← All services

20 European companies

P2P lending

Peer-to-peer lending platforms match investors directly with borrowers, with the platform facilitating the loan rather than acting as the lender itself. P2P lending bypasses bank intermediaries, potentially offering better rates for borrowers and better returns for investors. The European P2P market has consolidated significantly following regulatory tightening and defaults during economic stress, with remaining platforms operating under stricter investor protection requirements.

Typically offered by

European fintech companies offering P2P lending

Raize

Lending🇵🇹 Portugal

Raize operates an online lending and investment platform for Portuguese SMEs.

Founded 2014

auxmoney

Lending🇩🇪 Germany

auxmoney sits at the intersection of peer-to-peer lending and digital financial inclusion. The Berlin-based platform connects individual investors with borrowers seeking personal loans, sidestepping traditional bank gatekeeping through algorithmic credit assessment and a streamlined approval process.

Since 2007, it has built one of Europe's more mature alternative lending marketplaces, processing billions in credit and establishing itself as a credible counterweight to institutional finance for everyday lending needs. What sets auxmoney apart in the crowded P2P lending space is its focus on accessibility: borrowers who might struggle with conventional bank criteria can access capital, while investors gain exposure to diversified consumer credit without the friction of direct lending management. The platform automates origination, servicing, and investor payouts, handling the operational complexity that keeps most people out of direct lending. auxmoney doesn't pretend to be a bank—it's unapologetically a marketplace, transparent about risk and returns in ways traditional lenders rarely are.

In a European fintech landscape increasingly dominated by neobanks and payment startups, auxmoney represents a quieter but steadier category: the infrastructure that lets capital find borrowers efficiently. Its longevity and scale demonstrate that P2P lending, despite early hype and inevitable casualties, has become infrastructure for people and investors outside the conventional banking circle.

Founded 2007

EstateGuru

Real Estate Finance🇪🇪 Estonia

Real estate-backed lending across European markets has been one of the more durable categories within marketplace lending, partly because the underlying collateral provides recovery infrastructure that unsecured consumer lending lacks. EstateGuru was founded in Tallinn in 2014 to build a Pan-European platform connecting retail and institutional investors with property developers and real estate businesses needing project financing. The platform operates across multiple European markets, originating loans secured against real estate and offering investors the ability to diversify across geographies and loan types. EstateGuru has funded over a billion euros in real estate-backed loans since inception, making it one of the largest property-focused marketplace lending platforms in Europe. The model has proven more resilient through market cycles than unsecured consumer P2P lending — when borrowers default, the underlying real estate collateral provides recovery options that consumer loans don't have. The company has navigated the broader maturation of European marketplace lending while maintaining the property-secured focus that distinguishes it from generalist platforms. In the European alternative real estate finance landscape, EstateGuru represents one of the more substantial cross-border marketplace operators — building genuine geographic diversification rather than the single-market focus that characterises most regional property finance platforms.

Founded 2014

NeoFinance

Lending🇱🇹 Lithuania

Lithuanian peer-to-peer lending built one of the more substantial European markets for marketplace consumer credit, with multiple platforms competing for both borrowers and investors in a country that has cultivated a regulatory environment supportive of fintech experimentation. NeoFinance was founded in Vilnius in 2014 as one of those Lithuanian P2P pioneers, connecting Lithuanian and international investors with creditworthy local borrowers seeking personal loans. The platform's domestic focus gave it credit data depth in the Lithuanian market that pan-European platforms didn't match, while its EU passport allowed it to attract investor capital from across Europe. NeoFinance has expanded its operations and product range while navigating the maturation of European P2P lending — including the regulatory tightening that brought retail crowdfunding under the European Crowdfunding Service Provider Regulation framework. In the Lithuanian P2P landscape, NeoFinance represents one of the longer-running platforms operating with a domestic borrower focus and a Pan-European investor base — a combination that has proven more sustainable than purely cross-border models that lacked deep credit knowledge of any single market.

Founded 2014

Debitum

Wealth🇪🇪 Estonia

Debitum is a peer-to-peer lending platform that connects investors across Europe with emerging market borrowers, primarily small businesses and consumers in Africa and Southeast Asia. Rather than traditional bank intermediaries, Debitum uses blockchain technology and smart contracts to facilitate direct lending relationships, cutting out middlemen and offering investors returns typically unavailable in their home markets.

The platform operates on a marketplace model where verified borrowers access capital while European investors diversify into emerging markets at institutional-grade returns. What sets Debitum apart is its hybrid approach: it combines traditional credit underwriting with transparent, technology-enabled funding mechanics. Unlike neobanks focused on consumer checking or payment apps targeting young professionals, Debitum sits at the intersection of capital markets access and peer-to-peer finance, targeting financially sophisticated individuals seeking yield. The company tokenizes loans on its platform, allowing fractional investment and secondary market trading. Debitum represents a growing category of European fintech platforms that treat emerging markets not as charity cases but as genuine investment opportunities, democratizing access to higher-yielding assets traditionally reserved for institutional investors.

Founded 2015

RateSetter

Lending🇬🇧 United Kingdom

RateSetter is a peer-to-peer lending platform that cuts out the traditional bank middleman, connecting borrowers directly with retail investors seeking better returns. The London-based marketplace launched in 2010 and has processed billions in loans, operating on the principle that both sides deserve fairer terms than the high street offers. Rather than the opacity of conventional lending, RateSetter's model puts investors in control—they decide which loans to fund and at what rates, while borrowers get transparent pricing without the gatekeeping of legacy institutions. The platform has evolved beyond pure peer-to-peer lending into a more sophisticated investment marketplace, handling everything from personal loans to business finance. RateSetter positions itself as the thinking investor's alternative to savings accounts and bonds, offering yields that reflect real credit risk rather than central bank rates that punish savers. In the fragmented European lending landscape, where fintech platforms compete on transparency and speed, RateSetter remains one of the oldest and most credible players, having weathered multiple regulatory cycles and maintained investor confidence through market volatility. It represents a foundational model in the fintech revolution—the idea that technology and data can democratize finance better than institutional gatekeeping ever could.

Founded 2010

Lendosphere

Lending🇫🇷 France

Lendosphere is a European marketplace lending platform that connects small businesses with institutional investors hungry for alternative returns. Founded on the conviction that traditional banks systematically underserve SMEs, the platform has built a dual-sided network where vetted borrowers access capital at competitive rates while investors diversify beyond bonds and equities. What makes Lendosphere distinct isn't just the marketplace mechanics—it's the emphasis on data-driven credit assessment and a commitment to transparency that appeals to both cautious CFOs and yield-conscious institutional money. The company operates across multiple European markets, handling everything from loan origination through servicing, which means they've had to navigate fragmented regulatory environments while maintaining operational efficiency. In a lending landscape crowded with point solutions and pure-play platforms, Lendosphere positions itself as the connective tissue between supply and demand, enabling capital that would otherwise stay idle or be allocated inefficiently. For SMEs tired of bank gatekeeping, and for institutions seeking uncorrelated returns with human oversight, Lendosphere represents a pragmatic alternative—not utopian blockchain dreams, but boring-boring-good marketplace infrastructure that actually works across borders.

Founded 2014

October

Lending🇫🇷 France

Lending to European SMEs across multiple national markets is genuinely difficult — different regulatory regimes, different credit bureau infrastructures, different cultural attitudes toward debt that vary significantly between France, Germany, Italy, Spain, and the Netherlands. October was founded in Paris in 2014 (originally as Lendix) to build a Pan-European SME lending platform that could navigate that complexity, providing credit to small and medium-sized businesses across multiple European markets through a single platform. Its model combines retail and institutional capital, lending to creditworthy SMEs with proprietary underwriting that adapts to the specific data and regulatory environments of each market. October has built operations in France, Spain, Italy, the Netherlands, and Germany, becoming one of the few genuinely Pan-European SME lenders rather than a single-market platform with international ambitions. Its founder Olivier Goy is one of the more recognisable figures in French fintech, and the company's evolution — from retail P2P origins to institutional and government partnership funding — mirrors the broader maturation of European alternative SME lending. In a European market where SME credit infrastructure remains fragmented along national lines, October represents one of the more successful attempts to operate genuinely across borders.

Founded 2014

Assetz Capital

Lending🇬🇧 United Kingdom

Assetz Capital runs a peer-to-peer lending platform that connects individual investors with small and medium-sized businesses seeking growth capital. Rather than routing deals through traditional bank gatekeepers, the platform lets investors browse vetted SME borrowers, assess risk directly, and earn returns by funding loans. It's a middle ground between passive savings accounts and active equity investing, appealing to investors tired of rock-bottom deposit rates and businesses frustrated by bank credit committees.

The platform handles the heavy lifting: borrower vetting, loan servicing, and portfolio management. Investors can diversify across dozens of loans, while businesses get faster access to capital than traditional lenders typically offer. Returns vary by loan grade, giving investors choices between conservative and aggressive lending strategies.

Assetz Capital occupies a distinct niche in the UK fintech landscape. While equity crowdfunding platforms democratize startup investment and traditional banks control the SME lending market, P2P sits in between—offering real asset backing, regulatory oversight, and returns that reflect genuine credit risk rather than venture speculation. It's become a proving ground for how alternative finance can scale without abandoning prudence.

Founded 2013

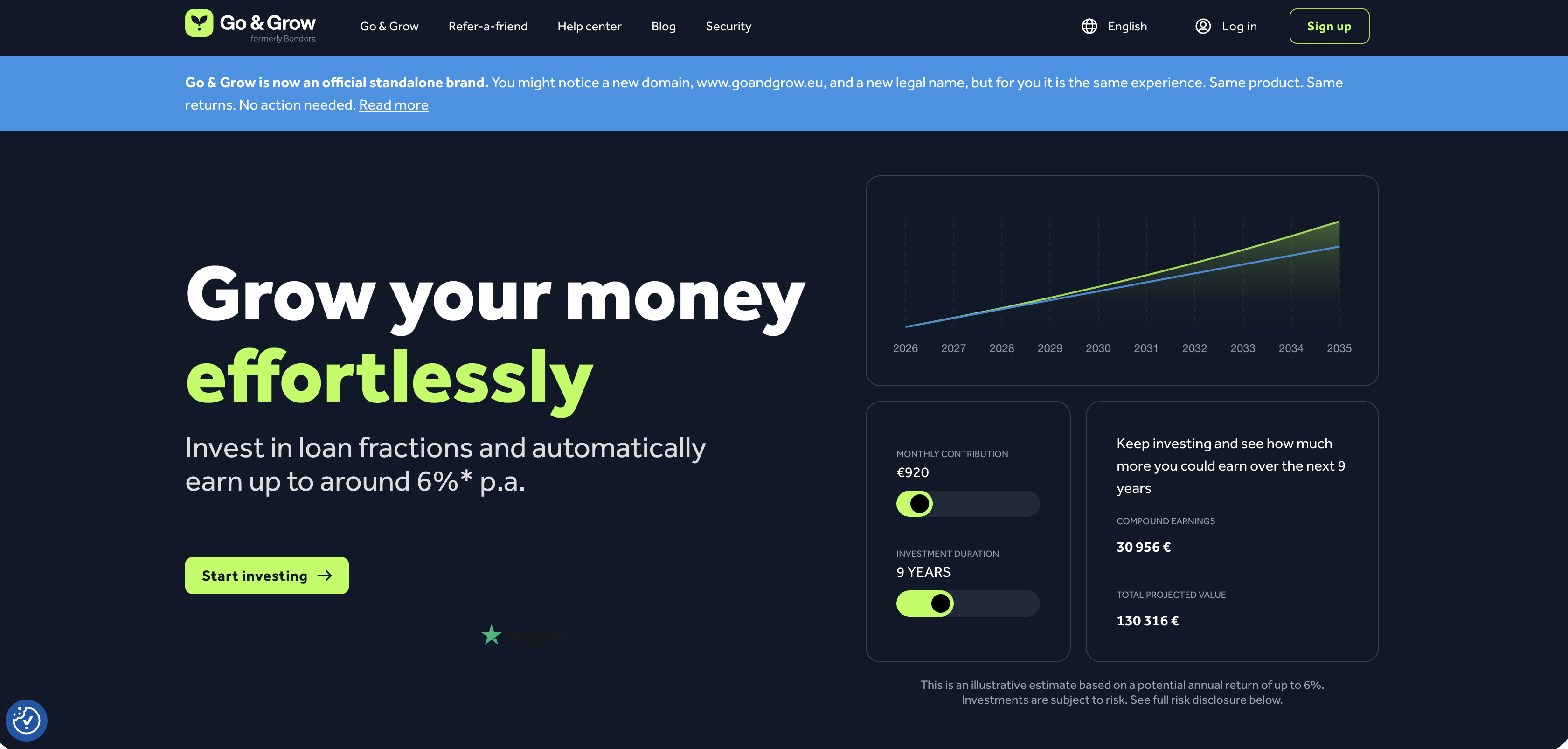

GoAndGrow

Lending🇪🇪 Estonia

GoAndGrow strips away the complexity of peer-to-peer lending by connecting retail investors directly with vetted borrowers across Europe. The platform democratizes alternative finance in a region where traditional banks still gatekeep access to capital, offering returns that actually reflect market conditions rather than the near-zero rates savers have endured for over a decade.

Founded 2015

Robo.cash

Lending🇭🇷 Croatia

Robo.cash operates in the intersection of peer-to-peer lending and alternative finance, offering investors access to curated loan portfolios across emerging markets. The platform automates investment selection and portfolio management through algorithmic underwriting, letting retail investors diversify across geographies without the friction of traditional private lending networks. Unlike conventional P2P platforms that focus on domestic markets, Robo.cash targets cross-border lending opportunities, primarily in Central and Eastern Europe and Latin America. The company positions itself as a fintech bridge between individual capital and underserved borrowing markets, using data-driven credit assessment to reduce default risk. It appeals to yield-seeking European investors looking for alternatives to negative real returns in traditional savings. Robo.cash's automation removes the manual effort from international lending, a category typically locked behind institutional gatekeeping. The platform operates as a regulated marketplace in multiple jurisdictions, handling currency conversion and cross-border settlement automatically. Its role in the broader landscape is part of the democratization wave that challenges traditional banking's monopoly on international capital allocation, though with higher risk profiles than conventional banking products.

Founded 2015

PeerBerry

Lending🇱🇻 Latvia

PeerBerry is a peer-to-peer lending marketplace that connects individual investors with borrowers across Central and Eastern Europe, creating a direct lending alternative to traditional bank loans. The platform operates as an open marketplace where retail investors can fund loans to small businesses and personal borrowers, earning returns through interest payments while borrowers access capital outside conventional banking channels. Unlike traditional peer-to-peer lending platforms that focus primarily on consumer loans, PeerBerry emphasizes business lending and has built a significant presence across multiple CEE markets. The platform functions as a secondary market facilitator, allowing investors to buy and sell loan portions after origination, adding liquidity to what would otherwise be illiquid investments. PeerBerry targets experienced retail investors seeking portfolio diversification through alternative assets, positioning itself as a bridge between European savers and credit-worthy borrowers in emerging markets where traditional lending often remains restrictive. In the broader fintech landscape, PeerBerry represents the maturation of European peer-to-peer lending, moving beyond novelty into established alternative finance infrastructure that now competes directly with institutional capital sources.

Founded 2015

Showing 12 of 20 companies. View all in the directory →