← All services

15 European companies

fraud detection

Fraud detection analyses transactions, account events, and user behaviour in real time to identify potentially fraudulent activity before it results in financial loss. Modern fraud detection combines machine learning models trained on large datasets with rules-based logic for known fraud patterns, returning risk scores alongside the signals driving them to enable efficient analyst review and continuous model improvement.

Typically offered by

European fintech companies offering fraud detection

Payhawk

Embedded Finance🇧🇬 Bulgaria

Most companies still manage corporate spending the way they did a decade ago—expense reports, manual reconciliation, scattered receipts. Payhawk has built something radically simpler: a unified spending platform that gives finance teams complete visibility into every company transaction, from the moment it's authorized to the moment it's reconciled. The platform combines physical and virtual cards, automated expense management, and real-time spend controls in a single dashboard.

What sets Payhawk apart in the crowded corporate finance space is its refusal to compromise on user experience. Employees aren't fighting clunky interfaces or wrestling with legacy systems. Instead, they get an intuitive mobile app that feels like personal fintech, while finance teams gain the analytical firepower to actually manage policy, catch fraud, and optimize spending patterns. The company treats visibility not as a nice-to-have but as the foundation of control.

In Europe's SME and mid-market space, where most alternatives still rely on outdated card programs or disconnected software suites, Payhawk's integration of issuance, spend management, and analytics represents a meaningful shift. The company has quietly built something that enterprises have wanted for years: a spending platform that doesn't require compromise between employee experience and financial governance. For finance leaders tired of spreadsheets and reactive reporting, it's become the natural choice.

Founded 2019

Hawk

Fraud & Security🇩🇪 Germany

Hawk brings machine learning firepower to financial crime detection, sitting at the intersection of compliance and computational intelligence. Rather than relying on static rule sets that miss novel fraud patterns, Hawk deploys adaptive algorithms that learn from transaction behavior in real time, catching what traditional systems let slip through the cracks. The platform ingests transaction data across multiple channels—payments, transfers, accounts—and surfaces suspicious activity before it becomes a problem. For banks and fintechs drowning in false positives from legacy systems, Hawk promises a different approach: smarter, faster, less noise. Its technology sits on the boundary between compliance necessity and operational efficiency, helping institutions detect actual threats rather than gaming alert thresholds. In an environment where financial crime is increasingly sophisticated and regulatory pressure unrelenting, Hawk positions itself as the thinking alternative to checkbox compliance, offering institutions a genuine competitive edge in the race to stay ahead of bad actors.

Founded 2019

Ravelin

Fraud & Security🇬🇧 United Kingdom

Ravelin is a fraud prevention and risk intelligence platform built for the modern payment landscape. Rather than relying on outdated blacklists and rule engines, the company uses behavioral analytics and machine learning to distinguish legitimate transactions from fraudulent ones in real time.

The platform sits between merchants and payment processors, analyzing transaction patterns, user behavior, and contextual signals to catch fraud before it hits the books. Ravelin's approach acknowledges a fundamental tension in fintech: overly aggressive fraud screening kills conversions, while loose controls breed chargebacks. The company's API-first architecture means it integrates directly into checkout flows without requiring merchants to rebuild their payments infrastructure.

What sets Ravelin apart is its focus on the nuance between fraud risk and business risk. Many competitors offer binary accept-or-decline decisions; Ravelin surfaces risk scores and behavioral indicators, letting merchants make informed decisions about which transactions to challenge, approve, or send to manual review. This flexibility matters especially for high-value or unusual transactions where false positives hurt revenue.

Ravelin operates primarily in the B2B space, serving mid-market and enterprise merchants across e-commerce, travel, and fintech. The company competes in a crowded fraud detection market dominated by established players, but gains ground through superior machine learning models and a merchant-centric product philosophy. As payment volumes continue to surge across Europe and digital fraud becomes increasingly sophisticated, Ravelin's technology sits at a critical chokepoint in the transaction flow.

Founded 2014

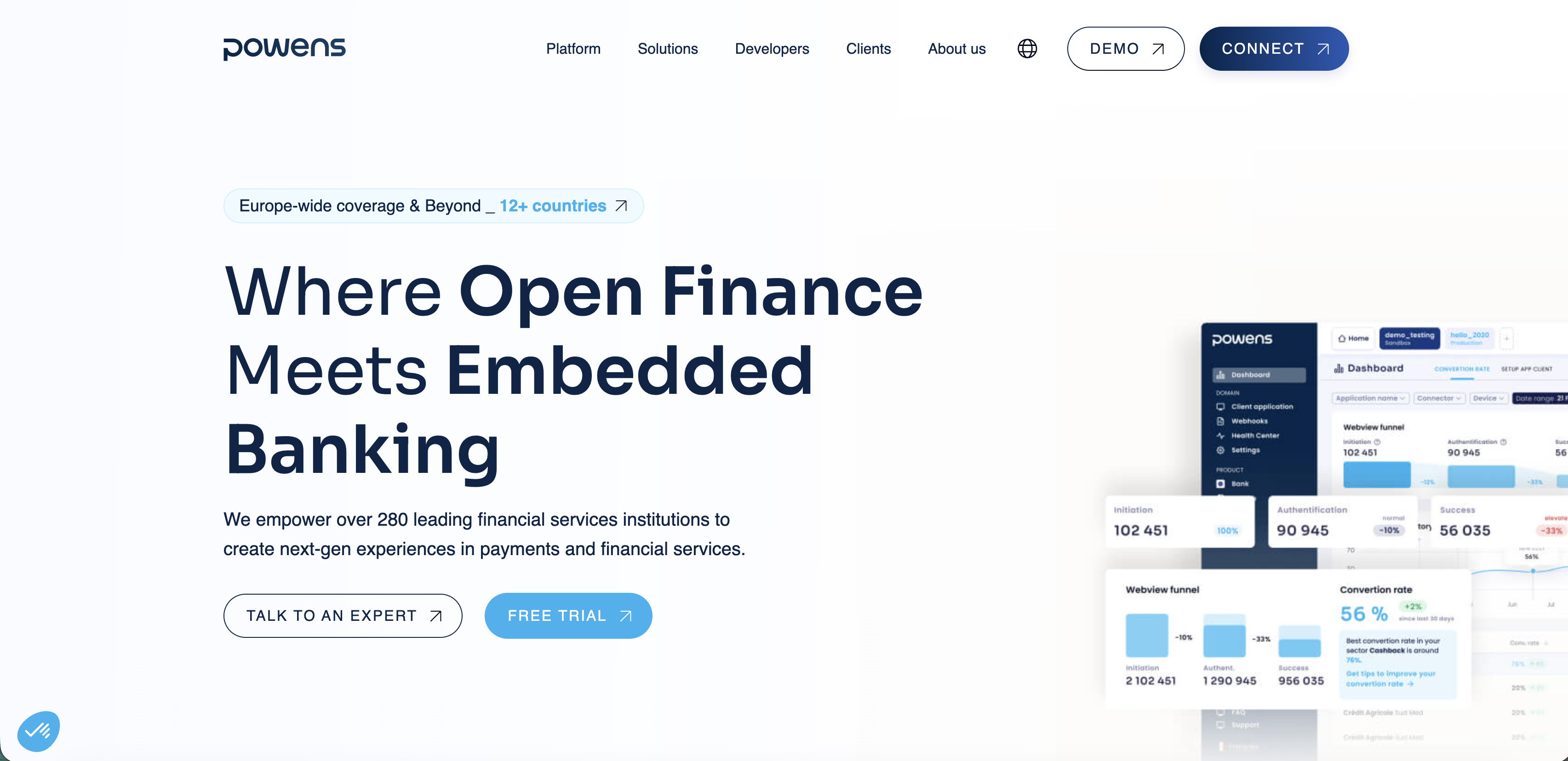

Powens

Fraud & Security🇫🇷 France

Powens sits at the intersection of open banking and financial data aggregation, helping European fintechs and traditional banks make sense of the fragmented payment and account landscape. Rather than building another me-too aggregator, the company positions itself as the connective tissue between institutions and the data they need to move capital efficiently and securely. Their platform ingests transaction data, payment initiation flows, and account information from thousands of financial institutions across Europe, surfacing clean, standardized intelligence to power lending decisions, fraud detection, and embedded finance experiences. What sets Powens apart is its focus on the continental European market—where open banking adoption is uneven and legacy banking infrastructure still dominates. While UK and US aggregators have enjoyed first-mover advantage, Powens saw an opportunity to build native expertise in Germany, France, Spain, and Benelux, where regulatory tailwinds and fragmented banking systems created genuine demand. The company works with both consumer-facing fintechs and institutional clients, meaning they've learned to navigate the messy reality of building infrastructure that talks to both sleek fintech apps and stuffy corporate banking platforms. This dual-sided approach has become their competitive moat—they understand both the user experience expectations of modern fintech and the compliance complexity of traditional finance. In the broader European fintech stack, Powens functions as a critical middleware layer, solving the unglamorous but essential problem of data connectivity that powers everything downstream—from embedded lending to fraud prevention to wealth management.

Founded 2015

Curve

Payments🇬🇧 United Kingdom

Curve sits at the intersection of payment practicality and modern banking convenience. The London-based fintech lets you consolidate all your cards and bank accounts into a single card and app, eliminating the friction of managing multiple payment methods across Europe. Rather than forcing you to choose between a credit card, debit card, and travel account, Curve sits on top of your existing financial life and intelligently routes transactions, offering real-time currency conversion, fraud protection, and transaction insights in one unified interface.

What makes Curve different is its approach to payment routing—the app learns your spending patterns and automatically decides which underlying card to use based on rewards, exchange rates, and cashback opportunities. You control the rules, but Curve does the heavy lifting. The platform supports cards and accounts from traditional banks, but also increasingly integrates with newer fintech providers, making it a natural gateway for anyone juggling multiple financial relationships. It's not a neobank replacement, but rather a layer above your existing banking infrastructure that makes managing money across borders and multiple institutions feel seamless. In the wider fintech ecosystem, Curve represents a growing category of unified banking experiences that acknowledge the reality of modern financial life—most people don't want one bank, they want all their banks working in sync.

Founded 2015

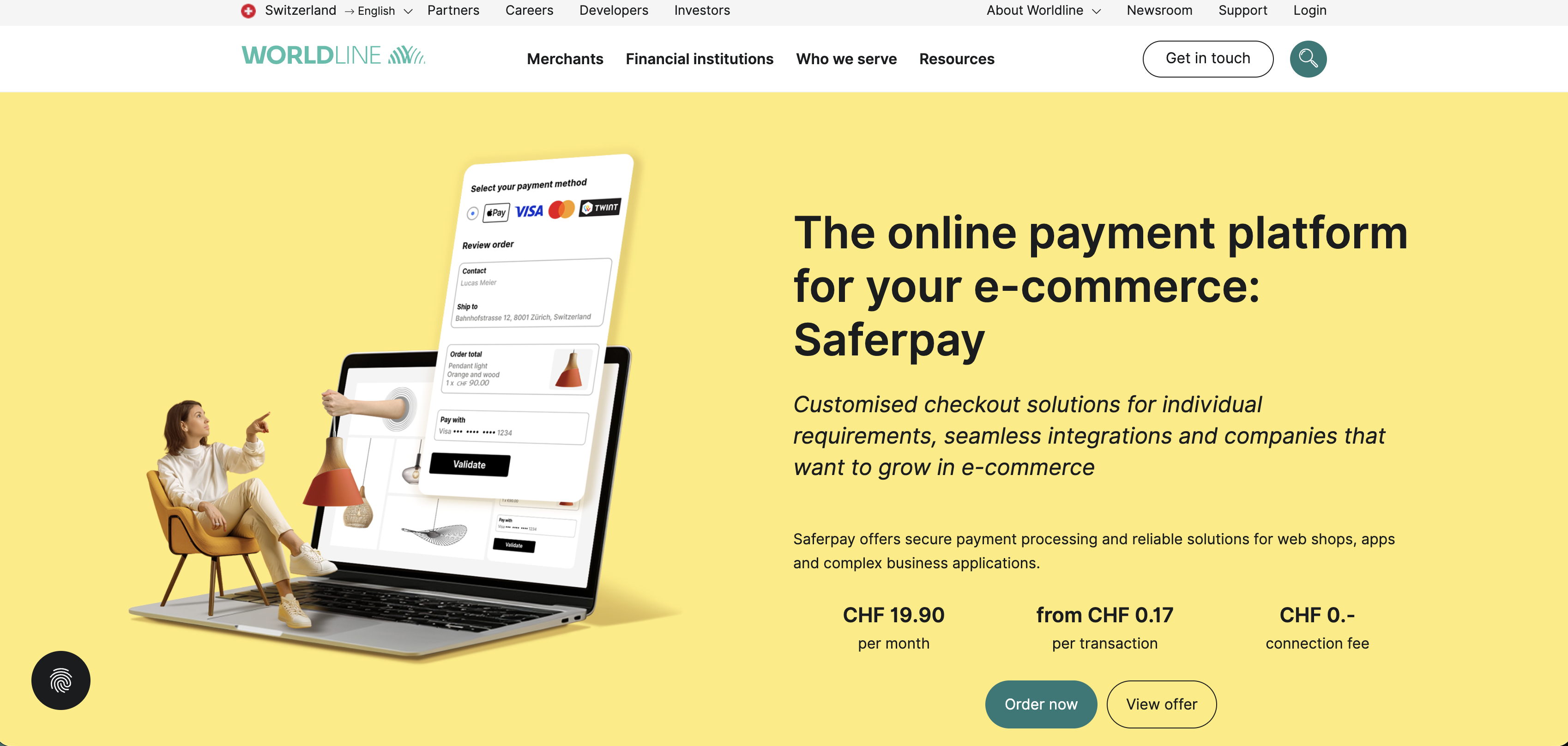

Saferpay

Payments🇨🇭 Switzerland

Saferpay is a Swiss payment solution that handles the unglamorous but critical work of processing card transactions safely. It sits between merchants and their customers, quietly managing the complexity of international payments, fraud prevention, and regulatory compliance that most people never think about until something goes wrong. The company has been around since the late 1990s, which in fintech terms makes it practically ancient—yet it continues to evolve rather than rest on its reputation. What sets Saferpay apart is its focus on security-first architecture. While newer payment players chase trends, Saferpay maintains obsessive attention to PCI DSS compliance, tokenization, and advanced fraud detection. It handles everything from simple card processing to complex multi-currency transactions across Europe and beyond. The platform is particularly strong in the DACH region and other heavily regulated European markets where compliance isn't negotiable. Saferpay operates as a B2B2C business, serving merchants directly and through integrations with banking partners and payment aggregators. Rather than trying to be everything to everyone, it's positioned itself as the reliable backbone for businesses that can't afford payment failures. For European merchants operating internationally or those in highly regulated industries, Saferpay offers a mature, battle-tested alternative to flashier payment startups.

Founded 1998

Brite Payments

Fraud & Security🇸🇪 Sweden

Brite Payments operates in the unglamorous but essential middle of European payments infrastructure, solving the one problem every online merchant dreads: chargebacks and payment disputes. Rather than building another payment gateway or adding another layer to the stack, Brite focuses on the friction that happens after the transaction settles—when customers dispute charges, fraudsters claim they never authorized a payment, or acquirers demand evidence of legitimacy. The company automates the collection and management of transaction evidence, turning what used to be manual spreadsheet hell into a streamlined workflow. For e-commerce teams and payment processors alike, this means faster dispute resolution, lower chargeback rates, and fewer abandoned cases because the right documentation was never dug up in time. Where traditional payment providers treat disputes as a grudging afterthought, Brite has built the entire operation around winning them. The platform integrates with major payment gateways and acquirers, capturing data at the moment of transaction so that when a dispute lands, you're not scrambling to reconstruct what happened six months ago. In a market obsessed with growth and conversion, Brite focuses on the less sexy metric that actually protects margin: keeping more of the money you thought you earned. European merchants and their payment partners recognize the value immediately—this is not innovation theater, it's operational necessity.

Founded 2021

ICEPAY

Payments🇳🇱 Netherlands

ICEPAY is a Dutch payment processor that handles everything from card transactions to alternative payment methods across Europe. The company powers checkout experiences for thousands of merchants, managing the complex plumbing of converting customer intent into settled funds. What sets ICEPAY apart is its focus on European merchants—particularly mid-market businesses that need more than a one-size-fits-all gateway. The platform bundles payment processing with risk management, offering fraud detection and chargeback protection alongside the standard card rails. It's built for merchants who want flexibility without complexity, handling both online and in-store payments through a unified infrastructure. ICEPAY operates in a crowded space where most competitors either stay focused on pure payment processing or sprawl into adjacent services. The company positions itself as the European alternative to global juggernauts, with deeper understanding of regional payment preferences and compliance requirements. It's a pragmatic choice for businesses scaling across multiple European markets—less startup energy, more mature operational backbone. In the broader fintech ecosystem, ICEPAY represents the unglamorous but essential layer: the infrastructure that makes European commerce work behind the scenes.

Founded 2007

Payconiq

Financial Infrastructure🇧🇪 Belgium

Payconiq operates at the intersection of mobile payments and merchant acquiring, building infrastructure that lets small shops and big retailers alike accept payments however their customers want to pay. Founded in Belgium and now operating across multiple European markets, the company has positioned itself as a bridge between the traditional card rails and the newer world of instant payments and digital wallets. Rather than forcing merchants into choosing between payment methods, Payconiq orchestrates them all—cards, mobile wallets, bank transfers—through a single integration. This unified approach appeals to retailers who are tired of managing separate terminals and reconciling multiple payment channels. What sets Payconiq apart in a crowded acquiring space is its focus on simplicity without sacrificing functionality. The platform handles the technical complexity—tokenization, fraud detection, settlement—so merchants can focus on running their business. It's built for the realities of modern retail: smaller merchants need affordable entry points, larger chains need API flexibility, and everyone wants visibility into their transactions. Payconiq's strategy reflects a deeper shift in European payments: the move away from hardware-centric acquiring toward software-first solutions that treat payment acceptance as a service rather than a product. In an industry where incumbent acquirers still dominate through sheer distribution, Payconiq represents the challenger mentality—stripping away legacy complexity and rebuilding payment acceptance from first principles.

Founded 2013

Autopay

Payments🇵🇱 Poland

Autopay operates in Poland's fast-moving payments ecosystem as a fintech that has quietly become essential infrastructure for merchants who need more than just a gateway. Previously known as Blue Media, the company built its reputation over years as a trusted Polish payments operator before evolving into the Autopay brand. That history matters: Autopay is not a new entrant trying to break into the market, but an established infrastructure player with deep roots in Poland’s digital payments landscape.

The company processes transactions, manages payment flows, and provides the plumbing that lets businesses accept card payments without drowning in complexity or integration headaches.

What separates Autopay from the crowded Polish payments space is its focus on the mid-market merchant rather than chasing everyone at once. It builds for businesses that care about conversion rates, fraud management, and the ability to retry failed transactions intelligently. The platform handles card acquiring, payment routing, and reconciliation—the unglamorous but crucial work that determines whether a transaction succeeds or fails.

In a market where international players dominate, Autopay remains distinctly local. It understands Polish regulations, speaks the language of regional merchants, and moves faster than the legacy banking infrastructure that still controls much of the country's payment flows. That proximity to its customers has become its competitive advantage.

Autopay represents a particular kind of European fintech: not the venture-backed darling chasing scale at any cost, but the pragmatic operator solving real problems for real businesses. Its Blue Media origins give it the credibility of an incumbent, while the Autopay brand reflects its push toward a more modern, consumer- and merchant-facing payments identity. It's the kind of infrastructure play that rarely makes headlines but quietly powers the Polish e-commerce boom.

Founded 1999

Shift4

Embedded Finance🇲🇹 Malta

Shift4 is a payments infrastructure company that processes transactions for some of the world's largest businesses—hotels, travel agencies, e-commerce platforms, and entertainment venues. Rather than building from scratch, Shift4 operates as the backbone that other payment systems rely on, handling everything from card processing to alternative payment methods across multiple continents and currencies. The company processes over $200 billion annually, quietly powering payment flows for thousands of merchants who may never see its name but absolutely depend on its reliability. What sets Shift4 apart in a crowded payment ecosystem is its operational focus. While many fintech companies obsess over consumer-facing innovation, Shift4 builds enterprise-grade infrastructure designed for resilience, speed, and compliance at scale. Its platform handles the complexity that makes most companies cringe: high-volume verticals like hospitality and gaming, multi-currency settlements, regulatory variance across jurisdictions, and the kind of uptime demands that simply cannot tolerate failure. The company has grown through both organic expansion and acquisitions—notably bringing PayMaker into its fold to expand its European footprint and capabilities. For businesses that process millions of transactions daily, Shift4 isn't sexy. It's indispensable. It represents the unglamorous but critical layer of fintech infrastructure that enables everyone else to function.

Founded 1999

Nethone

Fraud & Security🇵🇱 Poland

Fraud detection and prevention used to be reactive—companies would build rule engines and hope for the best, watching transactions after they happened. Nethone inverts that. The platform spots fraudsters before they strike, using behavioral analytics and device intelligence to identify bad actors in real time across payments, lending, and marketplaces. It's not just rule-based flagging; Nethone learns from every interaction, continuously adapting to new fraud tactics as they emerge.

The company serves mid-market and enterprise clients across Europe, particularly in Poland and the broader Central European market, where it's become trusted infrastructure for preventing losses. Unlike generic fraud tools that rely on blacklists and static rules, Nethone combines machine learning with behavioral signals—how someone moves their mouse, types their password, navigates your app—to build a detailed risk picture. This approach catches both account takeovers and credential stuffing before legitimate users even realize something's wrong.

In a market crowded with legacy fraud solutions and newer point tools, Nethone stands apart through device-centric intelligence and a focus on reducing false positives. Most fraud platforms block too much; Nethone aims for precision. For fintech companies, lenders, and payment networks that need fraud prevention without friction, it offers a middle ground between being too permissive and too paranoid. It's become a standard choice for European fintechs building trust at scale.

Founded 2012

Showing 12 of 15 companies. View all in the directory →