← Glossary

What is BNPL?

Buy Now Pay Later — BNPL — is the payment method that allows consumers to receive goods or services immediately and pay over a fixed number of instalments, typically interest-free if paid on time. The category grew explosively across Europe in the late 2010s and early 2020s, driven by e-commerce growth, changing consumer attitudes toward credit, and the commercial reality that BNPL at checkout measurably increases conversion rates and average order values for merchants. Regulatory scrutiny has intensified: the updated Consumer Credit Directive brings BNPL explicitly under consumer credit regulation in the EU from 2026, requiring affordability assessments and standardised disclosures.

Subcategories

SME BNPL

Instalment lending

Credit lines

Retail BNPL

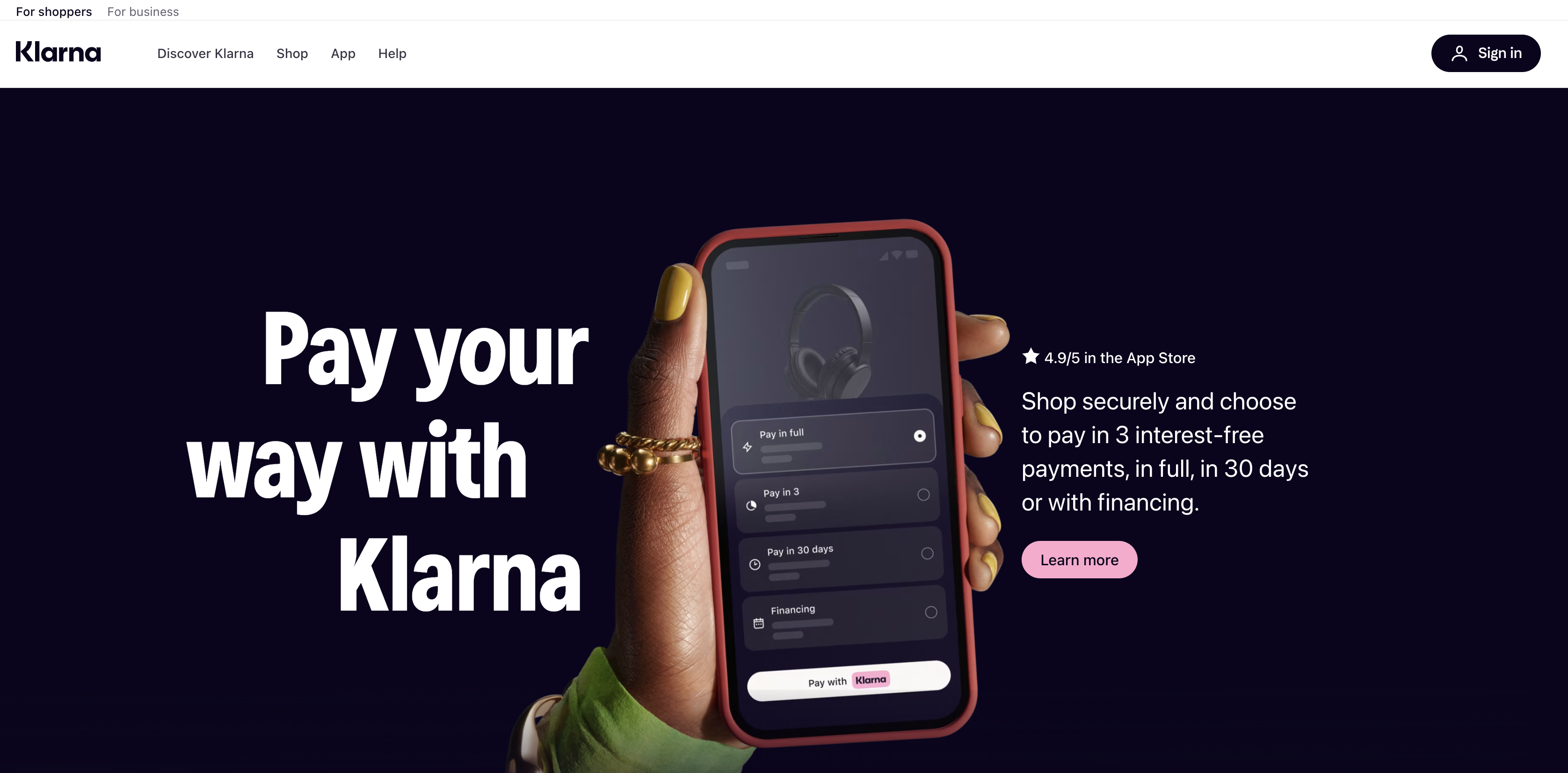

Retail BNPL is the consumer-facing instalment payment product integrated into e-commerce and physical retail checkouts. A customer splits their purchase into three or four equal payments over six to eight weeks — typically interest-free if paid on time. Merchants pay a percentage fee and receive full payment upfront.

Checkout financing

Checkout financing encompasses the broader category of credit products offered at the point of purchase — including instalment plans, deferred payment options, and longer-term financing for larger purchases like furniture, electronics, and travel where consumers may want six to twenty-four month payment plans.