What is Embedded Finance?

Embedded finance is the integration of financial products and services into non-financial platforms and applications. When a ride-hailing app offers drivers a debit card, when an e-commerce platform offers merchants a business account, or when a payroll software company adds earned wage access — that is embedded finance. What is new is the API infrastructure that makes it possible to embed regulated financial products into any software product in weeks rather than the multi-year regulatory effort that previously made financial services inaccessible to non-bank companies. Banking as a Service platforms and payment institution licences have together made embedded finance one of the fastest-growing categories in European fintech.

European Embedded Finance companies in our database

Pieter van der Does and Arnout Schuijff had already built and sold one payments company when they sat down in 2006 to start again. The result was Adyen — the name literally means "start over" in Surinamese — and the premise was simple: instead of stitching together the same fragmented payment infrastructure everyone else was using, they would build the whole thing themselves from scratch. That decision, made in an Amsterdam office nearly two decades ago, is still the reason Adyen is different. Most payment companies are assemblers — they buy a gateway here, a processor there, bolt them together and hope for the best. Adyen owns its own technology stack end to end, which means a merchant integrating once gets access to card processing, local payment methods, point-of-sale terminals, and real-time settlement data through a single platform. No middle layers, no reconciliation headaches, no finger-pointing between vendors when something breaks. The client list tells you everything about where Adyen sits in the market. McDonald's, Spotify, Microsoft, LVMH, H&M — these are companies with serious payment volumes and zero appetite for systems that don't work. Adyen became the default choice for enterprises that had outgrown the limitations of traditional payment stacks and needed something that could handle global scale without buckling. Since going public on Euronext Amsterdam in 2018, Adyen has grown into one of Europe's most valuable technology companies, with around 4,300 employees across 23 countries and net revenue of just under €2 billion in 2024. It remains headquartered in Amsterdam and consistently profitable — a combination that's rarer in fintech than it should be. For businesses that treat payments as infrastructure rather than an afterthought, Adyen is the benchmark everything else gets measured against.

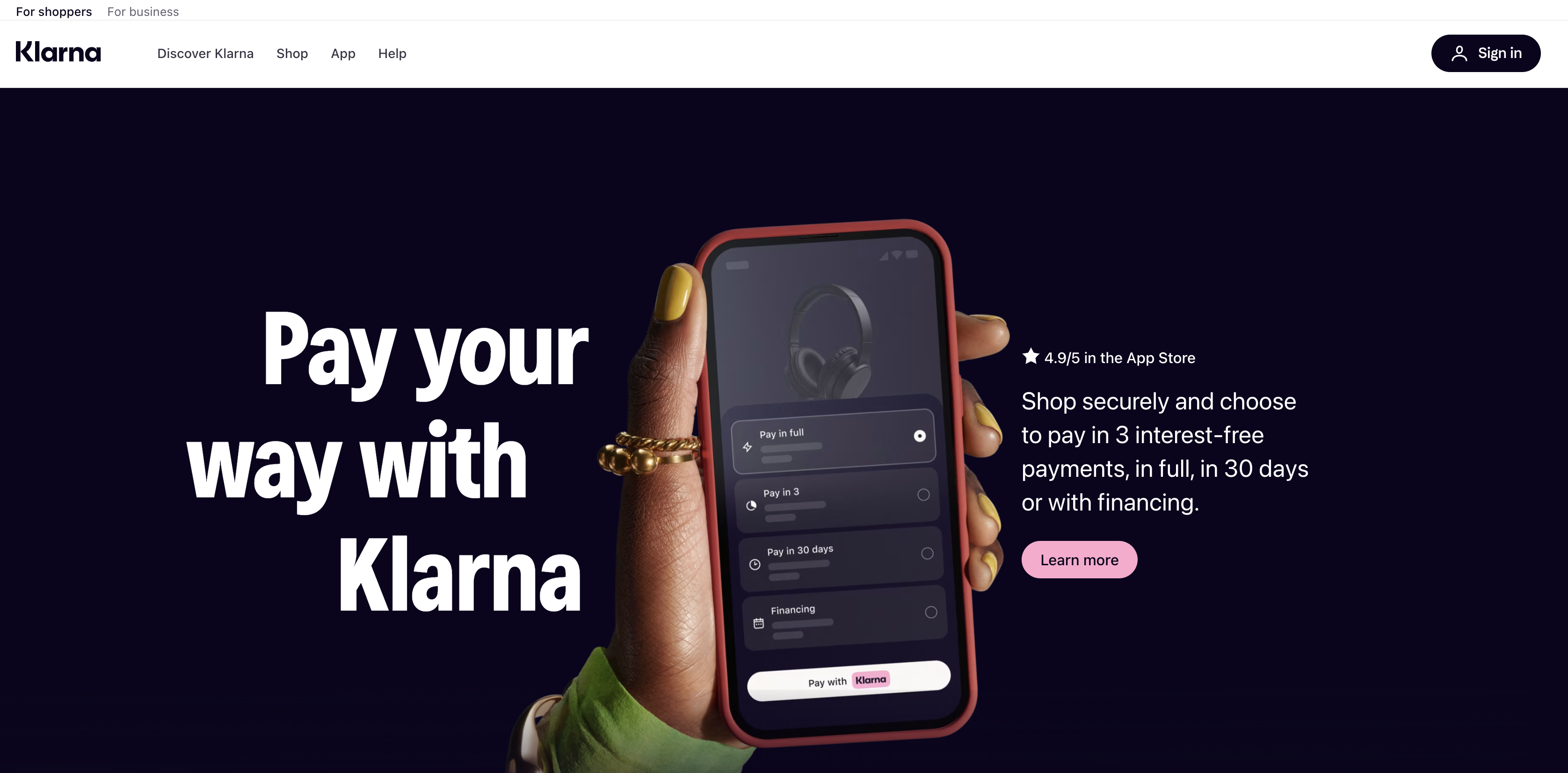

Three Stockholm School of Economics students pitched an idea at a university entrepreneurship competition in 2005: let shoppers receive goods before they pay, and put the credit risk on the merchant side. The pitch finished last. They built it anyway. Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson launched what was originally called Kreditor, later renamed Klarna, and spent the next two decades turning that rejected idea into one of Europe's most recognised fintech brands. The core insight held up: millions of people would rather split a purchase into three instalments than reach for a credit card, and merchants would pay for the privilege of offering that option because it reduces cart abandonment and increases average order values. Klarna grew from a Swedish checkout button into something considerably more complex. It now holds a banking licence in Sweden, offers savings accounts, issues its own card, and operates across more than 45 markets with around 93 million active consumers and 675,000 merchant partners at the end of 2024. The US, which Klarna entered in 2015, has become its largest market by revenue, a fact the company underlined by listing on the New York Stock Exchange in September 2025 under the ticker KLAR, raising $1.37 billion at IPO. The financial trajectory has been bumpy. Klarna reported net income of $21 million in 2024, a return to profitability after a bruising 2022 that included an 85% valuation cut and significant layoffs that reduced headcount from over 7,000 to around 3,400. What survived the restructuring was a leaner company with $2.81 billion in revenue and a clearer strategic direction: AI. Klarna's partnership with OpenAI produced a customer service assistant it claims handles the equivalent of 700 full-time agents, and generative AI now manages roughly two-thirds of customer chats. The honest assessment of where Klarna sits today: it's no longer purely a BNPL provider and it's not quite a bank. It's somewhere in between, a consumer finance platform that knows more about your shopping behaviour than your bank does, and is betting that's worth a lot.

Daniel Kjellén and Fredrik Hedberg didn't set out to build infrastructure. Tink started in Stockholm in 2012 as a consumer personal finance app — an attempt to give Swedish bank customers a cleaner view of their money across multiple accounts. It was a reasonable idea that ran into an unreasonable obstacle: getting reliable, consistent data out of European banks was extraordinarily hard. The technical problem turned out to be more interesting than the consumer product. In 2018 they pivoted, shifted focus entirely to the B2B layer, and started selling the very infrastructure they'd been forced to build for themselves. That pivot proved prescient. The EU's PSD2 directive, which came into full effect in 2019, legally required banks to open their data to authorised third parties — creating the regulatory foundation that open banking platforms needed to operate at scale. Tink had spent years building exactly those bank connections. When the regulation arrived, the company was ready. The platform Kjellén and Hedberg built connects to more than 3,400 banks and financial institutions across Europe, reaching over 250 million bank customers. Through a single API integration, banks, fintechs, and merchants can access aggregated account data, initiate payments directly from customer bank accounts, verify account ownership, and enrich transaction data — without maintaining their own connections to hundreds of separate banking systems with different technical standards and update schedules. Clients include Klarna, PayPal, NatWest, ABN AMRO, and BNP Paribas Fortis. In March 2022, Visa completed the acquisition of Tink for €1.8 billion — one of the largest European fintech acquisitions of that year, and a clear signal of how seriously the global payments industry had come to take open banking infrastructure. Visa's strategic rationale was straightforward: it had failed to acquire Plaid, the US equivalent, after an antitrust challenge, and needed a European open banking capability. Tink gave it 500 employees, 18 European markets, and relationships with over 300 banks and fintechs built over a decade. The founders stayed on as CEO and CTO through the transition, continuing to run Tink as a standalone Visa subsidiary from Stockholm. Both departed in 2025 — Kjellén and Hedberg announced they were building Freda, a new AI-driven legal and compliance technology startup, with the pair describing Tink as "now in better hands than ever." Francois Tornier, Visa's VP of Open Banking, took over as CEO. The product roadmap has continued under Visa ownership, including a 2024 expansion of Tink's open banking platform into the US market.

Most companies still manage corporate spending the way they did a decade ago—expense reports, manual reconciliation, scattered receipts. Payhawk has built something radically simpler: a unified spending platform that gives finance teams complete visibility into every company transaction, from the moment it's authorized to the moment it's reconciled. The platform combines physical and virtual cards, automated expense management, and real-time spend controls in a single dashboard. What sets Payhawk apart in the crowded corporate finance space is its refusal to compromise on user experience. Employees aren't fighting clunky interfaces or wrestling with legacy systems. Instead, they get an intuitive mobile app that feels like personal fintech, while finance teams gain the analytical firepower to actually manage policy, catch fraud, and optimize spending patterns. The company treats visibility not as a nice-to-have but as the foundation of control. In Europe's SME and mid-market space, where most alternatives still rely on outdated card programs or disconnected software suites, Payhawk's integration of issuance, spend management, and analytics represents a meaningful shift. The company has quietly built something that enterprises have wanted for years: a spending platform that doesn't require compromise between employee experience and financial governance. For finance leaders tired of spreadsheets and reactive reporting, it's become the natural choice.

Younited provides instant credit and embedded lending across Europe.

Checkout.com is a global payments infrastructure company that builds the plumbing beneath the surface of e-commerce. While most payment processors still operate like legacy banking rails, Checkout.com has constructed a single API that connects directly to card networks, acquiring banks, and alternative payment methods—eliminating the middlemen that slow everything down. The platform processes payments in over 150 currencies across 195 countries, handling everything from straightforward card transactions to complex multi-currency settlements for merchants operating at scale. What sets it apart in Europe and beyond is its refusal to be a typical payment gateway: instead of asking merchants to adapt to the network, Checkout.com adapts the network to the merchant. Founded in 2012 by Guillermo Gutiérrez García-Ceballos, the company has grown from a London-based startup into a critical piece of infrastructure for enterprises, fintechs, and marketplaces that need orchestration at the transaction level. It competes with traditional acquirers and modern payment platforms by combining the reliability of legacy banking with the speed and flexibility developers expect. In the fragmented European payments landscape, Checkout.com has become indispensable for companies that refuse to compromise on latency, coverage, or control. The company represents a fundamental shift in how payments should work: less about choosing between payment methods and more about making payments invisible.