← Categories

What is Wealth?

Wealth management fintech has democratised access to investment products and financial planning tools previously only available to high-net-worth individuals or through human advisers. The result is a category of platforms that allow anyone with a few hundred euros to build a diversified investment portfolio, access ETF investing, manage a pension, or use sophisticated financial planning tools. Fee compression has been the defining commercial theme: traditional wealth management charged 1-2% annually plus transaction fees, while robo-advisors and digital investment platforms typically charge 0.15-0.75% annually with no transaction costs — a difference that compounds significantly over long investment horizons.

Subcategories

Robo-advisors

Robo-advisors provide automated investment portfolio management using algorithms. A customer completes a risk questionnaire, the platform constructs a diversified ETF portfolio matched to their risk profile, and the portfolio is automatically rebalanced — at fees well below traditional wealth managers.

Retail investing

Retail investing platforms provide individual investors with access to stocks, ETFs, bonds, and other securities through low-cost digital interfaces — removing minimum investment requirements, reducing per-trade fees to near zero, and making market participation accessible to people without financial backgrounds.

Portfolio management

Portfolio management tools help both retail investors and professional wealth managers construct, monitor, and optimise investment portfolios. For professionals, these platforms provide client reporting, performance attribution, compliance documentation, and multi-asset class management across client portfolios. For retail investors, they provide transparency into holdings, performance tracking against benchmarks, and automatic rebalancing. The shift to ETF-based investing has driven demand for tools that manage diversified, low-cost portfolios efficiently.

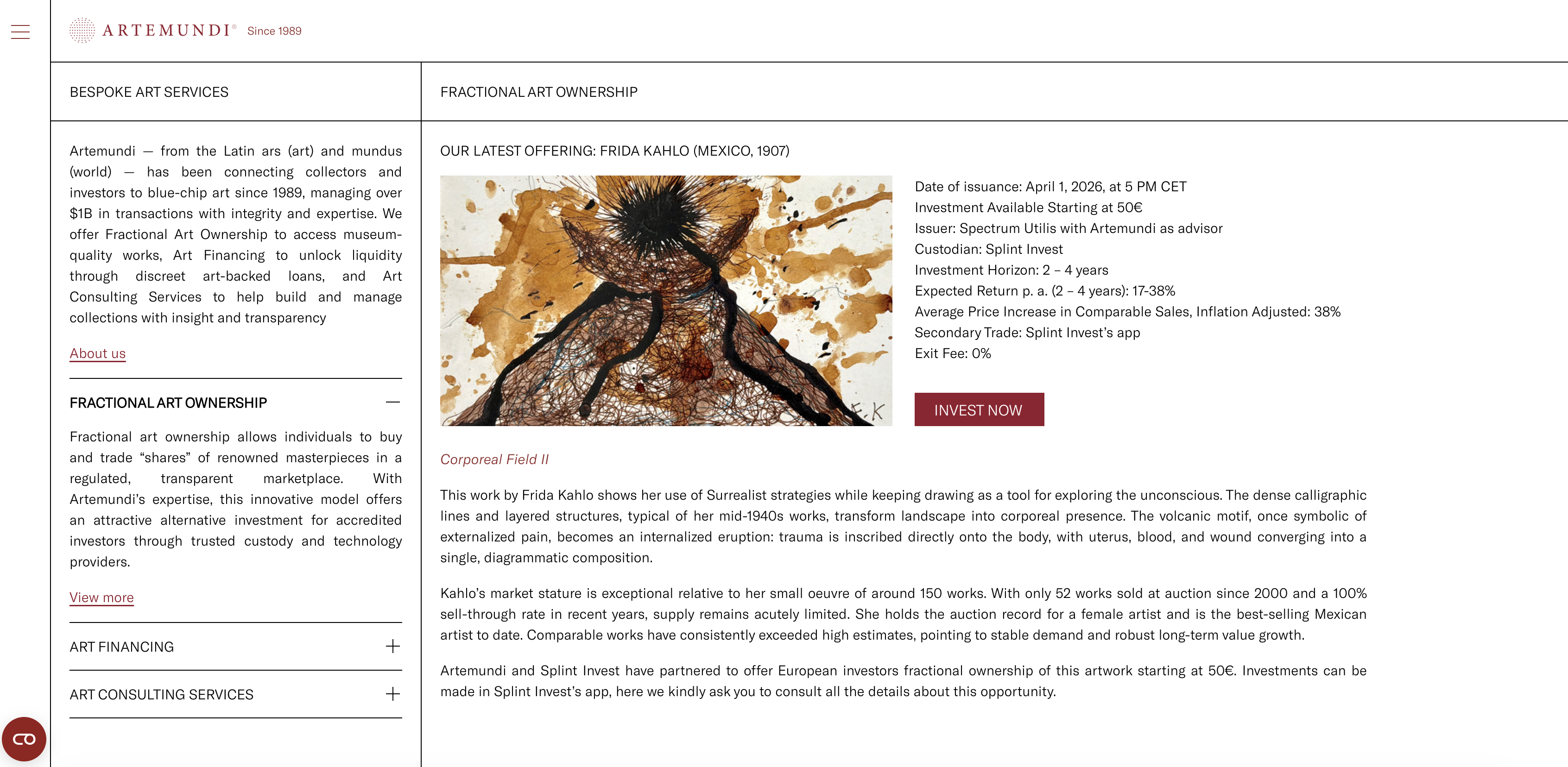

Private wealth tech

Private wealth technology serves the specific needs of high-net-worth individuals and family offices — portfolio analytics, alternative investment access, consolidated reporting across asset classes, estate planning tools, and the complex tax and reporting requirements of significant wealth. Private wealth tech has been slower to digitise than mass-market investing, but platforms are emerging that bring the reporting transparency and operational efficiency of institutional investment management to private clients.

Retirement tools

Retirement tools help individuals plan, manage, and optimise their retirement savings — projecting future income based on current savings rates, modelling different retirement scenarios, consolidating pension pots from previous employers, and optimising contributions across different pension and investment vehicles. As defined benefit pensions have been replaced by defined contribution schemes, individuals bear more responsibility for their retirement outcomes — creating genuine demand for tools that make retirement planning accessible and actionable.