convenience.

Trade Republic sits at the convergence of neobanking and trading. While competitors like Revolut added trading as a secondary feature, Trade Republic built the entire experience around it. The company holds banking licenses across multiple EU jurisdictions, giving it the infrastructure to manage cash, offer savings features, and issue debit cards—all in service of becoming a financial operating system for young Europeans.

Its expansion beyond trading into banking products reflects a broader industry shift: the most valuable fintech companies aren't specialists anymore. They're ecosystems. Trade Republic's role in the European fintech landscape is as a proof of concept that direct-to-consumer wealth management, executed with design discipline and regulatory precision, can scale rapidly while maintaining unit economics that would make traditional brokers blush.

Founded 2015

View profile →

Qonto

PaymentsDigital BankingSME Finance

🇫🇷 France

Qonto is a European business banking platform that treats SMEs and freelancers the way tech-forward founders wish their banks would: fast, transparent, and built for how modern companies actually operate. Instead of waiting days for payments to clear or wrestling with legacy banking interfaces, Qonto users get instant payments, real-time visibility across their accounts, and integrations that sync seamlessly with their existing tools.

The platform lives at the intersection of traditional banking and fintech simplicity. Qonto handles everything from multi-currency accounts and payment processing to expense management and financial reporting, all from a mobile-first interface that feels like an app, not a bank. The company has quietly become the go-to choice for growing SMEs across Europe who want banking that doesn't slow them down.

What sets Qonto apart in a crowded B2B banking space is its obsessive focus on the user experience and its commitment to European expansion. While many neobanks either chase mass-market consumers or hide behind enterprise complexity, Qonto sits in a sweet spot: accessible enough for a solo founder, powerful enough for teams managing millions in annual revenue. The company's growth across France, Germany, Spain, Italy, and beyond reflects a simple truth: European businesses have been waiting for a bank that understands their needs.

As European business banking undergoes its biggest transformation in decades, Qonto stands as proof that the future of SME finance isn't about moving fast and breaking things—it's about moving fast and building things that actually work.

Founded 2016

View profile →

Tinaba

WealthPaymentsDigital Banking

🇮🇹 Italy

Tinaba offers mobile banking, payments, and investment services in Italy.

View profile →

Bitpanda

WealthCrypto & BlockchainPersonal Finance

🇦🇹 Austria

Bitpanda is a Vienna-based fintech that democratized crypto investing for European retail users who found traditional exchanges intimidating or inaccessible. The platform launched in 2014 as a Bitcoin marketplace and evolved into a multi-asset investment app that lets anyone buy fractions of crypto, stocks, metals, and commodities with a few taps on their phone.

What sets Bitpanda apart is its aggressive focus on the everyday investor rather than crypto enthusiasts. The app strips away complexity, offers micro-investing (you can buy €1 worth of Bitcoin), and integrates savings automation through its Bitpanda Savings feature. It's become a household name in German-speaking Europe, with a clean mobile-first interface that appeals to younger savers who want exposure to alternative assets without the friction of traditional brokerages.

Bitpanda operates across multiple business units: a consumer investment app, an institutional trading platform called Bitpanda Pro, and Bitpanda Elements, its white-label infrastructure play for financial institutions. The company expanded beyond crypto into traditional asset classes to capture a broader addressable market and hedge regulatory risk as European crypto rules tightened.

Among European retail investment platforms, Bitpanda ranks as a serious contender—well-funded, profitable, and operating under tight regulatory scrutiny. It represents a shift in how Europeans think about alternative investments: not as speculative sidebets but as legitimate wealth-building tools accessible to anyone with a smartphone.

Founded 2014

View profile →

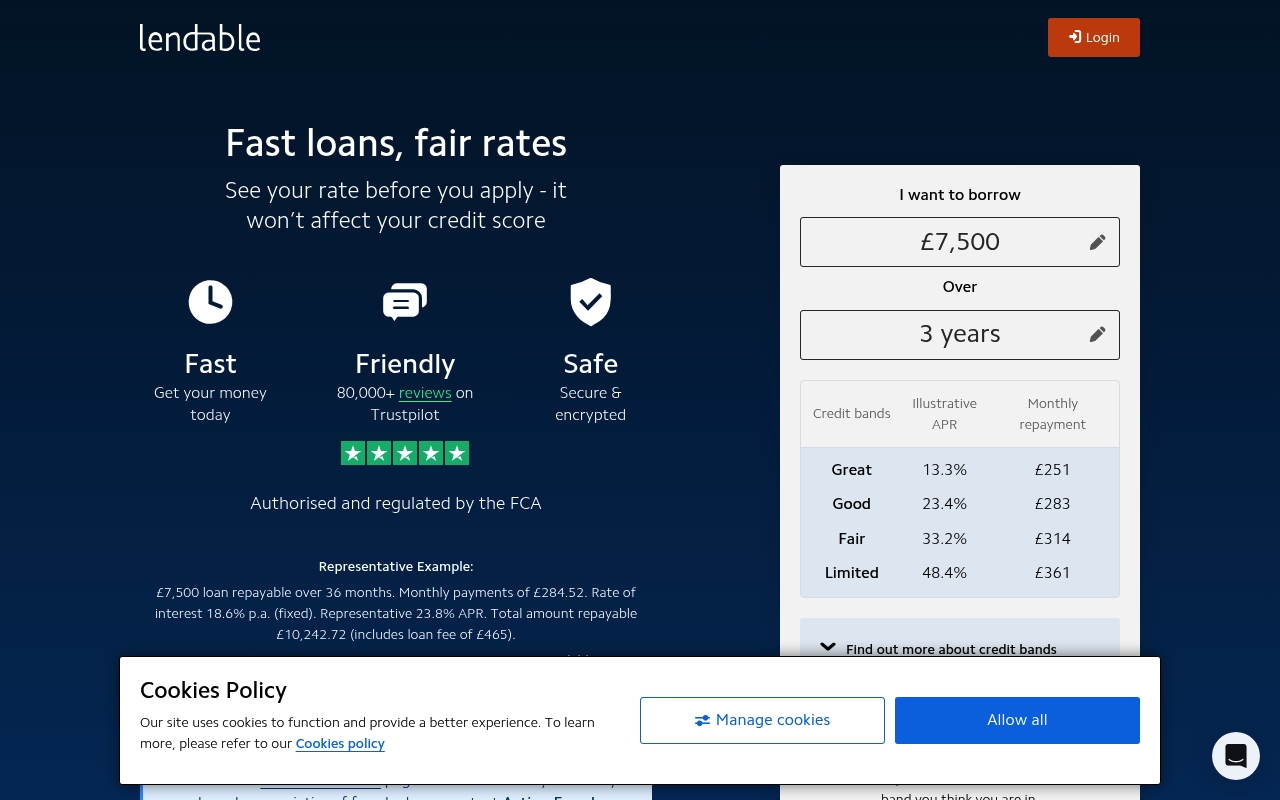

Lendable

Financial InfrastructureCapital MarketsLending

🇬🇧 United Kingdom

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates.

The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets.

In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names.

Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

Founded 2013

View profile →

PayFit

SME Finance

🇫🇷 France

PayFit is a French payroll and HR software platform that automates the tedious work of managing employee compensation, benefits, and compliance across Europe. Founded in 2015, the company has built something genuinely useful: a system that lets mid-market companies and SMEs stop wrestling with spreadsheets and outdated payroll systems, and instead manage their entire workforce in one place.

The platform handles everything from salary calculations and tax filings to expense reports and leave management—work that traditionally demanded a dedicated HR department or expensive outsourcing. What sets PayFit apart is its focus on reducing administrative friction rather than just digitizing existing processes. The interface feels designed for actual users, not consultants. It integrates with accounting software and handles the increasingly complex regulatory landscape across France, Germany, Spain, and the UK, where employment law differs wildly but payroll headaches remain universal.

In Europe's fragmented payroll software market, where legacy providers still dominate through inertia, PayFit represents a generational shift toward cloud-first, mobile-friendly HR operations. The company competes less on features (though it has plenty) and more on making payroll feel like a solved problem rather than an annual migraine. It's the kind of infrastructure play that startups and growth companies build themselves around once they've used it—not flashy, but fundamentally necessary.

Founded 2015

View profile →