← All services

21 European companies

reconciliation

Reconciliation is the process of confirming that financial records across different systems match — verifying that bank statements align with internal ledgers, that payments processed match payments expected, and that any discrepancies are identified and resolved. Automated reconciliation platforms replace manual spreadsheet matching with software that processes large transaction volumes, identifies breaks, and routes exceptions for investigation.

Typically offered by

European fintech companies offering reconciliation

Pleo

Payments🇩🇰 Denmark

Pleo is a corporate expense management platform that treats company spending like a personal finance problem solved through software. Rather than the tedious reimbursement cycles and spreadsheet chaos of traditional corporate cards, Pleo gives employees physical and virtual cards coupled with real-time expense categorization and approval workflows that happen at the speed of a Slack message.

The company positions itself as the antidote to finance teams drowning in manual reconciliation. Employees get instant card access, automatic receipt capture via smartphone, and intelligent categorization that learns spending patterns. Meanwhile, finance teams gain real-time visibility into company spending without the usual lag and friction.

Pleo operates in a market where most companies still rely on legacy corporate card providers or outdated expense management software that feels bolted together from the 1990s. The Danish fintech has expanded across Europe, building a platform that combines the convenience of consumer fintech with the compliance and control requirements of enterprise finance.

It's become a reference point for how embedded finance and B2B SaaS can simplify workflows that enterprises have tolerated as painful for decades. The company sits comfortably at the intersection of business banking, card issuing, and expense automation—categories that individually are crowded but rarely integrated as seamlessly.

Founded 2015

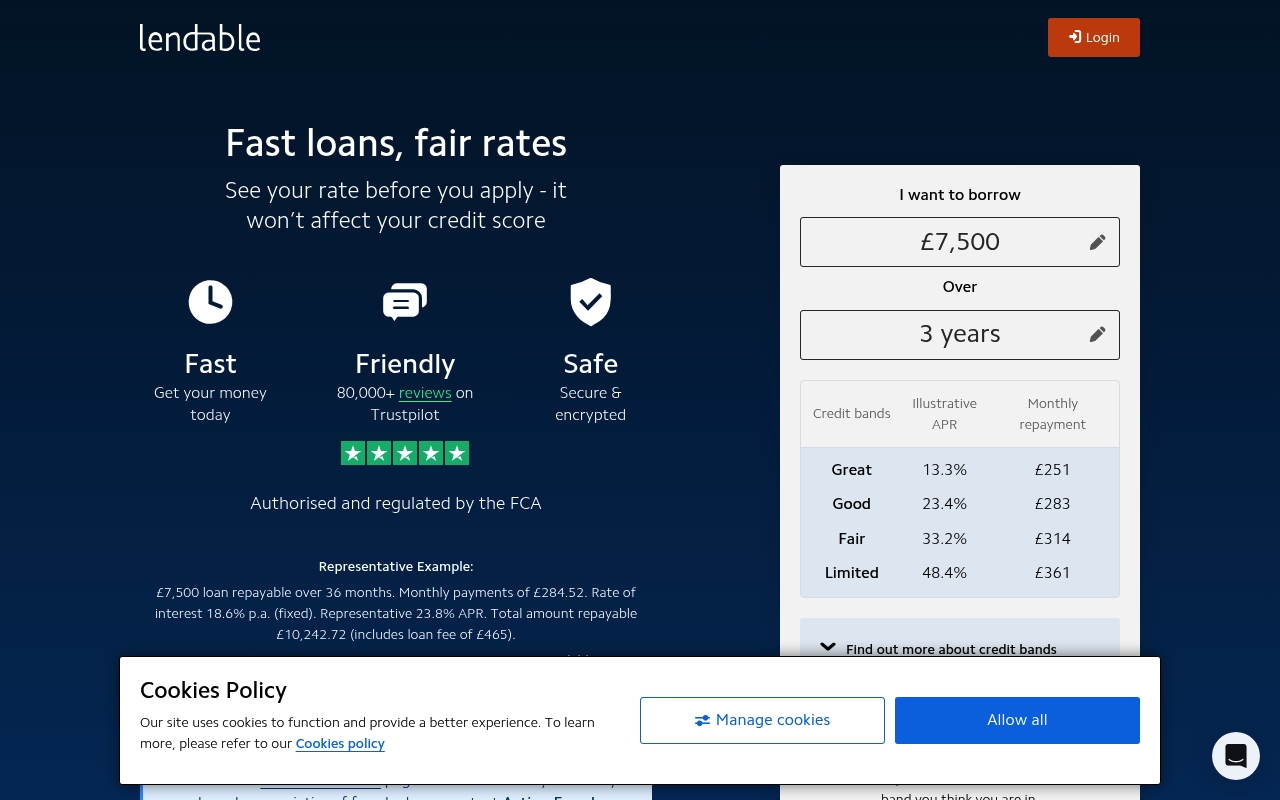

Lendable

Financial Infrastructure🇬🇧 United Kingdom

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates.

The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets.

In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names.

Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

Founded 2013

Payhawk

Embedded Finance🇧🇬 Bulgaria

Most companies still manage corporate spending the way they did a decade ago—expense reports, manual reconciliation, scattered receipts. Payhawk has built something radically simpler: a unified spending platform that gives finance teams complete visibility into every company transaction, from the moment it's authorized to the moment it's reconciled. The platform combines physical and virtual cards, automated expense management, and real-time spend controls in a single dashboard.

What sets Payhawk apart in the crowded corporate finance space is its refusal to compromise on user experience. Employees aren't fighting clunky interfaces or wrestling with legacy systems. Instead, they get an intuitive mobile app that feels like personal fintech, while finance teams gain the analytical firepower to actually manage policy, catch fraud, and optimize spending patterns. The company treats visibility not as a nice-to-have but as the foundation of control.

In Europe's SME and mid-market space, where most alternatives still rely on outdated card programs or disconnected software suites, Payhawk's integration of issuance, spend management, and analytics represents a meaningful shift. The company has quietly built something that enterprises have wanted for years: a spending platform that doesn't require compromise between employee experience and financial governance. For finance leaders tired of spreadsheets and reactive reporting, it's become the natural choice.

Founded 2019

Ramp

Financial Infrastructure🇵🇱 Poland

Ramp is rewriting how companies spend money. Built for finance teams tired of spreadsheets and manual processes, it combines a corporate card, expense management, and accounting integrations into a single platform that actually talks to the software finance teams already use. Most corporate card programs feel like they were designed in 1995. Ramp feels like software built this decade—mobile-first, API-forward, and deeply integrated with tools like NetSuite and QuickBooks. The company started by solving a real problem: CFOs and controllers wasting hours reconciling card statements and expense reports. Instead of patching that broken workflow, Ramp replaced it entirely. You get a card, real-time spending controls, automated categorization, and instant syncing to your accounting system. No more manual entries, no more approval bottlenecks, no more spreadsheet chaos. The platform goes deeper than most competitors by combining physical and virtual cards with embedded controls—spend limits by department, merchant category, or individual employee. Finance teams can actually enforce policy in real time rather than auditing violations weeks later. Ramp operates in a crowded space, but it's differentiated by speed and simplicity. Where competitors try to be everything to everyone, Ramp has kept focus on what CFOs actually care about: reducing manual work, improving visibility, and cutting unnecessary spending. Its integration-first approach means it's not trying to replace your entire finance stack—it's designed to slot in and make your existing tools work harder. For mid-market companies tired of manual expense management and lacking the complexity of enterprise-grade solutions, Ramp has become the obvious choice. It's also been ruthless about profitability, reaching positive unit economics early, which matters in a category where many competitors burned through billions before proving their model worked.

Founded 2019

Pennylane

Digital Banking🇫🇷 France

Pennylane is a French fintech that bundles accounting, invoicing, and banking into one platform built for freelancers and small businesses. Rather than piecing together separate tools, users get a unified workspace where transactions sync automatically, expenses categorize themselves, and tax calculations happen in the background. The company positions itself against the fragmented mess of legacy accounting software and generic banking solutions, betting that SMEs want a single interface that actually understands their cashflow.

What sets Pennylane apart in Europe's crowded SME finance space is its focus on simplicity without sacrificing depth. While competitors often target either accountants or business owners, Pennylane aims at the owner-operator who wants to understand their numbers without hiring bookkeeping help. The platform connects directly to bank feeds and invoice data, pulling everything into a dashboard that feels less like traditional accounting software and more like a modern finance app.

Pennylane represents a shift in how European SMEs are expected to manage money. Rather than quarterly accountant visits and spreadsheet chaos, the company argues that modern businesses should have real-time visibility into their finances. It's part of a broader movement to make financial operations software actually enjoyable to use, not just tolerable.

Founded 2018

Pay.nl

Financial Infrastructure🇳🇱 Netherlands

Pay.nl is a Dutch payment processor built for the complexity of modern commerce. Rather than forcing merchants into a one-size-fits-all payment flow, it offers a modular approach where acquirers, payment methods, and risk tools snap together like building blocks. This flexibility appeals to mid-market retailers and platform operators who've outgrown off-the-shelf solutions but don't have the resources to build from scratch.

The company positions itself as the pragmatic middle ground in European payments. While fintechs chase consumer flashiness and traditional PSPs move at legacy speed, Pay.nl focuses on the unglamorous reality of merchant operations: payment routing, multi-currency settlement, real-time reconciliation, and developer experience. Its API-first architecture means integrations take weeks instead of quarters.

Pay.nl operates across the full payment stack—card acquiring, alternative payment methods, tokenization, subscription billing—but treats them as components rather than marketing bullets. This modular thinking extends to risk management and compliance, which the company bundles without overhead.

Within Europe's crowded payments landscape, Pay.nl competes less on consumer reach and more on merchant control. It's the choice for companies that care about payment economics and operational efficiency rather than brand building. Its role in the broader ecosystem is to mature the middle market, proving that European merchants don't need either a tech giant's infrastructure or a startup's rough edges.

Founded 2007

Spendesk

Financial Infrastructure🇫🇷 France

Spendesk cuts through the chaos of corporate spending. It's a unified platform where teams manage expenses, issue corporate cards, approve invoices, and reconcile everything in one place—no more spreadsheets shuffled across email chains or finance teams drowning in admin work.

The platform sits somewhere between a spend management tool and a modern finance operating system. Companies connect their bank accounts, set spending rules, issue virtual or physical cards to employees, and watch transactions flow into an automated approval workflow. Invoices get coded automatically. Reconciliation happens in real time. The whole thing syncs with accounting software so the numbers always match reality.

What makes Spendesk different is that it treats spend management as a team sport, not a back-office chore. It's built for the actual workflows that modern finance teams use: expense reports that don't feel like punishment, card management that doesn't require IT involvement, and visibility that doesn't require a Ph.D. in Excel. Most competitors bolt features together; Spendesk designed the experience first.

In a market crowded with point solutions and legacy software masquerading as modern, Spendesk has become the de facto standard for mid-market companies in Europe that want to stop thinking about spending and start optimizing it. It's now a critical piece of infrastructure in how thousands of companies handle money.

Founded 2015

Mangopay

Embedded Finance🇱🇺 Luxembourg

Mangopay sits at the intersection of payments infrastructure and marketplace complexity. Rather than selling fintech features individually, the company tackles the full stack problem: how do you actually move money between dozens of parties—buyers, sellers, platforms, creators—when everyone needs different settlement rules and nobody trusts a stranger with their cash.

Founded in 2011, Mangopay is a Brussels-based powerhouse that specializes in payout infrastructure for marketplaces, platforms, and creator economies. The platform handles the messy reality of modern commerce: a freelancer in Barcelona getting paid by a client in London, a marketplace taking commission, a payment processor taking a fee, and a tax authority wanting its cut—all simultaneously, all reconciled, all compliant.

What sets Mangopay apart is its pragmatism. While most payment processors treat multi-party transactions as an edge case, Mangopay designed around it from the start. The company's white-label approach means you barely know it's there—you integrate their APIs, they handle the regulatory nightmare, and your users see your brand. That's the opposite of fintech theater.

The European fintech world has fractured into specialists: payments here, compliance there, ledger systems somewhere else. Mangopay refuses that fragmentation. In a landscape where payment orchestration feels trendy and new, Mangopay has been solving it at scale for over a decade.

Founded 2011

Tradeshift

Financial Infrastructure🇩🇰 Denmark

Tradeshift runs the operating system for global commerce—a cloud platform that lets businesses transact with each other in real time, from purchase orders to invoices to payments. It's built for a world where finance teams spend less time on manual reconciliation and more time on strategy, where supply chain visibility is instant, and where cash flow stops being a guessing game.

The company sits at the intersection of procurement, invoice management, and working capital, connecting enterprises with their supplier networks. Rather than forcing companies to adopt yet another SaaS tool, Tradeshift embeds itself into the workflows that already exist—automating the grunt work of B2B commerce that still happens through email, spreadsheets, and PDF attachments.

Trodeshift's positioning is distinctly European: it understands the complexity of multi-regional supply chains, VAT compliance, and the regulatory layers that global companies navigate daily. While American fintech still obsesses over consumer-facing dashboards, Tradeshift has spent years building the unglamorous but essential plumbing that keeps enterprise trading flowing.

In an era where digital transformation is finally table stakes for large corporates, Tradeshift has become infrastructure—the kind that companies discover they can't function without. It's not the flashiest story in fintech, but it's one of the most resilient.

Founded 2010

Twikey

Financial Infrastructure🇧🇪 Belgium

Twikey sits at the intersection of payment orchestration and direct debit management, solving a problem most European fintechs have overlooked: how to automate recurring payments at scale. The platform enables businesses to collect payments via SEPA direct debit, card, and bank transfer—all orchestrated through a single API that feels less like legacy plumbing and more like modern infrastructure. Rather than forcing companies to juggle multiple payment rails and compliance frameworks, Twikey abstracts the complexity into intuitive workflows that handle mandate management, collections, and reconciliation with minimal friction. What sets Twikey apart is its obsession with the boring-but-critical work: ensuring compliance across jurisdictions, reducing failed payments through intelligent retry logic, and making recurring billing feel frictionless for both merchants and their customers. The company operates primarily in Western Europe but has built a platform designed to scale across the continent. In a landscape crowded with payment processors chasing flashy one-off transactions, Twikey has carved out territory in the unglamorous but lucrative recurring payment economy, where consistency and reliability matter far more than novelty. It's fintech infrastructure that doesn't try to be sexy—it just tries to work.

Founded 2013

Brite Payments

Fraud & Security🇸🇪 Sweden

Brite Payments operates in the unglamorous but essential middle of European payments infrastructure, solving the one problem every online merchant dreads: chargebacks and payment disputes. Rather than building another payment gateway or adding another layer to the stack, Brite focuses on the friction that happens after the transaction settles—when customers dispute charges, fraudsters claim they never authorized a payment, or acquirers demand evidence of legitimacy. The company automates the collection and management of transaction evidence, turning what used to be manual spreadsheet hell into a streamlined workflow. For e-commerce teams and payment processors alike, this means faster dispute resolution, lower chargeback rates, and fewer abandoned cases because the right documentation was never dug up in time. Where traditional payment providers treat disputes as a grudging afterthought, Brite has built the entire operation around winning them. The platform integrates with major payment gateways and acquirers, capturing data at the moment of transaction so that when a dispute lands, you're not scrambling to reconstruct what happened six months ago. In a market obsessed with growth and conversion, Brite focuses on the less sexy metric that actually protects margin: keeping more of the money you thought you earned. European merchants and their payment partners recognize the value immediately—this is not innovation theater, it's operational necessity.

Founded 2021

GoCardless

Embedded Finance🇬🇧 United Kingdom

GoCardless began as an Oxford University side project. Hiroki Takeuchi, Tom Blomfield, and Matt Robinson were trying to solve a mundane problem — splitting bills among housemates without the awkwardness of chasing people for cash — and kept running into the same wall: bank payments were inaccessible to developers, buried behind banking relationships and legacy infrastructure that assumed you were a large corporation. Their solution became a company. Blomfield would later leave to co-found Monzo, but Takeuchi stayed and built GoCardless into one of Europe's most significant payments businesses.

The product sits in an unglamorous but essential corner of the payments market: direct debit and bank-to-bank transfers for recurring payments. Card payments get most of the attention in fintech, but the plumbing of subscription billing, utility direct debits, and B2B invoice collection runs on bank payment rails — and those rails are fragmented across Europe in ways that make simple problems genuinely complex. GoCardless built the abstraction layer that makes it invisible. A SaaS company or utility in the UK, France, Germany, or Australia connects once to the GoCardless API and gains access to the local direct debit scheme in each market, without having to navigate each scheme independently.

The platform processes over $130 billion in payments annually for more than 100,000 businesses, including significant enterprise clients. Revenue reached £126.8 million in FY2024, up 38% year on year. The company has not yet reached sustained profitability — it reported a pre-tax loss of £34.5 million for FY2024, though the loss had halved from the prior year — and cut staff by around 20% as part of a restructuring aimed at reaching breakeven.

The most significant development in GoCardless's recent history is also the most consequential for its independence: in December 2025, Dutch payments company Mollie agreed to acquire GoCardless for approximately $1.1 billion. The deal, expected to complete in mid-2026 pending regulatory approval, brings together Mollie's card payment infrastructure for 250,000 SME merchants with GoCardless's bank payment and recurring billing capabilities — creating a combined entity serving over 350,000 businesses with a more complete European payments stack.

The acquisition values GoCardless below its $2.1 billion peak valuation from its 2022 Series G round, reflecting both the company's ongoing losses and the broader compression of fintech valuations since 2022. For Takeuchi — who returned to lead GoCardless through rapid international expansion after a cycling accident in 2015 left him paralysed from the waist down — the deal represents a substantial exit and a new chapter for the infrastructure he spent fourteen years building.

Founded 2011

Showing 12 of 21 companies. View all in the directory →