← All services

7 European companies

debt planning

Debt planning tools help individuals and businesses understand, organise, and systematically reduce their debt obligations by providing visibility into outstanding balances, interest costs, repayment timelines, and prioritisation strategies. Some platforms connect directly to creditors or facilitate debt consolidation. Clear visibility into total debt and its cost is the first step in managing it effectively.

Typically offered by

European fintech companies offering debt planning

Anyfin

Lending🇸🇪 Sweden

Anyfin sits at the intersection of fintech and banking infrastructure, solving a problem most people don't know they have: buried in their financial life are loans and credit products scattered across multiple institutions, often at unfavorable terms. The Stockholm-based platform aggregates these fragmented debts and refinances them into a single, optimized package—think of it as a financial consolidation layer that actually works. Rather than building another neobank or another loan origination system, Anyfin focuses on the underserved middle ground: helping customers reclaim control of debt they already have, often saving thousands in the process.

The company positions itself as a counterweight to the traditional banking industry's opacity around refinancing, where customers rarely know whether they're getting a fair deal. What sets Anyfin apart in the crowded Nordic fintech scene is its technology-first approach to credit decisioning and underwriting, combined with a genuine mission to democratize access to better loan terms. It operates across multiple Scandinavian markets and has built partnerships with traditional financial institutions who recognize that Anyfin's platform actually drives better customer outcomes rather than cannibalizing their business. The company represents a new breed of fintech that doesn't try to replace banks—it intelligently sits between customers and the banking system, extracting value through transparency and automation in an industry built on opacity.

Founded 2017

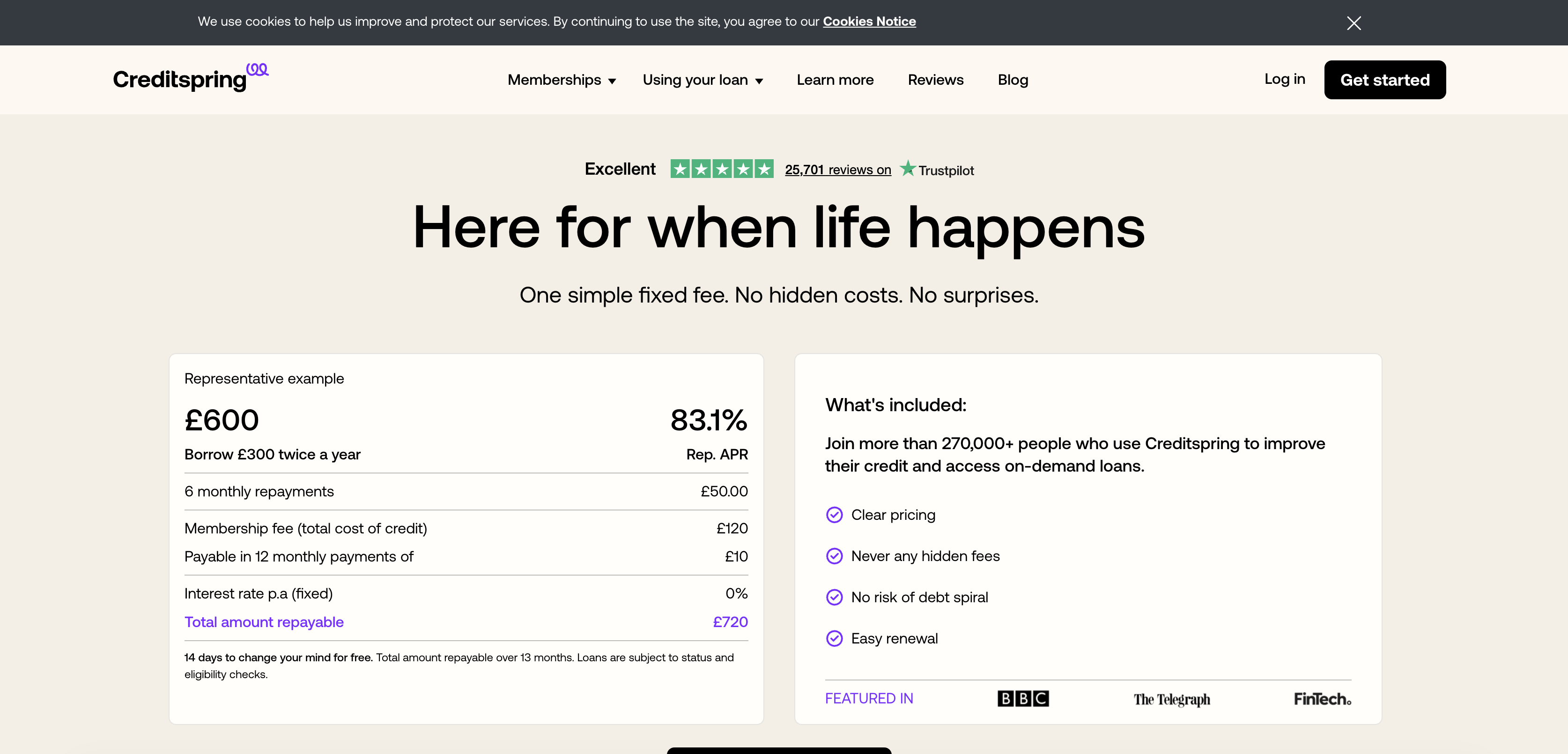

Credit Spring

Lending🇬🇧 United Kingdom

Credit Spring is a UK-based fintech that treats financial distress like a health problem—one that deserves diagnosis and treatment, not judgment. Rather than simply offering credit, the company combines short-term loans with financial coaching and debt management tools, recognizing that a quick cash injection without context is often a band-aid on a bigger problem. The platform helps borrowers understand their spending patterns and rebuild their financial foundation, not just patch a temporary shortfall. It's a provocative stance in a market crowded with BNPL and payday lenders that rarely ask why someone needs money in the first place. Credit Spring targets people in the credit-vulnerable segment—those with poor or limited credit histories who'd normally be shut out of mainstream lending. Instead of algorithmic rejection, the company uses alternative data and behavioral insights to assess creditworthiness beyond traditional scoring. For users, this means faster access to reasonable credit at transparent rates. For the market, it signals a shift toward lending that acknowledges financial fragility as a temporary state, not a permanent condition. The company represents a broader move within fintech to attach financial wellness services to credit products, treating lending as an entry point to deeper financial health rather than a transaction.

Founded 2016

Avanza

Wealth🇸🇪 Sweden

Avanza is Sweden's largest independent online brokerage, a no-frills investment platform that democratized stock trading for Swedish retail investors two decades ago. What started as a scrappy alternative to traditional banks has become the go-to app for millennials and Gen Z who want to trade, invest, and save without paying legacy banking fees. The platform strips away unnecessary complexity—no advisors, no jargon, just direct market access at transparent prices. Avanza operates in that interesting middle ground between a neobank and a pure trading platform. It offers savings accounts, pension accounts, and investment accounts with a sharp focus on user experience and low costs. The company has built a cultural following in Sweden, becoming almost synonymous with retail investing for a generation that views traditional brokers as relics. Beyond just equities and funds, Avanza has expanded into savings products, retirement planning, and financial education—positioning itself as a genuine financial companion rather than just a transaction layer. Its dominance in the Nordic market reflects a broader European shift toward direct-to-consumer investment platforms that compete on transparency, speed, and mobile-first design. Avanza exemplifies how fintech can win by doing one thing exceptionally well and then expanding thoughtfully into adjacent categories. The company's influence extends beyond Sweden into a broader shift in how younger Europeans think about investing: without gatekeepers, without unnecessary fees, and entirely on their own terms.

Founded 1999

Weefin

Lending🇫🇷 France

Weefin is a French fintech that helps consumers navigate the murky world of consumer credit with algorithmic precision. Rather than drowning users in confusing loan options, Weefin acts as a personal credit matchmaker, using data and AI to surface the most suitable financing products from a network of lenders. It's solving a genuine friction point: most people shopping for personal loans have no idea which option actually fits their circumstances, so they either overpay or get rejected. The company positions itself as a transparent intermediary in a market where traditional banks still treat credit like a black box. Weefin aggregates loan offers, compares terms, and guides users toward products that make financial sense for their specific situation rather than maximizing lender margins. It's the anti-payday-loan play—using technology to bring clarity to a category that thrives on confusion. The platform works with established financial institutions, making it a white-glove service for consumers who want intelligence, not just access. In a European fintech landscape crowded with neobanks and payment startups, Weefin occupies a narrower but genuinely useful niche: making consumer credit less of a gamble and more of an informed decision. It reflects a broader shift toward algorithmic transparency in lending, where the consumer's best interest and the platform's intelligence alignment create real value.

Founded 2018

Fincredible

Lending🇦🇹 Austria

Austria's fintech ecosystem is small relative to the major European markets but punches above its weight in specific segments — particularly in the area where consumer credit meets financial guidance for people whose financial situations don't fit neatly into traditional bank categories. Fincredible was founded in Vienna in 2017 to build a credit platform for Austrian consumers, with a focus on transparency and financial education alongside the actual lending product. Its platform offers personal loans with clear terms, applications processed digitally, and decisions made in minutes rather than days — a familiar fintech proposition applied to a market where Austrian consumers had limited alternatives to incumbent banks for unsecured personal credit. Fincredible has built its position in a market that is geographically concentrated — Vienna and the major Austrian cities account for the majority of digital financial product adoption — but has demonstrated that Austrian consumers respond to better products in ways that traditional banks have been slow to provide. In the DACH consumer credit landscape, where German and Austrian markets share many characteristics but operate under distinct regulatory regimes, Fincredible's Austrian focus reflects the importance of building credit products with genuine local depth rather than treating DACH as a single market.

Founded 2017

Monefit

Lending🇪🇪 Estonia

Consumer credit in Europe is in the middle of a slow renegotiation between flexibility and responsibility. Borrowers want access to credit without the formality of a personal loan application; lenders need underwriting models that work for revolving products without producing the kind of debt traps that have damaged the broader sector. Monefit was founded in Tallinn in 2020 as part of the Creditstar Group, building a digital revolving credit product for European consumers who want a flexible credit line they can draw on as needed rather than a fixed-term loan. Its model gives users access to credit up to a personalised limit, with interest charged only on the amount drawn, repayable on terms that flex with the borrower's circumstances. The Estonian base reflects both Creditstar Group's origins and the operational advantages of running a pan-European consumer credit business from a country whose digital infrastructure makes it possible. Monefit operates across multiple European markets, building a position in the segment of consumer credit that sits between traditional personal loans and credit card debt — a space that has been growing steadily as consumers become more comfortable with digital credit products and lenders find ways to underwrite them sustainably.

Founded 2020

Cleo

Personal Finance🇬🇧 United Kingdom

Cleo is a financial wellness app that meets you where you actually live: in your phone. Rather than another banking dashboard or budgeting spreadsheet, Cleo uses conversational AI to help you understand your money in real time, spot spending patterns you'd otherwise miss, and make better decisions without the friction of traditional finance apps.

The platform works as an intelligent money assistant embedded directly in your messaging apps—think of it as having a no-judgment financial coach in your pocket. It analyzes your transactions as they happen, flags unusual spending, alerts you to bills you might forget, and helps you save by automating small deposits when you have breathing room in your account. The experience feels less like finance and more like having a smart friend who actually knows your money.

Cleo operates in a crowded personal finance space, but its conversational, AI-first approach sets it apart from traditional budgeting apps that rely on charts and dashboards. Where most money apps treat finance as a problem to be solved with data visualization, Cleo treats it as a conversation. The company has built significant traction across Europe and North America by making financial management feel natural and accessible rather than intimidating.

In a fintech landscape increasingly built on APIs and automation, Cleo represents the human side of the equation—proving that sometimes the best financial tool is the one that feels less like a tool and more like advice from someone who gets it.

Founded 2015