← Back to Cleo

Alternatives

Alternatives to Cleo

Explore 12 European fintech companies similar to Cleo — operating in Personal Finance.

12 alternatives to Cleo

Sorted by similarity and popularityRevolut

WealthPaymentsDigital BankingCrypto & BlockchainPersonal Finance

🇱🇹 Lithuania

Nik Storonsky grew up moving between Russia and France before landing in London as a derivatives trader. Vlad Yatsenko was a software engineer who'd spent years building financial systems. In 2015 they sat down and asked a question that should have occurred to banks years earlier: why does spending money abroad still cost so much?

The answer they built was Revolut — initially a prepaid card with no foreign exchange fees, then a multi-currency account, then a trading platform, then an insurance product, then a business banking offering, then something that's increasingly hard to describe as anything other than a full financial operating system. Revolut didn't unbundle banking so much as rebuild it from scratch for people who found the existing version frustrating and expensive.

The numbers now are genuinely striking for a company that started with two people and a card. Revenue reached £4.5 billion in 2025, up 46% year on year, with net profit of £1.3 billion. The customer base grew to 68.3 million retail users — one in five working-age adults in Europe — plus 767,000 businesses. The company employs 12,200 people across more than 25 countries and was valued at $75 billion in a November 2025 secondary share sale, making it Europe's most valuable private technology company.

The milestone that mattered most, though, arrived in March 2026: a full UK banking licence from the Prudential Regulation Authority, ending a three-year application process that had become the most-watched regulatory saga in European fintech. The licence means Revolut can now protect UK deposits up to £120,000, offer authorised consumer credit, and compete directly with high street banks for mortgage and lending business. It's the piece that transforms Revolut from a very successful payments app into a regulated bank.

The company has also applied for a US banking charter and is expanding aggressively into Latin America, having opened its first bank outside Europe in Mexico. The original thesis — that banking could be cheaper, faster, and simpler — hasn't changed. The scale at which it's now being tested has.

Founded 2015

View profile →

Monzo

WealthDigital BankingLendingPersonal Finance

🇬🇧 United Kingdom

The founding team that built Monzo had all worked together before — at Starling Bank, another challenger bank startup that didn't survive its internal conflicts. Tom Blomfield, Gary Dolman, Jonas Huckestein, Jason Bates, and Paul Rippon left Starling together in 2015 and started again. The product they built was initially a prepaid card — a coral-coloured piece of plastic that became one of the most recognisable objects in British fintech — before becoming a fully licensed current account in 2017.

The early user community was unusual for a bank. Monzo ran community forums, published public blog posts about its engineering decisions, and invited customers into beta programmes for new features. When it broke the world record for the fastest crowdfunding raise in 2016 — £1 million in 96 seconds — it wasn't just raising money; it was building an identity. People felt ownership of the product in a way that no high street bank had ever managed to create. That emotional connection became a genuine competitive advantage.

The product has matured considerably since then. Monzo now offers current accounts, joint accounts, savings pots, personal loans, overdrafts, and investment products, all wrapped in the real-time notification experience and transaction categorisation that made its early reputation. Revenue reached £1.23 billion in 2024, up 40% year on year, with net income of £95 million — the second consecutive year of profitability after years of growth-first losses. The customer base reached 12.1 million by end of 2024, making Monzo the UK's largest digital bank by customer count. Customer deposits stood at £16.6 billion.

The business is still private — the much-discussed IPO has not yet happened, and internal disagreements about where to list (the former CEO TS Anil favoured the US, the board preferred London) contributed to Anil's departure in October 2025. Diana Layfield took over as CEO with a mandate focused on international expansion before any public listing. The company is valued at approximately $5.9 billion following a 2024 secondary sale backed by Alphabet's GIC and StepStone.

In December 2025 Monzo announced it had agreed to acquire Habito, the digital mortgage broker, pending regulatory approval — a move that extends the product into one of the last major financial products it didn't yet offer. With 3,821 employees and a loan book growing rapidly, Monzo has evolved from a prepaid card experiment into a bank with genuine scale and a growing claim on being the primary financial account for a generation of UK consumers.

Founded 2015

View profile →

Starling Bank

Digital BankingSME FinancePersonal Finance

🇬🇧 United Kingdom

Starling Bank is a British challenger bank that stripped away the friction of traditional banking and rebuilt it around what modern customers actually need: instant notifications, real-time spending insights, and accounts you can open in minutes without stepping into a branch. Founded in 2014, it operates as a fully regulated bank with its own banking license, not just a wrapper around legacy infrastructure.

The platform serves both consumers and SMEs, offering straightforward current accounts, savings pots, and increasingly sophisticated business banking tools. Unlike neobanks reliant on partnerships, Starling owns its core infrastructure, which means faster iteration and tighter product control. The company has built a reputation for no-nonsense transparency: no hidden fees, no overdraft tricks, and clear communication about what you're getting.

In the crowded UK digital banking space, Starling stands apart through consistent execution and a focus on solving real problems rather than chasing hype. It's profitable, self-sufficient, and treated by legacy banks as a genuine competitor rather than a novelty. For European fintechs, Starling represents the successful blueprint: regulated, capital-efficient, and genuinely preferred by millions of users who value simplicity over flashiness.

As the fintech landscape matures, Starling exemplifies the shift from disruption theater to sustainable banking infrastructure—a reminder that the most radical innovation often looks deceptively simple.

Founded 2014

View profile →

Pockit

Digital BankingPersonal Finance

🇬🇧 United Kingdom

Pockit is a mobile-first financial platform designed for people who've been locked out of traditional banking. Rather than chasing the affluent, Pockit focuses on the underbanked—those without access to a current account, credit history, or the documentation banks demand. The app serves as a genuine alternative to brick-and-mortar banking, offering digital accounts, card payments, and money management tools entirely through your phone.

What sets Pockit apart is its commitment to financial inclusion without the gatekeeping. You don't need a credit score or payslip to open an account. Instead, the platform builds trust through usage patterns and behavioral data, creating pathways for people traditionally rejected by high street banks. This shifts the relationship from one of suspicion to one of genuine access.

The company operates across the UK and Europe, proving that underserved segments aren't just a niche—they're a substantial market. Pockit's mission is radical in its simplicity: banking shouldn't require jumping through hoops or having the right background. It's a challenger in the truest sense, not because it offers flashy features, but because it solves a real problem for millions of people who simply want to participate in the financial system.

Founded 2015

View profile →

Trade Republic

WealthDigital BankingPersonal Finance

🇩🇪 Germany

Trade Republic has fundamentally rewritten the script for European retail investing. Where traditional brokers demanded minimums, paperwork, and fees that could swallow returns, this Berlin-based neobroker arrived in 2015 with a smartphone app and a radical premise: investing should cost almost nothing and take seconds.

The platform trades stocks, ETFs, and fractional shares across multiple European exchanges with zero commissions. Its core strength is simplicity—the interface strips away complexity while maintaining the depth serious investors expect. Execution is fast, the fee structure is transparent (mostly subscription-based rather than per-trade), and the onboarding process reflects modern expectations around speed and convenience.

Trade Republic sits at the convergence of neobanking and trading. While competitors like Revolut added trading as a secondary feature, Trade Republic built the entire experience around it. The company holds banking licenses across multiple EU jurisdictions, giving it the infrastructure to manage cash, offer savings features, and issue debit cards—all in service of becoming a financial operating system for young Europeans.

Its expansion beyond trading into banking products reflects a broader industry shift: the most valuable fintech companies aren't specialists anymore. They're ecosystems. Trade Republic's role in the European fintech landscape is as a proof of concept that direct-to-consumer wealth management, executed with design discipline and regulatory precision, can scale rapidly while maintaining unit economics that would make traditional brokers blush.

Founded 2015

View profile →

Bitpanda

WealthCrypto & BlockchainPersonal Finance

🇦🇹 Austria

Bitpanda is a Vienna-based fintech that democratized crypto investing for European retail users who found traditional exchanges intimidating or inaccessible. The platform launched in 2014 as a Bitcoin marketplace and evolved into a multi-asset investment app that lets anyone buy fractions of crypto, stocks, metals, and commodities with a few taps on their phone.

What sets Bitpanda apart is its aggressive focus on the everyday investor rather than crypto enthusiasts. The app strips away complexity, offers micro-investing (you can buy €1 worth of Bitcoin), and integrates savings automation through its Bitpanda Savings feature. It's become a household name in German-speaking Europe, with a clean mobile-first interface that appeals to younger savers who want exposure to alternative assets without the friction of traditional brokerages.

Bitpanda operates across multiple business units: a consumer investment app, an institutional trading platform called Bitpanda Pro, and Bitpanda Elements, its white-label infrastructure play for financial institutions. The company expanded beyond crypto into traditional asset classes to capture a broader addressable market and hedge regulatory risk as European crypto rules tightened.

Among European retail investment platforms, Bitpanda ranks as a serious contender—well-funded, profitable, and operating under tight regulatory scrutiny. It represents a shift in how Europeans think about alternative investments: not as speculative sidebets but as legitimate wealth-building tools accessible to anyone with a smartphone.

Founded 2014

View profile →

bunq

PaymentsDigital BankingPersonal Finance

🇳🇱 Netherlands

Bunq is a mobile-first bank that treats banking like a consumer product rather than a legacy service. Founded in the Netherlands, it ditches the branch experience entirely in favor of a sleek app where you can open accounts, send money across borders, and manage multiple sub-accounts from your phone.

What sets bunq apart is its obsession with user control and transparency—no hidden fees, no dark patterns, just straightforward banking built for people who've grown up with smartphones. It's positioning itself as the antidote to traditional banking bloat, offering real-time notifications, instant international transfers, and the ability to spin up separate accounts for different purposes (one for bills, one for travel, one for saving).

The company takes privacy seriously too, storing data locally on encrypted servers rather than in cloud warehouses. Bunq operates across Europe with full banking licenses, which means you get FDIC-style deposit protection alongside the modern interface. For the fintech generation that wants a genuine alternative to both legacy banks and overhyped challengers, bunq represents banking infrastructure that actually respects its users.

Founded 2012

View profile →

GoHenry

PaymentsPersonal Finance

🇬🇧 United Kingdom

GoHenry gives children and teens prepaid cards with parental controls.

Founded 2012

View profile →

BudgetBakers

Personal Finance

🇨🇿 Czech Republic

Budgeting apps have a retention problem. Most people download them enthusiastically, categorise their transactions for two weeks, and then quietly stop. BudgetBakers was founded in Prague in 2010 with a product philosophy built around making budgeting habitual rather than heroic — designing for the person who wants to be better with money but doesn't want budgeting to feel like a second job. Its Wallet app offers manual and automatic transaction tracking, budget management, and financial reporting across more than 50 countries and multiple currencies, with a clean interface that has earned it consistent recognition in app store rankings across Europe and beyond. The multi-currency, multi-country capability reflects a deliberate decision to build for a global audience rather than a single market — unusual for a Central European fintech that could easily have focused on the Czech and Slovak markets. BudgetBakers has built a substantial user base across Europe and emerging markets, monetising through a freemium subscription model that keeps the core product accessible while offering premium features to engaged users. In the personal finance app landscape, where most products are tied to specific banking ecosystems or regional markets, BudgetBakers' geographic neutrality is both a challenge and a genuine strength.

Founded 2010

View profile →

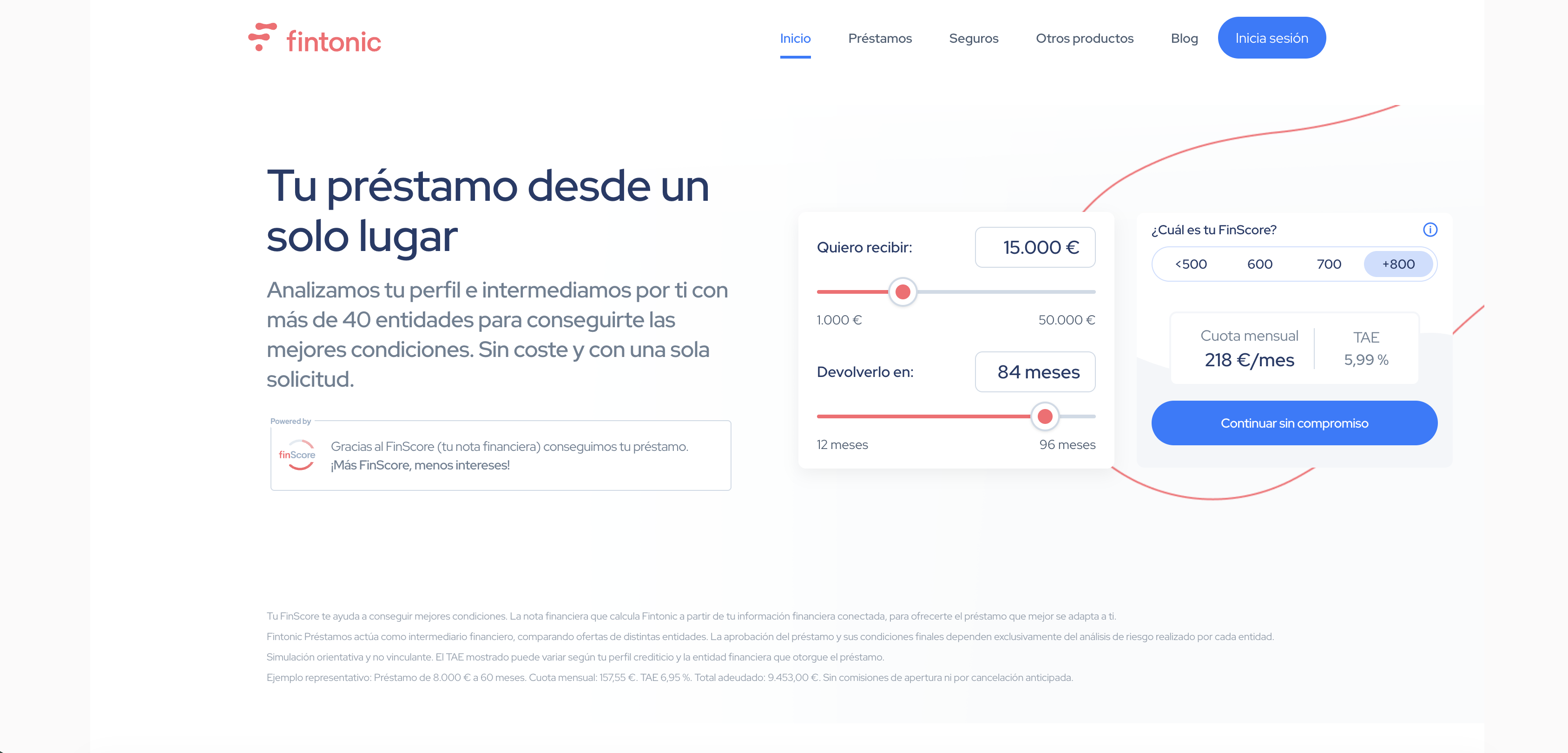

Fintonic

Open BankingPersonal Finance

🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

Founded 2011

View profile →

Taxfix

Personal Finance

🇩🇪 Germany

Taxfix helps consumers file tax returns through a guided mobile experience.

Founded 2016

View profile →

Avanza

WealthDigital BankingPersonal Finance

🇸🇪 Sweden

Avanza is Sweden's largest independent online brokerage, a no-frills investment platform that democratized stock trading for Swedish retail investors two decades ago. What started as a scrappy alternative to traditional banks has become the go-to app for millennials and Gen Z who want to trade, invest, and save without paying legacy banking fees. The platform strips away unnecessary complexity—no advisors, no jargon, just direct market access at transparent prices. Avanza operates in that interesting middle ground between a neobank and a pure trading platform. It offers savings accounts, pension accounts, and investment accounts with a sharp focus on user experience and low costs. The company has built a cultural following in Sweden, becoming almost synonymous with retail investing for a generation that views traditional brokers as relics. Beyond just equities and funds, Avanza has expanded into savings products, retirement planning, and financial education—positioning itself as a genuine financial companion rather than just a transaction layer. Its dominance in the Nordic market reflects a broader European shift toward direct-to-consumer investment platforms that compete on transparency, speed, and mobile-first design. Avanza exemplifies how fintech can win by doing one thing exceptionally well and then expanding thoughtfully into adjacent categories. The company's influence extends beyond Sweden into a broader shift in how younger Europeans think about investing: without gatekeepers, without unnecessary fees, and entirely on their own terms.

Founded 1999

View profile →