← All services

20 European companies

consumer credit apps

Consumer credit apps provide individuals with personal credit products — credit lines, personal loans, or instalment plans — through mobile-first interfaces outside traditional bank relationships. Digital consumer credit apps offer pre-approved limits, faster decisions, clearer terms, and better user experiences than traditional credit cards, often using open banking transaction data for more accurate underwriting.

Typically offered by

European fintech companies offering consumer credit apps

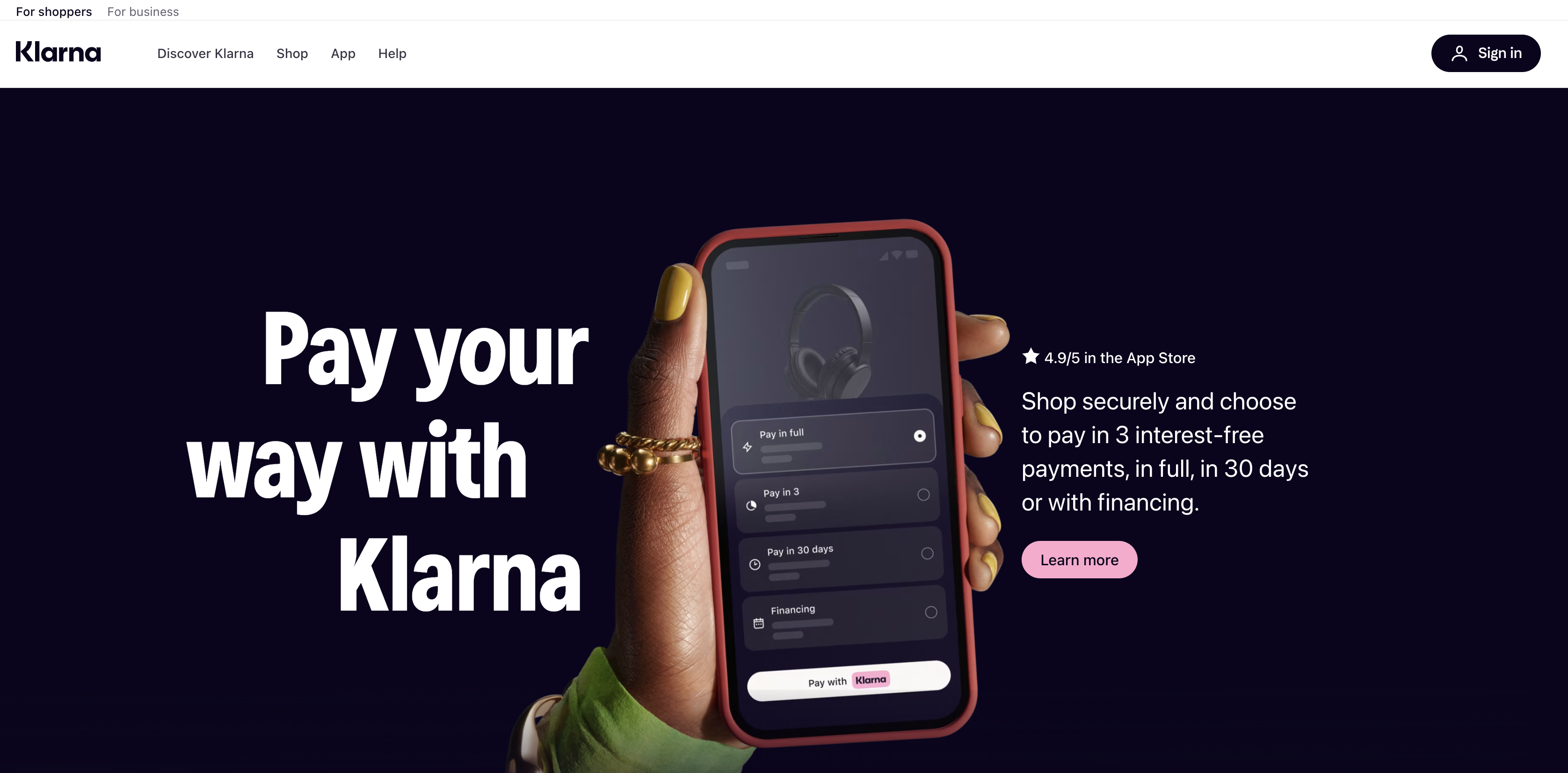

Klarna

Embedded Finance🇸🇪 Sweden

Three Stockholm School of Economics students pitched an idea at a university entrepreneurship competition in 2005: let shoppers receive goods before they pay, and put the credit risk on the merchant side. The pitch finished last. They built it anyway.

Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson launched what was originally called Kreditor, later renamed Klarna, and spent the next two decades turning that rejected idea into one of Europe's most recognised fintech brands. The core insight held up: millions of people would rather split a purchase into three instalments than reach for a credit card, and merchants would pay for the privilege of offering that option because it reduces cart abandonment and increases average order values.

Klarna grew from a Swedish checkout button into something considerably more complex. It now holds a banking licence in Sweden, offers savings accounts, issues its own card, and operates across more than 45 markets with around 93 million active consumers and 675,000 merchant partners at the end of 2024. The US, which Klarna entered in 2015, has become its largest market by revenue, a fact the company underlined by listing on the New York Stock Exchange in September 2025 under the ticker KLAR, raising $1.37 billion at IPO.

The financial trajectory has been bumpy. Klarna reported net income of $21 million in 2024, a return to profitability after a bruising 2022 that included an 85% valuation cut and significant layoffs that reduced headcount from over 7,000 to around 3,400. What survived the restructuring was a leaner company with $2.81 billion in revenue and a clearer strategic direction: AI. Klarna's partnership with OpenAI produced a customer service assistant it claims handles the equivalent of 700 full-time agents, and generative AI now manages roughly two-thirds of customer chats.

The honest assessment of where Klarna sits today: it's no longer purely a BNPL provider and it's not quite a bank. It's somewhere in between, a consumer finance platform that knows more about your shopping behaviour than your bank does, and is betting that's worth a lot.

Founded 2005

Inbank

Digital Banking🇪🇪 Estonia

Specialised banking for consumer credit — focused on lending products distributed through merchant partnerships rather than building general-purpose retail banking — is a model with deeper European roots than the venture-backed BNPL conversation suggests. Inbank was founded in Tallinn in 2011 as a specialist lender focused on point-of-sale consumer credit, partnering with retailers across Estonia and the broader Baltic and Central European region to offer instalment finance at the moment of purchase. The company received a full Estonian banking licence and has built operations across Estonia, Latvia, Lithuania, Poland, and the Czech Republic, expanding from a domestic specialist into a Pan-European consumer finance bank. Inbank is publicly listed on the Nasdaq Tallinn exchange — one of the few publicly traded Baltic fintechs — giving it both the regulatory standing of a licensed bank and the funding access of a public company. Its product range covers point-of-sale finance, BNPL, and consumer deposit products, with merchant partnerships across automotive, electronics, home improvement, and other categories where consumers commonly finance purchases. In the European specialist consumer banking landscape, Inbank represents one of the more successful examples of a focused operator scaling across borders while maintaining the operational discipline of a regulated bank.

Founded 2011

NeoFinance

Lending🇱🇹 Lithuania

Lithuanian peer-to-peer lending built one of the more substantial European markets for marketplace consumer credit, with multiple platforms competing for both borrowers and investors in a country that has cultivated a regulatory environment supportive of fintech experimentation. NeoFinance was founded in Vilnius in 2014 as one of those Lithuanian P2P pioneers, connecting Lithuanian and international investors with creditworthy local borrowers seeking personal loans. The platform's domestic focus gave it credit data depth in the Lithuanian market that pan-European platforms didn't match, while its EU passport allowed it to attract investor capital from across Europe. NeoFinance has expanded its operations and product range while navigating the maturation of European P2P lending — including the regulatory tightening that brought retail crowdfunding under the European Crowdfunding Service Provider Regulation framework. In the Lithuanian P2P landscape, NeoFinance represents one of the longer-running platforms operating with a domestic borrower focus and a Pan-European investor base — a combination that has proven more sustainable than purely cross-border models that lacked deep credit knowledge of any single market.

Founded 2014

4finance

Lending🇱🇻 Latvia

Consumer credit at scale across emerging European markets has been one of the more controversial and one of the larger businesses in European fintech. 4finance was founded in Riga in 2008 and grew into one of the largest digital consumer lenders in Europe, operating in over a dozen markets including Latvia, Lithuania, Poland, Spain, Czech Republic, Slovakia, Romania, Bulgaria, Denmark, Sweden, and beyond. Its product range includes short-term loans, instalment loans, and credit lines, distributed entirely through digital channels. The company's scale — billions in loans originated, millions of customers served — has made it both a significant financial institution and a frequent subject of regulatory and consumer protection scrutiny. The business has navigated the tightening regulation of consumer credit across multiple European jurisdictions, repositioning its product range and pricing as different markets have implemented caps on short-term lending costs. 4finance is owned by funds and operates with the operational scale of a substantial bank without holding traditional banking licences in most of its markets. In the broader European consumer fintech landscape, 4finance represents a category that exists outside the venture-backed startup conversation but processes meaningful credit volume across markets where formal banking remains less accessible than digital alternatives.

Founded 2008

Ferratum

Digital Banking🇫🇮 Finland

Mobile-first consumer lending was a genuinely novel concept in 2005, the year that Ferratum was founded in Helsinki. The company built one of Europe's earliest digital consumer credit businesses, offering small short-term loans through SMS and later through mobile apps — long before smartphone banking became universal. Its initial product targeted the gap between bank credit and informal lending, providing small loans quickly to consumers who needed flexibility that banks didn't offer. Ferratum expanded across more than 20 markets, received a Maltese banking licence, and rebranded to Multitude as it broadened from short-term consumer lending into a more diversified consumer banking business including a digital mobile bank. The transition from short-term lender to licensed bank reflects the broader maturation of European consumer fintech — companies that started with specific lending products evolving toward fuller-service banks as their licences and customer relationships justified the broader product range. Multitude is publicly listed on the Frankfurt Stock Exchange, making it one of the few publicly traded pan-European consumer fintechs. In the European consumer credit landscape, the company's two-decade trajectory illustrates both the original opportunity in mobile-first lending and the strategic logic of evolving toward a licensed banking model as the regulatory environment for short-term credit has tightened.

Founded 2005

Northmill

Embedded Finance🇸🇪 Sweden

Northmill is a Stockholm-based fintech that's spent the last decade building out the infrastructure for buy now, pay later and consumer credit across Europe. Rather than chase the hype cycle of BNPL as a consumer-facing product, Northmill positioned itself as the boring-but-essential backbone: lending technology, credit decisioning, and liquidity management for everyone from ambitious fintechs to established retailers who need payment flexibility options. The company operates across the Nordic region and Central Europe, managing the unglamorous work of underwriting, fraud prevention, and capital sourcing that makes the flashy checkout experience possible. What sets Northmill apart in a crowded market is its refusal to be just another point solution. Instead, it's built a modular platform where merchants, fintechs, and banks can plug in lending capabilities without reinventing the wheel. This appeals to pragmatic businesses that want BNPL functionality without the startup risk. The company has grown quietly while competitors burned through cash chasing consumer acquisition. Northmill represents a shift in how European fintech is maturing: less consumer brand, more B2B infrastructure play. It's the kind of company that powers transactions everyone sees but few people know exists, which is precisely where the sustainable economics lie.

Founded 2010

ESTO

Lending🇪🇪 Estonia

Estonian consumer credit at the point of online purchase has been transformed by the combination of digital infrastructure that lets credit decisions happen in real time and consumer expectations of completing purchases without leaving the merchant checkout. ESTO was founded in Tallinn in 2016 to serve that specific moment — providing buy now pay later and instalment financing options integrated into Estonian and Baltic merchant checkouts. The platform connects merchants with consumers seeking flexible payment options at purchase, handling underwriting, settlement, and ongoing customer relationship management for the credit products it originates. ESTO has expanded across the Baltic markets and into broader Central European territories, building a position in the BNPL category as one of the regional specialists that competes alongside the larger European platforms by virtue of its local market depth. In the Baltic BNPL landscape, where international platforms have made selective entries but have generally not built the merchant integration depth that domestic operators have, ESTO represents the local champion category. The competitive question for that category is whether local depth in a single regional market can sustain a competitive position as international BNPL platforms continue to expand and as the underlying economics of the category continue to evolve through cycles of growth and regulatory tightening.

Founded 2016

Kreditech

Lending🇩🇪 Germany

Algorithmic underwriting for consumer credit using non-traditional data was one of the most ambitious bets in European fintech a decade ago. Kreditech was founded in Hamburg in 2012 with the thesis that machine learning models trained on thousands of data points — far beyond traditional credit scoring inputs — could underwrite consumers in markets where conventional credit bureau coverage was thin. The company expanded across emerging markets, particularly in Latin America, Eastern Europe, and Asia, lending to consumers who were credit-invisible to traditional underwriters. The technology was genuinely advanced for its time, the addressable market was enormous, and the funding it attracted reflected the ambition — over $300 million across multiple rounds, including investments from PayU and other major institutional backers. The execution proved harder than the technology. Operating in multiple emerging markets simultaneously, navigating diverse regulatory regimes, and managing the credit performance of underbanked borrower populations created complexity that challenged the company's ability to scale profitably. Kreditech rebranded to Monedo and entered insolvency proceedings in 2020. Its story is one of the more instructive in European fintech — a technology-led approach to a real market opportunity that ultimately demonstrated the gap between algorithmic possibility and operational sustainability in consumer lending across emerging markets.

Founded 2012

Credissimo

Lending🇧🇬 Bulgaria

Bulgaria's consumer credit market evolved through a different trajectory than Western European countries, with the digital alternatives developing alongside rather than after the traditional banking sector. Credissimo was founded in Sofia in 2007 as one of the country's first digital consumer lenders, providing short-term and instalment loans through online channels at a time when most Bulgarian consumers were still receiving credit through bank branches and informal networks. The company has expanded across multiple European markets and built a substantial digital lending operation, with technology infrastructure that supports underwriting, servicing, and customer management across borders. Credissimo operates in a regulatory environment that has tightened significantly over the past decade — the Bulgarian and EU consumer credit frameworks have evolved to set clearer standards for short-term lending, and operators that survived the regulatory consolidation are those that adapted their products to the new requirements. In the broader European consumer credit landscape, Credissimo represents the kind of operator that has been quietly building scale across Central and Eastern European markets while the venture-backed fintechs of Western Europe have captured the headlines — a different model with different economics, but one that has demonstrated genuine durability across nearly two decades of operation.

Founded 2007

Fincredible

Lending🇦🇹 Austria

Austria's fintech ecosystem is small relative to the major European markets but punches above its weight in specific segments — particularly in the area where consumer credit meets financial guidance for people whose financial situations don't fit neatly into traditional bank categories. Fincredible was founded in Vienna in 2017 to build a credit platform for Austrian consumers, with a focus on transparency and financial education alongside the actual lending product. Its platform offers personal loans with clear terms, applications processed digitally, and decisions made in minutes rather than days — a familiar fintech proposition applied to a market where Austrian consumers had limited alternatives to incumbent banks for unsecured personal credit. Fincredible has built its position in a market that is geographically concentrated — Vienna and the major Austrian cities account for the majority of digital financial product adoption — but has demonstrated that Austrian consumers respond to better products in ways that traditional banks have been slow to provide. In the DACH consumer credit landscape, where German and Austrian markets share many characteristics but operate under distinct regulatory regimes, Fincredible's Austrian focus reflects the importance of building credit products with genuine local depth rather than treating DACH as a single market.

Founded 2017

Monefit

Lending🇪🇪 Estonia

Consumer credit in Europe is in the middle of a slow renegotiation between flexibility and responsibility. Borrowers want access to credit without the formality of a personal loan application; lenders need underwriting models that work for revolving products without producing the kind of debt traps that have damaged the broader sector. Monefit was founded in Tallinn in 2020 as part of the Creditstar Group, building a digital revolving credit product for European consumers who want a flexible credit line they can draw on as needed rather than a fixed-term loan. Its model gives users access to credit up to a personalised limit, with interest charged only on the amount drawn, repayable on terms that flex with the borrower's circumstances. The Estonian base reflects both Creditstar Group's origins and the operational advantages of running a pan-European consumer credit business from a country whose digital infrastructure makes it possible. Monefit operates across multiple European markets, building a position in the segment of consumer credit that sits between traditional personal loans and credit card debt — a space that has been growing steadily as consumers become more comfortable with digital credit products and lenders find ways to underwrite them sustainably.

Founded 2020

Lendico

Lending🇩🇪 Germany

Marketplace lending in Germany was supposed to disrupt the conservative German banking system by connecting borrowers directly to investors at better rates than the banks offered. Lendico was founded in Berlin in 2013 by Rocket Internet to do exactly that, launching as a peer-to-peer lending platform offering personal and business loans across multiple European markets. The company expanded aggressively in its early years, operating in Germany, Austria, Spain, Poland, the Netherlands, and South Africa, with the kind of scale-first ambition that defined Rocket Internet's portfolio approach. The marketplace lending thesis proved harder than the platform builders anticipated. Lendico repositioned its business model multiple times, eventually being acquired by ING in 2018 — turning a P2P platform into a digital SME lending arm of one of Europe's largest banks. The acquisition reflects a pattern that has played out repeatedly in European P2P lending: the platforms that proved the demand for alternative credit ultimately become acquired by the incumbents whose customers they were originally trying to win over. Lendico's trajectory from independent marketplace to bank-owned lending platform is one of the most explicit examples of that pattern in DACH fintech.

Founded 2013

Showing 12 of 20 companies. View all in the directory →