What is Financial Infrastructure?

Financial infrastructure companies build the core systems on which financial institutions run — core banking platforms, payment processing engines, middleware, data infrastructure, and the API layers that connect legacy banking systems to modern fintech products. These are not consumer-facing products; they are the foundational technology that banks, payment companies, and fintechs build their customer offerings on top of. The cloud banking market in Europe is dominated by a small number of well-capitalised players including Mambu and Thought Machine, operating in a high-barriers, high-value market where clients are institutions with long procurement cycles and significant technical requirements.

European Financial Infrastructure companies in our database

Pieter van der Does and Arnout Schuijff had already built and sold one payments company when they sat down in 2006 to start again. The result was Adyen — the name literally means "start over" in Surinamese — and the premise was simple: instead of stitching together the same fragmented payment infrastructure everyone else was using, they would build the whole thing themselves from scratch. That decision, made in an Amsterdam office nearly two decades ago, is still the reason Adyen is different. Most payment companies are assemblers — they buy a gateway here, a processor there, bolt them together and hope for the best. Adyen owns its own technology stack end to end, which means a merchant integrating once gets access to card processing, local payment methods, point-of-sale terminals, and real-time settlement data through a single platform. No middle layers, no reconciliation headaches, no finger-pointing between vendors when something breaks. The client list tells you everything about where Adyen sits in the market. McDonald's, Spotify, Microsoft, LVMH, H&M — these are companies with serious payment volumes and zero appetite for systems that don't work. Adyen became the default choice for enterprises that had outgrown the limitations of traditional payment stacks and needed something that could handle global scale without buckling. Since going public on Euronext Amsterdam in 2018, Adyen has grown into one of Europe's most valuable technology companies, with around 4,300 employees across 23 countries and net revenue of just under €2 billion in 2024. It remains headquartered in Amsterdam and consistently profitable — a combination that's rarer in fintech than it should be. For businesses that treat payments as infrastructure rather than an afterthought, Adyen is the benchmark everything else gets measured against.

Adriaan Mol built Mollie's first backend while living with his parents in the Netherlands in 2004. No investors, no office, no team — just a founder and an idea that small businesses deserved a payment integration that didn't require a team of lawyers and a six-month setup process. He bootstrapped it for over fifteen years before taking outside funding in 2019. By then, Mollie had already grown into one of the most important payment platforms in European e-commerce, entirely on the back of a product that developers actually liked using. The proposition is straightforward: one API, one dashboard, and access to the payment methods that actually matter across Europe. That means iDEAL in the Netherlands, Bancontact in Belgium, Klarna and SEPA Direct Debit everywhere, alongside cards, Apple Pay, and a growing list of local methods that would otherwise require separate integrations and separate acquirer relationships. Mollie handles the compliance, the fraud monitoring, and the settlement complexity. Merchants get a clean interface and a single invoice. For the 250,000 businesses using Mollie today — ranging from Gymshark and Wild to local bakeries and market stalls, as CEO Koen Köppen regularly points out — the appeal is less about feature lists and more about what they don't have to think about. European payments are fragmented by design. Every country has its preferred methods, its own regulatory quirks, its own consumer habits. Mollie's job is to make that invisible. The numbers from 2024 reflect a company that has found its model. Revenue reached €214 million, up 28% year on year, with gross profit growing 30% to €115 million and the company returning to positive EBITDA for the first time since 2018. Mollie raised a total of $940 million in funding and was valued at $6.5 billion following its 2021 Series C led by Blackstone. The most significant recent development is the acquisition of GoCardless in December 2025 — bringing the UK-based direct debit specialist into the Mollie group and substantially expanding its recurring payments and bank transfer capabilities across Europe. Combined, the two companies cover a considerable share of European e-commerce payment infrastructure. Mollie is still headquartered in Amsterdam, with around 900 employees across offices in Ghent, London, Lisbon, Munich, Milan, Paris, and beyond.

SumUp is Europe's answer to the merchant services problem: a scrappy fintech that turned point-of-sale payments into something actually accessible. While legacy payment processors still treat small businesses like second-class customers, SumUp built hardware and software that work together seamlessly, letting anyone from a street vendor to a café owner accept cards in minutes, not months. The company started by selling cheap card readers—simple, elegant devices that plugged into phones. But that was just the wedge. Today SumUp offers a stack: card readers, invoicing, basic accounting, and increasingly, working capital tools. It's the financial operating system for the SME who doesn't want to negotiate with a relationship manager. What sets SumUp apart in Europe is its refusal to stay in the payments lane. Most competitors eventually build one feature and call it a day. SumUp keeps layering—acquiring merchant acquirer licenses, launching its own acquiring infrastructure in key markets, adding payment links and e-commerce solutions. The company operates across Western Europe and beyond, working with hundreds of thousands of merchants who are too small for traditional banking but too important to ignore. SumUp represents the practical, unglamorous evolution of fintech: it's not trying to reinvent banking or blockchain. It's solving the cash flow problem for people who actually run businesses. That's a bigger opportunity than it sounds.

Daniel Kjellén and Fredrik Hedberg didn't set out to build infrastructure. Tink started in Stockholm in 2012 as a consumer personal finance app — an attempt to give Swedish bank customers a cleaner view of their money across multiple accounts. It was a reasonable idea that ran into an unreasonable obstacle: getting reliable, consistent data out of European banks was extraordinarily hard. The technical problem turned out to be more interesting than the consumer product. In 2018 they pivoted, shifted focus entirely to the B2B layer, and started selling the very infrastructure they'd been forced to build for themselves. That pivot proved prescient. The EU's PSD2 directive, which came into full effect in 2019, legally required banks to open their data to authorised third parties — creating the regulatory foundation that open banking platforms needed to operate at scale. Tink had spent years building exactly those bank connections. When the regulation arrived, the company was ready. The platform Kjellén and Hedberg built connects to more than 3,400 banks and financial institutions across Europe, reaching over 250 million bank customers. Through a single API integration, banks, fintechs, and merchants can access aggregated account data, initiate payments directly from customer bank accounts, verify account ownership, and enrich transaction data — without maintaining their own connections to hundreds of separate banking systems with different technical standards and update schedules. Clients include Klarna, PayPal, NatWest, ABN AMRO, and BNP Paribas Fortis. In March 2022, Visa completed the acquisition of Tink for €1.8 billion — one of the largest European fintech acquisitions of that year, and a clear signal of how seriously the global payments industry had come to take open banking infrastructure. Visa's strategic rationale was straightforward: it had failed to acquire Plaid, the US equivalent, after an antitrust challenge, and needed a European open banking capability. Tink gave it 500 employees, 18 European markets, and relationships with over 300 banks and fintechs built over a decade. The founders stayed on as CEO and CTO through the transition, continuing to run Tink as a standalone Visa subsidiary from Stockholm. Both departed in 2025 — Kjellén and Hedberg announced they were building Freda, a new AI-driven legal and compliance technology startup, with the pair describing Tink as "now in better hands than ever." Francois Tornier, Visa's VP of Open Banking, took over as CEO. The product roadmap has continued under Visa ownership, including a 2024 expansion of Tink's open banking platform into the US market.

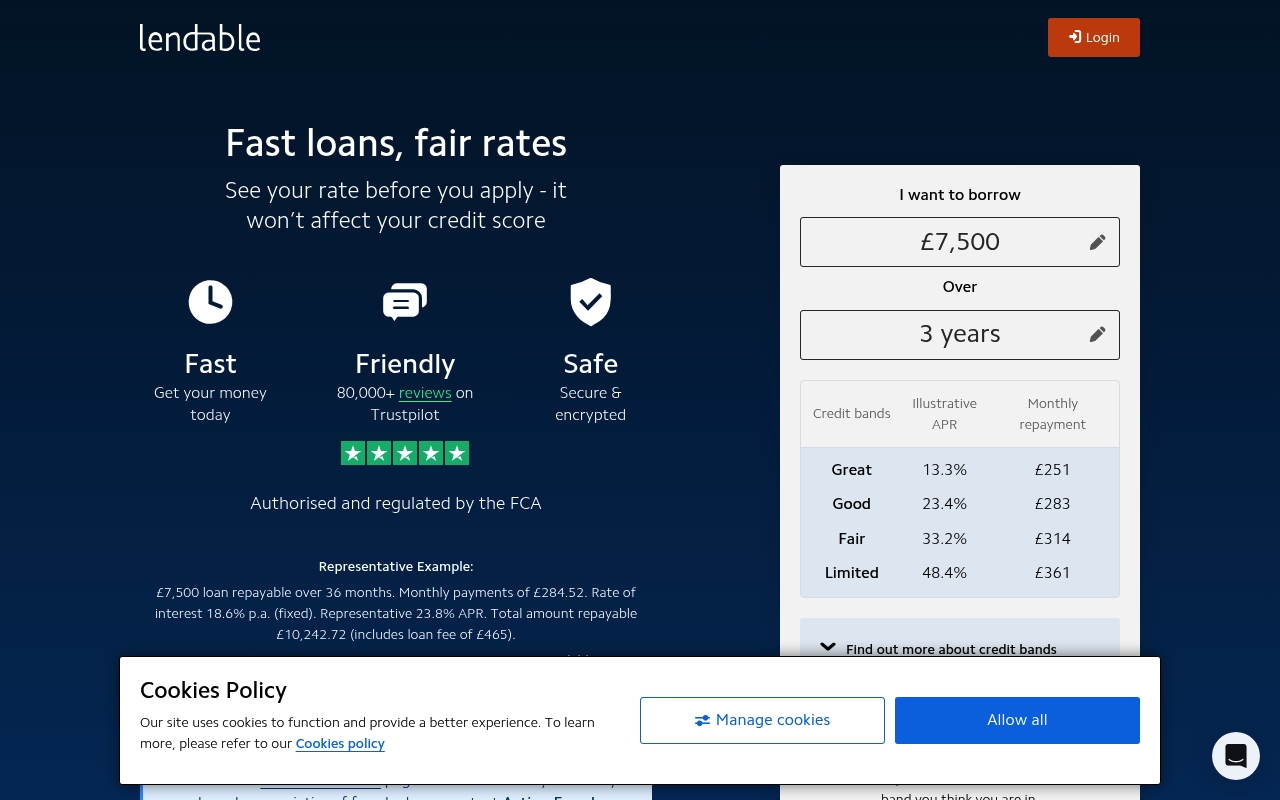

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates. The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets. In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names. Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

OpenGamma builds the computational backbone for how financial institutions price, value, and manage complex derivatives and fixed-income securities. In a world where legacy risk systems still demand custom Excel spreadsheets and manual reconciliation, OpenGamma delivers cloud-native valuation and risk analytics that run at scale—processing millions of trades in real time without the infrastructure headaches. The platform combines market data ingestion, advanced pricing models, and scenario analysis into a single integrated stack. Banks and asset managers use it to replace fragmented point solutions, cut operational risk, and accelerate the pace at which they can launch new products. Think of it as the plumbing beneath modern capital markets trading desks: invisible, but critical. OpenGamma's strength lies in its technical depth. The company targets sophisticated buy-side and sell-side institutions that need institutional-grade accuracy and auditability—not merely dashboards for non-experts. It competes against entrenched in-house systems and specialized vendors by offering flexibility and speed of deployment that rivals neither legacy providers nor lightweight startups can match. In Europe's push toward regulatory standardization and operational resilience, OpenGamma has positioned itself as infrastructure for the next generation of risk management, where transparency, speed, and compliance are no longer separate concerns but engineered into the same platform.