← All services

12 European companies

risk scoring

Risk scoring assigns quantitative risk assessments to customers, transactions, or counterparties based on data signals — credit risk scores for lending decisions, fraud risk scores for payment authorisation, or compliance risk scores for AML purposes. Good risk scoring reduces both bad outcomes (missed risks) and false positives (legitimate customers or transactions incorrectly flagged), directly affecting financial performance and customer experience.

Typically offered by

European fintech companies offering risk scoring

Hawk

Fraud & Security🇩🇪 Germany

Hawk brings machine learning firepower to financial crime detection, sitting at the intersection of compliance and computational intelligence. Rather than relying on static rule sets that miss novel fraud patterns, Hawk deploys adaptive algorithms that learn from transaction behavior in real time, catching what traditional systems let slip through the cracks. The platform ingests transaction data across multiple channels—payments, transfers, accounts—and surfaces suspicious activity before it becomes a problem. For banks and fintechs drowning in false positives from legacy systems, Hawk promises a different approach: smarter, faster, less noise. Its technology sits on the boundary between compliance necessity and operational efficiency, helping institutions detect actual threats rather than gaming alert thresholds. In an environment where financial crime is increasingly sophisticated and regulatory pressure unrelenting, Hawk positions itself as the thinking alternative to checkbox compliance, offering institutions a genuine competitive edge in the race to stay ahead of bad actors.

Founded 2019

Fenergo

Financial Infrastructure🇮🇪 Ireland

Compliance has long been the unglamorous backroom operation of financial services—heavy, expensive, and often painfully slow. Fenergo flips that script by turning regulatory friction into operational advantage. The Dublin-based software company automates the gruelling work of onboarding clients, managing their data, and staying compliant with an ever-shifting maze of regulations. What banks and investment firms once treated as a cost center, Fenergo repositions as competitive edge.

At its core, Fenergo is a digital client lifecycle management platform. It consolidates onboarding, KYC, AML screening, sanctions checks, and ongoing regulatory monitoring into a single, integrated workflow. Rather than legacy institutions juggling multiple point solutions and manual spreadsheet cultures, Fenergo orchestrates the entire client journey—from first interaction through renewal—in a single intelligent system. The software ingests regulatory data, flags anomalies, and automates approvals where rules allow, freeing compliance teams to focus on judgment calls that actually require human expertise.

What sets Fenergo apart in a crowded RegTech space is its disciplined focus on the regulated financial institution as customer, not the consumer. While plenty of fintechs chase sexy consumer-facing applications, Fenergo has built deep, sticky relationships with banks, asset managers, and brokers who need sophisticated, audit-proof compliance infrastructure. It operates at institutional scale—handling millions of client records, complex entity hierarchies, and regulatory jurisdictions spanning continents.

In an era when regulatory fines have become nine-figure line items and reputational damage from compliance failures can tank a bank's stock price, Fenergo sits at the nerve center of institutional risk management. It's not the flashy side of fintech, but it's arguably the most essential.

Founded 2008

Credolab

Identity & KYC🇳🇱 Netherlands

Credit decisions in markets without comprehensive credit bureau coverage have always been hard. The traditional underwriting model relies on credit history, income verification, and identity documents that significant portions of the global population either don't have or can't easily produce. Credolab was founded in 2016 with operations across Asia and Europe to address that gap with an unconventional data source — smartphone metadata. Its platform analyses behavioural patterns from a mobile device — without accessing personal content — to generate credit scores for consumers who have no traditional credit history. The data points are surprisingly predictive: how someone manages their phone storage, the pattern of their app usage, the regularity of their device behaviour all correlate with credit risk in ways that traditional underwriting misses. Credolab serves lenders, telcos, and digital platforms across emerging markets where credit bureau coverage is thin and the demand for digital credit is growing rapidly. In the alternative credit data landscape, where companies are competing to find the data sources that will define the next generation of underwriting, Credolab's behavioural smartphone approach is one of the more distinctive — and one that addresses a genuinely large unmet need in markets where billions of people remain credit-invisible to traditional financial systems.

Founded 2016

Pliant

RegTech🇩🇪 Germany

Pliant is a compliance automation platform built for financial services firms that are tired of drowning in spreadsheets and manual processes. Rather than layering another point solution onto an already fragmented tech stack, Pliant unifies risk, compliance, and audit workflows into a single operating system. The platform handles the tedious work—continuous monitoring, policy enforcement, evidence collection, regulatory reporting—that currently consumes entire compliance teams and slows down growth.

Founded 2020

Credit Benchmark

Financial Infrastructure🇬🇧 United Kingdom

Credit Benchmark sits at the intersection of market transparency and institutional risk management. Founded to solve a specific problem—banks and asset managers couldn't easily benchmark their credit exposures against the broader market—it's evolved into a critical infrastructure play in the institutional credit space. The platform aggregates anonymized credit opinions from major financial institutions, creating a real-time view of how the world's largest investors see credit risk. Rather than relying on traditional ratings agencies or proprietary models, Credit Benchmark lets institutions see how their views stack up against peers, identify outliers, and stress-test assumptions across thousands of corporates and sovereigns. This crowdsourced intelligence has become essential for risk committees, portfolio managers, and regulators navigating an increasingly complex credit landscape. The company operates quietly but with significant reach—used by central banks, pension funds, and major corporates to understand systemic credit risk. In a world where traditional credit signals lag reality, Credit Benchmark offers something rare: a real-time consensus view built on the opinions of sophisticated investors who have real money at stake. It's infrastructure for an industry that desperately needed transparency on how credit risk is actually perceived, not how it's officially rated.

Founded 2011

PayTweak

Financial Infrastructure🇫🇷 France

PayTweak sits at the intersection of payment orchestration and real-time optimization—a platform that lets merchants intelligently route transactions across multiple payment methods and acquirers to maximize approval rates and cut costs in a single motion. Rather than accepting whatever approval your default processor gives you, PayTweak continuously tests and learns which payment paths work best for each customer, adjusting strategy on the fly. It's less about adding another layer of complexity and more about turning payment infrastructure from a fixed cost into a dynamic, self-improving system.

The platform addresses a real friction point in European e-commerce: merchants have multiple acquirers and payment methods sitting in their tech stack, but no smart way to orchestrate them. PayTweak automates that decision-making, using machine learning to predict which combination of processor, method, and authentication approach will succeed for any given transaction—all while minimizing fraud losses and fees. It works especially well for cross-border merchants, subscription businesses, and high-volume retailers where even fractional improvements in approval rates translate to significant revenue recovery.

Compared to traditional payment gateways, PayTweak moves past the static integration model. Rather than forcing merchants to choose one acquirer or stick with preset rules, it treats the entire payment ecosystem as a resource to be optimized in real time. This approach resonates particularly in European markets where regulatory fragmentation and multiple payment rails mean no single processor can do it all equally well.

PayTweak represents the emerging category of intelligent payment infrastructure—less about moving money, more about making sure every eligible transaction succeeds. For merchants tired of leaving approval and revenue on the table, it's a meaningful efficiency play.

Founded 2019

Klear Lending

RegTech🇧🇬 Bulgaria

Klear Lending is a London-based fintech that automates credit decisions for alternative lenders and financial institutions across Europe. The company has built a machine learning platform that cuts through the complexity of underwriting—replacing outdated credit scoring with algorithmic assessment that learns from lender-specific data and performance patterns. Rather than forcing institutions into rigid scoring boxes, Klear's technology adapts to how different lenders actually price risk, meaning a borrower rejected by one algorithm might be approved by another using the same underlying data.

The platform processes loan applications in seconds, reducing the manual review work that traditionally chokes alternative lending operations. Its clients range from peer-to-peer platforms and buy-now-pay-later startups to traditional bank-owned lending divisions looking to modernize their decision engines. Klear sits at the intersection of infrastructure and risk—not quite a lender itself, but the invisible scoring layer that powers decisions across Europe's fragmented credit market.

In a landscape where underwriting talent is expensive and credit models age quickly, Klear's bet is that dynamic, data-driven decisioning will eventually become table stakes for any lender serious about competitive underwriting. The company has steadily built a niche serving institutions that can't build these capabilities themselves but can't afford to leave money on the table with overly conservative approval rates either.

Founded 2016

New10

Lending🇳🇱 Netherlands

New10 is a Amsterdam-based fintech platform that has carved out a distinct niche in SME lending by combining AI-driven credit assessment with a marketplace model. Rather than traditional bank underwriting, the company uses machine learning to evaluate small business creditworthiness, then connects approved borrowers with a network of institutional lenders—a model that sidesteps the gatekeeping that keeps many SMEs shut out of conventional finance. The platform processes loan requests from companies across Europe, particularly in the Netherlands, offering faster turnaround and more transparent terms than legacy banking. What sets New10 apart is its infrastructure-first approach: it's built less as a consumer app and more as a B2B2C system that other platforms and financial institutions can integrate into their own offerings. The company has positioned itself as the connective tissue between borrowers desperate for working capital and investors hungry for diversified credit exposure. In a landscape where SME lending remains fragmented and inefficient, New10 functions as both platform and accelerant, democratizing access while simultaneously proving that algorithmic credit assessment can work at scale across European markets.

Founded 2015

Eilla AI

RegTech🇪🇪 Estonia

AI for finance has moved quickly from experimental capability to genuine product opportunity, and the early movers building specialised AI tools for financial workflows have a chance to define how the technology integrates with the way finance professionals actually work. Eilla AI was founded in Tallinn in 2022 to apply large language models and AI agents to investment research and financial analysis workflows. Its platform helps investment professionals — analysts, portfolio managers, due diligence teams — process the enormous volume of unstructured information that financial decisions depend on: company filings, transcripts, market reports, news, alternative data sources. The product targets the specific bottleneck that AI is well-suited to address: the time-consuming work of synthesising large amounts of text into the structured insights that human analysts need to make decisions. The Estonian fintech ecosystem has produced a disproportionate number of internationally relevant companies, and Eilla represents the AI-native generation of European fintech infrastructure. In the broader landscape of AI applied to finance, where every major institution is experimenting with internal AI tools, specialist external platforms like Eilla have to demonstrate that their product depth and ongoing model development justify their use over generalist AI tools that everyone has access to.

Founded 2022

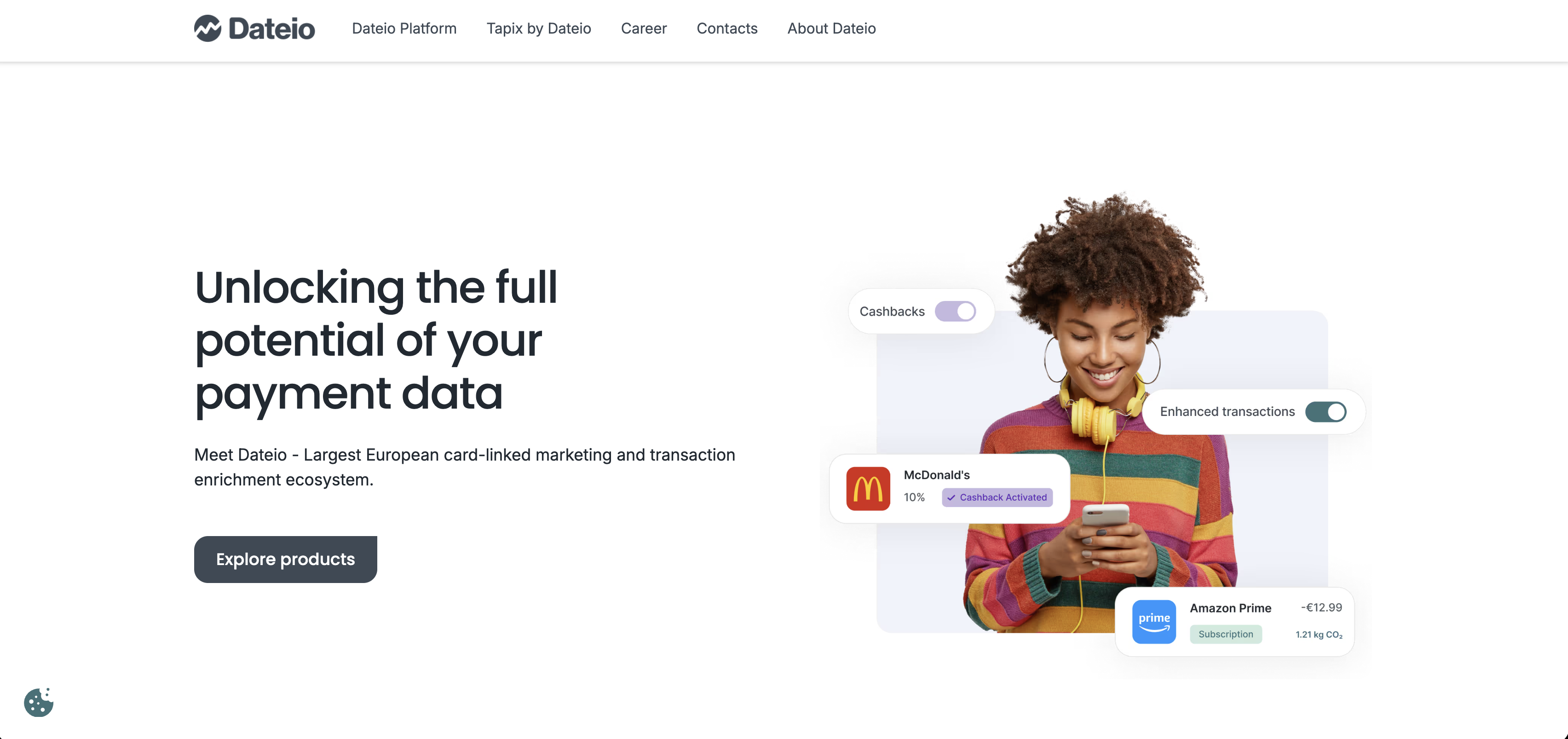

Dateio

Financial Infrastructure🇪🇪 Estonia

Dateio is a European open banking platform that sits at the intersection of data and credit. The company aggregates financial data from multiple banks and institutions across Europe, then applies machine learning to unlock lending decisions and financial insights that traditional scoring can't capture. Unlike legacy credit bureaus, Dateio builds its models on real transaction history and behavioral patterns, not just loan defaults and payment records.

The company positions itself as a data partner for fintechs, banks, and lenders who need smarter underwriting. Rather than building consumer-facing products, Dateio focuses on B2B infrastructure—providing APIs that other companies plug into to understand customer creditworthiness in real time. This approach means Dateio operates in the quieter, more valuable layer of fintech: the plumbing that powers better decisions.

In a market crowded with credit score providers and ID verification vendors, Dateio stands out by going deeper into the data layer. Most competitors offer point solutions; Dateio aggregates, normalizes, and analyzes transaction flows across borders. That matters in Europe, where fragmented banking systems and privacy rules have made cross-border financial data unusually hard to access. For lenders tired of crude risk models, Dateio offers a more granular, behavior-based alternative that reflects how Europeans actually spend and save money.

The company represents a broader shift in European fintech toward infrastructure and data intelligence, rather than consumer apps. As regulation tightens and competition intensifies in lending, better data becomes the primary competitive advantage. Dateio operates in that space.

Founded 2017

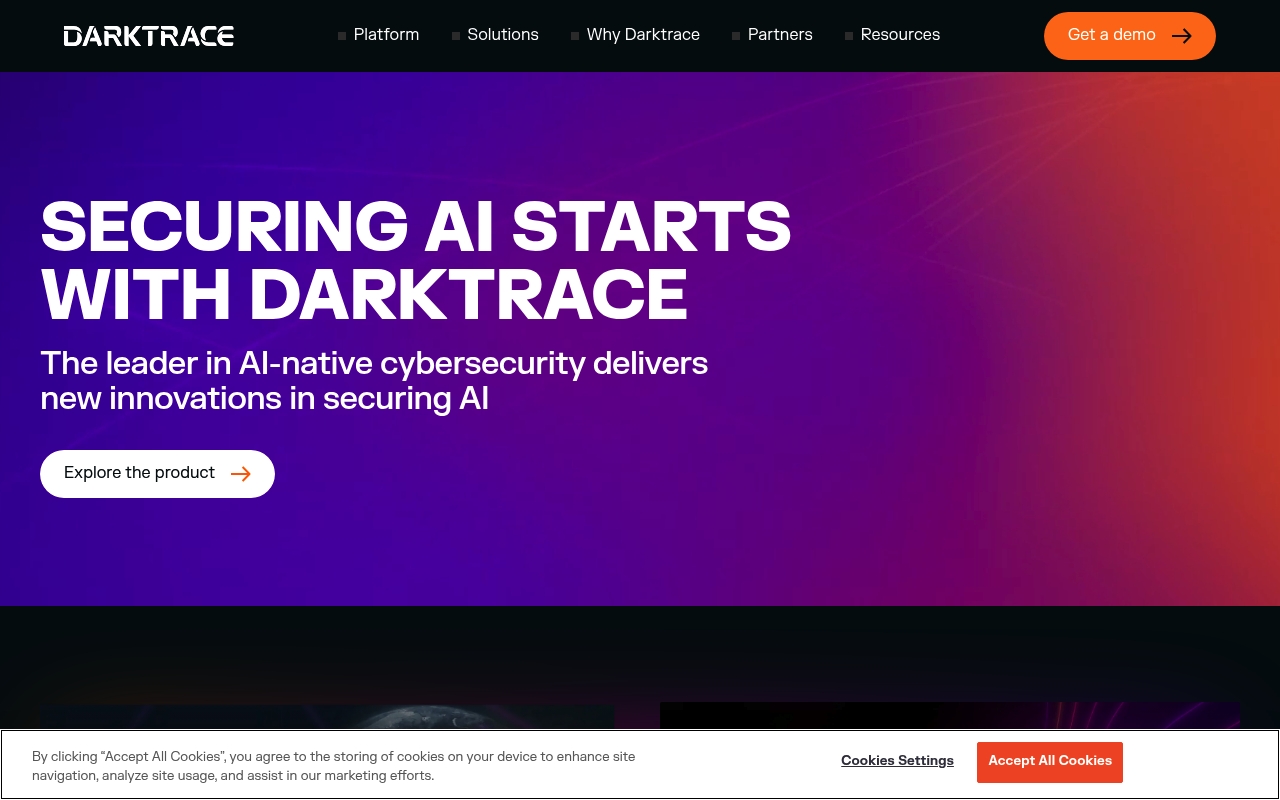

Darktrace

Fraud & Security🇬🇧 United Kingdom

Darktrace is a British artificial intelligence company that weaponizes self-learning algorithms against cyber threats in real-time. Founded in 2013 by mathematicians and former Cambridge scholars, it operates at the intersection of enterprise security and AI—teaching machines to recognize the fingerprint of normal behavior, then catching deviation before damage happens.

The platform works differently from traditional cybersecurity. Rather than relying on threat signatures or static rules, Darktrace's core AI engine learns what "normal" looks like inside an organization's network—every user, device, and data flow. When something deviates fundamentally from that baseline, it triggers. This approach has made it essential infrastructure for financial institutions, healthcare operators, and multinational enterprises handling sensitive data.

What separates Darktrace from older guard security providers is speed and scope. While competitors still operate on vulnerability lists and known-bad signatures, Darktrace catches unknown threats in motion. It's become the gold standard for enterprises that treat security as an ongoing conversation with AI, not a compliance checkbox.

In the broader fintech and enterprise tech landscape, Darktrace represents a generation of AI-native security companies that don't just react to attacks—they learn, predict, and evolve. For financial services and regulated industries, this autonomous intelligence has become non-negotiable.

Founded 2013

Strise

Fraud & Security🇳🇴 Norway

Strise is an AI-powered ESG risk platform built for institutional investors tired of spreadsheet-based due diligence. Instead of relying on lagging ESG ratings from traditional providers, Strise uses machine learning to surface real-time supply chain risks, labor violations, and environmental incidents that actually move portfolio companies. The platform aggregates unstructured data from thousands of sources—regulatory filings, news, satellite imagery, worker reports—and turns it into actionable risk scores that investors can trade on.

What sets Strise apart is its speed and granularity. While legacy ESG platforms deliver quarterly updates, Strise refreshes daily. It catches supply chain disruptions before they hit earnings calls and identifies geopolitical risks buried in subsidiary networks. The system learns from private investor feedback, getting smarter about what matters for specific asset classes and investment theses.

Strise positions itself as the anti-Morningstar approach to ESG—less about moral messaging, more about financial materiality. It's built for asset managers, insurers, and institutional investors who need ESG intelligence that moves faster than the news cycle. In an era where traditional ESG ratings are increasingly criticized for opacity and misalignment with actual risk, Strise offers a data-driven alternative that translates ESG into portfolio language: risk-adjusted returns.

Founded 2019