What is RegTech?

RegTech — regulatory technology — is the category of software and services that helps financial institutions and regulated businesses manage compliance more efficiently. The compliance burden on European financial services has grown substantially: GDPR, PSD2, PSD3, MiCA, DORA, EMIR, MiFID II, AMLD6, and a continuous stream of EBA guidelines have created regulatory complexity that legacy compliance processes struggle to keep pace with. RegTech companies address this by automating compliance workflows — transaction monitoring, regulatory reporting, risk assessment, audit trails, and policy management — that would otherwise require large manual compliance teams.

European RegTech companies in our database

Hawk brings machine learning firepower to financial crime detection, sitting at the intersection of compliance and computational intelligence. Rather than relying on static rule sets that miss novel fraud patterns, Hawk deploys adaptive algorithms that learn from transaction behavior in real time, catching what traditional systems let slip through the cracks. The platform ingests transaction data across multiple channels—payments, transfers, accounts—and surfaces suspicious activity before it becomes a problem. For banks and fintechs drowning in false positives from legacy systems, Hawk promises a different approach: smarter, faster, less noise. Its technology sits on the boundary between compliance necessity and operational efficiency, helping institutions detect actual threats rather than gaming alert thresholds. In an environment where financial crime is increasingly sophisticated and regulatory pressure unrelenting, Hawk positions itself as the thinking alternative to checkbox compliance, offering institutions a genuine competitive edge in the race to stay ahead of bad actors.

ION Group is a sprawling financial software empire that has quietly become one of Europe's most comprehensive infrastructure plays. The company operates across trading, risk management, and post-trade processing—the unsexy but absolutely critical backbone that powers global capital markets. Unlike flashy fintech startups chasing consumer adoption, ION builds the invisible plumbing that institutional traders, hedge funds, and investment banks depend on every single day. Its portfolio spans front-office platforms, market data aggregation, clearing and settlement systems, and regulatory reporting tools. ION serves as a counterweight to the purely consumer-focused fintech narrative, proving there's enormous value in solving problems for professionals who move billions. The company's strength lies in its ability to connect disparate financial systems, providing what amounts to a unified operating system for institutional finance. For European financial institutions, ION represents a trusted partner in an increasingly complex regulatory landscape, offering solutions that integrate seamlessly with legacy infrastructure while modernizing workflows. Its acquisition-driven growth strategy—picking up niche specialists and consolidating them into a cohesive platform—mirrors the broader consolidation happening across enterprise fintech. ION's market position underscores a fundamental truth about fintech: the biggest opportunities often lie in B2B infrastructure rather than consumer apps.

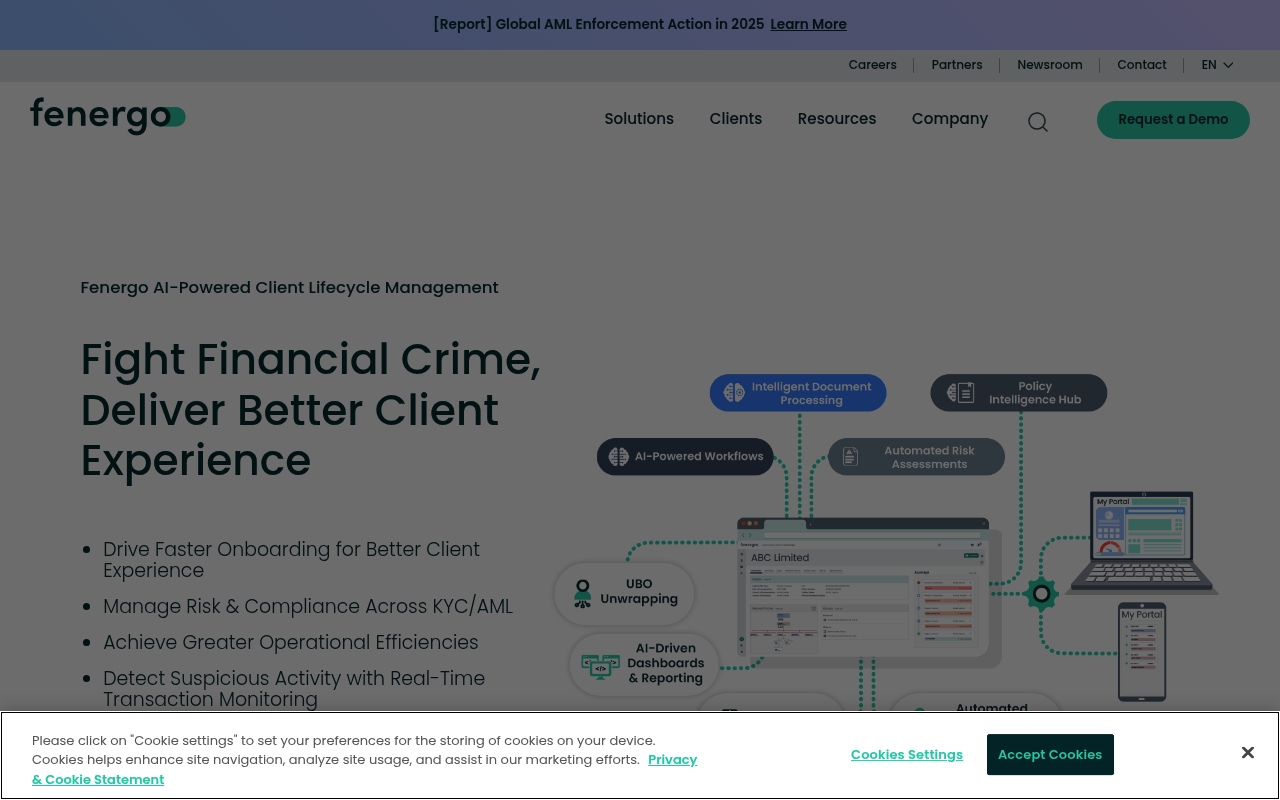

Compliance has long been the unglamorous backroom operation of financial services—heavy, expensive, and often painfully slow. Fenergo flips that script by turning regulatory friction into operational advantage. The Dublin-based software company automates the gruelling work of onboarding clients, managing their data, and staying compliant with an ever-shifting maze of regulations. What banks and investment firms once treated as a cost center, Fenergo repositions as competitive edge. At its core, Fenergo is a digital client lifecycle management platform. It consolidates onboarding, KYC, AML screening, sanctions checks, and ongoing regulatory monitoring into a single, integrated workflow. Rather than legacy institutions juggling multiple point solutions and manual spreadsheet cultures, Fenergo orchestrates the entire client journey—from first interaction through renewal—in a single intelligent system. The software ingests regulatory data, flags anomalies, and automates approvals where rules allow, freeing compliance teams to focus on judgment calls that actually require human expertise. What sets Fenergo apart in a crowded RegTech space is its disciplined focus on the regulated financial institution as customer, not the consumer. While plenty of fintechs chase sexy consumer-facing applications, Fenergo has built deep, sticky relationships with banks, asset managers, and brokers who need sophisticated, audit-proof compliance infrastructure. It operates at institutional scale—handling millions of client records, complex entity hierarchies, and regulatory jurisdictions spanning continents. In an era when regulatory fines have become nine-figure line items and reputational damage from compliance failures can tank a bank's stock price, Fenergo sits at the nerve center of institutional risk management. It's not the flashy side of fintech, but it's arguably the most essential.

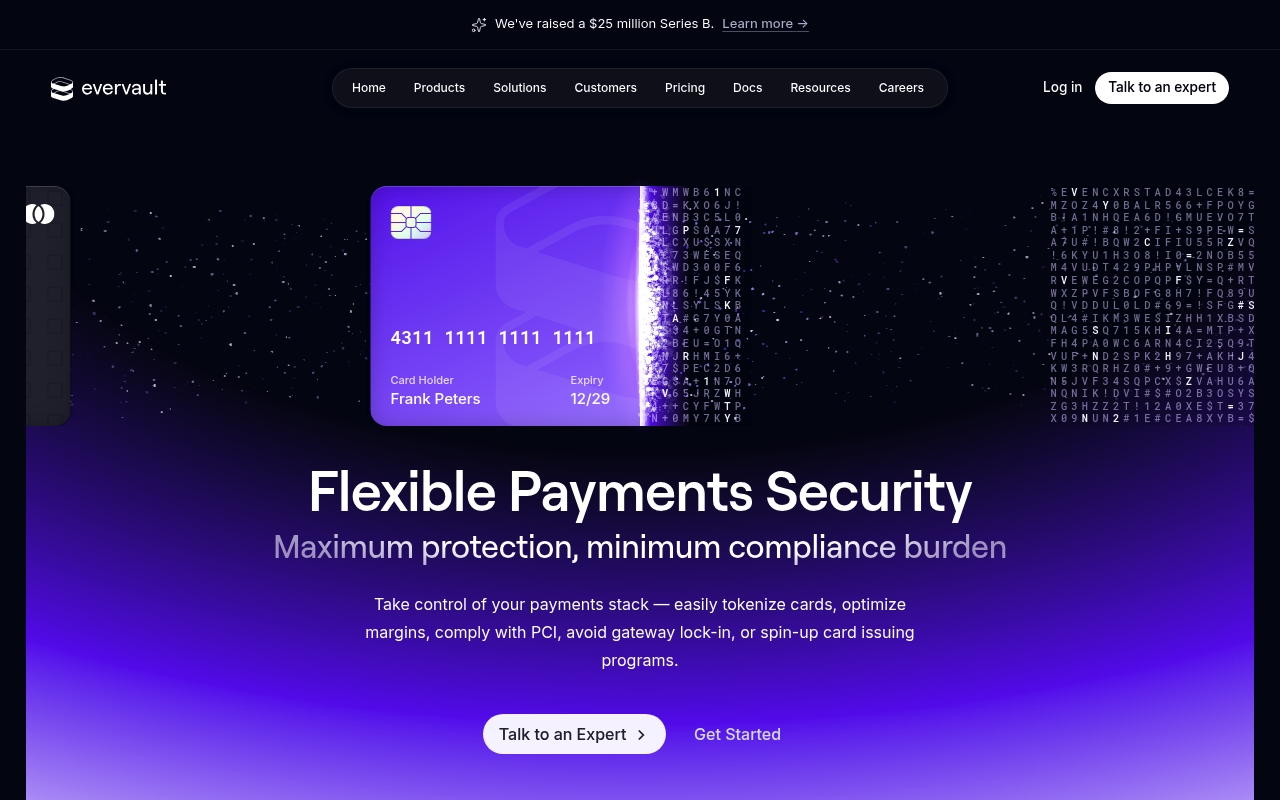

Evervault is a European cryptography company that lets developers encrypt sensitive data in transit and at rest without rearchitecting their systems. Rather than forcing teams to build custom encryption pipelines or rely on legacy HSM infrastructure, Evervault provides APIs and SDKs that integrate directly into applications—turning what was once a compliance headache into a developer experience problem. The company operates at the infrastructure layer, sitting between your database and your users. It handles encryption orchestration, tokenization, and secure computation without requiring you to manage keys or understand the underlying cryptography. This means your data stays encrypted in your own cloud account, your keys stay with you, and third-party vendors never see plaintext information. In a European market where data residency and privacy regulations have teeth, Evervault solves a real problem: companies need to protect customer data but can't afford to rebuild their entire tech stack. The platform works with existing databases, APIs, and infrastructure, making compliance less of an engineering ordeal. Evervault positions itself as the encryption layer for modern applications—not a database replacement, not a VPN, but the plumbing that makes data protection feel native to your code. It's particularly relevant for fintech companies handling payment cards, personal identifiers, and healthcare records across distributed systems. The company is helping reshape how European companies think about security: not as an afterthought, but as architecture.

OpenWrks was the UK's first FCA regulated AIS Open Banking platform. In 2020 OpenWrks was acquired by Tink. Credit decisions have historically been made on backward-looking data — credit files that reflect what happened years ago rather than what a person's financial life looks like today. OpenWrks was founded in London in 2017 to change that with open banking data. Its platform uses transaction data from bank accounts to generate real-time financial insights — income verification, affordability assessments, and cash flow analytics — that lenders, debt advisors, and financial services companies can use to make better decisions about the people they serve. The focus on affordability and debt support is deliberate — OpenWrks has built particular depth in the debt advice sector, providing tools that help debt charities and money guidance services understand their clients' financial situations with precision and speed that paper-based assessments cannot match. Its work with the Money and Pensions Service and other UK debt support organisations reflects a commitment to using open banking data for financial inclusion rather than purely commercial lending optimisation. In the open banking ecosystem, where most data applications focus on acquisition and credit origination, OpenWrks' orientation toward debt support and financial wellbeing is a distinctive positioning that has built genuine trust with the organisations that serve financially vulnerable people.

Feedzai is a fraud detection and financial crime prevention platform that works behind the scenes for banks, payment processors, and fintech companies across Europe and beyond. The company uses machine learning to spot suspicious transactions in real time, flagging fraud before it costs institutions millions while keeping legitimate customers from being blocked unnecessarily. Unlike legacy fraud systems that rely on rigid rules and lag behind new attack patterns, Feedzai's approach adapts continuously, learning from emerging threats across its network of financial institutions. The platform handles everything from card fraud and money laundering to synthetic identity schemes and account takeover attempts. It's become a critical layer of defense for institutions managing enormous transaction volumes, where manual review is impossible and false positives destroy customer experience. In the European market, Feedzai competes alongside more traditional risk vendors but stands out through its speed and sophistication. Banks increasingly rely on AI-driven systems rather than rule-based gatekeepers, and Feedzai has positioned itself as the intelligent alternative that doesn't just block transactions—it understands behavior. The company serves everyone from global systemically important banks to smaller regional players, offering both real-time decisioning and historical analytics. Feedzai represents a broader shift in how financial institutions approach security: from reactive policing to predictive intelligence.