← Back to Payhip

Alternatives

Alternatives to Payhip

Explore 12 European fintech companies similar to Payhip — operating in Embedded Finance and Payments.

12 alternatives to Payhip

Sorted by similarity and popularityAdyen

Embedded FinanceFinancial InfrastructurePayments

🇳🇱 Netherlands

Pieter van der Does and Arnout Schuijff had already built and sold one payments company when they sat down in 2006 to start again. The result was Adyen — the name literally means "start over" in Surinamese — and the premise was simple: instead of stitching together the same fragmented payment infrastructure everyone else was using, they would build the whole thing themselves from scratch.

That decision, made in an Amsterdam office nearly two decades ago, is still the reason Adyen is different. Most payment companies are assemblers — they buy a gateway here, a processor there, bolt them together and hope for the best. Adyen owns its own technology stack end to end, which means a merchant integrating once gets access to card processing, local payment methods, point-of-sale terminals, and real-time settlement data through a single platform. No middle layers, no reconciliation headaches, no finger-pointing between vendors when something breaks.

The client list tells you everything about where Adyen sits in the market. McDonald's, Spotify, Microsoft, LVMH, H&M — these are companies with serious payment volumes and zero appetite for systems that don't work. Adyen became the default choice for enterprises that had outgrown the limitations of traditional payment stacks and needed something that could handle global scale without buckling.

Since going public on Euronext Amsterdam in 2018, Adyen has grown into one of Europe's most valuable technology companies, with around 4,300 employees across 23 countries and net revenue of just under €2 billion in 2024. It remains headquartered in Amsterdam and consistently profitable — a combination that's rarer in fintech than it should be.

For businesses that treat payments as infrastructure rather than an afterthought, Adyen is the benchmark everything else gets measured against.

Founded 2006

View profile →

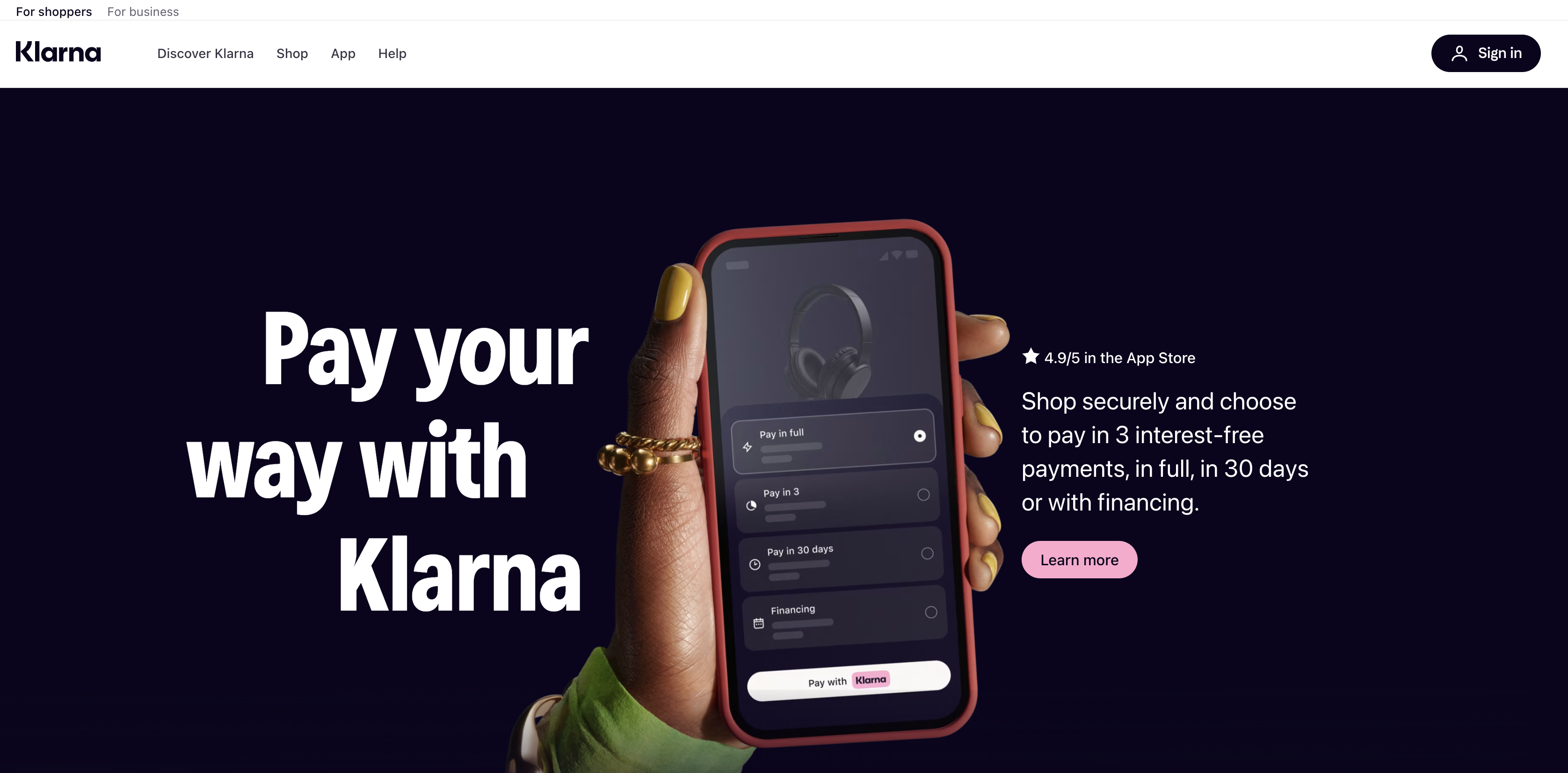

Klarna

Embedded FinancePaymentsDigital BankingBNPL

🇸🇪 Sweden

Three Stockholm School of Economics students pitched an idea at a university entrepreneurship competition in 2005: let shoppers receive goods before they pay, and put the credit risk on the merchant side. The pitch finished last. They built it anyway.

Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson launched what was originally called Kreditor, later renamed Klarna, and spent the next two decades turning that rejected idea into one of Europe's most recognised fintech brands. The core insight held up: millions of people would rather split a purchase into three instalments than reach for a credit card, and merchants would pay for the privilege of offering that option because it reduces cart abandonment and increases average order values.

Klarna grew from a Swedish checkout button into something considerably more complex. It now holds a banking licence in Sweden, offers savings accounts, issues its own card, and operates across more than 45 markets with around 93 million active consumers and 675,000 merchant partners at the end of 2024. The US, which Klarna entered in 2015, has become its largest market by revenue, a fact the company underlined by listing on the New York Stock Exchange in September 2025 under the ticker KLAR, raising $1.37 billion at IPO.

The financial trajectory has been bumpy. Klarna reported net income of $21 million in 2024, a return to profitability after a bruising 2022 that included an 85% valuation cut and significant layoffs that reduced headcount from over 7,000 to around 3,400. What survived the restructuring was a leaner company with $2.81 billion in revenue and a clearer strategic direction: AI. Klarna's partnership with OpenAI produced a customer service assistant it claims handles the equivalent of 700 full-time agents, and generative AI now manages roughly two-thirds of customer chats.

The honest assessment of where Klarna sits today: it's no longer purely a BNPL provider and it's not quite a bank. It's somewhere in between, a consumer finance platform that knows more about your shopping behaviour than your bank does, and is betting that's worth a lot.

Founded 2005

View profile →

Checkout.com

Embedded FinanceFinancial InfrastructurePayments

🇬🇧 United Kingdom

Checkout.com is a global payments infrastructure company that builds the plumbing beneath the surface of e-commerce. While most payment processors still operate like legacy banking rails, Checkout.com has constructed a single API that connects directly to card networks, acquiring banks, and alternative payment methods—eliminating the middlemen that slow everything down. The platform processes payments in over 150 currencies across 195 countries, handling everything from straightforward card transactions to complex multi-currency settlements for merchants operating at scale.

What sets it apart in Europe and beyond is its refusal to be a typical payment gateway: instead of asking merchants to adapt to the network, Checkout.com adapts the network to the merchant. Founded in 2012 by Guillermo Gutiérrez García-Ceballos, the company has grown from a London-based startup into a critical piece of infrastructure for enterprises, fintechs, and marketplaces that need orchestration at the transaction level. It competes with traditional acquirers and modern payment platforms by combining the reliability of legacy banking with the speed and flexibility developers expect.

In the fragmented European payments landscape, Checkout.com has become indispensable for companies that refuse to compromise on latency, coverage, or control. The company represents a fundamental shift in how payments should work: less about choosing between payment methods and more about making payments invisible.

Founded 2012

View profile →

ClearBank

Embedded FinanceFinancial InfrastructurePayments

🇬🇧 United Kingdom

ClearBank provides cloud-based clearing, accounts, and embedded banking infrastructure.

Founded 2015

View profile →

Paynetics

Embedded FinanceFinancial InfrastructurePayments

🇧🇬 Bulgaria

Paynetics operates at the intersection of payment infrastructure and embedded finance, building the plumbing that lets fintechs and traditional companies accept, process, and manage payments without wrestling with legacy banking systems. The Bulgarian-founded company has positioned itself as a critical middleware layer—connecting merchants, fintech platforms, and financial institutions through a unified API. Rather than forcing clients into proprietary ecosystems, Paynetics emphasizes flexibility and interoperability, allowing partners to plug into multiple acquiring networks, payment gateways, and settlement rails from a single integration point. This approach has resonated particularly with regional players across Europe seeking alternatives to Western-dominated payment processors.

The company's strength lies not in flashy consumer-facing products but in unglamorous, essential infrastructure: payment orchestration that routes transactions intelligently, card issuing APIs that power embedded finance plays, and acquiring services that work across markets where local nuance matters. For fintech founders building in Central and Eastern Europe or scaling across fragmented European payment corridors, Paynetics removes the friction of navigating dozens of local processors and compliance regimes. Its expansion into treasury and FX services suggests ambitions beyond pure payments—positioning itself as a platform for companies managing cross-border complexity. In an industry dominated by American giants and large European incumbents, Paynetics represents a rare example of a challenger emerging from the region's underestimated fintech ecosystem, proving that critical infrastructure doesn't always require Silicon Valley pedigree.

Founded 2013

View profile →

Mangopay

Embedded FinanceFinancial InfrastructurePayments

🇱🇺 Luxembourg

Mangopay sits at the intersection of payments infrastructure and marketplace complexity. Rather than selling fintech features individually, the company tackles the full stack problem: how do you actually move money between dozens of parties—buyers, sellers, platforms, creators—when everyone needs different settlement rules and nobody trusts a stranger with their cash.

Founded in 2011, Mangopay is a Brussels-based powerhouse that specializes in payout infrastructure for marketplaces, platforms, and creator economies. The platform handles the messy reality of modern commerce: a freelancer in Barcelona getting paid by a client in London, a marketplace taking commission, a payment processor taking a fee, and a tax authority wanting its cut—all simultaneously, all reconciled, all compliant.

What sets Mangopay apart is its pragmatism. While most payment processors treat multi-party transactions as an edge case, Mangopay designed around it from the start. The company's white-label approach means you barely know it's there—you integrate their APIs, they handle the regulatory nightmare, and your users see your brand. That's the opposite of fintech theater.

The European fintech world has fractured into specialists: payments here, compliance there, ledger systems somewhere else. Mangopay refuses that fragmentation. In a landscape where payment orchestration feels trendy and new, Mangopay has been solving it at scale for over a decade.

Founded 2011

View profile →

Enity

Embedded FinancePaymentsLending

🇩🇪 Germany

Enity sits at the intersection of embedded finance and merchant payments, letting businesses embed lending directly into their checkout flows. Rather than forcing customers to apply for credit elsewhere, Enity's API lets companies offer point-of-sale financing instantly—think Buy Now, Pay Later but more flexible and customizable. The platform handles underwriting, decisioning, and funding, meaning merchants don't carry the credit risk themselves. It's the kind of infrastructure that makes sense as e-commerce and marketplaces mature beyond simple transaction processing. Enity works across Europe, tapping into fragmented credit markets where unified APIs for embedded finance remain rare. The company positions itself against both traditional BNPL providers—which often dictate terms to merchants—and against the friction of integrating multiple lenders. Its real edge is speed and developer experience: getting live takes days, not months. For merchants handling high-value transactions or B2B sales, Enity's underwriting engine and multi-lender orchestration solve a genuine pain point. The rise of embedded lending means platforms like this will become table stakes for any serious commerce infrastructure player.

Founded 2020

View profile →

Rapyd

Embedded FinanceFinancial InfrastructurePayments

🇬🇧 United Kingdom

Rapyd is a global fintech infrastructure company that lets businesses accept payments and move money across 170+ countries without needing local banking relationships. Rather than forcing companies to navigate fragmented payment ecosystems country by country, Rapyd abstracts away the complexity—providing a single API that connects to local payment methods, wallets, and bank accounts everywhere from Southeast Asia to Latin America. The platform handles the unglamorous but essential work: acquiring local licenses, managing compliance, and integrating with hyperlocal payment rails so a startup in Berlin can charge a customer in Lagos as easily as one in London. For merchants and platforms operating globally, this means ditching the spreadsheet of payment processors and compliance frameworks. Instead of cobbling together 15 different providers to cover emerging markets, they get one dashboard, one contract, one API. Rapyd has positioned itself as the plumbing for the next wave of global commerce—the infrastructure layer that makes it possible for any business to think globally from day one, not after they've scaled. In a fintech landscape dominated by Western-centric payment networks, Rapyd's bet on true geographic diversity and local payment methods feels like a deliberate counterweight, making it an essential piece of the infrastructure for companies serious about serving the rest of the world.

Founded 2018

View profile →

Worldpay

Embedded FinanceFinancial InfrastructurePayments

🇬🇧 United Kingdom

Worldpay is one of Europe's most established payment infrastructure plays, handling transactions at the backbone of commerce across the continent. The company processes payments for retailers, e-commerce merchants, and financial institutions, sitting at the critical intersection where customer intent becomes settled value. Rather than chasing consumer attention, Worldpay operates in the plumbing layer—orchestrating card payments, merchant acquiring, and real-time settlement across borders with the quiet efficiency of infrastructure that's been stress-tested for decades. It's the kind of company most Europeans have never heard of but rely on every time they buy something online or in-store. What sets Worldpay apart in a crowded acquiring space is its scale and geographic reach. While newer fintech challengers chase flashy use cases, Worldpay manages the unglamorous work of connecting merchants to banks, processing disputes, and maintaining 99.9% uptime across payment rails that move billions. The company has evolved from a pure processor into a platform, offering tools for payment orchestration, subscription billing, and omnichannel commerce support. Its strength lies not in disruption but in resilience and reach—it powers payments for everything from corner shops to multinational retailers. In the European fintech ecosystem, Worldpay represents institutional financial infrastructure: old enough to be trusted, large enough to absorb regulatory change, and integrated deeply enough that replacing it would be prohibitively complex for most businesses.

Founded 1989

View profile →

Satispay

Embedded FinancePayments

🇮🇹 Italy

Satispay cuts through the noise of payment processing by letting consumers pay directly from their bank account at checkout, skipping cards entirely. It's a mobile-first payment solution that arrived in Europe when digital wallets were becoming ubiquitous, but with a twist: it works offline and without requiring consumers to pre-load funds or enter card details repeatedly.

The company operates across Italy, France, Belgium, and other European markets, positioning itself as a bridge between traditional banking and modern commerce. Rather than competing head-to-head with card networks, Satispay enables merchants to accept payments through a lightweight app integration, with consumers confirming transactions via their phones in seconds.

What sets Satispay apart is its focus on simplicity and lower merchant costs compared to card acquiring. While payment gateways obsess over feature parity with every major card scheme, Satispay keeps the experience minimal: scan, tap, pay. It appeals to retailers tired of high interchange fees and consumers who prefer direct bank debits over recurring card charges.

In a fragmented European payments landscape, Satispay represents a pragmatic alternative to cards for in-store and online commerce, carving out space by solving a specific friction point rather than trying to be everything.

Founded 2013

View profile →

Revolut

WealthPaymentsDigital BankingCrypto & BlockchainPersonal Finance

🇱🇹 Lithuania

Nik Storonsky grew up moving between Russia and France before landing in London as a derivatives trader. Vlad Yatsenko was a software engineer who'd spent years building financial systems. In 2015 they sat down and asked a question that should have occurred to banks years earlier: why does spending money abroad still cost so much?

The answer they built was Revolut — initially a prepaid card with no foreign exchange fees, then a multi-currency account, then a trading platform, then an insurance product, then a business banking offering, then something that's increasingly hard to describe as anything other than a full financial operating system. Revolut didn't unbundle banking so much as rebuild it from scratch for people who found the existing version frustrating and expensive.

The numbers now are genuinely striking for a company that started with two people and a card. Revenue reached £4.5 billion in 2025, up 46% year on year, with net profit of £1.3 billion. The customer base grew to 68.3 million retail users — one in five working-age adults in Europe — plus 767,000 businesses. The company employs 12,200 people across more than 25 countries and was valued at $75 billion in a November 2025 secondary share sale, making it Europe's most valuable private technology company.

The milestone that mattered most, though, arrived in March 2026: a full UK banking licence from the Prudential Regulation Authority, ending a three-year application process that had become the most-watched regulatory saga in European fintech. The licence means Revolut can now protect UK deposits up to £120,000, offer authorised consumer credit, and compete directly with high street banks for mortgage and lending business. It's the piece that transforms Revolut from a very successful payments app into a regulated bank.

The company has also applied for a US banking charter and is expanding aggressively into Latin America, having opened its first bank outside Europe in Mexico. The original thesis — that banking could be cheaper, faster, and simpler — hasn't changed. The scale at which it's now being tested has.

Founded 2015

View profile →

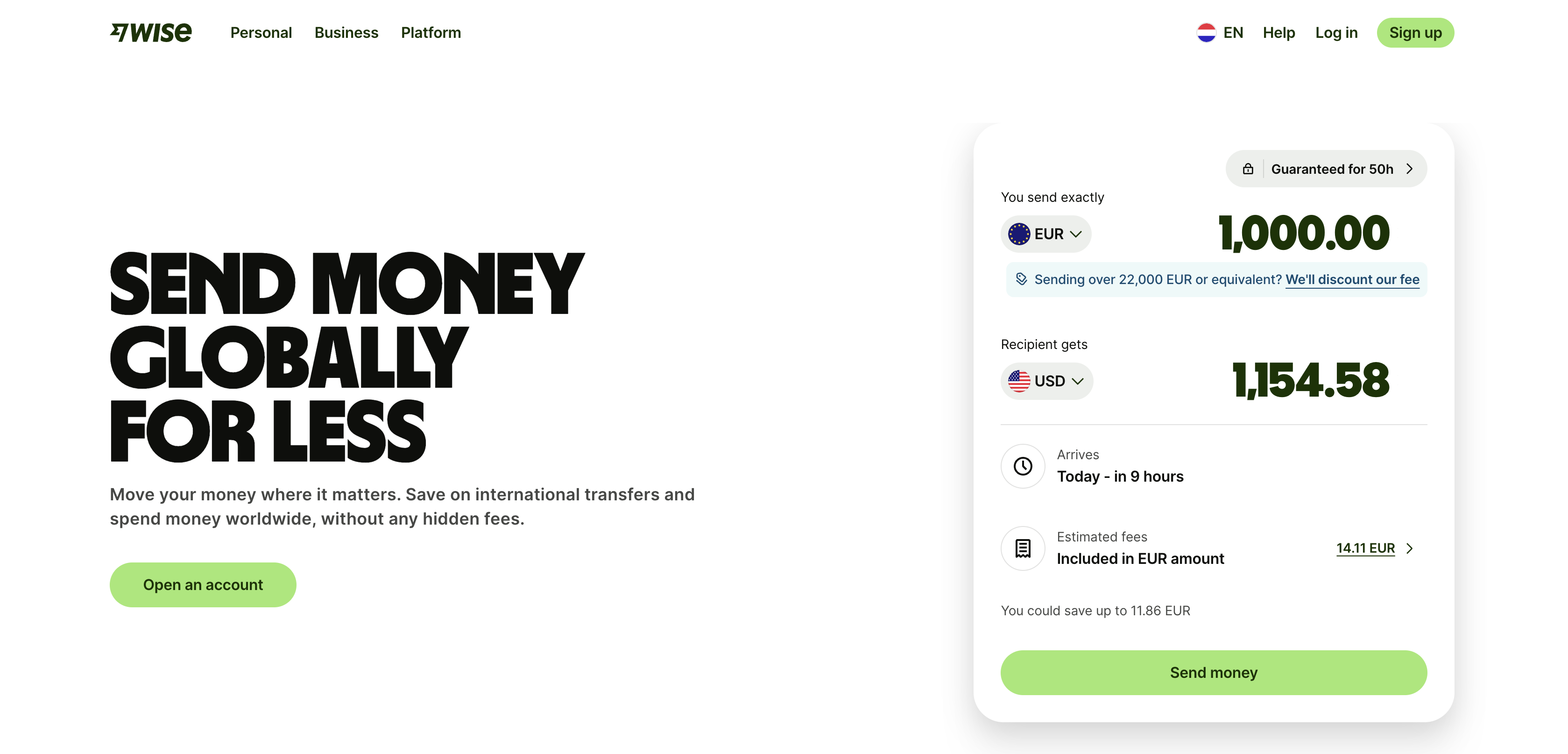

Wise

PaymentsDigital Banking

🇬🇧 United Kingdom

Taavet Hinrikus had a problem that was embarrassingly simple to describe and maddeningly hard to solve. He was one of Skype's first employees, living in London and getting paid in euros while his bills were in pounds. Every month he was losing money to bank fees and exchange rate markups that his bank never disclosed upfront. Kristo Käärmann, a Deloitte consultant, had the same problem in reverse. In 2011 they sat down, compared rates, and started swapping money directly between each other's bank accounts — bypassing the banks entirely. Then they thought: what if anyone could do this?

That informal arrangement became TransferWise, launched in London in January 2011 with a straightforward promise that banks had been making impossible for decades: the real exchange rate, with fees shown upfront before you commit to a transfer. The early pitch was almost deliberately confrontational — the founders publicly compared bank exchange rate markups to theft, took out billboard ads outside banks, and built a campaign around showing customers exactly how much they were being overcharged. It worked.

TransferWise rebranded to Wise in 2021, the same year it listed directly on the London Stock Exchange — bypassing the traditional IPO process in a move consistent with a company that had spent a decade bypassing traditional financial processes. The listing valued the business at around £9 billion and gave it public-company discipline without the fanfare of a conventional float.

The product has expanded well beyond the original currency transfer use case. Wise now offers multi-currency accounts supporting over 40 currencies, a debit card, a business product for SMEs and freelancers managing cross-border payments, and a platform business that lets banks and other fintechs embed Wise's infrastructure into their own products. By June 2025, the platform had 15.6 million active customers processing £145 billion in cross-border volume annually — up 23% year on year. Revenue crossed £1 billion in 2024, with profit of £354 million.

The most significant recent development is structural: shareholders voted in July 2025 to move Wise's primary listing from London to a US exchange, with the transfer expected by early 2026. It's a pragmatic decision — the US is a large and growing market, the company has money-transmission licences in 48 states, and American institutional investors have historically valued fintech companies at higher multiples than London's market has.

Wise employs around 5,500 people and operates across more than 70 countries. Both founders remain involved — Käärmann as CEO, Hinrikus having stepped back from the board in recent years.

The core offer is deceptively simple. Wise operates its own network rather than renting access to SWIFT, which means it can cut out the middlemen taking cuts at every stage. You send pounds, it converts at the mid-market rate (the one you see on Google), and your recipient gets euros without the usual 3-5% tax that banks quietly extract. The company issues multi-currency accounts and cards that work globally, positioning itself as infrastructure for anyone whose life doesn't fit neatly into a single currency zone.

In the European market, Wise has become synonymous with cross-border reality. While traditional banks still talk about "international banking solutions," Wise customers are already sending money to fifteen countries from their phone without a second thought. The company went public in 2021, which paradoxically made it less of a fintech insurgent and more of an established player—but the underlying model hasn't changed: transparency and efficiency where opacity used to be profitable.

Wise represents a particular kind of fintech maturity: the startup that solved a specific, universal problem well enough that it became essential infrastructure for millions of people operating across borders. Its role in the European landscape is that of the pragmatist, proving that you don't need regulatory capture or cross-subsidization to build a sustainable business in payments.

Founded 2011

View profile →