← All services

23 European companies

budgeting apps

Budgeting apps help individuals plan and track their spending against targets across categories, using open banking data to automatically categorise transactions and provide real-time visibility into financial behaviour. Modern budgeting apps have moved from manual spreadsheet entry to automatic data aggregation, making the gap between actual and planned spending visible without ongoing effort.

Typically offered by

European fintech companies offering budgeting apps

Monzo

Wealth🇬🇧 United Kingdom

The founding team that built Monzo had all worked together before — at Starling Bank, another challenger bank startup that didn't survive its internal conflicts. Tom Blomfield, Gary Dolman, Jonas Huckestein, Jason Bates, and Paul Rippon left Starling together in 2015 and started again. The product they built was initially a prepaid card — a coral-coloured piece of plastic that became one of the most recognisable objects in British fintech — before becoming a fully licensed current account in 2017.

The early user community was unusual for a bank. Monzo ran community forums, published public blog posts about its engineering decisions, and invited customers into beta programmes for new features. When it broke the world record for the fastest crowdfunding raise in 2016 — £1 million in 96 seconds — it wasn't just raising money; it was building an identity. People felt ownership of the product in a way that no high street bank had ever managed to create. That emotional connection became a genuine competitive advantage.

The product has matured considerably since then. Monzo now offers current accounts, joint accounts, savings pots, personal loans, overdrafts, and investment products, all wrapped in the real-time notification experience and transaction categorisation that made its early reputation. Revenue reached £1.23 billion in 2024, up 40% year on year, with net income of £95 million — the second consecutive year of profitability after years of growth-first losses. The customer base reached 12.1 million by end of 2024, making Monzo the UK's largest digital bank by customer count. Customer deposits stood at £16.6 billion.

The business is still private — the much-discussed IPO has not yet happened, and internal disagreements about where to list (the former CEO TS Anil favoured the US, the board preferred London) contributed to Anil's departure in October 2025. Diana Layfield took over as CEO with a mandate focused on international expansion before any public listing. The company is valued at approximately $5.9 billion following a 2024 secondary sale backed by Alphabet's GIC and StepStone.

In December 2025 Monzo announced it had agreed to acquire Habito, the digital mortgage broker, pending regulatory approval — a move that extends the product into one of the last major financial products it didn't yet offer. With 3,821 employees and a loan book growing rapidly, Monzo has evolved from a prepaid card experiment into a bank with genuine scale and a growing claim on being the primary financial account for a generation of UK consumers.

Founded 2015

Starling Bank

Digital Banking🇬🇧 United Kingdom

Starling Bank is a British challenger bank that stripped away the friction of traditional banking and rebuilt it around what modern customers actually need: instant notifications, real-time spending insights, and accounts you can open in minutes without stepping into a branch. Founded in 2014, it operates as a fully regulated bank with its own banking license, not just a wrapper around legacy infrastructure.

The platform serves both consumers and SMEs, offering straightforward current accounts, savings pots, and increasingly sophisticated business banking tools. Unlike neobanks reliant on partnerships, Starling owns its core infrastructure, which means faster iteration and tighter product control. The company has built a reputation for no-nonsense transparency: no hidden fees, no overdraft tricks, and clear communication about what you're getting.

In the crowded UK digital banking space, Starling stands apart through consistent execution and a focus on solving real problems rather than chasing hype. It's profitable, self-sufficient, and treated by legacy banks as a genuine competitor rather than a novelty. For European fintechs, Starling represents the successful blueprint: regulated, capital-efficient, and genuinely preferred by millions of users who value simplicity over flashiness.

As the fintech landscape matures, Starling exemplifies the shift from disruption theater to sustainable banking infrastructure—a reminder that the most radical innovation often looks deceptively simple.

Founded 2014

Pockit

Digital Banking🇬🇧 United Kingdom

Pockit is a mobile-first financial platform designed for people who've been locked out of traditional banking. Rather than chasing the affluent, Pockit focuses on the underbanked—those without access to a current account, credit history, or the documentation banks demand. The app serves as a genuine alternative to brick-and-mortar banking, offering digital accounts, card payments, and money management tools entirely through your phone.

What sets Pockit apart is its commitment to financial inclusion without the gatekeeping. You don't need a credit score or payslip to open an account. Instead, the platform builds trust through usage patterns and behavioral data, creating pathways for people traditionally rejected by high street banks. This shifts the relationship from one of suspicion to one of genuine access.

The company operates across the UK and Europe, proving that underserved segments aren't just a niche—they're a substantial market. Pockit's mission is radical in its simplicity: banking shouldn't require jumping through hoops or having the right background. It's a challenger in the truest sense, not because it offers flashy features, but because it solves a real problem for millions of people who simply want to participate in the financial system.

Founded 2015

Ritmo

Digital Banking🇪🇸 Spain

Ritmo is a neobank built specifically for the gig economy—the millions of freelancers, contractors, and self-employed workers across Europe who operate outside traditional employment structures. Instead of forcing gig workers into standard business banking products, Ritmo designed from the ground up to understand the rhythms of irregular income, multiple clients, and the administrative burden that comes with self-employment.

The platform combines a business checking account with invoicing, expense tracking, and tax preparation tools, removing the friction between earning money and managing it. You get real-time visibility into cash flow, automated categorization of business expenses, and direct integration with tax authorities—so when it's time to file, the data is already organized.

What sets Ritmo apart isn't just its feature set. Most fintech players either chase the consumer market or build enterprise solutions for corporations. Ritmo recognized a gap: gig workers are economically significant but underserved by both traditional banks and most neobanks. The company speaks their language, understands their cash flow volatility, and builds products that actually reflect how they work.

In the broader European fintech landscape, Ritmo represents a growing trend of vertical-specific banking platforms. Rather than being all things to all people, it's solving a precise problem for a rapidly growing demographic. For the gig worker tired of explaining variable income to a bank manager or juggling multiple apps, Ritmo is the kind of focused, no-nonsense solution that defines modern fintech at its best.

Founded 2021

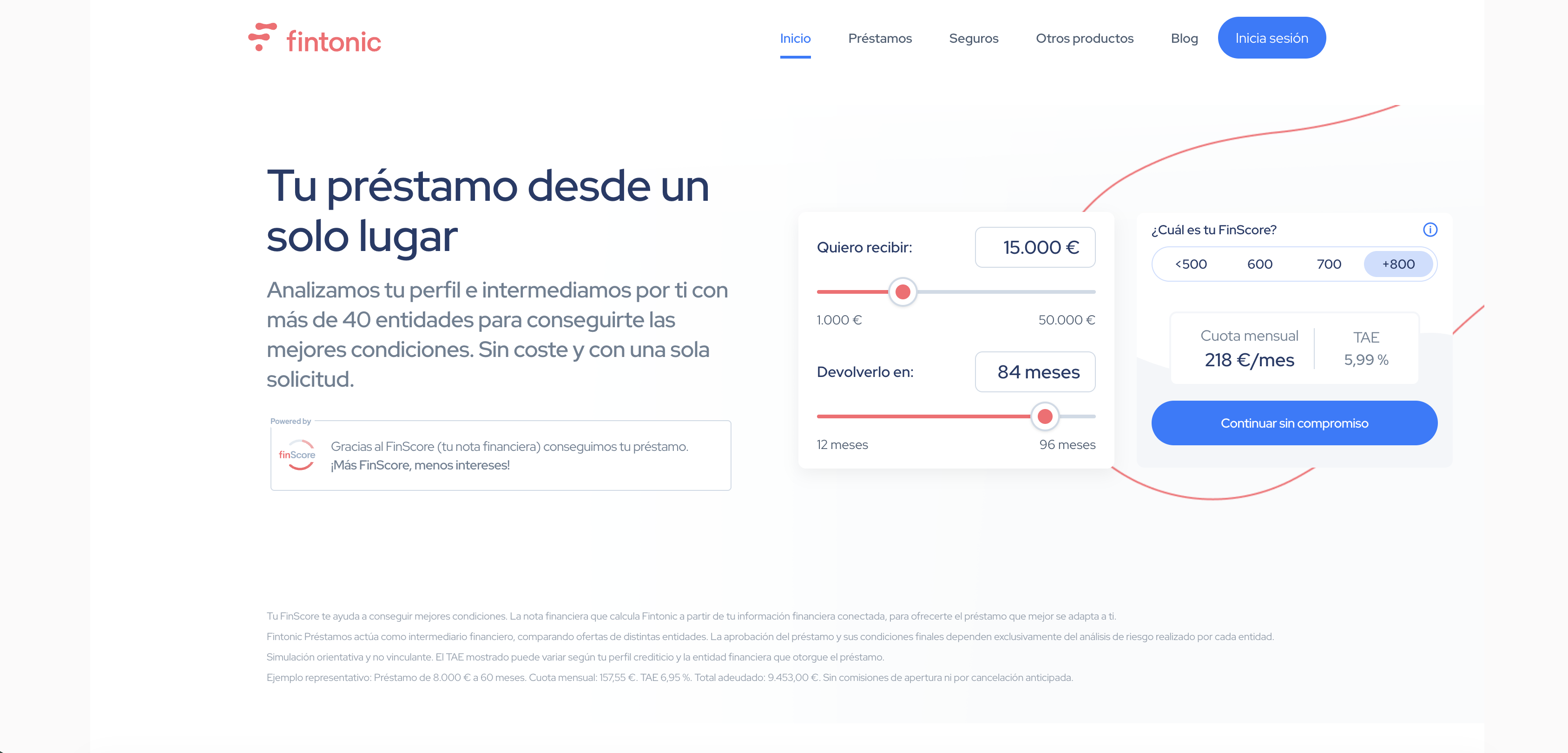

Fintonic

Open Banking🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

Founded 2011

Avanza

Wealth🇸🇪 Sweden

Avanza is Sweden's largest independent online brokerage, a no-frills investment platform that democratized stock trading for Swedish retail investors two decades ago. What started as a scrappy alternative to traditional banks has become the go-to app for millennials and Gen Z who want to trade, invest, and save without paying legacy banking fees. The platform strips away unnecessary complexity—no advisors, no jargon, just direct market access at transparent prices. Avanza operates in that interesting middle ground between a neobank and a pure trading platform. It offers savings accounts, pension accounts, and investment accounts with a sharp focus on user experience and low costs. The company has built a cultural following in Sweden, becoming almost synonymous with retail investing for a generation that views traditional brokers as relics. Beyond just equities and funds, Avanza has expanded into savings products, retirement planning, and financial education—positioning itself as a genuine financial companion rather than just a transaction layer. Its dominance in the Nordic market reflects a broader European shift toward direct-to-consumer investment platforms that compete on transparency, speed, and mobile-first design. Avanza exemplifies how fintech can win by doing one thing exceptionally well and then expanding thoughtfully into adjacent categories. The company's influence extends beyond Sweden into a broader shift in how younger Europeans think about investing: without gatekeepers, without unnecessary fees, and entirely on their own terms.

Founded 1999

Blackcat

SME Finance🇩🇪 Germany

Blackcat is a German fintech platform designed to help freelancers and self-employed professionals manage their finances with minimal friction. Rather than forcing users into complex accounting workflows, Blackcat simplifies the entire money flow—from invoicing to tax filing—with a mobile-first interface that feels more like a consumer app than enterprise software.

The platform tackles a real pain point in the European freelance economy: most existing tools are either bloated legacy systems or fragmented point solutions that don't talk to each other. Blackcat bundles invoicing, expense tracking, tax preparation, and business banking into one coherent experience, removing the cognitive load of juggling multiple services.

What sets Blackcat apart is its opinionated approach to simplicity. Rather than mirroring traditional accounting software's feature sprawl, it prioritizes the workflows that matter most to freelancers—getting paid faster, documenting expenses, and staying tax-compliant without the headache. The platform's integration with German tax authorities and compliance frameworks positions it as particularly valuable in the DACH region, where self-employed taxation can be notoriously complex.

In a market crowded with accounting tools and SME platforms, Blackcat represents a new generation of fintech that starts with the freelancer's actual needs rather than retrofitting legacy processes into a digital wrapper. It's part of a broader shift toward consolidated SME finance platforms that understand that complexity itself is the problem.

Linxo

Open Banking🇫🇷 France

Linxo is a European personal finance platform that aggregates bank accounts, credit cards, and investments across multiple institutions into a single dashboard. Rather than asking users to switch banks entirely, the app pulls live data from existing accounts—a model that respects the European's pragmatic relationship with their primary bank while offering the insights and control they actually want. The company positions itself as the financial operating system for everyday money management, not a replacement for banking itself.

What sets Linxo apart in a crowded personal finance space is its focus on actionable intelligence. Beyond simple balance-checking, the platform categorizes spending automatically, alerts users to unusual transactions, and helps track progress toward financial goals—all without the paternalistic tone of many budgeting apps. It works across France, Spain, Germany, Italy, and Belgium, making it one of the few genuinely pan-European plays in a category often dominated by single-market apps.

Linxo has built its infrastructure on open banking standards, leveraging PSD2 APIs to connect securely to banking institutions rather than relying on screen-scraping. This approach gives it a technical moat while also keeping it aligned with regulatory trends. The company targets digitally-native adults who want visibility into their finances without the friction of traditional banking interfaces.

In the broader fintech landscape, Linxo represents a specific bet: that most people won't abandon their bank, but they will absolutely pay for—or accept advertising within—a tool that makes that bank easier to use. It's less disruptive than a neobank, more practical than an investment app, and more design-forward than legacy personal finance software.

Founded 2015

Bankin

Digital Banking🇫🇷 France

Bankin is a French fintech that connects you to your money across multiple banks through a single app. Rather than juggling five different banking apps, Bankin aggregates all your accounts—checking, savings, investments, crypto—into one place where you can see your full financial picture. The company doesn't hold your money or replace your banks; it's an overlay that reads your data securely and gives you control over what happens next. What sets Bankin apart is its focus on switching: unlike most aggregators that just show you balances, Bankin helps you move money between banks, find better rates, and actually leave a bank if you want to. It's positioned somewhere between a personal finance dashboard and a financial comparison tool, but with genuine switching capability baked in. The app works across Europe, though strongest in France and the Nordics, and has built a loyal base of power users who genuinely use it to manage their money rather than just peek at their balance. In a landscape crowded with robo-advisors and neobanks offering me-too features, Bankin solves a more mundane but more urgent problem: most people still bank with multiple institutions and hate managing them. The company has positioned itself as the glue holding fragmented European banking together, and that simplicity—aggregation plus switching—gives it a unique role in the open banking revolution.

Founded 2013

FinFrog

Digital Banking🇫🇷 France

FinFrog is a French neobank designed for the Instagram generation—a mobile-first challenger that strips away the pretense of traditional banking and treats financial management like a social experience. Rather than positioning itself as a replacement for your main bank, FinFrog positions as the fun account you actually use, complete with spending analytics that actually make sense and a card that feels like an extension of your lifestyle rather than a financial obligation.

The platform focuses on real-time spending visibility, automated savings mechanisms, and a philosophy that younger Europeans shouldn't have to tolerate clunky interfaces or hidden fees just to manage their money. It's built on the premise that financial literacy and engagement happen through friction-free, mobile-native experiences, not through apps bolted onto legacy systems.

Within the European challenger banking landscape, FinFrog carves out space by leaning heavily into design and user experience clarity rather than attempting to be everything at once. While competitors chase feature bloat, FinFrog has maintained focus on core banking and budgeting fundamentals executed at a level that feels genuinely differentiated.

As part of the broader shift toward mobile-first financial services in continental Europe, FinFrog represents the next wave of neobanks that treat banking as a utility that should be boring, fast, and actually yours—no corporate messaging, no pretense, just money that works.

Founded 2018

Meniga

Digital Banking🇮🇸 Iceland

Personal finance management has been fragmented for years—users juggle multiple accounts across different banks, struggle to categorize expenses, and lose sight of their actual spending patterns. Meniga built the operating system for that chaos, connecting directly to banks across Europe and beyond to give people a unified view of their financial life.

The company aggregates account data from thousands of financial institutions, automatically categorizes transactions, and surfaces actionable insights through intuitive mobile and web interfaces. Rather than forcing users to manually log expenses or switch banks, Meniga meets them where their money already is. The platform learns spending habits over time and can flag anomalies, suggest savings opportunities, and help families coordinate finances in one place.

While most fintech startups chase headlines with flashy features, Meniga has stayed disciplined on the unglamorous work of data plumbing and user experience. It's become the backend for other financial services—banks, brokers, and insurers across the region use Meniga's APIs and white-label solutions to power their own personal finance tools, rather than building from scratch.

The company operates quietly but pervasively across Northern Europe and beyond, having grown from a Reykjavik startup into a critical piece of financial infrastructure for millions of users and dozens of institutional partners. In an era of financial fragmentation, Meniga is the connective tissue.

Founded 2009

Hype

Digital Banking🇮🇹 Italy

Hype is Italy's answer to the mobile banking revolution, a neobank that has spent nearly a decade proving that digital-first doesn't mean stripped-down. Rather than chase global scale with generic features, Hype has built a hyperlocal following by understanding what young Italians actually want from their money: instant transfers, cashback rewards, zero monthly fees, and a sleek app that doesn't feel like it was designed by a committee of compliance officers.

The platform operates as a digital-only current account backed by actual IBAN credentials, so it's not playing at banking—it's the real thing, licensed and regulated. Users get a contactless Mastercard, push-notification alerts for every transaction, and the kind of interface that makes traditional banking feel positively medieval by comparison. Hype's cashback ecosystem is its signature move, offering percentage returns on spending across partner merchants, which transforms the app from a mere account holder into a lifestyle spending companion.

In a market where European neobanks have largely converged around identical feature sets, Hype has chosen to go deep rather than broad, cementing itself as the default neobank for Italian millennials and Gen Z. It's proof that you don't need hundreds of millions in funding or ambitions to be present in every time zone to build something genuinely meaningful. The company represents a particular kind of fintech success: profitable, focused, and beloved by its core audience rather than chased by venture capitalists.

Hype demonstrates that the future of banking in Europe isn't about creating one global super-app, but rather a network of fiercely intelligent regional players, each optimized for the specific financial behaviors and preferences of their home market.

Founded 2014

Showing 12 of 23 companies. View all in the directory →