← Back to Moneyhub

Alternatives

Alternatives to Moneyhub

Explore 12 European fintech companies similar to Moneyhub — operating in Wealth and Open Banking and Personal Finance.

12 alternatives to Moneyhub

Sorted by similarity and popularityRevolut

WealthPaymentsDigital BankingCrypto & BlockchainPersonal Finance

🇱🇹 Lithuania

Nik Storonsky grew up moving between Russia and France before landing in London as a derivatives trader. Vlad Yatsenko was a software engineer who'd spent years building financial systems. In 2015 they sat down and asked a question that should have occurred to banks years earlier: why does spending money abroad still cost so much?

The answer they built was Revolut — initially a prepaid card with no foreign exchange fees, then a multi-currency account, then a trading platform, then an insurance product, then a business banking offering, then something that's increasingly hard to describe as anything other than a full financial operating system. Revolut didn't unbundle banking so much as rebuild it from scratch for people who found the existing version frustrating and expensive.

The numbers now are genuinely striking for a company that started with two people and a card. Revenue reached £4.5 billion in 2025, up 46% year on year, with net profit of £1.3 billion. The customer base grew to 68.3 million retail users — one in five working-age adults in Europe — plus 767,000 businesses. The company employs 12,200 people across more than 25 countries and was valued at $75 billion in a November 2025 secondary share sale, making it Europe's most valuable private technology company.

The milestone that mattered most, though, arrived in March 2026: a full UK banking licence from the Prudential Regulation Authority, ending a three-year application process that had become the most-watched regulatory saga in European fintech. The licence means Revolut can now protect UK deposits up to £120,000, offer authorised consumer credit, and compete directly with high street banks for mortgage and lending business. It's the piece that transforms Revolut from a very successful payments app into a regulated bank.

The company has also applied for a US banking charter and is expanding aggressively into Latin America, having opened its first bank outside Europe in Mexico. The original thesis — that banking could be cheaper, faster, and simpler — hasn't changed. The scale at which it's now being tested has.

Founded 2015

View profile →

Monzo

WealthDigital BankingLendingPersonal Finance

🇬🇧 United Kingdom

The founding team that built Monzo had all worked together before — at Starling Bank, another challenger bank startup that didn't survive its internal conflicts. Tom Blomfield, Gary Dolman, Jonas Huckestein, Jason Bates, and Paul Rippon left Starling together in 2015 and started again. The product they built was initially a prepaid card — a coral-coloured piece of plastic that became one of the most recognisable objects in British fintech — before becoming a fully licensed current account in 2017.

The early user community was unusual for a bank. Monzo ran community forums, published public blog posts about its engineering decisions, and invited customers into beta programmes for new features. When it broke the world record for the fastest crowdfunding raise in 2016 — £1 million in 96 seconds — it wasn't just raising money; it was building an identity. People felt ownership of the product in a way that no high street bank had ever managed to create. That emotional connection became a genuine competitive advantage.

The product has matured considerably since then. Monzo now offers current accounts, joint accounts, savings pots, personal loans, overdrafts, and investment products, all wrapped in the real-time notification experience and transaction categorisation that made its early reputation. Revenue reached £1.23 billion in 2024, up 40% year on year, with net income of £95 million — the second consecutive year of profitability after years of growth-first losses. The customer base reached 12.1 million by end of 2024, making Monzo the UK's largest digital bank by customer count. Customer deposits stood at £16.6 billion.

The business is still private — the much-discussed IPO has not yet happened, and internal disagreements about where to list (the former CEO TS Anil favoured the US, the board preferred London) contributed to Anil's departure in October 2025. Diana Layfield took over as CEO with a mandate focused on international expansion before any public listing. The company is valued at approximately $5.9 billion following a 2024 secondary sale backed by Alphabet's GIC and StepStone.

In December 2025 Monzo announced it had agreed to acquire Habito, the digital mortgage broker, pending regulatory approval — a move that extends the product into one of the last major financial products it didn't yet offer. With 3,821 employees and a loan book growing rapidly, Monzo has evolved from a prepaid card experiment into a bank with genuine scale and a growing claim on being the primary financial account for a generation of UK consumers.

Founded 2015

View profile →

Trade Republic

WealthDigital BankingPersonal Finance

🇩🇪 Germany

Trade Republic has fundamentally rewritten the script for European retail investing. Where traditional brokers demanded minimums, paperwork, and fees that could swallow returns, this Berlin-based neobroker arrived in 2015 with a smartphone app and a radical premise: investing should cost almost nothing and take seconds.

The platform trades stocks, ETFs, and fractional shares across multiple European exchanges with zero commissions. Its core strength is simplicity—the interface strips away complexity while maintaining the depth serious investors expect. Execution is fast, the fee structure is transparent (mostly subscription-based rather than per-trade), and the onboarding process reflects modern expectations around speed and convenience.

Trade Republic sits at the convergence of neobanking and trading. While competitors like Revolut added trading as a secondary feature, Trade Republic built the entire experience around it. The company holds banking licenses across multiple EU jurisdictions, giving it the infrastructure to manage cash, offer savings features, and issue debit cards—all in service of becoming a financial operating system for young Europeans.

Its expansion beyond trading into banking products reflects a broader industry shift: the most valuable fintech companies aren't specialists anymore. They're ecosystems. Trade Republic's role in the European fintech landscape is as a proof of concept that direct-to-consumer wealth management, executed with design discipline and regulatory precision, can scale rapidly while maintaining unit economics that would make traditional brokers blush.

Founded 2015

View profile →

Bitpanda

WealthCrypto & BlockchainPersonal Finance

🇦🇹 Austria

Bitpanda is a Vienna-based fintech that democratized crypto investing for European retail users who found traditional exchanges intimidating or inaccessible. The platform launched in 2014 as a Bitcoin marketplace and evolved into a multi-asset investment app that lets anyone buy fractions of crypto, stocks, metals, and commodities with a few taps on their phone.

What sets Bitpanda apart is its aggressive focus on the everyday investor rather than crypto enthusiasts. The app strips away complexity, offers micro-investing (you can buy €1 worth of Bitcoin), and integrates savings automation through its Bitpanda Savings feature. It's become a household name in German-speaking Europe, with a clean mobile-first interface that appeals to younger savers who want exposure to alternative assets without the friction of traditional brokerages.

Bitpanda operates across multiple business units: a consumer investment app, an institutional trading platform called Bitpanda Pro, and Bitpanda Elements, its white-label infrastructure play for financial institutions. The company expanded beyond crypto into traditional asset classes to capture a broader addressable market and hedge regulatory risk as European crypto rules tightened.

Among European retail investment platforms, Bitpanda ranks as a serious contender—well-funded, profitable, and operating under tight regulatory scrutiny. It represents a shift in how Europeans think about alternative investments: not as speculative sidebets but as legitimate wealth-building tools accessible to anyone with a smartphone.

Founded 2014

View profile →

Brand New Day

WealthPersonal Finance

🇳🇱 Netherlands

Brand New Day provides online pensions, savings, and investment accounts in the Netherlands.

Founded 2010

View profile →

Scalable Capital

WealthPersonal Finance

🇩🇪 Germany

Scalable Capital sits at the intersection of wealth management and technology, offering algorithmic portfolio management that strips away the pretense of traditional advisory. The Berlin-based platform automates investment decisions through factor-based strategies, letting users build diversified portfolios without the six-figure minimums or quarterly check-ins that characterize private banking.

What makes Scalable different is its obsession with cost transparency. Rather than burying fees in percentages most investors never question, the platform charges a flat monthly fee regardless of account size, eliminating the perverse incentive for advisors to push larger positions. The investment thesis itself is refreshingly unsentimental: diversify broadly across global equities and bonds, rebalance automatically, and let compound interest do the work.

Scalable operates in a market crowded with robo-advisors, but it's positioned itself as the thinking person's alternative to both passive ETF apps and expensive human advisors. It's gained meaningful traction across Germany, Austria, and Switzerland, where wealth management has traditionally meant stuffy bank meetings and outdated fee structures.

The company represents a broader European fintech trend: taking institutional investment practices and making them accessible, affordable, and friction-free for ordinary people who simply want their money to work without constant hand-holding.

Founded 2014

View profile →

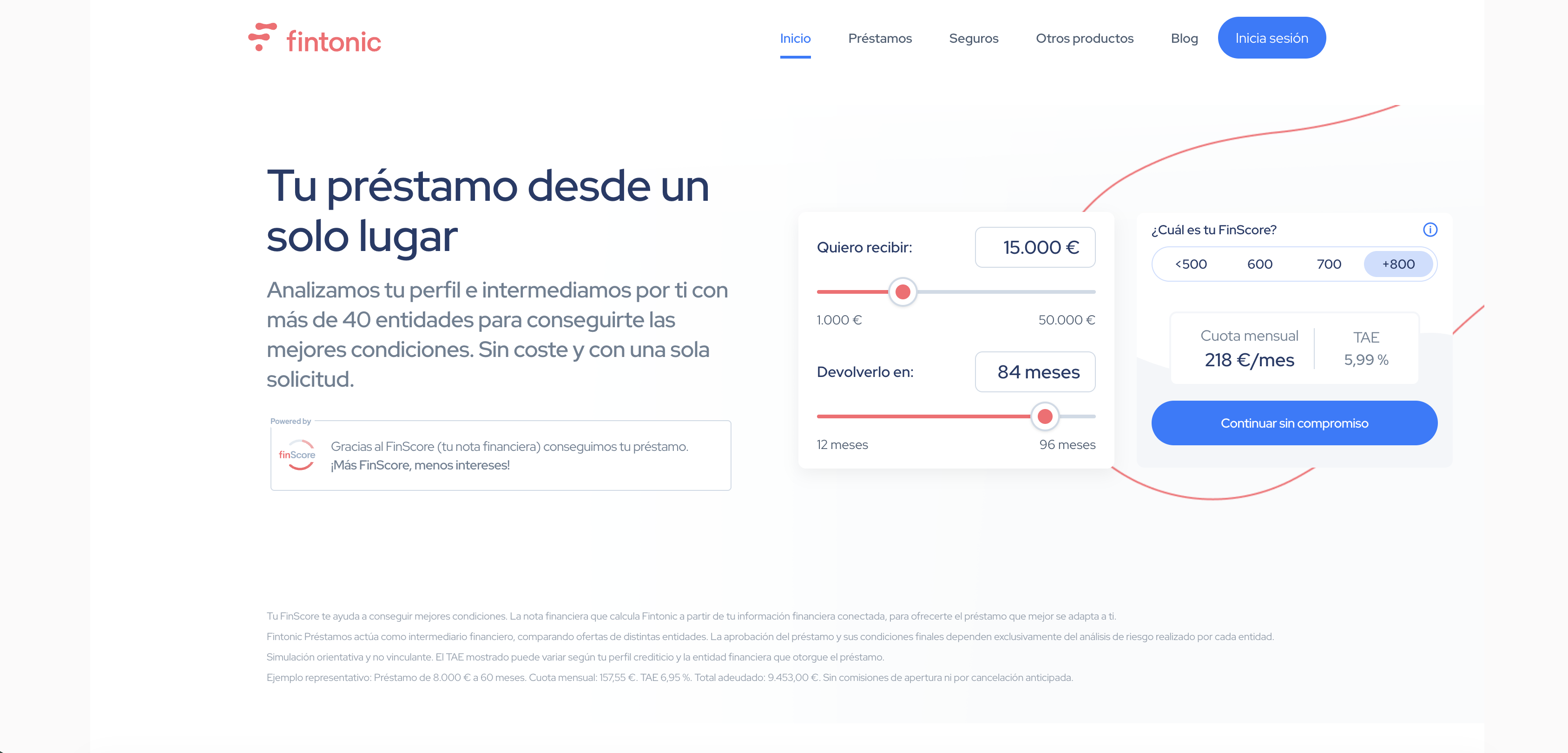

Fintonic

Open BankingPersonal Finance

🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

Founded 2011

View profile →

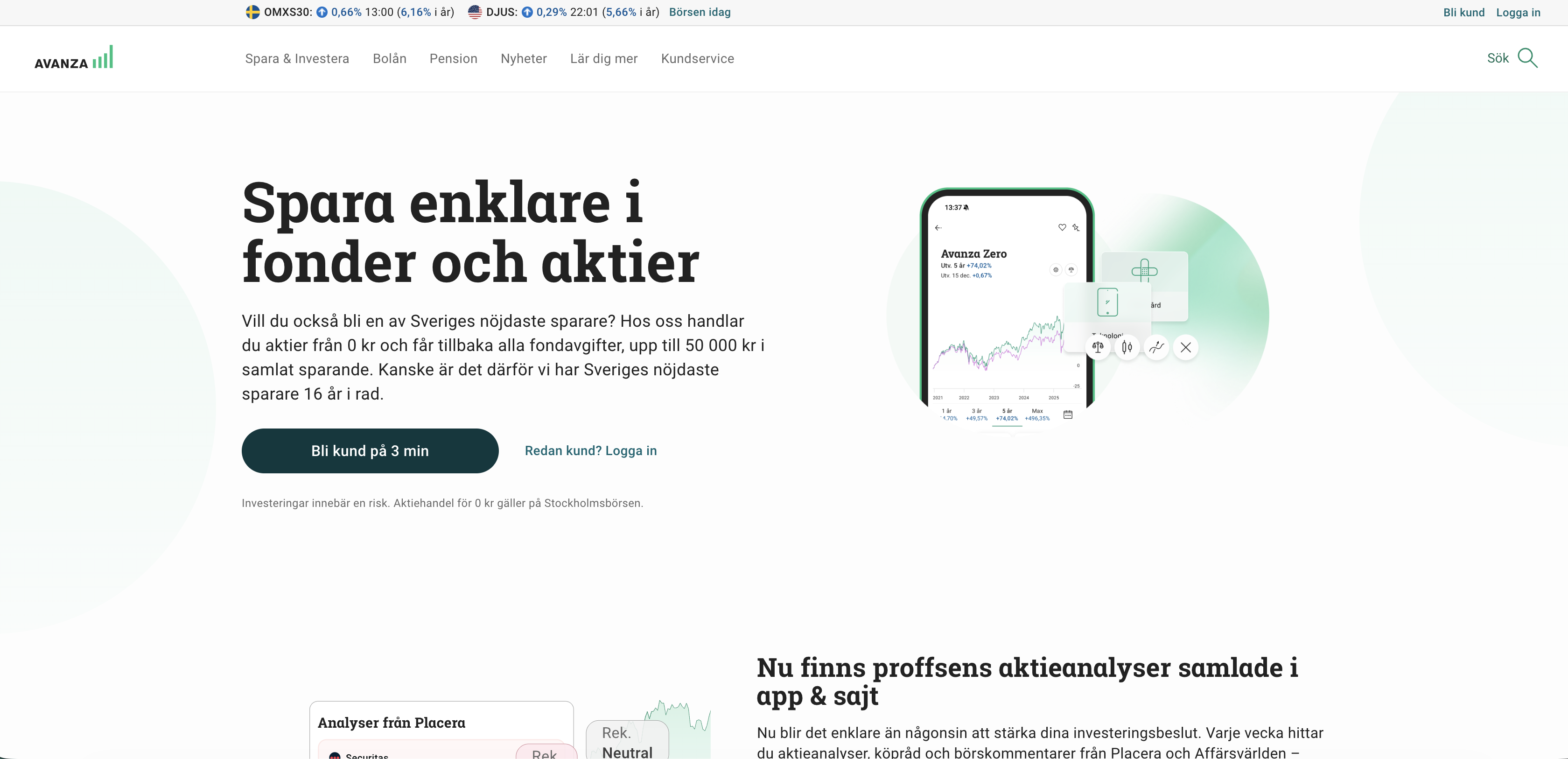

Avanza

WealthDigital BankingPersonal Finance

🇸🇪 Sweden

Avanza is Sweden's largest independent online brokerage, a no-frills investment platform that democratized stock trading for Swedish retail investors two decades ago. What started as a scrappy alternative to traditional banks has become the go-to app for millennials and Gen Z who want to trade, invest, and save without paying legacy banking fees. The platform strips away unnecessary complexity—no advisors, no jargon, just direct market access at transparent prices. Avanza operates in that interesting middle ground between a neobank and a pure trading platform. It offers savings accounts, pension accounts, and investment accounts with a sharp focus on user experience and low costs. The company has built a cultural following in Sweden, becoming almost synonymous with retail investing for a generation that views traditional brokers as relics. Beyond just equities and funds, Avanza has expanded into savings products, retirement planning, and financial education—positioning itself as a genuine financial companion rather than just a transaction layer. Its dominance in the Nordic market reflects a broader European shift toward direct-to-consumer investment platforms that compete on transparency, speed, and mobile-first design. Avanza exemplifies how fintech can win by doing one thing exceptionally well and then expanding thoughtfully into adjacent categories. The company's influence extends beyond Sweden into a broader shift in how younger Europeans think about investing: without gatekeepers, without unnecessary fees, and entirely on their own terms.

Founded 1999

View profile →

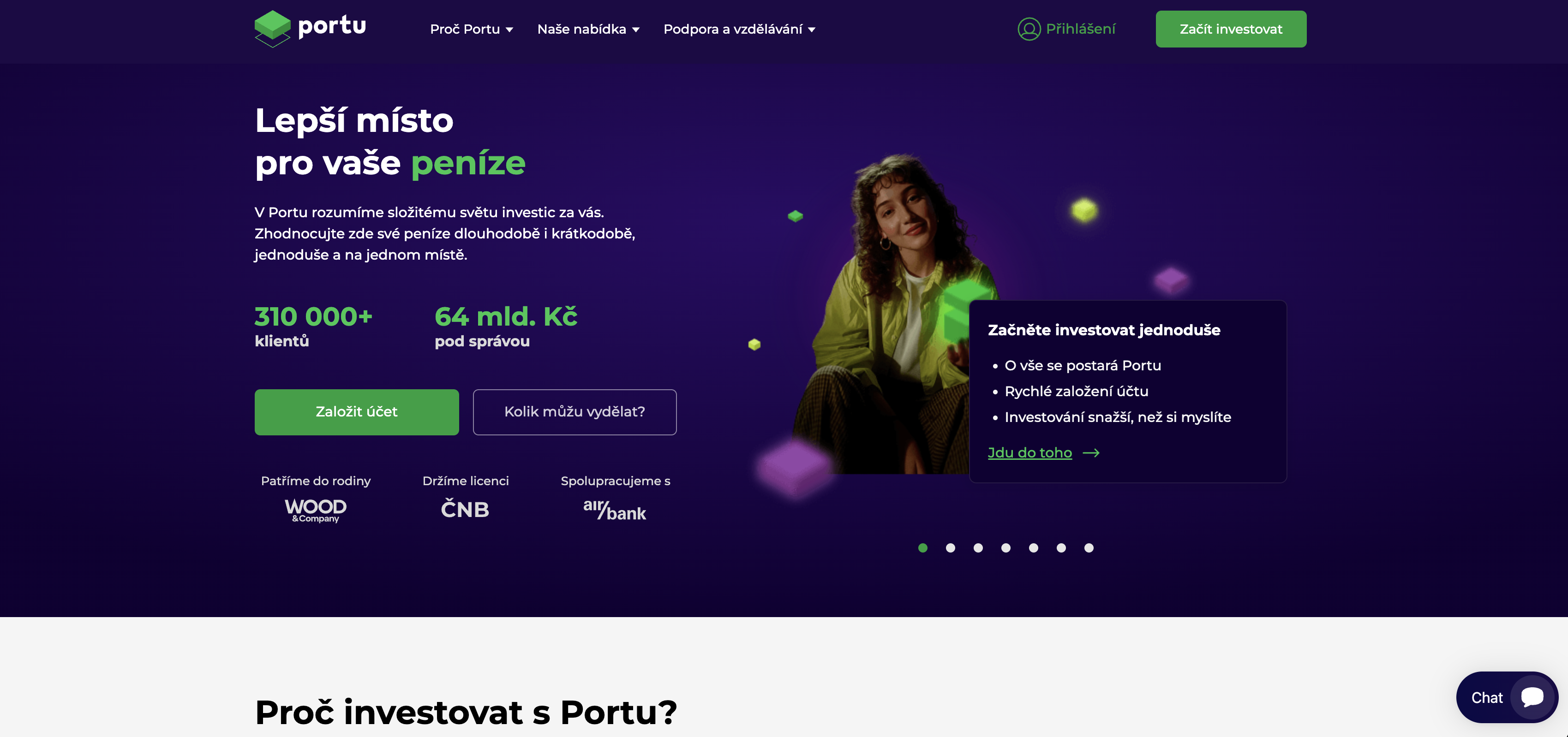

Portu

WealthPersonal Finance

🇨🇿 Czech Republic

Czech investment culture has shifted noticeably over the past decade — from a population that primarily held cash savings to one increasingly comfortable with regulated investment products, particularly among the generation that came of age financially after 2010. Portu was founded in Prague in 2018 to serve that emerging investor base with a digital wealth management platform offering diversified ETF portfolios, retirement planning products, and child savings accounts under a single mobile-first interface. The product was deliberately designed for first-time investors — clear language, low minimum investments, transparent fees, and educational content that helps users understand what they are actually buying rather than the opaque advice models of traditional Czech wealth management. Portu is part of the WOOD Group ecosystem, giving it the institutional backing of one of Central Europe's significant investment firms while maintaining the digital-native product experience that its target users expect. In the Czech wealth tech landscape, Portu has built one of the more successful examples of a Central European robo-advisor reaching genuine consumer scale — proof that the broader European thesis about digital wealth management for first-time investors translates well into markets where investment culture is still being formed.

Founded 2018

View profile →

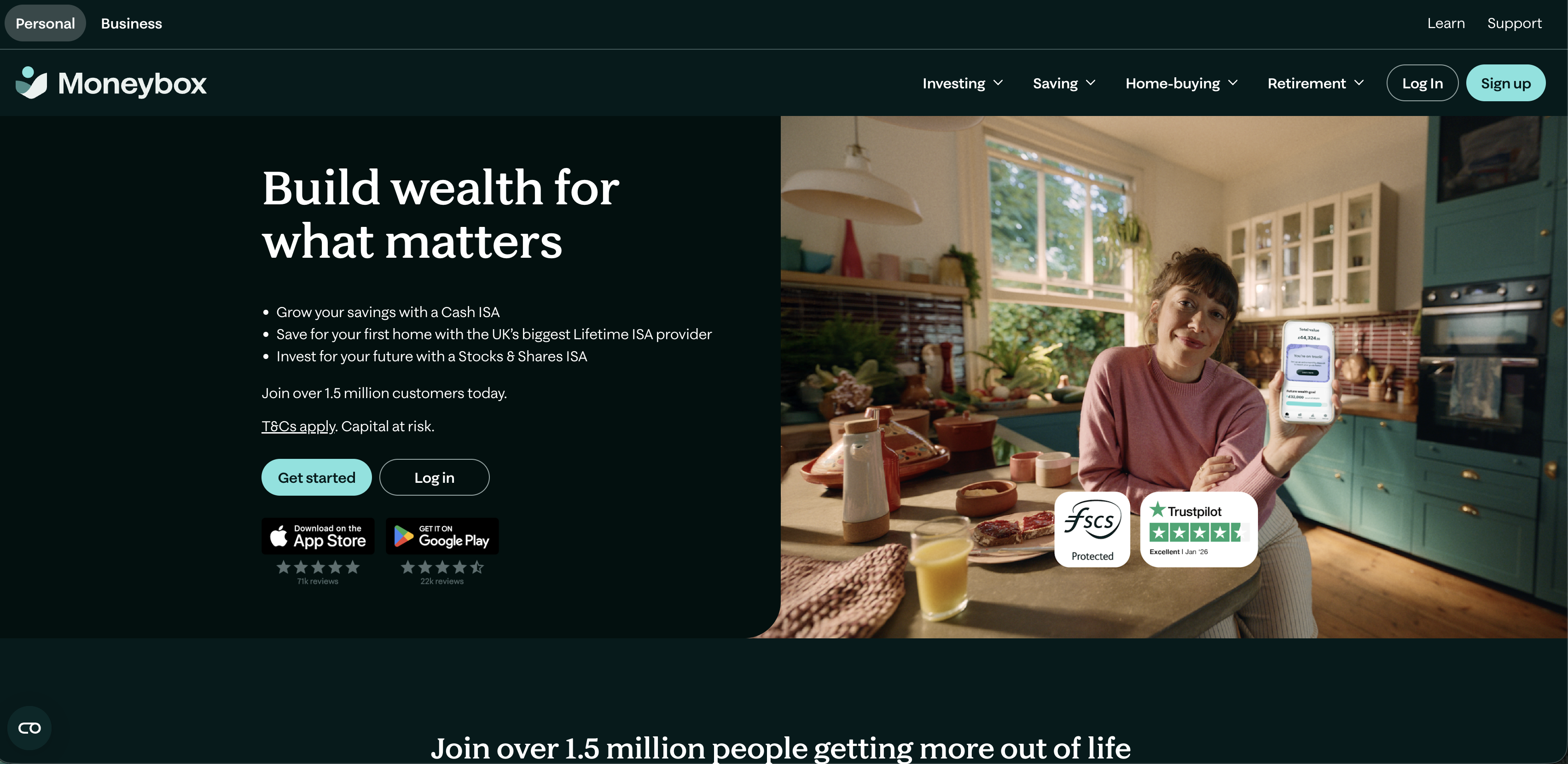

Moneybox

WealthPersonal Finance

🇬🇧 United Kingdom

Moneybox is a British savings and investment app that treats money management like a habit rather than a chore. It rounds up your everyday card purchases to the nearest pound and automatically invests the spare change, turning small moments of spending into genuine wealth-building opportunities. The app sits somewhere between a savings account and an investment platform, democratizing retail investing for people who'd otherwise struggle to find the discipline or capital to start.

What makes Moneybox different is its behavioral psychology angle. Rather than asking users to set aside cash manually, it leverages the friction-free nature of mobile payments to make investing feel frictionless and even invisible. Your coffee costs £3.50? It rounds to £4, and that 50p joins a growing pot invested in a diversified portfolio matched to your risk tolerance.

Launched in 2016, Moneybox has spent the better part of a decade refining this approach across the UK market. It's accrued millions of users precisely because it removes two of the biggest barriers to retail investing: the psychological burden of cutting back elsewhere, and the paralysis of deciding where to actually put your money. The app integrates with your everyday banking, making wealth-building feel less like a separate financial task and more like an automatic consequence of how you already spend.

Moneybox represents a category-defining shift in European fintech: proving that small, consistent nudges—powered by smart design and behavioral insights—can genuinely shift how people relate to money. In an era of headline-grabbing mega-rounds and complex financial engineering, Moneybox's insight is almost defiantly simple: make investing as easy as spending.

Founded 2016

View profile →

Linxo

Open BankingPersonal Finance

🇫🇷 France

Linxo is a European personal finance platform that aggregates bank accounts, credit cards, and investments across multiple institutions into a single dashboard. Rather than asking users to switch banks entirely, the app pulls live data from existing accounts—a model that respects the European's pragmatic relationship with their primary bank while offering the insights and control they actually want. The company positions itself as the financial operating system for everyday money management, not a replacement for banking itself.

What sets Linxo apart in a crowded personal finance space is its focus on actionable intelligence. Beyond simple balance-checking, the platform categorizes spending automatically, alerts users to unusual transactions, and helps track progress toward financial goals—all without the paternalistic tone of many budgeting apps. It works across France, Spain, Germany, Italy, and Belgium, making it one of the few genuinely pan-European plays in a category often dominated by single-market apps.

Linxo has built its infrastructure on open banking standards, leveraging PSD2 APIs to connect securely to banking institutions rather than relying on screen-scraping. This approach gives it a technical moat while also keeping it aligned with regulatory trends. The company targets digitally-native adults who want visibility into their finances without the friction of traditional banking interfaces.

In the broader fintech landscape, Linxo represents a specific bet: that most people won't abandon their bank, but they will absolutely pay for—or accept advertising within—a tool that makes that bank easier to use. It's less disruptive than a neobank, more practical than an investment app, and more design-forward than legacy personal finance software.

Founded 2015

View profile →

Vivid Money

WealthDigital BankingCrypto & BlockchainPersonal Finance

🇩🇪 Germany

Vivid Money is a Berlin-based fintech that collapsed the traditional distinction between banking, investing, and spending into a single mobile-first experience. Launched in 2020, it positioned itself as the European answer to all-in-one financial apps—a place where you could manage your checking account, invest in fractional shares and crypto, and pay with virtual cards, all without leaving the app.

The platform built its early reputation on speed and accessibility. Account opening took minutes rather than days. The investment side felt more like TradingView-for-consumers than stuffy wealth management. Virtual card creation was instantaneous, and the app's design sensibility leaned toward the minimalist and modern rather than corporate banking's beige aesthetic.

Vivid positioned itself against traditional banks' glacial pace and regulatory burden, while also differentiating from pure-play neobanks that didn't offer investing. It moved quickly to add crypto features when the market demanded them, and secured backing from tier-one investors who believed in the all-in-one thesis.

However, the company faced headwinds from regulatory tightening around crypto and the broader fintech funding winter. In late 2024, reports emerged of operational restructuring and potential insolvency, marking a sobering turn for what had been one of Europe's most closely watched fintech challengers. Vivid's arc—from breakthrough disruptor to distressed turnaround—reflects the volatility of the European fintech landscape and the challenge of building a diversified financial platform without institutional heritage or captive customer bases.

Founded 2020

View profile →