← All services

11 European companies

merchant BNPL

Merchant BNPL provides businesses with the integration tools and credit infrastructure to offer instalment payment options to their customers at checkout. The merchant proposition is primarily commercial: BNPL integration increases conversion rates, reduces cart abandonment, and increases average order values. Merchants pay a percentage fee to the BNPL provider and receive full payment upfront, with the provider assuming credit risk.

Typically offered by

European fintech companies offering merchant BNPL

Klarna

Embedded Finance🇸🇪 Sweden

Three Stockholm School of Economics students pitched an idea at a university entrepreneurship competition in 2005: let shoppers receive goods before they pay, and put the credit risk on the merchant side. The pitch finished last. They built it anyway.

Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson launched what was originally called Kreditor, later renamed Klarna, and spent the next two decades turning that rejected idea into one of Europe's most recognised fintech brands. The core insight held up: millions of people would rather split a purchase into three instalments than reach for a credit card, and merchants would pay for the privilege of offering that option because it reduces cart abandonment and increases average order values.

Klarna grew from a Swedish checkout button into something considerably more complex. It now holds a banking licence in Sweden, offers savings accounts, issues its own card, and operates across more than 45 markets with around 93 million active consumers and 675,000 merchant partners at the end of 2024. The US, which Klarna entered in 2015, has become its largest market by revenue, a fact the company underlined by listing on the New York Stock Exchange in September 2025 under the ticker KLAR, raising $1.37 billion at IPO.

The financial trajectory has been bumpy. Klarna reported net income of $21 million in 2024, a return to profitability after a bruising 2022 that included an 85% valuation cut and significant layoffs that reduced headcount from over 7,000 to around 3,400. What survived the restructuring was a leaner company with $2.81 billion in revenue and a clearer strategic direction: AI. Klarna's partnership with OpenAI produced a customer service assistant it claims handles the equivalent of 700 full-time agents, and generative AI now manages roughly two-thirds of customer chats.

The honest assessment of where Klarna sits today: it's no longer purely a BNPL provider and it's not quite a bank. It's somewhere in between, a consumer finance platform that knows more about your shopping behaviour than your bank does, and is betting that's worth a lot.

Founded 2005

Scalapay

Embedded Finance🇮🇹 Italy

Scalapay is a BNPL (buy now, pay later) platform built for the European e-commerce market, offering shoppers the ability to split purchases into interest-free instalments at checkout. Rather than simply bolting financing onto existing payment flows, Scalapay positions itself as a full-stack infrastructure play—handling underwriting, risk management, and merchant integration from a single API. The company targets mid-market and enterprise retailers across fashion, electronics, and beauty verticals, regions where instalment purchasing is becoming table stakes for conversion.

What sets Scalapay apart is its focus on merchant flexibility and real-time decision-making. While competitors often impose rigid lending terms or lengthy approval processes, Scalapay emphasizes transparent pricing and instant qualification, allowing merchants to offer financing without friction or hidden costs. The platform integrates seamlessly into checkout experiences—both web and mobile—and provides merchants with detailed analytics on customer behaviour and financing uptake.

Scalapay operates in a crowded BNPL landscape, but differentiates through its emphasis on profitability and sustainable lending rather than growth-at-any-cost customer acquisition. The company has expanded across multiple European markets, particularly in Southern Europe and the Mediterranean, where instalment culture is deeply embedded. Its positioning sits between pure-play consumer lenders and white-label infrastructure providers, serving merchants who want financing capabilities without building their own credit infrastructure.

In the broader fintech ecosystem, Scalapay exemplifies the maturation of embedded finance—moving beyond the novelty of BNPL into building durable, profitable lending platforms that merchants and consumers both trust.

Founded 2019

Credimi

Embedded Finance🇮🇹 Italy

Credimi sits at the intersection of e-commerce and embedded finance, solving a problem that online retailers have largely ignored: making checkout friction disappear. Rather than forcing customers to choose between card payments and bank transfers, Credimi lets shoppers access buy-now-pay-later directly at the point of sale, turning the checkout moment into a financing decision rather than a payment one. The company essentially white-labels installment lending for merchants, handling everything from credit decisioning to collections behind the scenes.

What sets Credimi apart in a crowded BNPL market is its focus on the merchant relationship rather than the consumer one. While competitors chase customer loyalty through branded apps and direct marketing, Credimi takes a B2B approach, embedding its credit engine into partner payment flows and e-commerce platforms. This means retailers get better conversion rates without bearing the customer acquisition cost. The company operates across multiple European markets, particularly strong in the Nordics and DACH region, where fintech-native commerce has matured fastest.

In an industry obsessed with speed and simplicity, Credimi's real edge is its underwriting—it deploys machine learning to make instant credit decisions without the awkward friction of traditional lending. This isn't flashy consumer fintech; it's infrastructure. But it's exactly what online retailers need to compete in markets where BNPL has become table stakes.

Founded 2016

Northmill

Embedded Finance🇸🇪 Sweden

Northmill is a Stockholm-based fintech that's spent the last decade building out the infrastructure for buy now, pay later and consumer credit across Europe. Rather than chase the hype cycle of BNPL as a consumer-facing product, Northmill positioned itself as the boring-but-essential backbone: lending technology, credit decisioning, and liquidity management for everyone from ambitious fintechs to established retailers who need payment flexibility options. The company operates across the Nordic region and Central Europe, managing the unglamorous work of underwriting, fraud prevention, and capital sourcing that makes the flashy checkout experience possible. What sets Northmill apart in a crowded market is its refusal to be just another point solution. Instead, it's built a modular platform where merchants, fintechs, and banks can plug in lending capabilities without reinventing the wheel. This appeals to pragmatic businesses that want BNPL functionality without the startup risk. The company has grown quietly while competitors burned through cash chasing consumer acquisition. Northmill represents a shift in how European fintech is maturing: less consumer brand, more B2B infrastructure play. It's the kind of company that powers transactions everyone sees but few people know exists, which is precisely where the sustainable economics lie.

Founded 2010

Zaver

Embedded Finance🇸🇪 Sweden

Zaver is a buy-now-pay-later platform built for the European e-commerce and retail landscape, letting shoppers split purchases into manageable payments without the friction of traditional credit checks. The company positions itself as the checkout financing solution for merchants who want to reduce cart abandonment and unlock higher transaction values, while giving consumers a flexible, instant alternative to credit cards and bank loans.

Unlike the mainstream BNPL players that blanket the market with consumer-first messaging, Zaver works backwards from merchant needs—helping online and physical retailers embed installment options directly into their payment flow. The product emphasizes merchant control, transparent pricing, and straightforward integration for businesses of all sizes.

Zaver competes in a crowded BNPL segment but focuses on underserved European markets and SME merchants rather than chasing venture-scale consumer adoption. The company's model centers on merchant acquiring and payment orchestration, positioning BNPL as a revenue driver rather than a customer acquisition cost. In the broader fintech infrastructure play, Zaver represents the shift toward embedded lending—turning payment processing into a financial product.

Founded 2018

ESTO

Lending🇪🇪 Estonia

Estonian consumer credit at the point of online purchase has been transformed by the combination of digital infrastructure that lets credit decisions happen in real time and consumer expectations of completing purchases without leaving the merchant checkout. ESTO was founded in Tallinn in 2016 to serve that specific moment — providing buy now pay later and instalment financing options integrated into Estonian and Baltic merchant checkouts. The platform connects merchants with consumers seeking flexible payment options at purchase, handling underwriting, settlement, and ongoing customer relationship management for the credit products it originates. ESTO has expanded across the Baltic markets and into broader Central European territories, building a position in the BNPL category as one of the regional specialists that competes alongside the larger European platforms by virtue of its local market depth. In the Baltic BNPL landscape, where international platforms have made selective entries but have generally not built the merchant integration depth that domestic operators have, ESTO represents the local champion category. The competitive question for that category is whether local depth in a single regional market can sustain a competitive position as international BNPL platforms continue to expand and as the underlying economics of the category continue to evolve through cycles of growth and regulatory tightening.

Founded 2016

Sequra

Embedded Finance🇪🇸 Spain

Sequra is a Spanish fintech that's quietly become one of Europe's most pragmatic buy-now-pay-later platforms. Rather than chasing the glossy consumer narrative, Sequra built itself as the infrastructure layer for merchants—retailers, e-commerce platforms, and marketplaces across Europe who need flexible payment options without the operational overhead.

The company operates a two-sided model: on one end, it handles merchant acquisiton and underwriting; on the other, it manages the consumer credit experience through instant decisioning and repayment flexibility. What sets Sequra apart is its merchant-first approach. It doesn't market directly to consumers. Instead, it embeds itself into checkout flows and relies on merchant partnerships to scale. This is embedded finance done deliberately.

Sequra's competitive positioning sits between pure BNPL platforms (Klarna, Clearpay) and traditional point-of-sale lending. It's more disciplined about credit risk than some BNPL peers, more tech-native than legacy installers. Across Spain, Italy, France, and Germany, it's become the quiet backbone for thousands of merchants who want flexible payment rails without the consumer brand overhead.

In a fintech landscape increasingly obsessed with consumer apps, Sequra represents a different thesis: sometimes the real value is in being invisible, reliable infrastructure.

Founded 2012

Billink

Payments🇳🇱 Netherlands

Billink is a Dutch payment platform that strips away the friction from business-to-business transactions. Rather than forcing companies to choose between immediate payment and extended credit terms, Billink lets B2B buyers pay later while sellers get funded upfront—a genuine middle ground that's rare in European commerce. The company operates as a bridge between e-commerce platforms, marketplaces, and their merchants, embedding flexible payment options directly into the checkout experience. For online sellers, Billink handles the credit risk and collections; for buyers, it means cash flow breathing room without the paperwork of traditional trade credit. It's not quite a lender, not quite a payments processor, but something more pragmatic: a working capital solution disguised as a checkout button. The platform has gained traction in the Benelux and beyond by solving a specific, genuine problem—SMEs and small merchants need working capital flexibility, and their customers need better payment terms. Billink does both simultaneously. In a fintech landscape crowded with neobanks and lending startups chasing consumer audiences, Billink operates in the quieter, more profitable corner of B2B commerce, where financial friction still costs businesses real money.

Founded 2013

Clearpay

Embedded Finance🇬🇧 United Kingdom

Buy now, pay later has become the default move for a generation of online shoppers, but most BNPL solutions feel bolted on—clunky checkouts, rigid payment schedules, zero personality. Clearpay flips that script by embedding itself seamlessly into the checkout experience, letting customers split purchases into four interest-free instalments without the friction. The platform works with major retailers across fashion, electronics, and home goods, treating payment flexibility as something that should feel as natural as the shopping itself. What sets Clearpay apart in the crowded BNPL space is its focus on the merchant side: brands get instant funding, flexible integration, and customer loyalty tools baked in, while shoppers enjoy a genuinely frictionless experience that doesn't feel like they're applying for a credit product. It's BNPL stripped of complexity and pretension. The company operates across the UK, Australia, and New Zealand, building regional dominance rather than chasing global scale. Clearpay has become one of Europe's most recognizable BNPL platforms precisely because it treats payments as something that should disappear into the shopping experience, not dominate it. In an increasingly crowded fintech landscape, it represents the shift toward embedded finance that doesn't announce itself.

Founded 2013

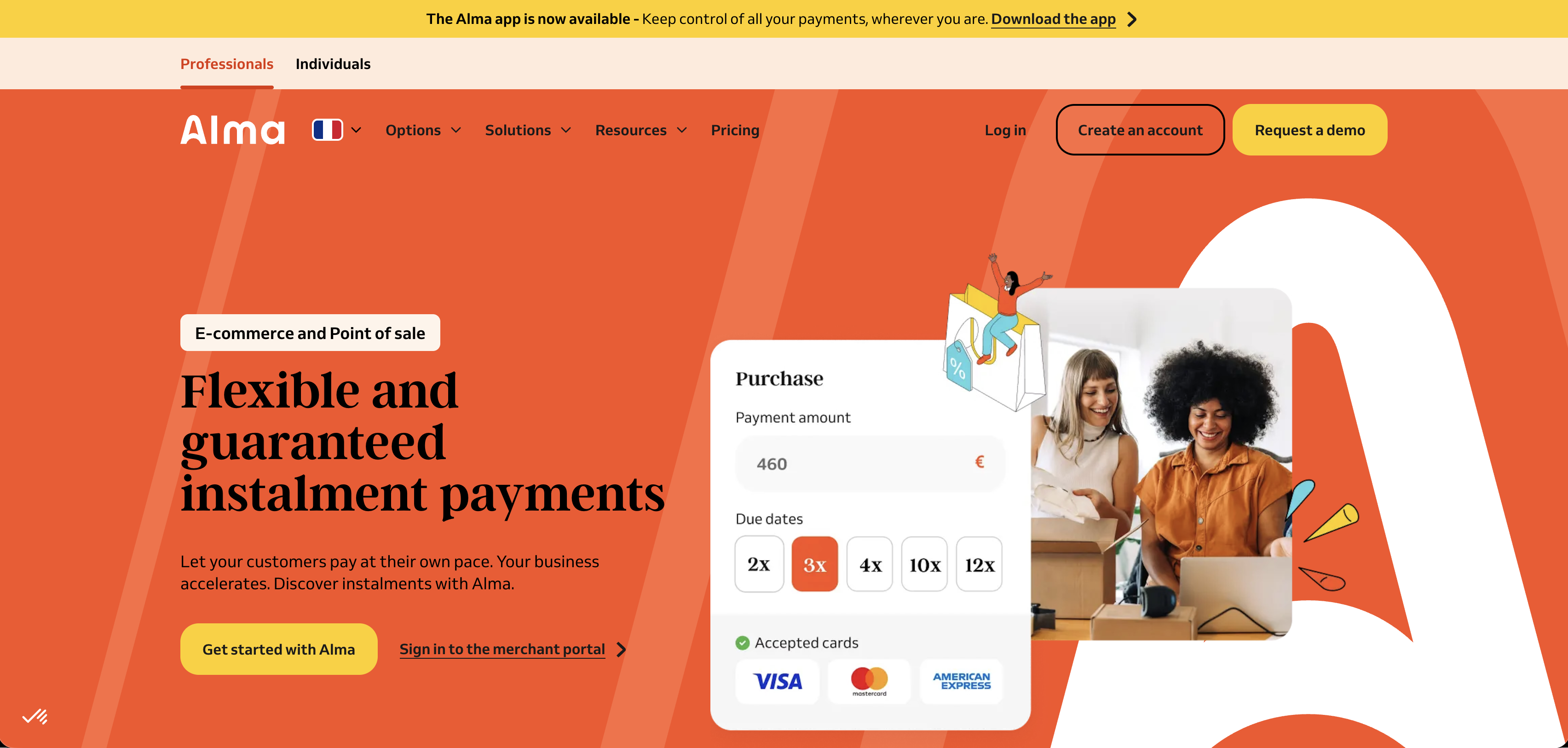

Alma

Embedded Finance🇫🇷 France

Alma is a European fintech built for the modern checkout experience. It sits between merchants and consumers, offering flexible payment options that look and feel native to the shopping journey rather than bolted-on afterthoughts. The platform combines buy-now-pay-later, installment plans, and direct payment methods into a single orchestration layer that merchants can drop into their websites or apps with minimal friction.

What sets Alma apart is its focus on the merchant, not the consumer. While most BNPL startups chase consumer adoption metrics, Alma has positioned itself as the infrastructure behind the scenes, working with e-commerce platforms, marketplaces, and SaaS companies to embed flexible payment options into their products. It handles the underwriting, the risk, and the complexity so merchants don't have to.

The company operates across Western Europe with particular strength in France, Spain, and Germany. Its investor backing and regional focus give it credibility with mid-market and enterprise merchants skeptical of younger fintech players. Alma represents a shift in how payment choice is distributed in Europe—not as a direct-to-consumer play, but as middleware that makes commerce better for everyone involved in the transaction.

Founded 2020

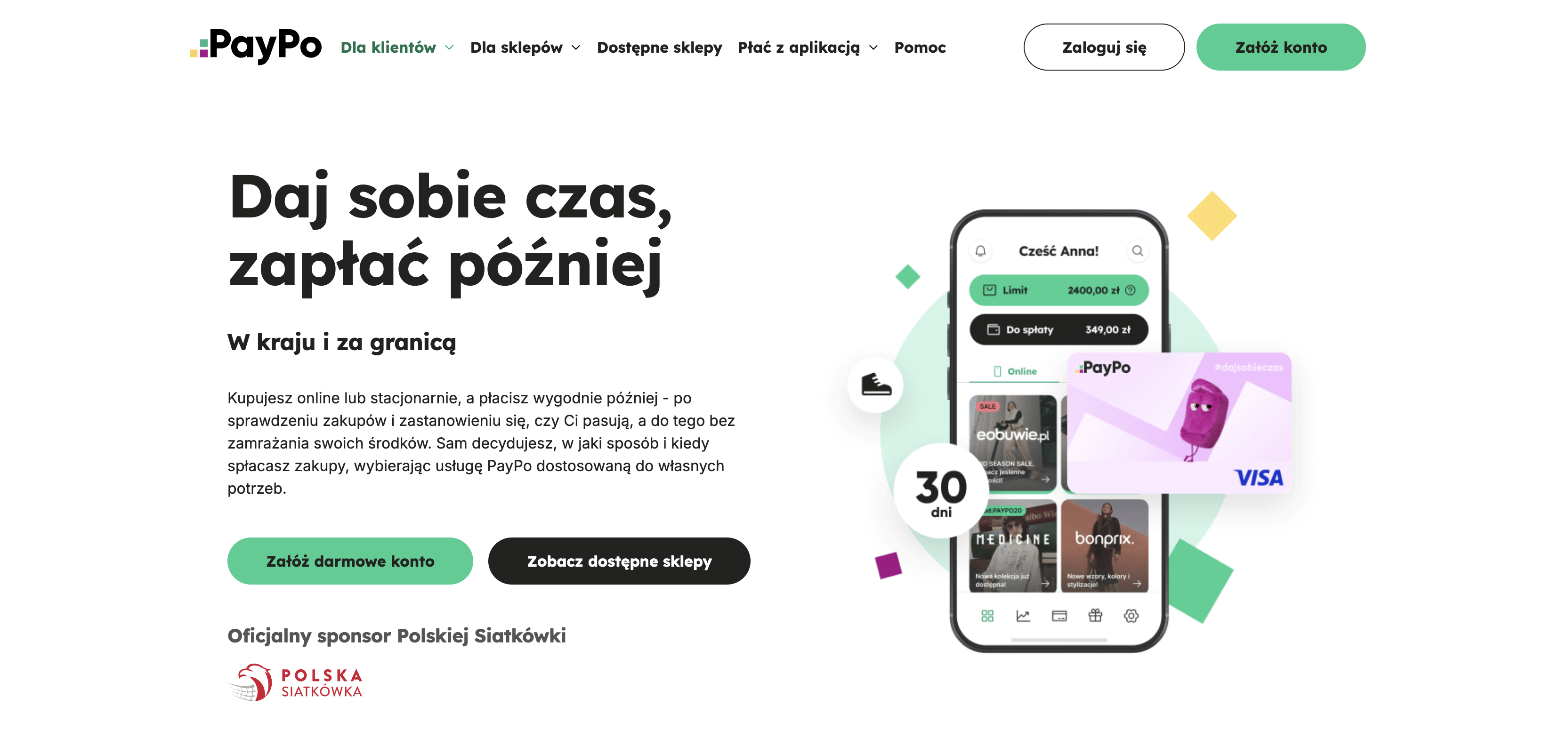

PayPo

Lending🇵🇱 Poland

Polish buy now pay later developed as a category specifically suited to Polish e-commerce dynamics — high online shopping volumes combined with consumer preferences for deferred payment options that fit the cultural patterns of Polish retail finance. PayPo was founded in Warsaw in 2016 to serve that demand with a BNPL product designed for the Polish market, integrating with Polish e-commerce platforms and offering consumers the ability to receive products immediately and pay later through structured instalment plans. The Polish-first focus has been operationally significant — building merchant relationships, credit underwriting infrastructure, and consumer trust in a single market produces depth that international BNPL platforms have generally not matched in Poland despite the size of the market. PayPo has built one of the more substantial Polish BNPL operations, with merchant integration across the platforms that define Polish online retail and a consumer base that has grown alongside the broader Polish e-commerce expansion. In the European BNPL landscape, where the largest international platforms compete for primary market position across multiple countries, the Polish market has remained a genuinely competitive environment for domestic specialists. PayPo represents the category of national champion BNPL operators that have built sustainable positions through operational focus on a single substantial market.

Founded 2016