← Back to Verestro

Alternatives

Alternatives to Verestro

Explore 12 European fintech companies similar to Verestro — operating in Financial Infrastructure and Payments and Treasury.

12 alternatives to Verestro

Sorted by similarity and popularityAdyen

Embedded FinanceFinancial InfrastructurePayments

🇳🇱 Netherlands

Pieter van der Does and Arnout Schuijff had already built and sold one payments company when they sat down in 2006 to start again. The result was Adyen — the name literally means "start over" in Surinamese — and the premise was simple: instead of stitching together the same fragmented payment infrastructure everyone else was using, they would build the whole thing themselves from scratch.

That decision, made in an Amsterdam office nearly two decades ago, is still the reason Adyen is different. Most payment companies are assemblers — they buy a gateway here, a processor there, bolt them together and hope for the best. Adyen owns its own technology stack end to end, which means a merchant integrating once gets access to card processing, local payment methods, point-of-sale terminals, and real-time settlement data through a single platform. No middle layers, no reconciliation headaches, no finger-pointing between vendors when something breaks.

The client list tells you everything about where Adyen sits in the market. McDonald's, Spotify, Microsoft, LVMH, H&M — these are companies with serious payment volumes and zero appetite for systems that don't work. Adyen became the default choice for enterprises that had outgrown the limitations of traditional payment stacks and needed something that could handle global scale without buckling.

Since going public on Euronext Amsterdam in 2018, Adyen has grown into one of Europe's most valuable technology companies, with around 4,300 employees across 23 countries and net revenue of just under €2 billion in 2024. It remains headquartered in Amsterdam and consistently profitable — a combination that's rarer in fintech than it should be.

For businesses that treat payments as infrastructure rather than an afterthought, Adyen is the benchmark everything else gets measured against.

Founded 2006

View profile →

Mollie

Financial InfrastructurePayments

🇳🇱 Netherlands

Adriaan Mol built Mollie's first backend while living with his parents in the Netherlands in 2004. No investors, no office, no team — just a founder and an idea that small businesses deserved a payment integration that didn't require a team of lawyers and a six-month setup process. He bootstrapped it for over fifteen years before taking outside funding in 2019. By then, Mollie had already grown into one of the most important payment platforms in European e-commerce, entirely on the back of a product that developers actually liked using.

The proposition is straightforward: one API, one dashboard, and access to the payment methods that actually matter across Europe. That means iDEAL in the Netherlands, Bancontact in Belgium, Klarna and SEPA Direct Debit everywhere, alongside cards, Apple Pay, and a growing list of local methods that would otherwise require separate integrations and separate acquirer relationships. Mollie handles the compliance, the fraud monitoring, and the settlement complexity. Merchants get a clean interface and a single invoice.

For the 250,000 businesses using Mollie today — ranging from Gymshark and Wild to local bakeries and market stalls, as CEO Koen Köppen regularly points out — the appeal is less about feature lists and more about what they don't have to think about. European payments are fragmented by design. Every country has its preferred methods, its own regulatory quirks, its own consumer habits. Mollie's job is to make that invisible.

The numbers from 2024 reflect a company that has found its model. Revenue reached €214 million, up 28% year on year, with gross profit growing 30% to €115 million and the company returning to positive EBITDA for the first time since 2018. Mollie raised a total of $940 million in funding and was valued at $6.5 billion following its 2021 Series C led by Blackstone.

The most significant recent development is the acquisition of GoCardless in December 2025 — bringing the UK-based direct debit specialist into the Mollie group and substantially expanding its recurring payments and bank transfer capabilities across Europe. Combined, the two companies cover a considerable share of European e-commerce payment infrastructure.

Mollie is still headquartered in Amsterdam, with around 900 employees across offices in Ghent, London, Lisbon, Munich, Milan, Paris, and beyond.

Founded 2004

View profile →

SumUp

Financial InfrastructurePaymentsDigital BankingSME Finance

🇩🇪 Germany

SumUp is Europe's answer to the merchant services problem: a scrappy fintech that turned point-of-sale payments into something actually accessible. While legacy payment processors still treat small businesses like second-class customers, SumUp built hardware and software that work together seamlessly, letting anyone from a street vendor to a café owner accept cards in minutes, not months.

The company started by selling cheap card readers—simple, elegant devices that plugged into phones. But that was just the wedge. Today SumUp offers a stack: card readers, invoicing, basic accounting, and increasingly, working capital tools. It's the financial operating system for the SME who doesn't want to negotiate with a relationship manager.

What sets SumUp apart in Europe is its refusal to stay in the payments lane. Most competitors eventually build one feature and call it a day. SumUp keeps layering—acquiring merchant acquirer licenses, launching its own acquiring infrastructure in key markets, adding payment links and e-commerce solutions. The company operates across Western Europe and beyond, working with hundreds of thousands of merchants who are too small for traditional banking but too important to ignore.

SumUp represents the practical, unglamorous evolution of fintech: it's not trying to reinvent banking or blockchain. It's solving the cash flow problem for people who actually run businesses. That's a bigger opportunity than it sounds.

Founded 2012

View profile →

Checkout.com

Embedded FinanceFinancial InfrastructurePayments

🇬🇧 United Kingdom

Checkout.com is a global payments infrastructure company that builds the plumbing beneath the surface of e-commerce. While most payment processors still operate like legacy banking rails, Checkout.com has constructed a single API that connects directly to card networks, acquiring banks, and alternative payment methods—eliminating the middlemen that slow everything down. The platform processes payments in over 150 currencies across 195 countries, handling everything from straightforward card transactions to complex multi-currency settlements for merchants operating at scale.

What sets it apart in Europe and beyond is its refusal to be a typical payment gateway: instead of asking merchants to adapt to the network, Checkout.com adapts the network to the merchant. Founded in 2012 by Guillermo Gutiérrez García-Ceballos, the company has grown from a London-based startup into a critical piece of infrastructure for enterprises, fintechs, and marketplaces that need orchestration at the transaction level. It competes with traditional acquirers and modern payment platforms by combining the reliability of legacy banking with the speed and flexibility developers expect.

In the fragmented European payments landscape, Checkout.com has become indispensable for companies that refuse to compromise on latency, coverage, or control. The company represents a fundamental shift in how payments should work: less about choosing between payment methods and more about making payments invisible.

Founded 2012

View profile →

Omnius

Financial InfrastructurePayments

🇩🇪 Germany

Omnius is a European fintech infrastructure player that builds the plumbing for digital finance. Rather than launching consumer apps or chasing trends, the company focuses on giving financial institutions and fintech operators the core technology to move faster. The platform handles payment processing, account management, and the underlying APIs that let banks and non-banks operate at scale without reinventing the wheel.

What distinguishes Omnius in a crowded infrastructure market is its pragmatic approach to complexity. European banks still manage legacy core systems alongside new digital channels—a messy, expensive reality most fintech companies ignore. Omnius doesn't fight that; it sits in the middle, connecting old and new, and abstracts the chaos away from the business logic above it.

The company targets institutions that need to modernize faster than their technology stacks allow. That includes challenger banks that need banking-as-a-service foundations, traditional banks building new digital channels, and fintech companies that want to scale without owning every layer. It's unsexy infrastructure work—the kind that doesn't generate headlines but quietly powers the financial services layer that consumers interact with.

In the European fintech stack, Omnius occupies a critical but overlooked position: the vendor that lets faster companies stay fast, and slower ones move at all.

View profile →

Nexi

Financial InfrastructurePaymentsOpen Banking

🇮🇹 Italy

Nexi is Italy's largest payment services operator, controlling the infrastructure that moves money across the country's retail and corporate sectors. Founded in 2013 through a merger of two major Italian payment processors, it manages card transactions, merchant acquiring, and digital payment rails for banks, retailers, and businesses across Europe.

The company operates across the full payments stack—from traditional POS terminals and card networks to modern API-based solutions and instant payment systems. Unlike most fintech startups, Nexi doesn't target consumers directly. Instead, it powers the payment backbone for Italian and European financial institutions and retailers, processing tens of billions in transactions annually. Its business model sits at the intersection of traditional payment infrastructure and modern open banking, positioning it as a critical node in Europe's shift toward real-time payments and embedded finance.

Nexi's role is unglamorous but essential: it's the plumbing that makes modern commerce work, handling everything from contactless cards to mobile wallets to cross-border transfers. In the broader European fintech landscape, it represents the "boring" but profitable core—the infrastructure layer that fintechs themselves depend on to function.

Founded 2013

View profile →

ClearBank

Embedded FinanceFinancial InfrastructurePayments

🇬🇧 United Kingdom

ClearBank provides cloud-based clearing, accounts, and embedded banking infrastructure.

Founded 2015

View profile →

ION Group

Financial InfrastructureRegTechCapital MarketsTreasury

🇬🇧 United Kingdom

ION Group is a sprawling financial software empire that has quietly become one of Europe's most comprehensive infrastructure plays. The company operates across trading, risk management, and post-trade processing—the unsexy but absolutely critical backbone that powers global capital markets. Unlike flashy fintech startups chasing consumer adoption, ION builds the invisible plumbing that institutional traders, hedge funds, and investment banks depend on every single day. Its portfolio spans front-office platforms, market data aggregation, clearing and settlement systems, and regulatory reporting tools. ION serves as a counterweight to the purely consumer-focused fintech narrative, proving there's enormous value in solving problems for professionals who move billions. The company's strength lies in its ability to connect disparate financial systems, providing what amounts to a unified operating system for institutional finance. For European financial institutions, ION represents a trusted partner in an increasingly complex regulatory landscape, offering solutions that integrate seamlessly with legacy infrastructure while modernizing workflows. Its acquisition-driven growth strategy—picking up niche specialists and consolidating them into a cohesive platform—mirrors the broader consolidation happening across enterprise fintech. ION's market position underscores a fundamental truth about fintech: the biggest opportunities often lie in B2B infrastructure rather than consumer apps.

Founded 2005

View profile →

Currencies Direct

PaymentsTreasury

🇬🇧 United Kingdom

Long before Wise existed, there was a generation of UK companies serving the British expatriate community with foreign exchange services that were better than what banks offered, even if they still required phone calls and forms. Currencies Direct was founded in London in 1996 — making it ancient by fintech standards — and built one of the longest-running international payment businesses in Europe by serving exactly that market. Its core customer base has historically been British expatriates buying property abroad, sending pensions overseas, and managing the cross-border financial complexity of living in one country with assets and obligations in another. The company has evolved with the digital era, building online platforms while maintaining the relationship-based service model that its core customers valued — and continue to value, even as younger demographics have moved to app-based alternatives. Currencies Direct has expanded into broader international payment services for SMEs and individuals, processing billions in cross-border transfers annually. In the UK FX landscape, Currencies Direct represents the established alternative — older, more relationship-driven, and serving customer segments that the venture-backed fintechs sometimes overlook in their focus on digital-native users. Three decades of FX service is not nothing.

Founded 1996

View profile →

Swan

Financial InfrastructurePaymentsOpen Banking

🇫🇷 France

Swan is reshaping how European businesses handle payments by offering a modern, developer-friendly infrastructure layer that sits between companies and the complexity of traditional banking rails. Rather than forcing startups and established firms to navigate fragmented payment ecosystems, Swan bundles together payment processing, banking APIs, and compliance tooling into a single, coherent platform.

The company targets mid-market and enterprise customers—think e-commerce platforms, SaaS businesses, and financial services—who need to embed payments into their core operations without hiring a dedicated payments team. Swan's core strength lies in its ability to strip away legacy banking friction: it handles card processing, instant payments, payouts, and cross-border transfers through a unified API, while managing the regulatory headaches that usually consume engineering bandwidth.

In a European landscape crowded with payment gateways and banking APIs, Swan distinguishes itself through developer experience and architectural clarity. Where competitors often bolt together disparate services, Swan presents a genuinely integrated stack—one codebase, one dashboard, one billing model. The company serves as both a payments operator and a bridge to traditional banking, making it particularly valuable for businesses scaling beyond their first million transactions.

Swan represents a broader maturation in European fintech infrastructure: the shift from "we'll process your payments" to "we'll become your payments backbone," enabling a generation of companies to focus on their core product rather than payment plumbing.

Founded 2019

View profile →

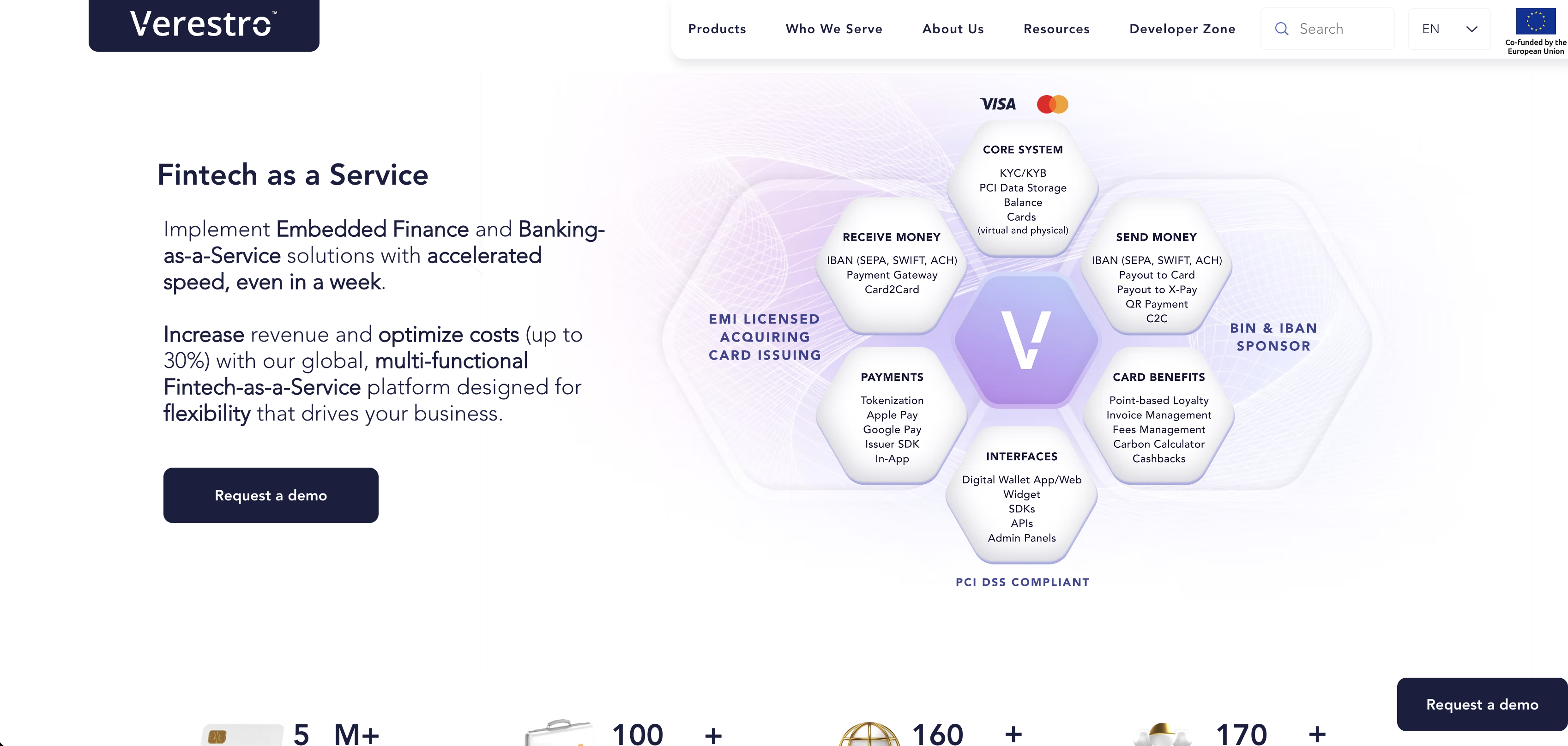

Paynetics

Embedded FinanceFinancial InfrastructurePayments

🇧🇬 Bulgaria

Paynetics operates at the intersection of payment infrastructure and embedded finance, building the plumbing that lets fintechs and traditional companies accept, process, and manage payments without wrestling with legacy banking systems. The Bulgarian-founded company has positioned itself as a critical middleware layer—connecting merchants, fintech platforms, and financial institutions through a unified API. Rather than forcing clients into proprietary ecosystems, Paynetics emphasizes flexibility and interoperability, allowing partners to plug into multiple acquiring networks, payment gateways, and settlement rails from a single integration point. This approach has resonated particularly with regional players across Europe seeking alternatives to Western-dominated payment processors.

The company's strength lies not in flashy consumer-facing products but in unglamorous, essential infrastructure: payment orchestration that routes transactions intelligently, card issuing APIs that power embedded finance plays, and acquiring services that work across markets where local nuance matters. For fintech founders building in Central and Eastern Europe or scaling across fragmented European payment corridors, Paynetics removes the friction of navigating dozens of local processors and compliance regimes. Its expansion into treasury and FX services suggests ambitions beyond pure payments—positioning itself as a platform for companies managing cross-border complexity. In an industry dominated by American giants and large European incumbents, Paynetics represents a rare example of a challenger emerging from the region's underestimated fintech ecosystem, proving that critical infrastructure doesn't always require Silicon Valley pedigree.

Founded 2013

View profile →

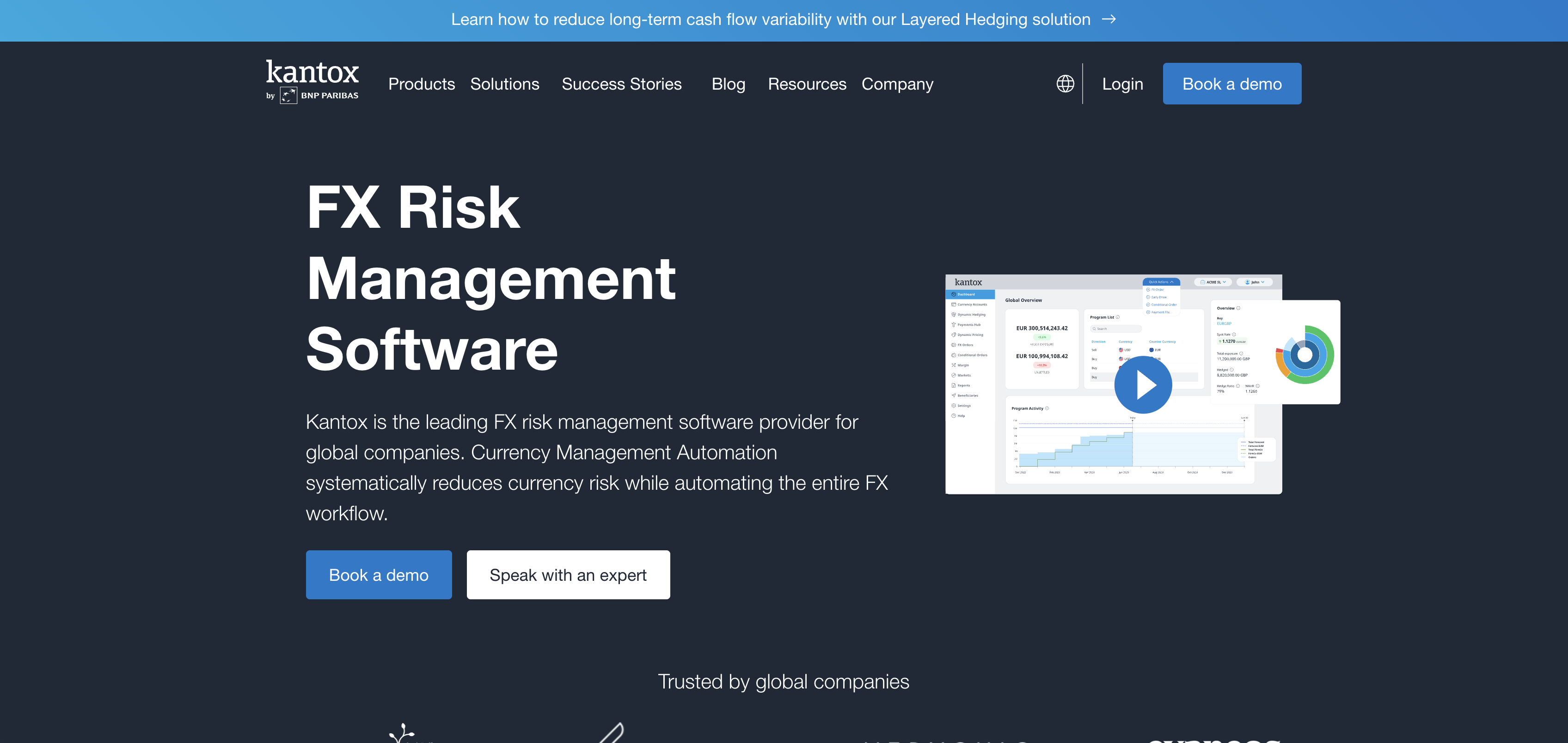

Kantox

PaymentsTreasury

🇪🇸 Spain

Kantox sits at the intersection of corporate finance and fintech, solving a problem that has plagued treasurers and CFOs for decades: the cost and complexity of managing foreign exchange. Rather than forcing companies through the byzantine world of traditional banks or crude hedging tools, Kantox built a platform that lets businesses buy and sell currency with transparency, speed, and intelligence.

The platform aggregates liquidity from multiple sources—banks, non-bank liquidity providers, and peer matching—and surfaces the best rates in real time. No more vendor lock-in, no more opaque spreads, no more waiting. A mid-market company can execute a multi-million euro FX trade in minutes, seeing exactly what they're paying and why.

What sets Kantox apart in a crowded treasury tech space is its refusal to abstract away the mechanics. The platform shows you the market, then lets you trade. It's designed for finance professionals who know what they're doing and want control back from intermediaries. The company has built serious depth in emerging markets and supply chain currencies, which most legacy providers still treat as afterthoughts.

Kantox represents a broader shift in European fintech: the recognition that some of the most valuable problems live in the unglamorous corners of corporate finance, where even small improvements in execution cost save companies millions annually. In that sense, it's doing for FX what more visible fintechs have done for payments—stripping away friction and opacity from a process that should have been digital decades ago.

Founded 2009

View profile →