← All services

34 European companies

embedded payments

Embedded payments allow non-financial platforms to offer payment acceptance and disbursement natively within their own product, without directing users to a third-party processor. A marketplace can pay sellers directly from buyer payments; a software platform can collect subscription fees within its own interface. Embedded payments typically use payment facilitation infrastructure.

Typically offered by

European fintech companies offering embedded payments

Adyen

Embedded Finance🇳🇱 Netherlands

Pieter van der Does and Arnout Schuijff had already built and sold one payments company when they sat down in 2006 to start again. The result was Adyen — the name literally means "start over" in Surinamese — and the premise was simple: instead of stitching together the same fragmented payment infrastructure everyone else was using, they would build the whole thing themselves from scratch.

That decision, made in an Amsterdam office nearly two decades ago, is still the reason Adyen is different. Most payment companies are assemblers — they buy a gateway here, a processor there, bolt them together and hope for the best. Adyen owns its own technology stack end to end, which means a merchant integrating once gets access to card processing, local payment methods, point-of-sale terminals, and real-time settlement data through a single platform. No middle layers, no reconciliation headaches, no finger-pointing between vendors when something breaks.

The client list tells you everything about where Adyen sits in the market. McDonald's, Spotify, Microsoft, LVMH, H&M — these are companies with serious payment volumes and zero appetite for systems that don't work. Adyen became the default choice for enterprises that had outgrown the limitations of traditional payment stacks and needed something that could handle global scale without buckling.

Since going public on Euronext Amsterdam in 2018, Adyen has grown into one of Europe's most valuable technology companies, with around 4,300 employees across 23 countries and net revenue of just under €2 billion in 2024. It remains headquartered in Amsterdam and consistently profitable — a combination that's rarer in fintech than it should be.

For businesses that treat payments as infrastructure rather than an afterthought, Adyen is the benchmark everything else gets measured against.

Founded 2006

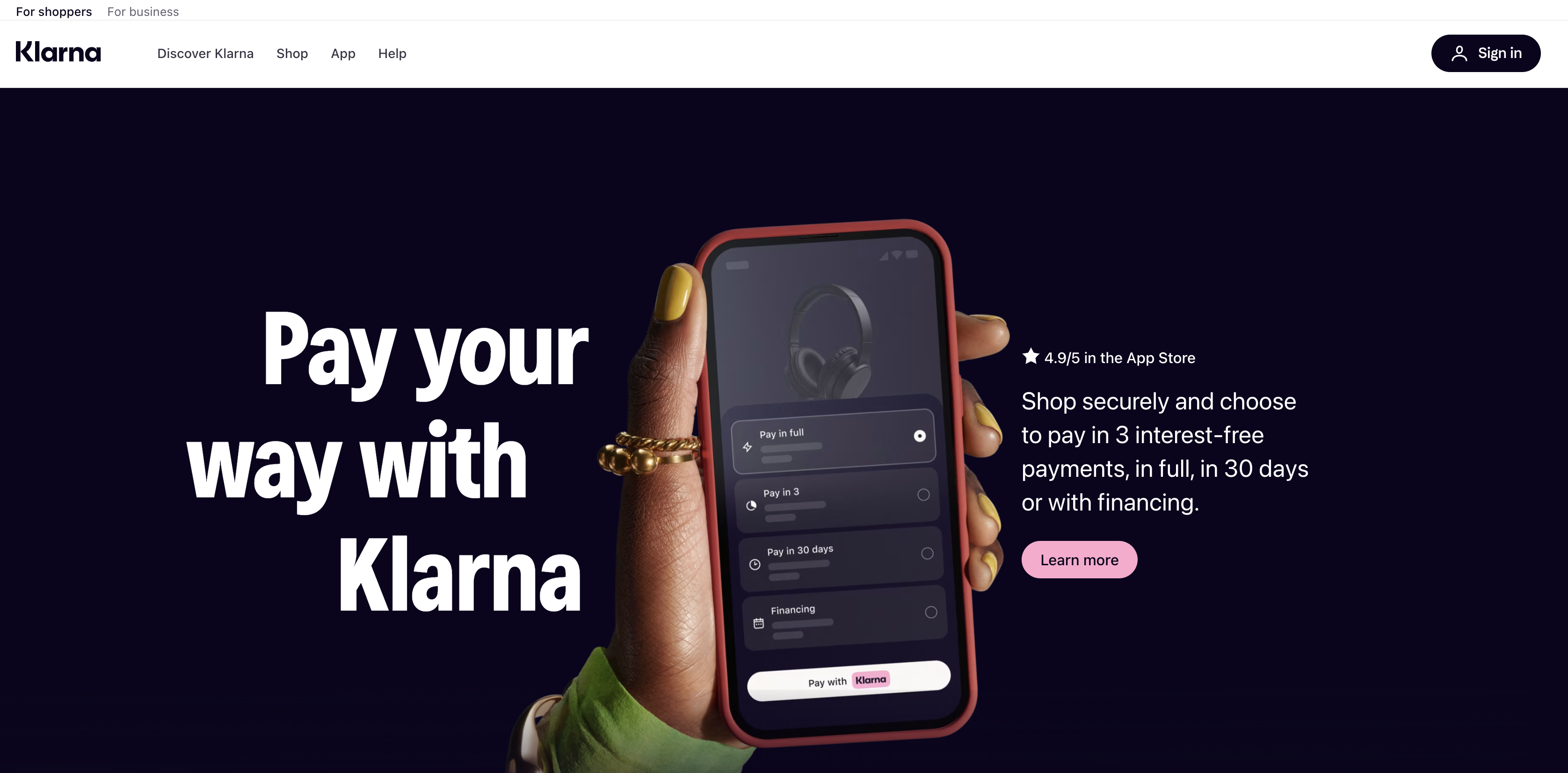

Klarna

Embedded Finance🇸🇪 Sweden

Three Stockholm School of Economics students pitched an idea at a university entrepreneurship competition in 2005: let shoppers receive goods before they pay, and put the credit risk on the merchant side. The pitch finished last. They built it anyway.

Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson launched what was originally called Kreditor, later renamed Klarna, and spent the next two decades turning that rejected idea into one of Europe's most recognised fintech brands. The core insight held up: millions of people would rather split a purchase into three instalments than reach for a credit card, and merchants would pay for the privilege of offering that option because it reduces cart abandonment and increases average order values.

Klarna grew from a Swedish checkout button into something considerably more complex. It now holds a banking licence in Sweden, offers savings accounts, issues its own card, and operates across more than 45 markets with around 93 million active consumers and 675,000 merchant partners at the end of 2024. The US, which Klarna entered in 2015, has become its largest market by revenue, a fact the company underlined by listing on the New York Stock Exchange in September 2025 under the ticker KLAR, raising $1.37 billion at IPO.

The financial trajectory has been bumpy. Klarna reported net income of $21 million in 2024, a return to profitability after a bruising 2022 that included an 85% valuation cut and significant layoffs that reduced headcount from over 7,000 to around 3,400. What survived the restructuring was a leaner company with $2.81 billion in revenue and a clearer strategic direction: AI. Klarna's partnership with OpenAI produced a customer service assistant it claims handles the equivalent of 700 full-time agents, and generative AI now manages roughly two-thirds of customer chats.

The honest assessment of where Klarna sits today: it's no longer purely a BNPL provider and it's not quite a bank. It's somewhere in between, a consumer finance platform that knows more about your shopping behaviour than your bank does, and is betting that's worth a lot.

Founded 2005

Tink

Embedded Finance🇸🇪 Sweden

Daniel Kjellén and Fredrik Hedberg didn't set out to build infrastructure. Tink started in Stockholm in 2012 as a consumer personal finance app — an attempt to give Swedish bank customers a cleaner view of their money across multiple accounts. It was a reasonable idea that ran into an unreasonable obstacle: getting reliable, consistent data out of European banks was extraordinarily hard. The technical problem turned out to be more interesting than the consumer product. In 2018 they pivoted, shifted focus entirely to the B2B layer, and started selling the very infrastructure they'd been forced to build for themselves.

That pivot proved prescient. The EU's PSD2 directive, which came into full effect in 2019, legally required banks to open their data to authorised third parties — creating the regulatory foundation that open banking platforms needed to operate at scale. Tink had spent years building exactly those bank connections. When the regulation arrived, the company was ready.

The platform Kjellén and Hedberg built connects to more than 3,400 banks and financial institutions across Europe, reaching over 250 million bank customers. Through a single API integration, banks, fintechs, and merchants can access aggregated account data, initiate payments directly from customer bank accounts, verify account ownership, and enrich transaction data — without maintaining their own connections to hundreds of separate banking systems with different technical standards and update schedules. Clients include Klarna, PayPal, NatWest, ABN AMRO, and BNP Paribas Fortis.

In March 2022, Visa completed the acquisition of Tink for €1.8 billion — one of the largest European fintech acquisitions of that year, and a clear signal of how seriously the global payments industry had come to take open banking infrastructure. Visa's strategic rationale was straightforward: it had failed to acquire Plaid, the US equivalent, after an antitrust challenge, and needed a European open banking capability. Tink gave it 500 employees, 18 European markets, and relationships with over 300 banks and fintechs built over a decade.

The founders stayed on as CEO and CTO through the transition, continuing to run Tink as a standalone Visa subsidiary from Stockholm. Both departed in 2025 — Kjellén and Hedberg announced they were building Freda, a new AI-driven legal and compliance technology startup, with the pair describing Tink as "now in better hands than ever." Francois Tornier, Visa's VP of Open Banking, took over as CEO. The product roadmap has continued under Visa ownership, including a 2024 expansion of Tink's open banking platform into the US market.

Founded 2012

Payhip

Embedded Finance🇬🇧 United Kingdom

Payhip lets creators and small businesses sell directly to their audience without the usual gatekeeping. It's a all-in-one commerce platform that handles digital products, physical goods, subscriptions, and memberships—essentially a Shopify alternative built for creators who want simplicity and fair pricing.

The platform lives in that sweet spot between marketplace and self-hosted store. You upload your product, set your price, share a link, and start selling. No approval process, no middleman deciding what you can or can't do. Payhip takes a percentage of each sale rather than charging upfront fees, which resonates with bootstrapped creators and solopreneurs who don't have predictable revenue yet.

What sets Payhip apart is its lightness. While traditional payment processors demand integration work and setup headaches, Payhip is deliberately frictionless—you can be live within minutes. It also gives sellers control over their own affiliate networks and customer relationships, something most platforms charge extra for or restrict.

In the crowded world of creator monetization tools, Payhip occupies the pragmatic middle: more powerful than a simple payment link, simpler than a full ecommerce platform, and designed specifically for people who want to sell without becoming a software engineer. It's quietly influential in how independent creators think about direct sales.

Founded 2010

Credimi

Embedded Finance🇮🇹 Italy

Credimi sits at the intersection of e-commerce and embedded finance, solving a problem that online retailers have largely ignored: making checkout friction disappear. Rather than forcing customers to choose between card payments and bank transfers, Credimi lets shoppers access buy-now-pay-later directly at the point of sale, turning the checkout moment into a financing decision rather than a payment one. The company essentially white-labels installment lending for merchants, handling everything from credit decisioning to collections behind the scenes.

What sets Credimi apart in a crowded BNPL market is its focus on the merchant relationship rather than the consumer one. While competitors chase customer loyalty through branded apps and direct marketing, Credimi takes a B2B approach, embedding its credit engine into partner payment flows and e-commerce platforms. This means retailers get better conversion rates without bearing the customer acquisition cost. The company operates across multiple European markets, particularly strong in the Nordics and DACH region, where fintech-native commerce has matured fastest.

In an industry obsessed with speed and simplicity, Credimi's real edge is its underwriting—it deploys machine learning to make instant credit decisions without the awkward friction of traditional lending. This isn't flashy consumer fintech; it's infrastructure. But it's exactly what online retailers need to compete in markets where BNPL has become table stakes.

Founded 2016

Solaris

Financial Infrastructure🇩🇪 Germany

Solaris is a Berlin-based fintech infrastructure platform that lets financial institutions and fintechs launch their own digital banking products without building tech from scratch. Rather than wrestling with legacy core banking systems, clients plug into Solaris's cloud-native API layer to issue cards, manage accounts, and process payments at speed.

The company operates in the shadows of most consumer apps—you won't see the Solaris logo in an app store—but its backbone runs through dozens of European fintechs, neobanks, and traditional financial institutions. Think of it as the plumbing that powers other people's banking ambitions.

Solaris dominates a specific niche: the BaaS (Banking-as-a-Service) and embedded finance layer for Europe. While competitors like Thought Machine and Temenos chase enterprise banking overhauls, Solaris stays focused on the modern fintech workflow. Its modular design appeals to companies that need speed and flexibility, not a 10-year implementation project.

In a market crowded with infrastructure plays, Solaris has become essential plumbing for European digital banking. It sits at the intersection of regulatory compliance, technical simplicity, and startup ambition—precisely where the next wave of European fintech is being built.

Founded 2015

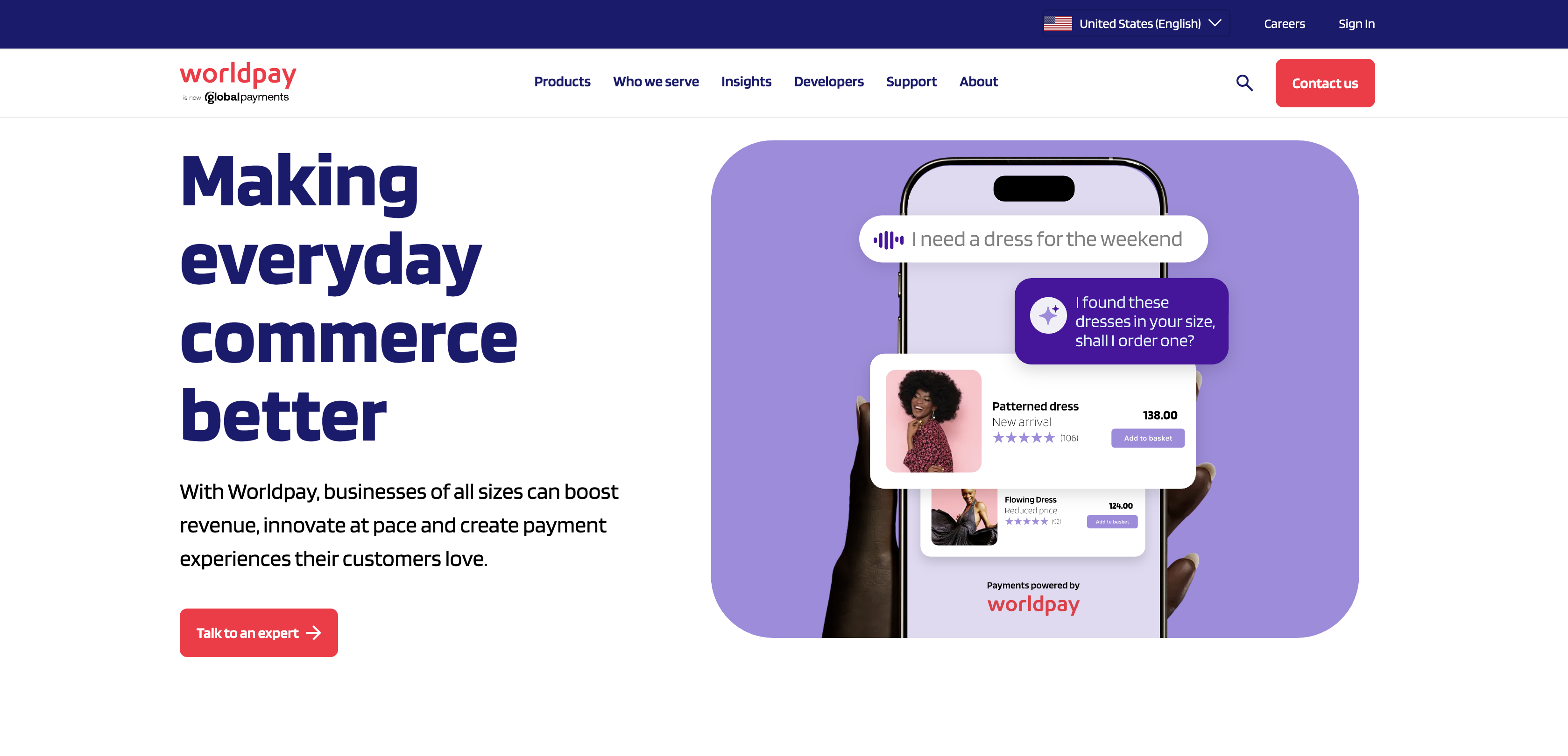

Worldpay

Embedded Finance🇬🇧 United Kingdom

Worldpay is one of Europe's most established payment infrastructure plays, handling transactions at the backbone of commerce across the continent. The company processes payments for retailers, e-commerce merchants, and financial institutions, sitting at the critical intersection where customer intent becomes settled value. Rather than chasing consumer attention, Worldpay operates in the plumbing layer—orchestrating card payments, merchant acquiring, and real-time settlement across borders with the quiet efficiency of infrastructure that's been stress-tested for decades. It's the kind of company most Europeans have never heard of but rely on every time they buy something online or in-store. What sets Worldpay apart in a crowded acquiring space is its scale and geographic reach. While newer fintech challengers chase flashy use cases, Worldpay manages the unglamorous work of connecting merchants to banks, processing disputes, and maintaining 99.9% uptime across payment rails that move billions. The company has evolved from a pure processor into a platform, offering tools for payment orchestration, subscription billing, and omnichannel commerce support. Its strength lies not in disruption but in resilience and reach—it powers payments for everything from corner shops to multinational retailers. In the European fintech ecosystem, Worldpay represents institutional financial infrastructure: old enough to be trusted, large enough to absorb regulatory change, and integrated deeply enough that replacing it would be prohibitively complex for most businesses.

Founded 1989

Rapyd

Embedded Finance🇬🇧 United Kingdom

Rapyd is a global fintech infrastructure company that lets businesses accept payments and move money across 170+ countries without needing local banking relationships. Rather than forcing companies to navigate fragmented payment ecosystems country by country, Rapyd abstracts away the complexity—providing a single API that connects to local payment methods, wallets, and bank accounts everywhere from Southeast Asia to Latin America. The platform handles the unglamorous but essential work: acquiring local licenses, managing compliance, and integrating with hyperlocal payment rails so a startup in Berlin can charge a customer in Lagos as easily as one in London. For merchants and platforms operating globally, this means ditching the spreadsheet of payment processors and compliance frameworks. Instead of cobbling together 15 different providers to cover emerging markets, they get one dashboard, one contract, one API. Rapyd has positioned itself as the plumbing for the next wave of global commerce—the infrastructure layer that makes it possible for any business to think globally from day one, not after they've scaled. In a fintech landscape dominated by Western-centric payment networks, Rapyd's bet on true geographic diversity and local payment methods feels like a deliberate counterweight, making it an essential piece of the infrastructure for companies serious about serving the rest of the world.

Founded 2018

Narvi

Embedded Finance🇫🇮 Finland

Narvi is a European fintech that simplifies embedded lending for e-commerce and marketplace platforms. Rather than forcing merchants to build lending infrastructure from scratch, Narvi handles the entire loan lifecycle—from origination through servicing—as a white-label API that integrates directly into checkout flows.

The company targets online retailers and marketplace operators who want to offer buy-now-pay-later and installment credit without the operational overhead of underwriting, collections, or compliance. Narvi handles credit decisions using proprietary scoring models and manages all regulatory requirements, while merchants simply embed a widget and capture incremental revenue.

In a market crowded with point-solution BNPL providers, Narvi positions itself as a full-stack lending partner rather than a payment mode. The company serves merchants across Europe and has built integrations with major e-commerce platforms, making it simpler for smaller retailers to compete with well-funded rivals on financing offerings.

Narvi represents a growing class of embedded finance infrastructure plays—companies enabling non-financial businesses to offer financial products without becoming financial institutions themselves. Its role is to abstract complexity and regulatory burden, letting merchants focus on customer experience and growth.

Founded 2020

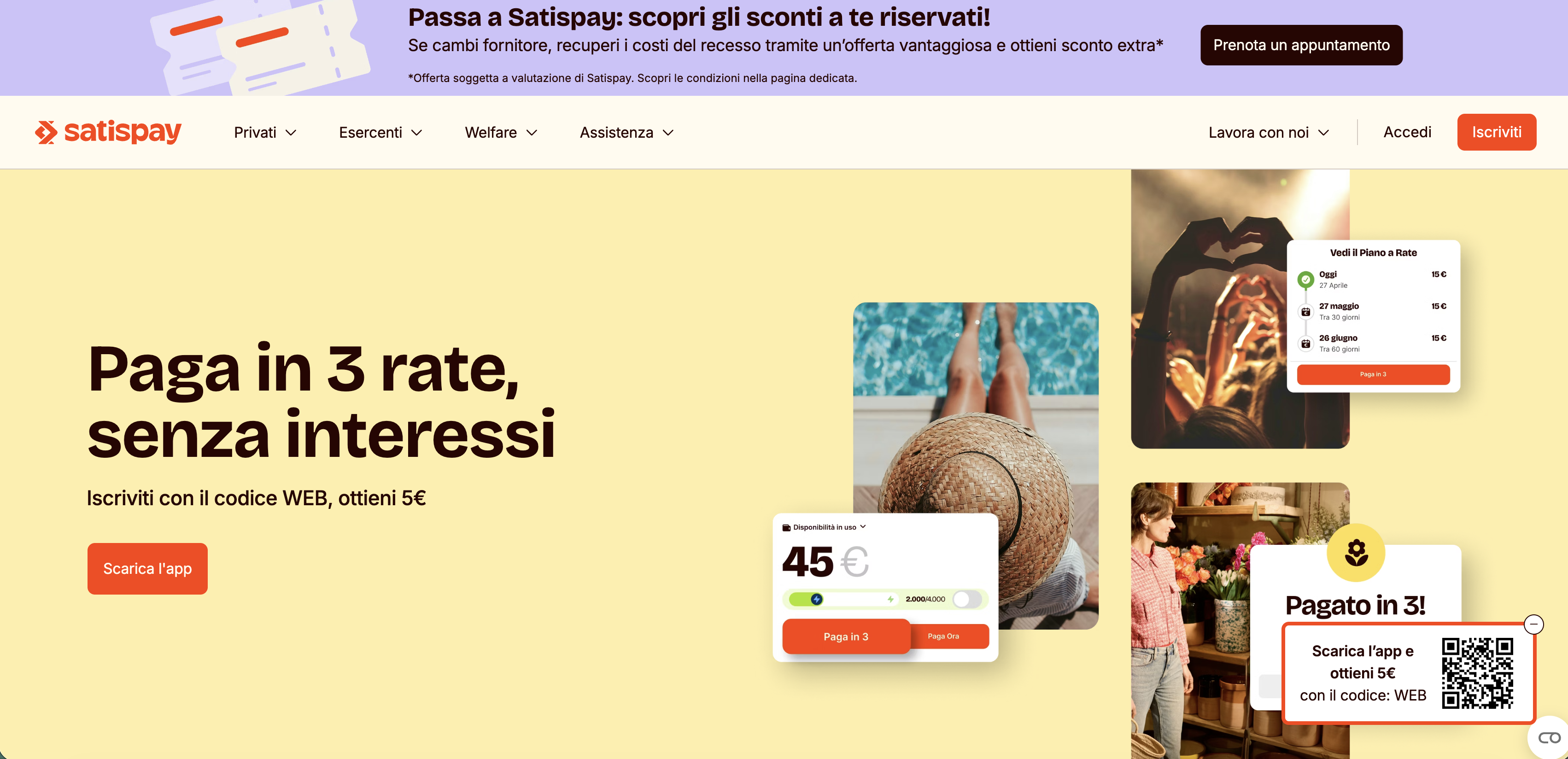

Satispay

Embedded Finance🇮🇹 Italy

Satispay cuts through the noise of payment processing by letting consumers pay directly from their bank account at checkout, skipping cards entirely. It's a mobile-first payment solution that arrived in Europe when digital wallets were becoming ubiquitous, but with a twist: it works offline and without requiring consumers to pre-load funds or enter card details repeatedly.

The company operates across Italy, France, Belgium, and other European markets, positioning itself as a bridge between traditional banking and modern commerce. Rather than competing head-to-head with card networks, Satispay enables merchants to accept payments through a lightweight app integration, with consumers confirming transactions via their phones in seconds.

What sets Satispay apart is its focus on simplicity and lower merchant costs compared to card acquiring. While payment gateways obsess over feature parity with every major card scheme, Satispay keeps the experience minimal: scan, tap, pay. It appeals to retailers tired of high interchange fees and consumers who prefer direct bank debits over recurring card charges.

In a fragmented European payments landscape, Satispay represents a pragmatic alternative to cards for in-store and online commerce, carving out space by solving a specific friction point rather than trying to be everything.

Founded 2013

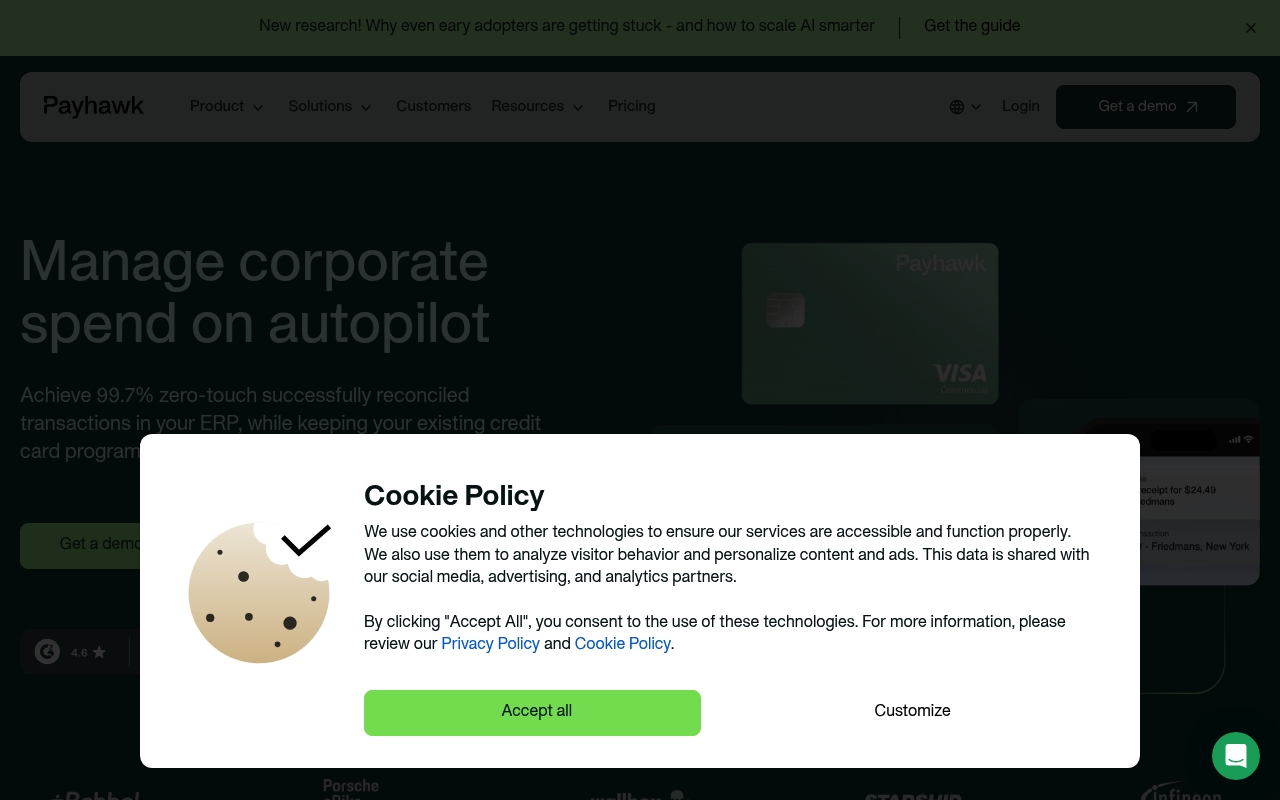

Payhawk

Embedded Finance🇧🇬 Bulgaria

Most companies still manage corporate spending the way they did a decade ago—expense reports, manual reconciliation, scattered receipts. Payhawk has built something radically simpler: a unified spending platform that gives finance teams complete visibility into every company transaction, from the moment it's authorized to the moment it's reconciled. The platform combines physical and virtual cards, automated expense management, and real-time spend controls in a single dashboard.

What sets Payhawk apart in the crowded corporate finance space is its refusal to compromise on user experience. Employees aren't fighting clunky interfaces or wrestling with legacy systems. Instead, they get an intuitive mobile app that feels like personal fintech, while finance teams gain the analytical firepower to actually manage policy, catch fraud, and optimize spending patterns. The company treats visibility not as a nice-to-have but as the foundation of control.

In Europe's SME and mid-market space, where most alternatives still rely on outdated card programs or disconnected software suites, Payhawk's integration of issuance, spend management, and analytics represents a meaningful shift. The company has quietly built something that enterprises have wanted for years: a spending platform that doesn't require compromise between employee experience and financial governance. For finance leaders tired of spreadsheets and reactive reporting, it's become the natural choice.

Founded 2019

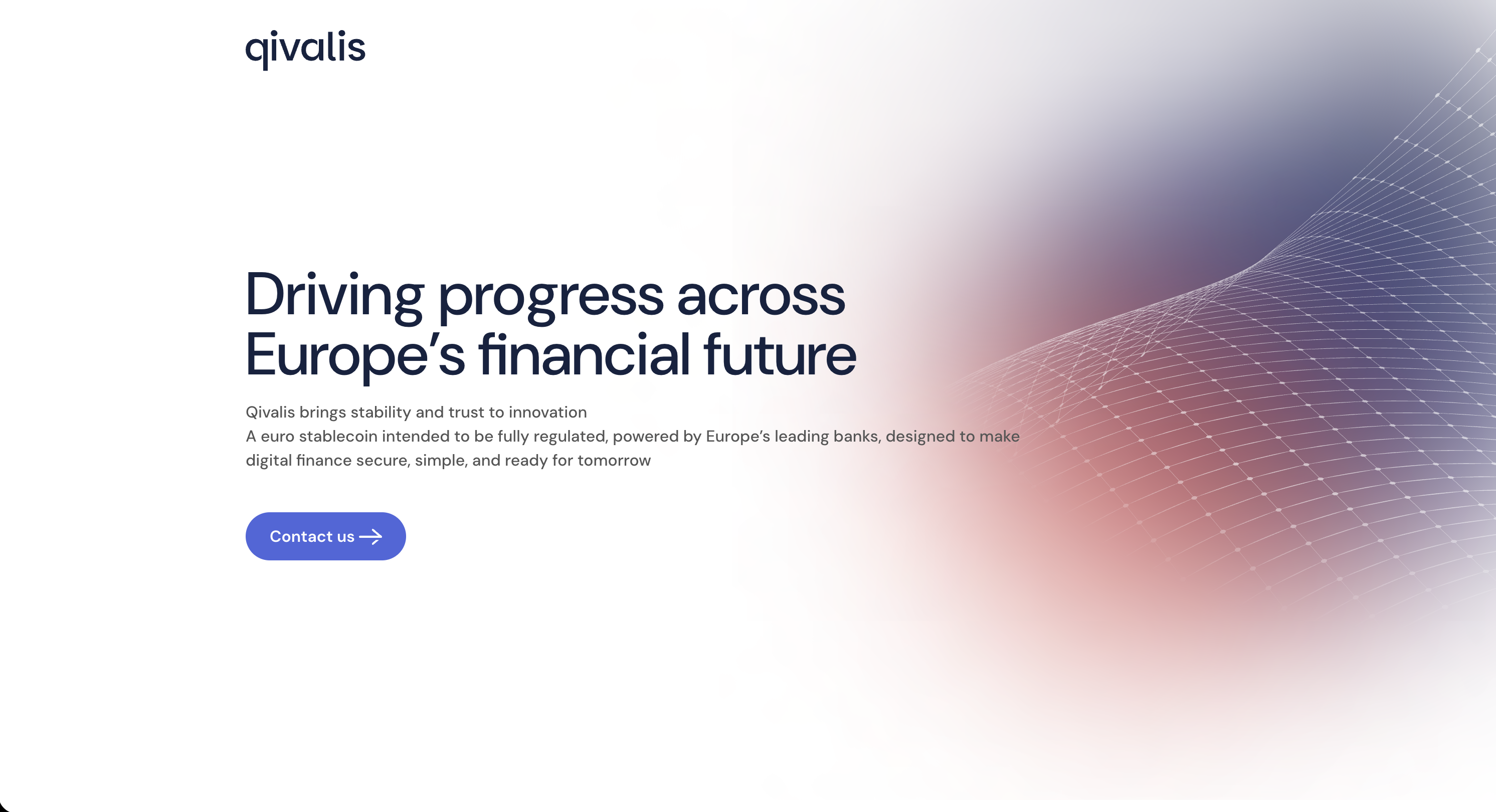

Qivalis

Payments🇳🇱 Netherlands

Europe has spent years talking about digital sovereignty in finance. Qivalis is what happens when that conversation turns into a stablecoin.

Based in Amsterdam, Qivalis is a bank-backed euro stablecoin initiative designed to bring regulated, euro-denominated money onto blockchain rails. The idea is simple but strategically loaded: create a digital euro asset that can move with the speed and programmability of crypto, while carrying the institutional trust of Europe’s banking sector. Its stablecoin is intended to be fully regulated, euro-backed, and built for secure digital payments and settlement.

What makes Qivalis different is not just that it wants to issue a euro stablecoin. Plenty of crypto-native companies have tried to make euro stablecoins happen, with limited traction. Qivalis enters the market from the other side: not as a crypto startup trying to win over banks, but as a bank-led consortium trying to build a shared piece of European digital financial infrastructure.

The consortium started with major European banks including ING, UniCredit, CaixaBank, Danske Bank, DekaBank, KBC, SEB, Raiffeisen Bank International and Banca Sella, with BNP Paribas later joining the group. Reuters reported that Qivalis was set up in Amsterdam and is applying for an Electronic Money Institution licence from De Nederlandsche Bank, with a planned launch in the second half of 2026.

Since then, the project has become larger. Reuters reported on 20 May 2026 that the Qivalis consortium had expanded to 37 financial institutions across 15 countries, with additions including ABN AMRO, Rabobank, Sabadell, Bankinter, Bank of Ireland, Handelsbanken and Nordea. That scale matters because stablecoins are only useful if people and institutions actually use them. A euro stablecoin backed by one bank is a product. A euro stablecoin backed by dozens of banks starts to look more like infrastructure.

Qivalis is aimed at a very specific problem: Europe does not want the future of digital money to be dominated only by dollar stablecoins. Today’s stablecoin market is heavily shaped by US dollar-denominated tokens such as USDT and USDC, issued by companies like Tether and Circle. The Financial Times reported that Qivalis is trying to create a euro-based alternative for use cases such as cross-border payments and atomic settlement, rather than replacing domestic payment systems.

That distinction is important. Qivalis is not trying to become the next payment app for buying coffee in Amsterdam. It is closer to a wholesale and institutional digital money layer: a euro token that can be used for blockchain-based settlement, digital asset transactions, cross-border value movement and future tokenised finance. In that sense, Qivalis sits somewhere between banking infrastructure, stablecoins, payments and capital markets modernisation.

The company is also part of the bigger MiCA story. Europe’s Markets in Crypto-Assets Regulation created a clearer framework for regulated crypto-assets and stablecoins, which gives bank-led initiatives a more credible path into the market. Qivalis is pursuing Dutch Central Bank authorisation as an Electronic Money Institution and has positioned itself as a MiCA-compliant euro stablecoin issuer.

Its leadership also signals the bridge it is trying to build. Reuters reported that Jan-Oliver Sell, formerly of Coinbase Germany, is CEO; ING digital asset lead Floris Lugt is CFO; and former NatWest chair Howard Davies is chair. That mix tells the story neatly: crypto market experience, bank digital asset expertise and old-school financial governance in one company.

Qivalis feels different from most fintechs because it is not selling rebellion. It is not trying to make banks look outdated. It is trying to give banks a way to stay relevant in a financial system where tokenisation, blockchain settlement and programmable money are becoming harder to ignore. The pitch is not “move fast and break finance.” It is more European than that: move carefully, regulate properly, and build shared rails before someone else owns the market.

The opportunity is clear. If tokenised assets, stablecoin settlement and on-chain financial markets keep growing, Europe will need a trusted euro-denominated settlement asset. A bank-backed stablecoin could help reduce reliance on dollar tokens, support faster cross-border settlement and give institutions a regulated way to use blockchain-based money without depending entirely on crypto-native issuers.

The challenge is just as clear. Stablecoins need liquidity, distribution, trust and actual use cases. Euro stablecoins have historically struggled to gain meaningful adoption compared with dollar stablecoins. Qivalis will need to prove that banks can move fast enough, coordinate effectively and create a product that institutions actually prefer over existing alternatives.

That is what makes Qivalis interesting. It is not just another stablecoin project. It is a test of whether European banks can build shared digital infrastructure before the market is fully captured by non-European players.

Qivalis is Europe’s banking sector trying to answer a difficult question: if money is moving on-chain, who issues the euro that moves with it?

Founded 2025

Showing 12 of 34 companies. View all in the directory →