← All services

13 European companies

settlement rails

Settlement rails are the underlying financial market infrastructure that completes the final transfer of securities and funds between counterparties after a trade is agreed. In European markets, settlement typically occurs through central securities depositories like Euroclear and Clearstream. The move toward T+1 settlement across European markets is driving investment in faster, more automated settlement infrastructure.

Typically offered by

European fintech companies offering settlement rails

Thought Machine

Financial Infrastructure🇬🇧 United Kingdom

Thought Machine builds the operating system for modern banking. Its Vault platform is a cloud-native core banking system that replaces the legacy infrastructure most banks still depend on—the kind that was written when personal computers were novel and the internet was optional. Rather than patching decades-old mainframes with band-aids, Vault lets banks modernize from the ground up, moving away from monolithic systems toward modular architecture that can actually adapt to change. The platform serves as the nervous system for digital banking, payment processing, and lending at scale, handling everything from transactions to regulatory compliance in real time. Thought Machine competes directly against vendors like Temenos and Finastra, but with a fundamentally different philosophy: born in the cloud, designed for APIs, built for speed. The company works with tier-one banks and ambitious challengers alike, essentially selling them the technical freedom to compete in fintech's pace rather than their legacy system's glacial timeline. In the broader European fintech ecosystem, Thought Machine represents the infrastructure layer that makes everything else possible—without modern core banking, the rest of the fintech revolution stays locked in legacy constraints.

Founded 2014

Pay.nl

Financial Infrastructure🇳🇱 Netherlands

Pay.nl is a Dutch payment processor built for the complexity of modern commerce. Rather than forcing merchants into a one-size-fits-all payment flow, it offers a modular approach where acquirers, payment methods, and risk tools snap together like building blocks. This flexibility appeals to mid-market retailers and platform operators who've outgrown off-the-shelf solutions but don't have the resources to build from scratch.

The company positions itself as the pragmatic middle ground in European payments. While fintechs chase consumer flashiness and traditional PSPs move at legacy speed, Pay.nl focuses on the unglamorous reality of merchant operations: payment routing, multi-currency settlement, real-time reconciliation, and developer experience. Its API-first architecture means integrations take weeks instead of quarters.

Pay.nl operates across the full payment stack—card acquiring, alternative payment methods, tokenization, subscription billing—but treats them as components rather than marketing bullets. This modular thinking extends to risk management and compliance, which the company bundles without overhead.

Within Europe's crowded payments landscape, Pay.nl competes less on consumer reach and more on merchant control. It's the choice for companies that care about payment economics and operational efficiency rather than brand building. Its role in the broader ecosystem is to mature the middle market, proving that European merchants don't need either a tech giant's infrastructure or a startup's rough edges.

Founded 2007

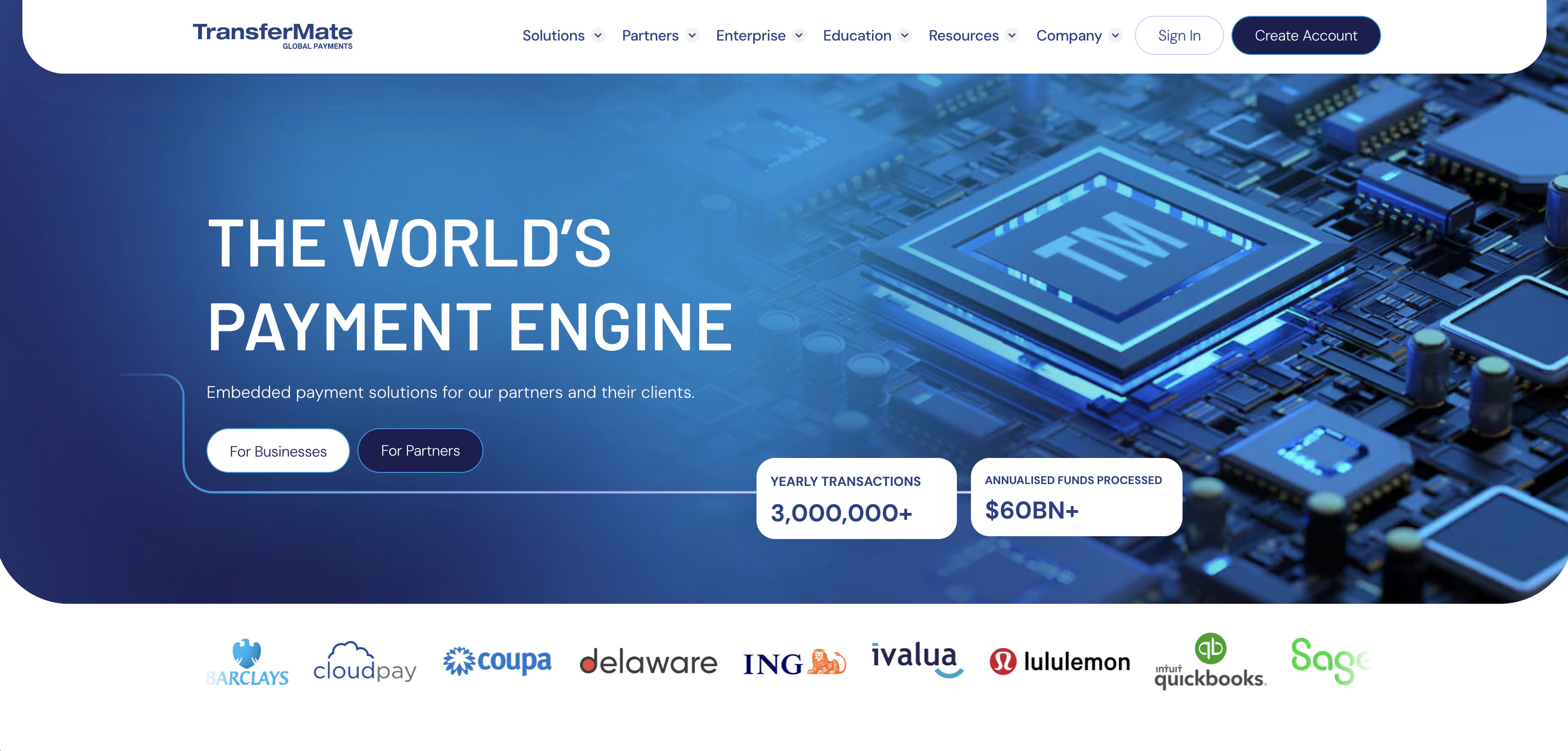

TransferMate

Financial Infrastructure🇮🇪 Ireland

Building a global payments network from Ireland sounds geographically ambitious until you understand that what TransferMate built is the network rather than the consumer-facing product. Founded in Kilkenny in 2010, the company has spent over a decade assembling banking licences and direct connections to local payment systems across more than 200 countries — infrastructure that allows it to settle international payments domestically in each market rather than routing through correspondent banking. The technical achievement is substantial: TransferMate holds payment institution licences across multiple jurisdictions and has direct integrations with national clearing systems that most international payment companies access only through intermediaries. That infrastructure powers the international payment capabilities of major banks, fintechs, and platform companies including Allied Irish Banks, Wells Fargo, and ING. TransferMate operates primarily as a B2B infrastructure provider — the engine behind cross-border payment products that other companies offer to their customers. In the global payments infrastructure landscape, the companies that have built genuine local network access — rather than just routing through SWIFT and correspondent banks — represent a structurally different category of provider. TransferMate's two decades of regulatory and infrastructure investment make it one of the most credible examples of that model.

Founded 2010

Form3

Financial Infrastructure🇬🇧 United Kingdom

Payment processing infrastructure at the scale that banks and fintechs actually operate is a different problem from payment processing for individual transactions. At millions of transactions per day, the reliability, latency, and regulatory compliance requirements of the underlying infrastructure become as important as the feature set. Form3 was founded in London in 2016 to build cloud-native payment infrastructure specifically for financial institutions — banks, payment processors, and fintechs that need the reliability of enterprise infrastructure without the cost and complexity of building it in-house. Its platform provides direct connectivity to payment schemes including Faster Payments, BACS, CHAPS, SEPA, and TARGET2, with a resilient architecture designed for the uptime requirements of financial institutions that cannot afford downtime. Form3 serves some of the UK and Europe's largest financial institutions, providing the payment rails infrastructure that underlies a significant share of European electronic payments. In the payment infrastructure market, Form3 occupies the institutional end of the spectrum — not a product for SMEs or consumer fintechs, but foundational infrastructure for the organisations that process payments at the scale where custom-built solutions are no longer viable and where the cost of failure is measured in regulatory fines and reputational damage.

Founded 2016

Banking Circle

Financial Infrastructure🇱🇺 Luxembourg

Correspondent banking is one of the most expensive and least efficient parts of global finance — a network of bilateral relationships between banks that enables cross-border payments but extracts significant cost and time in the process. Banking Circle was founded in Luxembourg in 2016 to build an alternative — a licensed bank that provides financial infrastructure to payment businesses, banks, and fintechs, enabling them to offer cross-border payment and banking services without relying on traditional correspondent banking relationships. Its platform provides virtual IBANs, multi-currency accounts, cross-border payments, and lending products to payment service providers and fintechs that need banking infrastructure without wanting to become a bank themselves. Banking Circle holds a full European banking licence from the Luxembourg financial regulator, giving it the regulatory standing to provide banking services across the EEA. The company processes hundreds of billions in payment volume annually, making it one of the most significant financial infrastructure providers in Europe that most consumers have never heard of. In the embedded finance and Banking-as-a-Service landscape, Banking Circle occupies the institutional layer — providing the actual banking infrastructure that BaaS platforms often rely on to deliver their own products.

Founded 2016

Axerve

Financial Infrastructure🇮🇹 Italy

Axerve is an Italian payment orchestration platform that handles the messy middle ground between merchants and the fragmented world of European payment networks. Rather than forcing businesses to build integrations with dozens of acquirers, processors, and alternative payment methods, Axerve sits between them—routing transactions intelligently, managing failures, and turning what should be simple into something actually manageable. The platform connects to over 200 payment methods across Europe, from traditional card networks to regional players and emerging wallets, all accessible through a single API. What sets Axerve apart in a crowded space is its focus on the European complexity that most global payment platforms gloss over. They understand that Italian merchants need different acquiring rules than German ones, that transaction regulations shift by country, and that real flexibility means handling local nuances without forcing businesses to hire armies of integration engineers. The company operates with the efficiency of fintech but the institutional credibility of a traditional payments company—they're backed by solid Italian financial infrastructure rather than pure venture capital. For mid-market and enterprise merchants navigating Europe's byzantine payments landscape, Axerve removes the integrations tax and lets teams focus on selling instead of managing payment plumbing. In the broader fintech ecosystem, Axerve represents the infrastructure layer that rarely gets press but quietly enables thousands of European businesses to accept payments without drowning in technical debt.

Founded 1995

Frictionless Markets

Financial Infrastructure🇱🇺 Luxembourg

Frictionless Markets is building the infrastructure layer for cross-border capital flows in Europe. Rather than forcing companies to navigate fragmented clearing and settlement systems across jurisdictions, they've created a unified platform that collapses the friction out of moving money across borders—think of it as the plumbing that lets financial institutions actually operate seamlessly across the continent.

The company tackles a surprisingly stubborn problem: despite decades of fintech progress, moving capital between countries still involves Byzantine manual processes, multiple intermediaries, and settlement delays that would make a 1990s bank nervous. Frictionless automates what should be simple, letting institutions execute, clear, and settle cross-border transactions in a fraction of the time it currently takes.

What sets them apart is their approach to the European market specifically. While global platforms treat Europe as one market, Frictionless has built infrastructure that actually understands and respects the regional regulatory mosaic—different clearing codes, settlement windows, compliance requirements. They're not trying to bulldoze standardization; they're engineering around fragmentation.

The company sits at the critical intersection where traditional finance infrastructure meets modern fintech. As regulatory frameworks like T2S consolidation and PSD3 continue reshaping European payments, Frictionless is positioned as the connective tissue that makes the transition actually work for mid-market institutions.

Founded 2022

Shift4

Embedded Finance🇲🇹 Malta

Shift4 is a payments infrastructure company that processes transactions for some of the world's largest businesses—hotels, travel agencies, e-commerce platforms, and entertainment venues. Rather than building from scratch, Shift4 operates as the backbone that other payment systems rely on, handling everything from card processing to alternative payment methods across multiple continents and currencies. The company processes over $200 billion annually, quietly powering payment flows for thousands of merchants who may never see its name but absolutely depend on its reliability. What sets Shift4 apart in a crowded payment ecosystem is its operational focus. While many fintech companies obsess over consumer-facing innovation, Shift4 builds enterprise-grade infrastructure designed for resilience, speed, and compliance at scale. Its platform handles the complexity that makes most companies cringe: high-volume verticals like hospitality and gaming, multi-currency settlements, regulatory variance across jurisdictions, and the kind of uptime demands that simply cannot tolerate failure. The company has grown through both organic expansion and acquisitions—notably bringing PayMaker into its fold to expand its European footprint and capabilities. For businesses that process millions of transactions daily, Shift4 isn't sexy. It's indispensable. It represents the unglamorous but critical layer of fintech infrastructure that enables everyone else to function.

Founded 1999

Eligma

Financial Infrastructure🇸🇮 Slovenia

Eligma is a cross-border payment and settlement infrastructure built for the digital economy. The company operates a network that simplifies how businesses and consumers move money across borders, stripping away the friction and opacity that characterizes traditional banking corridors. Rather than routing payments through legacy correspondent banking, Eligma connects participants directly, reducing settlement times from days to minutes while cutting costs substantially.

The platform bridges emerging markets with developed economies, focusing particularly on Southeast Asia and Europe. It's built for businesses that operate across jurisdictions—from e-commerce platforms to remittance providers to financial institutions themselves. Eligma abstracts away currency complexity and regulatory variance, presenting a single API that handles what would otherwise require juggling multiple banking relationships.

In a landscape crowded with neobanks and payment startups chasing domestic convenience, Eligma tackles the harder problem: the actual plumbing of international finance. It competes not on consumer interface but on network effects and operational resilience. The company positions itself as infrastructure for the fintech ecosystem itself, enabling other players to offer cross-border services without building the pipes from scratch.

Eligma represents a category increasingly important to European fintech: the B2B rails that sit beneath consumer-facing products, quietly moving capital where legacy banking leaves gaps. As European fintechs expand beyond their home markets, platforms like Eligma become critical dependencies rather than nice-to-have integrations.

Founded 2019

Circit

Financial Infrastructure🇩🇪 Germany

Circit is building the infrastructure layer for European fintechs that need to move money across borders without the complexity. Rather than wrestling with correspondent banking networks or building proprietary integrations, startups and established players alike can plug into Circit's API and access a unified network of payment rails—from SEPA and instant payments to cross-border corridors that traditionally required manual workarounds. The platform abstracts away the operational friction of multi-currency settlement, letting fintech teams focus on product instead of plumbing.

What sets Circit apart is its developer-first approach combined with institutional-grade reliability. The API is clean and modern, designed for teams that expect speed and transparency, not byzantine fee structures or opaque routing logic. Behind the scenes, Circit manages the relationships, compliance, and liquidity that usually tie up engineering resources at smaller companies.

In a market where cross-border payments remain stubbornly expensive and slow despite years of disruption rhetoric, Circit occupies a pragmatic middle ground: not replacing banks, but making it frictionless for fintechs to offer borderless payments without becoming experts in international settlement themselves. It's infrastructure as it should be—invisible, reliable, and genuinely simpler than the alternative.

Founded 2017

Everypay

Financial Infrastructure🇬🇷 Greece

Everypay is a Greek fintech that's built a modern payment infrastructure for local businesses and developers who've grown tired of legacy banking gatekeepers. The platform sits somewhere between a payment gateway and a banking-as-a-service provider, handling card processing, payouts, and settlement for merchants and platforms across Greece and increasingly beyond. What sets Everypay apart in the fragmented Southern European payments landscape is its developer-first approach—clean APIs, transparent pricing, and a focus on solving real operational headaches rather than selling complexity. The company has managed to capture significant volume from SMEs and marketplaces in a market where payment options have historically felt limited or expensive. For Greek merchants especially, Everypay represents a genuine alternative to the traditional banking corridors, offering both acquiring services and access to modern payment rails. It's the kind of infrastructure play that rarely gets headlines but quietly becomes indispensable to the ecosystem it serves.

Founded 2010

Earthport

Financial Infrastructure🇬🇧 United Kingdom

Cross-border payment infrastructure for banks has been one of the longest-running unfinished projects in financial services. Banks need to make international payments for their customers but maintaining direct correspondent relationships in every market is uneconomic. SWIFT solves part of the problem but introduces its own costs and delays. Earthport was founded in London in 1997 to provide an alternative — a payment network that connected banks directly to local clearing systems across multiple countries, enabling lower-cost, faster cross-border payments without traditional correspondent intermediaries. The company built a global network covering over 90 countries and served major banks and money transfer operators as the wholesale infrastructure underlying their consumer-facing international payment products. Earthport was acquired by Visa in 2019 — a deal that integrated its real-time payment network into Visa Direct, dramatically expanding Visa's cross-border push payment capabilities. The acquisition reflected the strategic value of a global payment network at a moment when real-time international payments were becoming a competitive battleground. For the European fintech ecosystem, Earthport's trajectory — from independent payment innovator to Visa-owned infrastructure — illustrates how the most valuable cross-border payment infrastructure ultimately gets absorbed by the card networks whose own businesses depend increasingly on global reach.

Founded 1997

Showing 12 of 13 companies. View all in the directory →