← All services

24 European companies

card issuing APIs

Card issuing APIs allow non-bank companies to create and manage branded debit, credit, and prepaid card programmes for their customers or employees through a technical integration, without holding a banking licence. The issuing platform handles BIN sponsorship, card network connectivity, transaction processing, and compliance — the company controls the card product experience and branding.

Typically offered by

European fintech companies offering card issuing APIs

Mollie

Financial Infrastructure🇳🇱 Netherlands

Adriaan Mol built Mollie's first backend while living with his parents in the Netherlands in 2004. No investors, no office, no team — just a founder and an idea that small businesses deserved a payment integration that didn't require a team of lawyers and a six-month setup process. He bootstrapped it for over fifteen years before taking outside funding in 2019. By then, Mollie had already grown into one of the most important payment platforms in European e-commerce, entirely on the back of a product that developers actually liked using.

The proposition is straightforward: one API, one dashboard, and access to the payment methods that actually matter across Europe. That means iDEAL in the Netherlands, Bancontact in Belgium, Klarna and SEPA Direct Debit everywhere, alongside cards, Apple Pay, and a growing list of local methods that would otherwise require separate integrations and separate acquirer relationships. Mollie handles the compliance, the fraud monitoring, and the settlement complexity. Merchants get a clean interface and a single invoice.

For the 250,000 businesses using Mollie today — ranging from Gymshark and Wild to local bakeries and market stalls, as CEO Koen Köppen regularly points out — the appeal is less about feature lists and more about what they don't have to think about. European payments are fragmented by design. Every country has its preferred methods, its own regulatory quirks, its own consumer habits. Mollie's job is to make that invisible.

The numbers from 2024 reflect a company that has found its model. Revenue reached €214 million, up 28% year on year, with gross profit growing 30% to €115 million and the company returning to positive EBITDA for the first time since 2018. Mollie raised a total of $940 million in funding and was valued at $6.5 billion following its 2021 Series C led by Blackstone.

The most significant recent development is the acquisition of GoCardless in December 2025 — bringing the UK-based direct debit specialist into the Mollie group and substantially expanding its recurring payments and bank transfer capabilities across Europe. Combined, the two companies cover a considerable share of European e-commerce payment infrastructure.

Mollie is still headquartered in Amsterdam, with around 900 employees across offices in Ghent, London, Lisbon, Munich, Milan, Paris, and beyond.

Founded 2004

Solaris

Financial Infrastructure🇩🇪 Germany

Solaris is a Berlin-based fintech infrastructure platform that lets financial institutions and fintechs launch their own digital banking products without building tech from scratch. Rather than wrestling with legacy core banking systems, clients plug into Solaris's cloud-native API layer to issue cards, manage accounts, and process payments at speed.

The company operates in the shadows of most consumer apps—you won't see the Solaris logo in an app store—but its backbone runs through dozens of European fintechs, neobanks, and traditional financial institutions. Think of it as the plumbing that powers other people's banking ambitions.

Solaris dominates a specific niche: the BaaS (Banking-as-a-Service) and embedded finance layer for Europe. While competitors like Thought Machine and Temenos chase enterprise banking overhauls, Solaris stays focused on the modern fintech workflow. Its modular design appeals to companies that need speed and flexibility, not a 10-year implementation project.

In a market crowded with infrastructure plays, Solaris has become essential plumbing for European digital banking. It sits at the intersection of regulatory compliance, technical simplicity, and startup ambition—precisely where the next wave of European fintech is being built.

Founded 2015

Paynetics

Embedded Finance🇧🇬 Bulgaria

Paynetics operates at the intersection of payment infrastructure and embedded finance, building the plumbing that lets fintechs and traditional companies accept, process, and manage payments without wrestling with legacy banking systems. The Bulgarian-founded company has positioned itself as a critical middleware layer—connecting merchants, fintech platforms, and financial institutions through a unified API. Rather than forcing clients into proprietary ecosystems, Paynetics emphasizes flexibility and interoperability, allowing partners to plug into multiple acquiring networks, payment gateways, and settlement rails from a single integration point. This approach has resonated particularly with regional players across Europe seeking alternatives to Western-dominated payment processors.

The company's strength lies not in flashy consumer-facing products but in unglamorous, essential infrastructure: payment orchestration that routes transactions intelligently, card issuing APIs that power embedded finance plays, and acquiring services that work across markets where local nuance matters. For fintech founders building in Central and Eastern Europe or scaling across fragmented European payment corridors, Paynetics removes the friction of navigating dozens of local processors and compliance regimes. Its expansion into treasury and FX services suggests ambitions beyond pure payments—positioning itself as a platform for companies managing cross-border complexity. In an industry dominated by American giants and large European incumbents, Paynetics represents a rare example of a challenger emerging from the region's underestimated fintech ecosystem, proving that critical infrastructure doesn't always require Silicon Valley pedigree.

Founded 2013

Tieto

Financial Infrastructure🇫🇮 Finland

Tieto operates in the murky middle ground between traditional IT services and fintech infrastructure, building the unsexy-but-essential systems that European financial institutions actually run on. The company provides core banking platforms, payment systems, and digital banking solutions to banks and financial services firms across the Nordic and European markets. Where most fintech captures headlines with consumer apps, Tieto stays disciplined in the B2B infrastructure game—modernizing legacy systems, managing complex regulatory requirements, and keeping payments flowing. Its positioning reflects a particular Nordic pragmatism: less about disruption, more about making banking systems reliable, scalable, and compliant. In a landscape crowded with flashy consumer fintechs, Tieto represents the unglamorous but critical plumbing layer that enables everyone else to operate. The company remains one of Europe's largest fintech infrastructure players, though its parent company structure and steady-handed approach means it rarely commands the venture attention of younger competitors.

Founded 1969

Pay.nl

Financial Infrastructure🇳🇱 Netherlands

Pay.nl is a Dutch payment processor built for the complexity of modern commerce. Rather than forcing merchants into a one-size-fits-all payment flow, it offers a modular approach where acquirers, payment methods, and risk tools snap together like building blocks. This flexibility appeals to mid-market retailers and platform operators who've outgrown off-the-shelf solutions but don't have the resources to build from scratch.

The company positions itself as the pragmatic middle ground in European payments. While fintechs chase consumer flashiness and traditional PSPs move at legacy speed, Pay.nl focuses on the unglamorous reality of merchant operations: payment routing, multi-currency settlement, real-time reconciliation, and developer experience. Its API-first architecture means integrations take weeks instead of quarters.

Pay.nl operates across the full payment stack—card acquiring, alternative payment methods, tokenization, subscription billing—but treats them as components rather than marketing bullets. This modular thinking extends to risk management and compliance, which the company bundles without overhead.

Within Europe's crowded payments landscape, Pay.nl competes less on consumer reach and more on merchant control. It's the choice for companies that care about payment economics and operational efficiency rather than brand building. Its role in the broader ecosystem is to mature the middle market, proving that European merchants don't need either a tech giant's infrastructure or a startup's rough edges.

Founded 2007

Zwipe

Financial Infrastructure🇳🇴 Norway

Zwipe is building the infrastructure for secure, contactless payments at the physical point of sale. The company makes biometric card technology—specifically fingerprint-activated payment cards—that eliminate the need for PINs and signatures while dramatically reducing fraud. Instead of fumbling for passwords or worrying about shoulder surfers, you just tap and touch.What makes Zwipe different is its focus on the hardware layer. While most fintech companies live in apps and APIs, Zwipe sits at the intersection of physical cards and digital security, creating a tangible product that banks and card issuers can actually deploy. The biometric verification happens on the card itself, not on a terminal or in the cloud, which means faster transactions and genuine privacy—your fingerprint never leaves the card.The company operates in a narrow but critical space: the next generation of payment cards. As contactless payments have become mainstream, Zwipe sees the obvious next step: making those cards smarter and more secure. European banks and payment networks are watching closely, particularly as regulators tighten authentication standards. Zwipe's technology addresses a real pain point in the payment infrastructure stack, positioning it as a key player in the hardware innovation side of fintech.

Founded 2014

Wallester

Embedded Finance🇪🇪 Estonia

Wallester is a European fintech infrastructure company that makes it simple for other businesses to issue, manage, and distribute payment cards at scale. Rather than wrestling with legacy banking systems and complex integrations, companies use Wallester's APIs and platforms to embed card programs directly into their own products—think neobanks, fintechs, and platforms that need white-label card solutions without the operational overhead. The company handles the technical plumbing: card issuance, real-time transaction processing, compliance, and customer-facing controls, all delivered through clean, developer-friendly APIs. Wallester operates across multiple European markets and works with everyone from emerging challenger banks to established financial institutions looking to modernize their card infrastructure. What sets Wallester apart is its focus on removing friction from the card-issuing process. Most issuers are bound to cumbersome core banking relationships or have to build entirely custom solutions. Wallester sits in the middle, offering a turnkey platform that scales with demand without forcing companies to reinvent core banking. It's become a quiet backbone for European fintechs that need cards fast, reliably, and without the bureaucracy. The company represents a broader trend in fintech infrastructure: the unbundling of banking services into modular, API-first components that let smaller players compete with traditional incumbents.

Founded 2019

Netcetera

Financial Infrastructure🇨🇭 Switzerland

Netcetera is a Swiss-based financial software company that builds infrastructure for digital payments and banking. Rather than chasing flashy consumer apps, they focus on the unsexy but essential work of connecting banks, payment networks, and merchants through APIs and platforms that handle the plumbing beneath every transaction. Their reach spans card payments, mobile banking, and open banking rails—serving a global roster of financial institutions that need rock-solid, scalable technology rather than venture-backed disruption narratives. In markets where regulatory complexity and legacy system integration matter more than speed-to-market, Netcetera has quietly become indispensable. They approach fintech as a B2B engineering problem, not a consumer trend, which is exactly why you've never heard of them despite their work touching millions of transactions daily. The company represents a particular strain of European fintech: deeply technical, institution-friendly, and skeptical of hype. They're the kind of partner that traditional banks and payment processors turn to when they need to modernize without tearing everything down. In an ecosystem crowded with neobanks and consumer lending apps, Netcetera's unglamorous expertise in payment orchestration, card processing, and banking APIs underscores a fundamental truth about fintech infrastructure: the real value often hides behind the scenes, in systems nobody sees but everyone depends on.

Founded 1996

RS2

Financial Infrastructure🇲🇹 Malta

RS2 sits at the infrastructure layer of European fintech, operating as a silent but essential backbone for digital banking. The company builds payment and banking systems that power everything from challenger banks to traditional financial institutions, handling the plumbing that most customers never see but every modern bank needs. Rather than competing for end-user attention, RS2 focuses on solving the unglamorous but critical problem: how do you move money, verify identities, and manage accounts at scale across multiple countries and currencies. Their platform approach means banks and fintechs can launch new services faster without rebuilding core systems from scratch. In a landscape crowded with consumer-facing apps and robo-advisors, RS2 represents the infrastructure play—the company that enables others to be innovative. They've built particular strength in payments orchestration and acquiring, areas where fragmentation across European markets creates real complexity. The company's positioning is fundamentally B2B, serving financial institutions that need to modernize their tech stacks rather than competing directly for customer wallets. For European fintech, RS2 is part of the connective tissue that allows the entire ecosystem to function more efficiently and move faster.

Founded 2005

myPOS

Financial Infrastructure🇧🇬 Bulgaria

myPOS is a fintech company that sits at the intersection of payments and merchant services, focused on modernizing how small businesses and entrepreneurs handle transactions across Europe. Rather than forcing merchants into legacy payment processing workflows, myPOS bundles hardware, software, and financial services into a seamless ecosystem that feels native to how modern retailers actually operate. The platform combines point-of-sale systems, payment processing, and merchant acquiring into a single integrated offering, with particular strength in high-risk verticals where traditional acquirers have historically been hesitant. What sets myPOS apart in the European market is its commitment to serving the long tail of merchants—from food vendors and boutiques to service providers—without the bureaucratic friction that characterizes incumbent payment processors. The company has built its infrastructure to support cross-border operations across multiple European markets while maintaining competitive pricing that doesn't penalize small transaction volumes. In the broader fintech landscape, myPOS exemplifies the shift toward vertical integration in payments, where success increasingly depends on controlling the full merchant experience rather than being relegated to a single layer of the payment stack.

Founded 2012

Viva

Financial Infrastructure🇬🇷 Greece

Viva is a Greek payment infrastructure company that's quietly rewriting how businesses handle transactions across Europe. Rather than forcing merchants into proprietary ecosystems, Viva acts as the connective tissue between retailers and the complex world of payment rails, offering a unified platform that simplifies what was once fragmented and painful. The company processes billions in transaction volume annually, operating across multiple countries with a particular stronghold in Southern and Central Europe where it's become the go-to backbone for everything from small cafes to large retail chains.

What sets Viva apart is its pragmatic approach to the payments problem. While competitors obsess over consumer-facing design or venture-scale ambitions, Viva has built a deeply integrated merchant platform that handles card acquiring, billing, reporting, and reconciliation in one place. It's the kind of infrastructure that doesn't make headlines but makes operators' lives measurably easier. The company operates with a B2B lens, working directly with acquiring banks and payment processors rather than trying to disrupt them, which has allowed it to expand methodically across Europe without the cultural friction that doomed earlier fintech challengers.

In the broader European fintech landscape, Viva represents a different breed of company—one focused on solving unglamorous, permanent problems at scale rather than chasing consumer trends or speculative technologies. It's the connective infrastructure that enables other fintechs to exist, a role that's proven far more defensible and profitable than most initially assumed.

Founded 2013

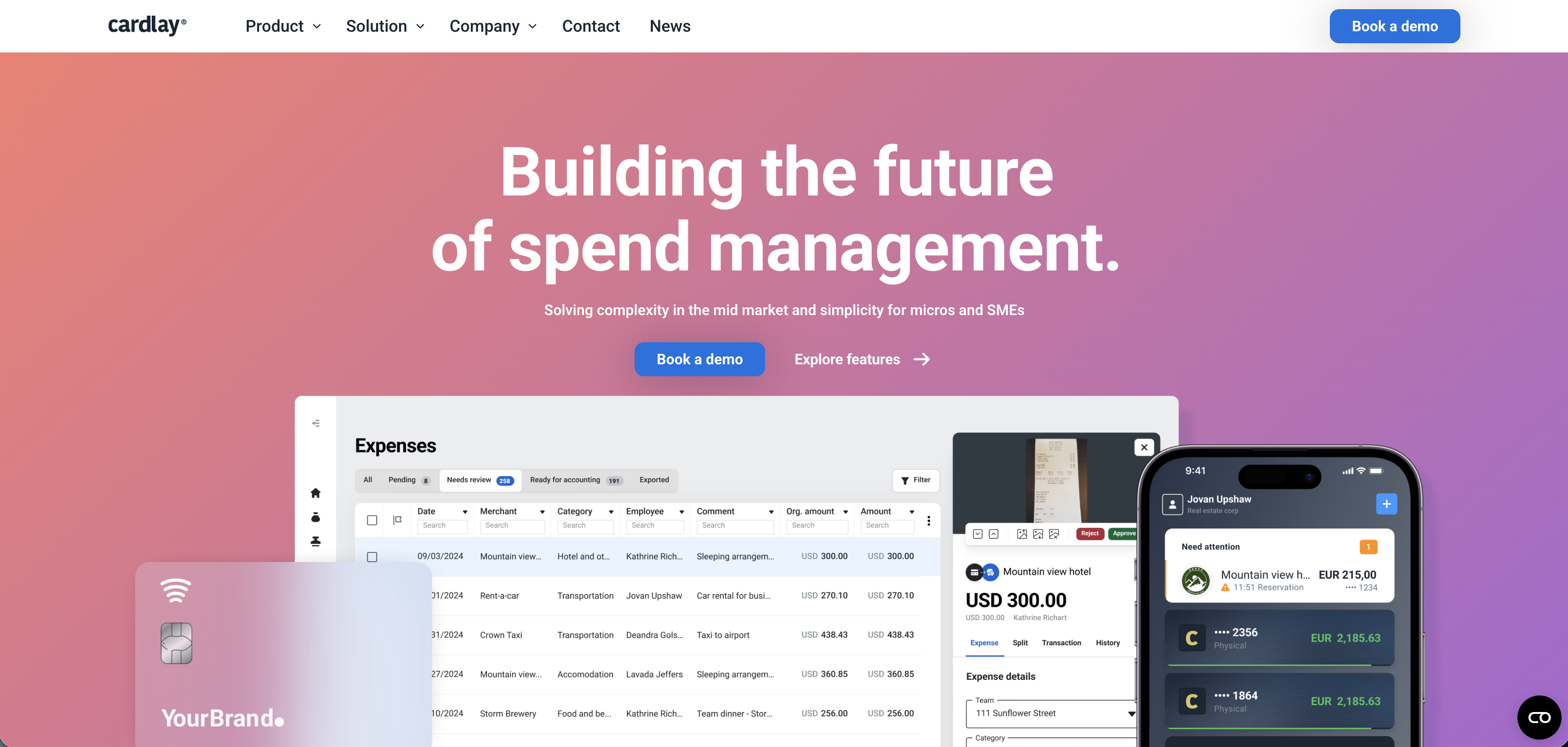

Cardlay

Embedded Finance🇩🇪 Germany

Cardlay sits at the intersection of embedded finance and modern merchant infrastructure, making it possible for platforms and marketplaces to offer payment solutions directly to their users without needing a banking license. The Berlin-based company essentially acts as a bridge, enabling marketplaces to issue virtual and physical cards, manage spending, and embed payment functionality into their platforms as seamlessly as adding another feature.

What sets Cardlay apart is its focus on the embedded card market—a category that's exploded as platforms realize they can monetize payment flows while improving user experience. Rather than directing users to third-party payment providers, Cardlay lets platforms own the entire card experience, from issuance to transaction controls to spend analytics.

The company operates in a space where B2B2C models dominate, meaning its real clients are platforms that want to offer banking-grade payment products without the regulatory headache. This positions Cardlay somewhere between a traditional fintech infrastructure player and a modern card issuer. In a European market increasingly crowded with card-issuing platforms, Cardlay distinguishes itself through developer-friendly APIs and a focus on use cases that larger players haven't yet dominated—from gig economy platforms to niche marketplaces.

Cardlay represents the shift toward distributed financial infrastructure, where payment capability becomes just another feature any well-funded platform can activate. It's emblematic of how European fintech has matured from consumer-focused apps to deeper, quieter plays that reshape how commerce and finance intersect.

Founded 2021

Showing 12 of 24 companies. View all in the directory →