← All services

34 European companies

accounting integration

Accounting integration connects financial platforms — banks, payment processors, and expense tools — directly to accounting software like Xero, QuickBooks, and Sage, automatically syncing transactions, invoices, and reconciliation data. For small businesses, deep accounting integrations eliminate manual bookkeeping and reduce the risk of errors in financial records.

Typically offered by

European fintech companies offering accounting integration

Pleo

Payments🇩🇰 Denmark

Pleo is a corporate expense management platform that treats company spending like a personal finance problem solved through software. Rather than the tedious reimbursement cycles and spreadsheet chaos of traditional corporate cards, Pleo gives employees physical and virtual cards coupled with real-time expense categorization and approval workflows that happen at the speed of a Slack message.

The company positions itself as the antidote to finance teams drowning in manual reconciliation. Employees get instant card access, automatic receipt capture via smartphone, and intelligent categorization that learns spending patterns. Meanwhile, finance teams gain real-time visibility into company spending without the usual lag and friction.

Pleo operates in a market where most companies still rely on legacy corporate card providers or outdated expense management software that feels bolted together from the 1990s. The Danish fintech has expanded across Europe, building a platform that combines the convenience of consumer fintech with the compliance and control requirements of enterprise finance.

It's become a reference point for how embedded finance and B2B SaaS can simplify workflows that enterprises have tolerated as painful for decades. The company sits comfortably at the intersection of business banking, card issuing, and expense automation—categories that individually are crowded but rarely integrated as seamlessly.

Founded 2015

PayFit

SME Finance🇫🇷 France

PayFit is a French payroll and HR software platform that automates the tedious work of managing employee compensation, benefits, and compliance across Europe. Founded in 2015, the company has built something genuinely useful: a system that lets mid-market companies and SMEs stop wrestling with spreadsheets and outdated payroll systems, and instead manage their entire workforce in one place.

The platform handles everything from salary calculations and tax filings to expense reports and leave management—work that traditionally demanded a dedicated HR department or expensive outsourcing. What sets PayFit apart is its focus on reducing administrative friction rather than just digitizing existing processes. The interface feels designed for actual users, not consultants. It integrates with accounting software and handles the increasingly complex regulatory landscape across France, Germany, Spain, and the UK, where employment law differs wildly but payroll headaches remain universal.

In Europe's fragmented payroll software market, where legacy providers still dominate through inertia, PayFit represents a generational shift toward cloud-first, mobile-friendly HR operations. The company competes less on features (though it has plenty) and more on making payroll feel like a solved problem rather than an annual migraine. It's the kind of infrastructure play that startups and growth companies build themselves around once they've used it—not flashy, but fundamentally necessary.

Founded 2015

Payhawk

Embedded Finance🇧🇬 Bulgaria

Most companies still manage corporate spending the way they did a decade ago—expense reports, manual reconciliation, scattered receipts. Payhawk has built something radically simpler: a unified spending platform that gives finance teams complete visibility into every company transaction, from the moment it's authorized to the moment it's reconciled. The platform combines physical and virtual cards, automated expense management, and real-time spend controls in a single dashboard.

What sets Payhawk apart in the crowded corporate finance space is its refusal to compromise on user experience. Employees aren't fighting clunky interfaces or wrestling with legacy systems. Instead, they get an intuitive mobile app that feels like personal fintech, while finance teams gain the analytical firepower to actually manage policy, catch fraud, and optimize spending patterns. The company treats visibility not as a nice-to-have but as the foundation of control.

In Europe's SME and mid-market space, where most alternatives still rely on outdated card programs or disconnected software suites, Payhawk's integration of issuance, spend management, and analytics represents a meaningful shift. The company has quietly built something that enterprises have wanted for years: a spending platform that doesn't require compromise between employee experience and financial governance. For finance leaders tired of spreadsheets and reactive reporting, it's become the natural choice.

Founded 2019

Ritmo

Digital Banking🇪🇸 Spain

Ritmo is a neobank built specifically for the gig economy—the millions of freelancers, contractors, and self-employed workers across Europe who operate outside traditional employment structures. Instead of forcing gig workers into standard business banking products, Ritmo designed from the ground up to understand the rhythms of irregular income, multiple clients, and the administrative burden that comes with self-employment.

The platform combines a business checking account with invoicing, expense tracking, and tax preparation tools, removing the friction between earning money and managing it. You get real-time visibility into cash flow, automated categorization of business expenses, and direct integration with tax authorities—so when it's time to file, the data is already organized.

What sets Ritmo apart isn't just its feature set. Most fintech players either chase the consumer market or build enterprise solutions for corporations. Ritmo recognized a gap: gig workers are economically significant but underserved by both traditional banks and most neobanks. The company speaks their language, understands their cash flow volatility, and builds products that actually reflect how they work.

In the broader European fintech landscape, Ritmo represents a growing trend of vertical-specific banking platforms. Rather than being all things to all people, it's solving a precise problem for a rapidly growing demographic. For the gig worker tired of explaining variable income to a bank manager or juggling multiple apps, Ritmo is the kind of focused, no-nonsense solution that defines modern fintech at its best.

Founded 2021

Rauva

SME Finance🇵🇹 Portugal

Rauva is a fintech platform built specifically for small business owners who are tired of juggling spreadsheets and fragmented tools. It combines invoicing, expense tracking, and financial reporting into a single dashboard, giving SMEs real-time visibility into their business finances without the accountant overhead. The platform connects directly to bank accounts and automatically categorizes transactions, turning raw financial data into actionable insights.

What sets Rauva apart is its focus on simplicity and speed. Rather than forcing businesses through complicated setup processes or charging enterprise-level fees, it delivers straightforward features that address the immediate pain points SMEs face: understanding cash flow, managing invoices, and staying on top of tax obligations. The interface feels built for people who run businesses, not for finance professionals.

In the crowded landscape of SME fintech, Rauva competes by refusing complexity. While competitors bundle accounting, payroll, and inventory management into bloated suites, Rauva stays laser-focused on financial visibility and reporting. It's the kind of tool a busy founder pulls up on Monday morning without needing a training session. The company has positioned itself as the alternative to traditional accounting software that feels stuck in the 2000s and overly expensive cloud-based platforms that are overkill for small teams.

Rauva represents the practical middle ground in SME finance: powerful enough to matter, simple enough to use.

Founded 2018

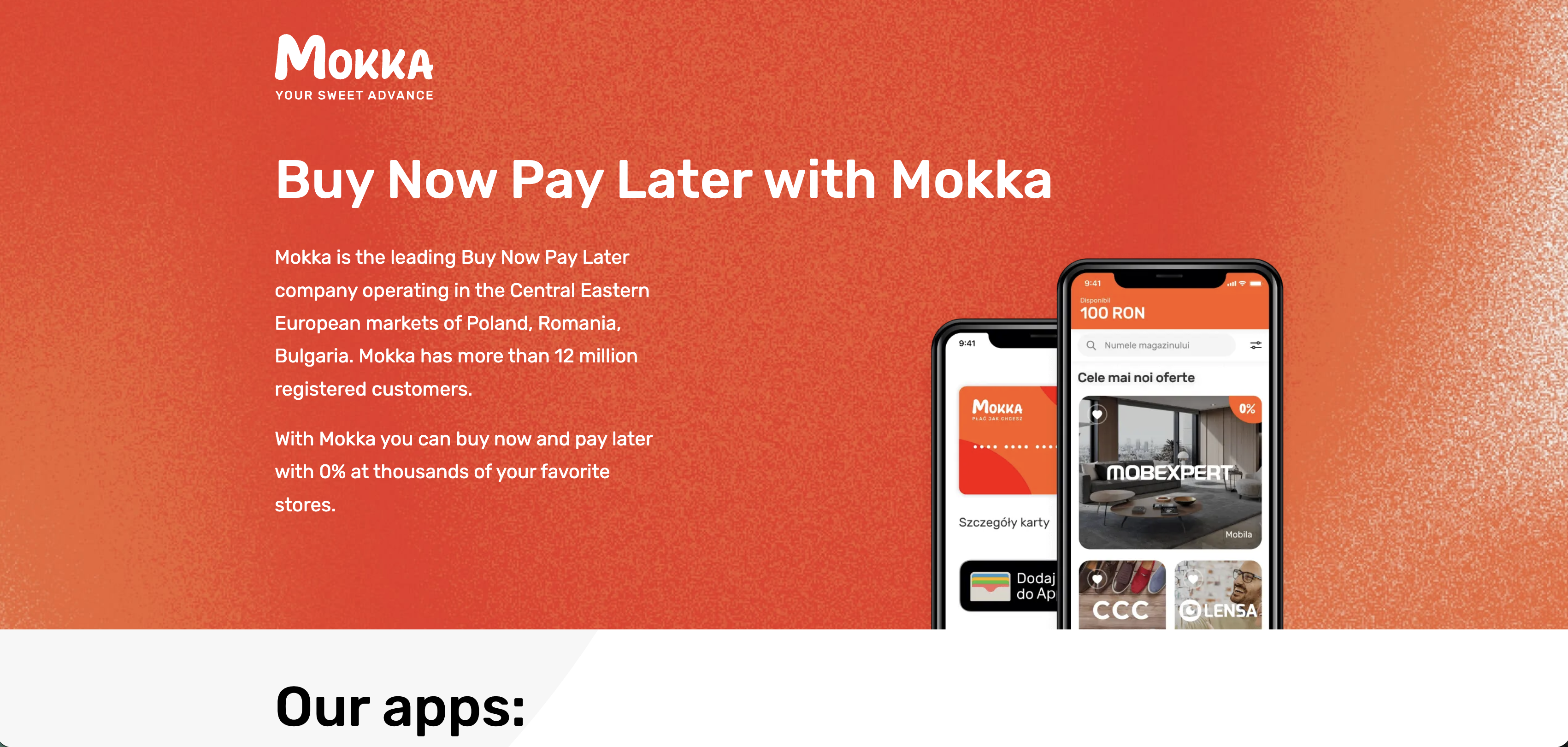

Mokka

Financial Infrastructure🇷🇴 Romania

Mokka is a Romanian fintech platform built for the modern seller. Rather than forcing merchants into the rigid infrastructure of traditional payment processors, Mokka gives them a unified dashboard to manage payments, invoicing, and business basics from one place. The platform handles card payments, digital wallets, and local payment methods—all wired into a clean, merchant-friendly interface that feels less like enterprise software and more like something designed for actual humans. For Romanian SMEs and freelancers tired of juggling multiple logins and opaque fee structures, Mokka offers transparency and control that legacy banking and payment gateways simply don't provide. It's part merchant acquirer, part business backbone—a practical response to how payment infrastructure in Central & Eastern Europe still lags behind Western standards. Mokka sits at the intersection of embedded finance and merchant enablement, serving businesses that want payment functionality without the complexity.

Founded 2020

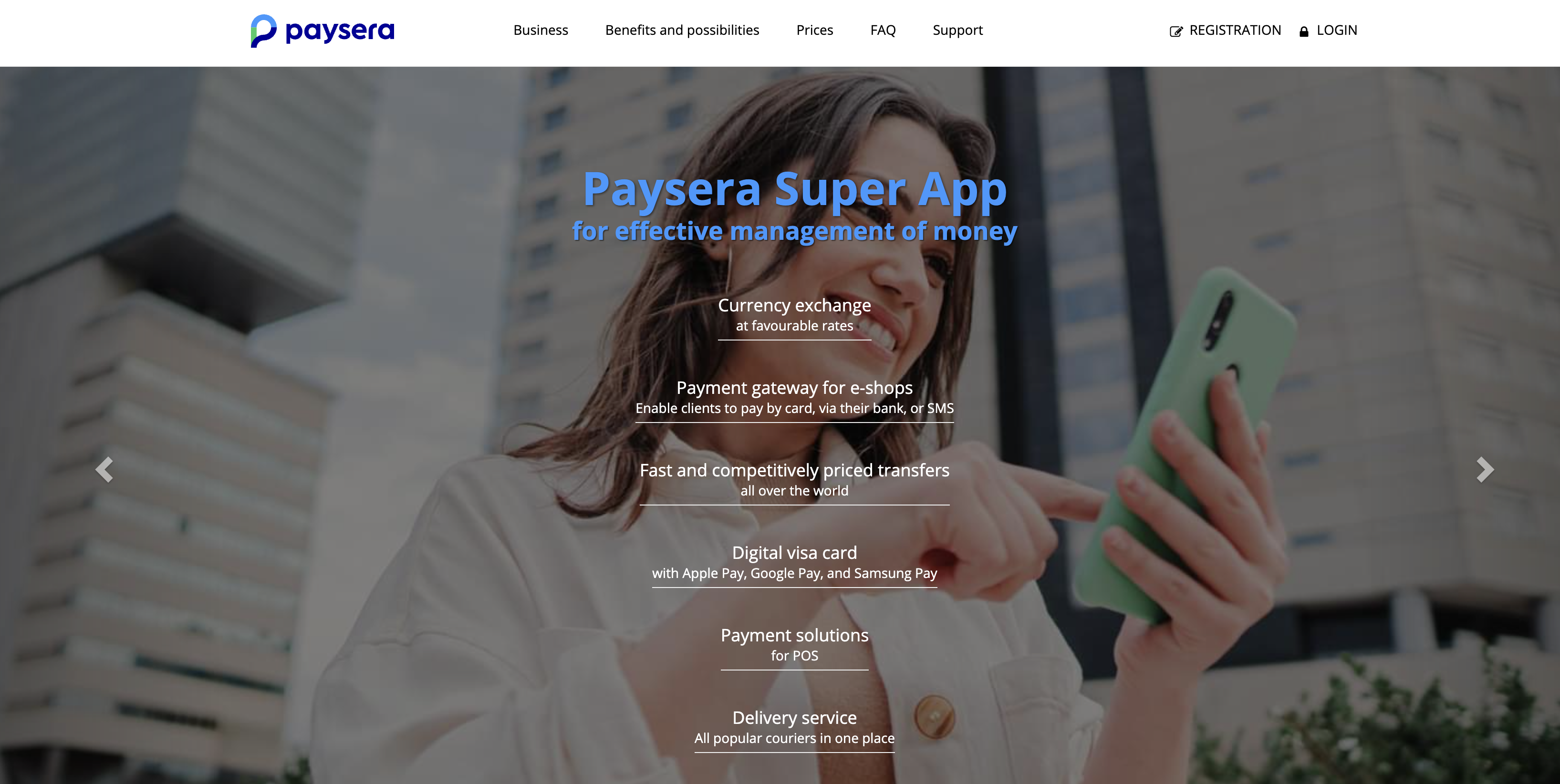

Paysera

Financial Infrastructure🇱🇹 Lithuania

Paysera is a Lithuanian fintech company that has quietly built one of Europe's most comprehensive payment and banking platforms, serving millions of users across the continent. Rather than chasing hype, Paysera focuses on practical utility—combining payment processing, digital accounts, currency exchange, and invoicing tools into a single interface that works across borders and languages. The platform powers everything from freelancers managing invoices to SMEs handling payroll, while also offering consumer-facing services like multi-currency wallets and competitive exchange rates. What sets Paysera apart is its unglamorous pragmatism: it solves real friction in how Europeans move, spend, and manage money across different countries, without the startup theatrics. It's the kind of company that doesn't dominate headlines but has become indispensable infrastructure for a significant portion of the continent's digital economy. In the crowded European fintech landscape, where newer players chase consumer attention and legacy banks chase compliance, Paysera operates in the profitable middle—trusted by businesses and individuals who value reliability and cross-border simplicity over brand prestige.

Founded 2004

Blackcat

SME Finance🇩🇪 Germany

Blackcat is a German fintech platform designed to help freelancers and self-employed professionals manage their finances with minimal friction. Rather than forcing users into complex accounting workflows, Blackcat simplifies the entire money flow—from invoicing to tax filing—with a mobile-first interface that feels more like a consumer app than enterprise software.

The platform tackles a real pain point in the European freelance economy: most existing tools are either bloated legacy systems or fragmented point solutions that don't talk to each other. Blackcat bundles invoicing, expense tracking, tax preparation, and business banking into one coherent experience, removing the cognitive load of juggling multiple services.

What sets Blackcat apart is its opinionated approach to simplicity. Rather than mirroring traditional accounting software's feature sprawl, it prioritizes the workflows that matter most to freelancers—getting paid faster, documenting expenses, and staying tax-compliant without the headache. The platform's integration with German tax authorities and compliance frameworks positions it as particularly valuable in the DACH region, where self-employed taxation can be notoriously complex.

In a market crowded with accounting tools and SME platforms, Blackcat represents a new generation of fintech that starts with the freelancer's actual needs rather than retrofitting legacy processes into a digital wrapper. It's part of a broader shift toward consolidated SME finance platforms that understand that complexity itself is the problem.

Ramp

Financial Infrastructure🇵🇱 Poland

Ramp is rewriting how companies spend money. Built for finance teams tired of spreadsheets and manual processes, it combines a corporate card, expense management, and accounting integrations into a single platform that actually talks to the software finance teams already use. Most corporate card programs feel like they were designed in 1995. Ramp feels like software built this decade—mobile-first, API-forward, and deeply integrated with tools like NetSuite and QuickBooks. The company started by solving a real problem: CFOs and controllers wasting hours reconciling card statements and expense reports. Instead of patching that broken workflow, Ramp replaced it entirely. You get a card, real-time spending controls, automated categorization, and instant syncing to your accounting system. No more manual entries, no more approval bottlenecks, no more spreadsheet chaos. The platform goes deeper than most competitors by combining physical and virtual cards with embedded controls—spend limits by department, merchant category, or individual employee. Finance teams can actually enforce policy in real time rather than auditing violations weeks later. Ramp operates in a crowded space, but it's differentiated by speed and simplicity. Where competitors try to be everything to everyone, Ramp has kept focus on what CFOs actually care about: reducing manual work, improving visibility, and cutting unnecessary spending. Its integration-first approach means it's not trying to replace your entire finance stack—it's designed to slot in and make your existing tools work harder. For mid-market companies tired of manual expense management and lacking the complexity of enterprise-grade solutions, Ramp has become the obvious choice. It's also been ruthless about profitability, reaching positive unit economics early, which matters in a category where many competitors burned through billions before proving their model worked.

Founded 2019

Pennylane

Digital Banking🇫🇷 France

Pennylane is a French fintech that bundles accounting, invoicing, and banking into one platform built for freelancers and small businesses. Rather than piecing together separate tools, users get a unified workspace where transactions sync automatically, expenses categorize themselves, and tax calculations happen in the background. The company positions itself against the fragmented mess of legacy accounting software and generic banking solutions, betting that SMEs want a single interface that actually understands their cashflow.

What sets Pennylane apart in Europe's crowded SME finance space is its focus on simplicity without sacrificing depth. While competitors often target either accountants or business owners, Pennylane aims at the owner-operator who wants to understand their numbers without hiring bookkeeping help. The platform connects directly to bank feeds and invoice data, pulling everything into a dashboard that feels less like traditional accounting software and more like a modern finance app.

Pennylane represents a shift in how European SMEs are expected to manage money. Rather than quarterly accountant visits and spreadsheet chaos, the company argues that modern businesses should have real-time visibility into their finances. It's part of a broader movement to make financial operations software actually enjoyable to use, not just tolerable.

Founded 2018

Spendesk

Financial Infrastructure🇫🇷 France

Spendesk cuts through the chaos of corporate spending. It's a unified platform where teams manage expenses, issue corporate cards, approve invoices, and reconcile everything in one place—no more spreadsheets shuffled across email chains or finance teams drowning in admin work.

The platform sits somewhere between a spend management tool and a modern finance operating system. Companies connect their bank accounts, set spending rules, issue virtual or physical cards to employees, and watch transactions flow into an automated approval workflow. Invoices get coded automatically. Reconciliation happens in real time. The whole thing syncs with accounting software so the numbers always match reality.

What makes Spendesk different is that it treats spend management as a team sport, not a back-office chore. It's built for the actual workflows that modern finance teams use: expense reports that don't feel like punishment, card management that doesn't require IT involvement, and visibility that doesn't require a Ph.D. in Excel. Most competitors bolt features together; Spendesk designed the experience first.

In a market crowded with point solutions and legacy software masquerading as modern, Spendesk has become the de facto standard for mid-market companies in Europe that want to stop thinking about spending and start optimizing it. It's now a critical piece of infrastructure in how thousands of companies handle money.

Founded 2015

Qonto

Payments🇫🇷 France

Qonto is a European business banking platform that treats SMEs and freelancers the way tech-forward founders wish their banks would: fast, transparent, and built for how modern companies actually operate. Instead of waiting days for payments to clear or wrestling with legacy banking interfaces, Qonto users get instant payments, real-time visibility across their accounts, and integrations that sync seamlessly with their existing tools.

The platform lives at the intersection of traditional banking and fintech simplicity. Qonto handles everything from multi-currency accounts and payment processing to expense management and financial reporting, all from a mobile-first interface that feels like an app, not a bank. The company has quietly become the go-to choice for growing SMEs across Europe who want banking that doesn't slow them down.

What sets Qonto apart in a crowded B2B banking space is its obsessive focus on the user experience and its commitment to European expansion. While many neobanks either chase mass-market consumers or hide behind enterprise complexity, Qonto sits in a sweet spot: accessible enough for a solo founder, powerful enough for teams managing millions in annual revenue. The company's growth across France, Germany, Spain, Italy, and beyond reflects a simple truth: European businesses have been waiting for a bank that understands their needs.

As European business banking undergoes its biggest transformation in decades, Qonto stands as proof that the future of SME finance isn't about moving fast and breaking things—it's about moving fast and building things that actually work.

Founded 2016

Showing 12 of 34 companies. View all in the directory →