← Categories

What is Personal Finance?

Personal finance fintech helps individuals understand, manage, and improve their financial lives — budgeting, expense tracking, savings goals, debt management, credit monitoring, and financial planning. Open banking has been transformative for the category: before PSD2, personal finance apps relied on fragile screen-scraping to access bank data; after PSD2, authorised apps access transaction data directly through bank APIs with customer consent, dramatically improving accuracy and reliability. Consumer financial literacy across Europe is improving but uneven — personal finance tools address this by making financial data visible, actionable, and engaging rather than opaque.

Subcategories

Budgeting apps

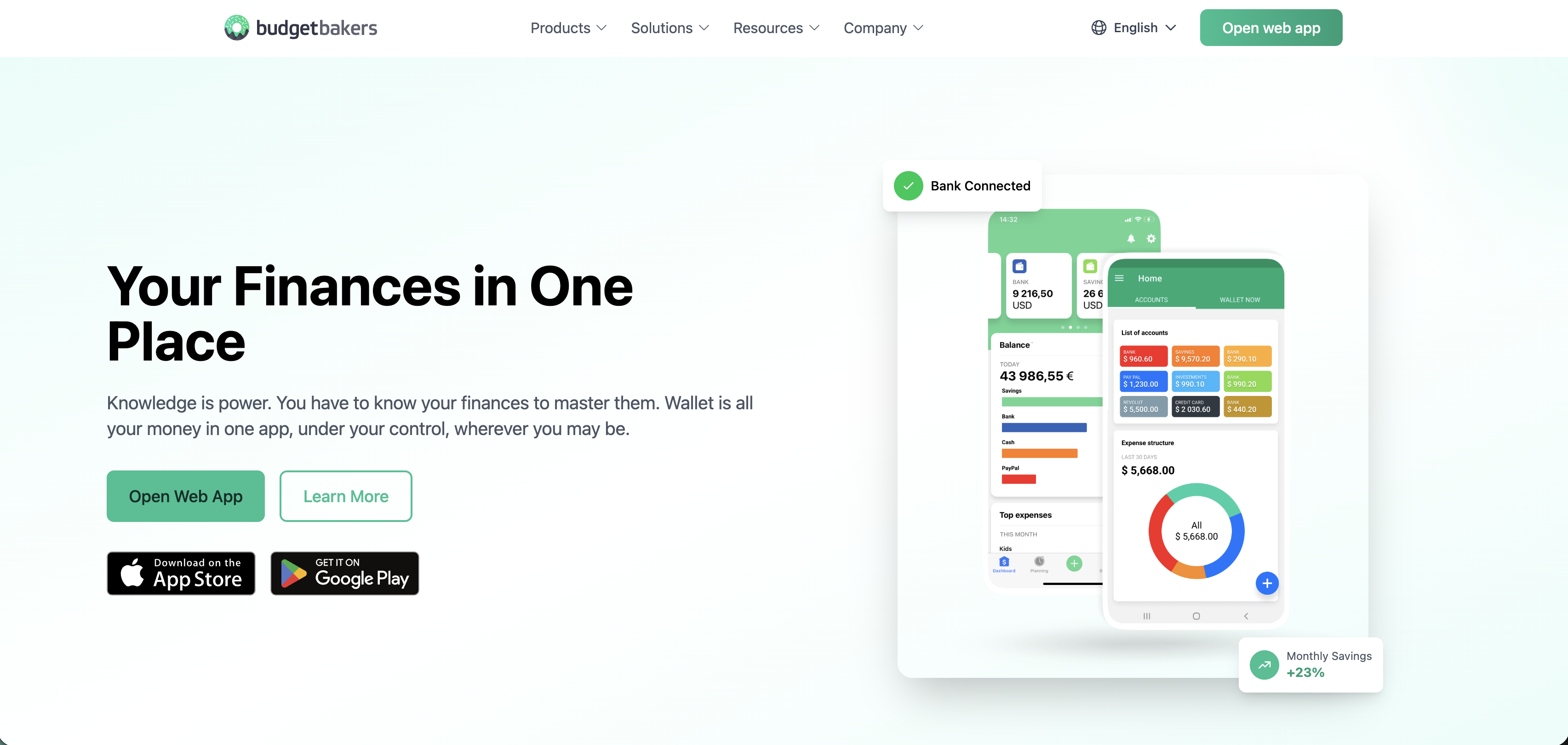

Budgeting apps help individuals and households plan and track spending against predefined targets across categories — groceries, rent, transport, subscriptions, and discretionary spending. Modern budgeting apps connect to bank accounts via open banking APIs, automatically categorise transactions, and provide real-time visibility into spending patterns. The best apps reduce the effort of budgeting to near zero by automating the data collection that manual budgeting has always required.

Debt management

Debt management platforms help individuals and businesses understand, organise, and reduce their debt obligations. Consumer debt management tools provide visibility into outstanding balances, interest costs, and repayment projections, helping users prioritise which debts to pay down first. Some platforms connect directly to creditors or offer debt consolidation products. For businesses, debt management tools track credit facilities, covenant compliance, and refinancing opportunities.

Expense tracking

Expense tracking tools provide individuals and businesses with detailed visibility into where money is being spent. For consumers, expense tracking answers the fundamental question of where income actually goes — categorising transactions, identifying recurring costs, and highlighting unusual spending. For businesses and freelancers, expense tracking is the foundation of bookkeeping, tax preparation, and financial reporting. Open banking has made real-time expense tracking dramatically more accurate by replacing manual entry with automatic transaction data.

Financial coaching

Financial coaching platforms provide personalised guidance and education to help individuals improve their financial health — building savings habits, reducing debt, improving credit scores, and making better financial decisions. Unlike robo-advisors (which focus on investments) or budgeting apps (which focus on tracking), financial coaching addresses the behavioural and knowledge gaps that prevent people from acting on the financial data they already have. Some platforms combine human coaches with software; others use AI to deliver personalised guidance at scale.

Savings tools

Savings tools help individuals build and manage savings through goal-setting, automated transfers, and progress tracking. They range from simple savings pot features within banking apps to dedicated savings platforms that route money to higher-rate accounts automatically. The most effective savings tools reduce the friction of saving through automation — round-ups, scheduled transfers, and rule-based saving triggers — so that saving happens without requiring ongoing conscious decisions from the user.