← All services

16 European companies

savings automation

Savings automation moves money into savings accounts, investment accounts, or savings goals automatically based on predefined rules — scheduled transfers, round-ups on transactions, or percentage-of-income rules. By removing the need for ongoing conscious decisions, savings automation dramatically improves the consistency of saving behaviour and helps users accumulate savings they would not have set aside manually.

Typically offered by

European fintech companies offering savings automation

Monzo

Wealth🇬🇧 United Kingdom

The founding team that built Monzo had all worked together before — at Starling Bank, another challenger bank startup that didn't survive its internal conflicts. Tom Blomfield, Gary Dolman, Jonas Huckestein, Jason Bates, and Paul Rippon left Starling together in 2015 and started again. The product they built was initially a prepaid card — a coral-coloured piece of plastic that became one of the most recognisable objects in British fintech — before becoming a fully licensed current account in 2017.

The early user community was unusual for a bank. Monzo ran community forums, published public blog posts about its engineering decisions, and invited customers into beta programmes for new features. When it broke the world record for the fastest crowdfunding raise in 2016 — £1 million in 96 seconds — it wasn't just raising money; it was building an identity. People felt ownership of the product in a way that no high street bank had ever managed to create. That emotional connection became a genuine competitive advantage.

The product has matured considerably since then. Monzo now offers current accounts, joint accounts, savings pots, personal loans, overdrafts, and investment products, all wrapped in the real-time notification experience and transaction categorisation that made its early reputation. Revenue reached £1.23 billion in 2024, up 40% year on year, with net income of £95 million — the second consecutive year of profitability after years of growth-first losses. The customer base reached 12.1 million by end of 2024, making Monzo the UK's largest digital bank by customer count. Customer deposits stood at £16.6 billion.

The business is still private — the much-discussed IPO has not yet happened, and internal disagreements about where to list (the former CEO TS Anil favoured the US, the board preferred London) contributed to Anil's departure in October 2025. Diana Layfield took over as CEO with a mandate focused on international expansion before any public listing. The company is valued at approximately $5.9 billion following a 2024 secondary sale backed by Alphabet's GIC and StepStone.

In December 2025 Monzo announced it had agreed to acquire Habito, the digital mortgage broker, pending regulatory approval — a move that extends the product into one of the last major financial products it didn't yet offer. With 3,821 employees and a loan book growing rapidly, Monzo has evolved from a prepaid card experiment into a bank with genuine scale and a growing claim on being the primary financial account for a generation of UK consumers.

Founded 2015

Pockit

Digital Banking🇬🇧 United Kingdom

Pockit is a mobile-first financial platform designed for people who've been locked out of traditional banking. Rather than chasing the affluent, Pockit focuses on the underbanked—those without access to a current account, credit history, or the documentation banks demand. The app serves as a genuine alternative to brick-and-mortar banking, offering digital accounts, card payments, and money management tools entirely through your phone.

What sets Pockit apart is its commitment to financial inclusion without the gatekeeping. You don't need a credit score or payslip to open an account. Instead, the platform builds trust through usage patterns and behavioral data, creating pathways for people traditionally rejected by high street banks. This shifts the relationship from one of suspicion to one of genuine access.

The company operates across the UK and Europe, proving that underserved segments aren't just a niche—they're a substantial market. Pockit's mission is radical in its simplicity: banking shouldn't require jumping through hoops or having the right background. It's a challenger in the truest sense, not because it offers flashy features, but because it solves a real problem for millions of people who simply want to participate in the financial system.

Founded 2015

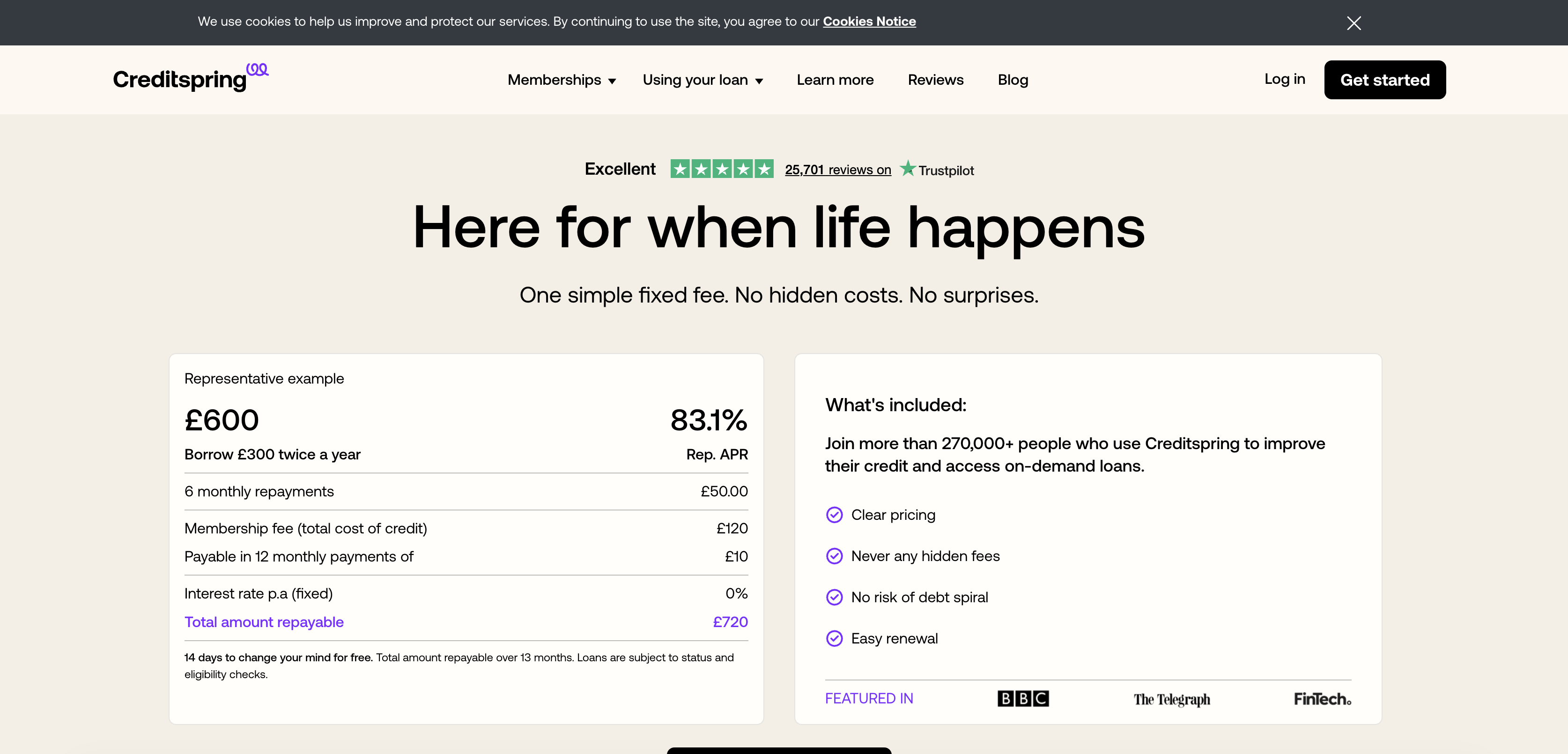

Credit Spring

Lending🇬🇧 United Kingdom

Credit Spring is a UK-based fintech that treats financial distress like a health problem—one that deserves diagnosis and treatment, not judgment. Rather than simply offering credit, the company combines short-term loans with financial coaching and debt management tools, recognizing that a quick cash injection without context is often a band-aid on a bigger problem. The platform helps borrowers understand their spending patterns and rebuild their financial foundation, not just patch a temporary shortfall. It's a provocative stance in a market crowded with BNPL and payday lenders that rarely ask why someone needs money in the first place. Credit Spring targets people in the credit-vulnerable segment—those with poor or limited credit histories who'd normally be shut out of mainstream lending. Instead of algorithmic rejection, the company uses alternative data and behavioral insights to assess creditworthiness beyond traditional scoring. For users, this means faster access to reasonable credit at transparent rates. For the market, it signals a shift toward lending that acknowledges financial fragility as a temporary state, not a permanent condition. The company represents a broader move within fintech to attach financial wellness services to credit products, treating lending as an entry point to deeper financial health rather than a transaction.

Founded 2016

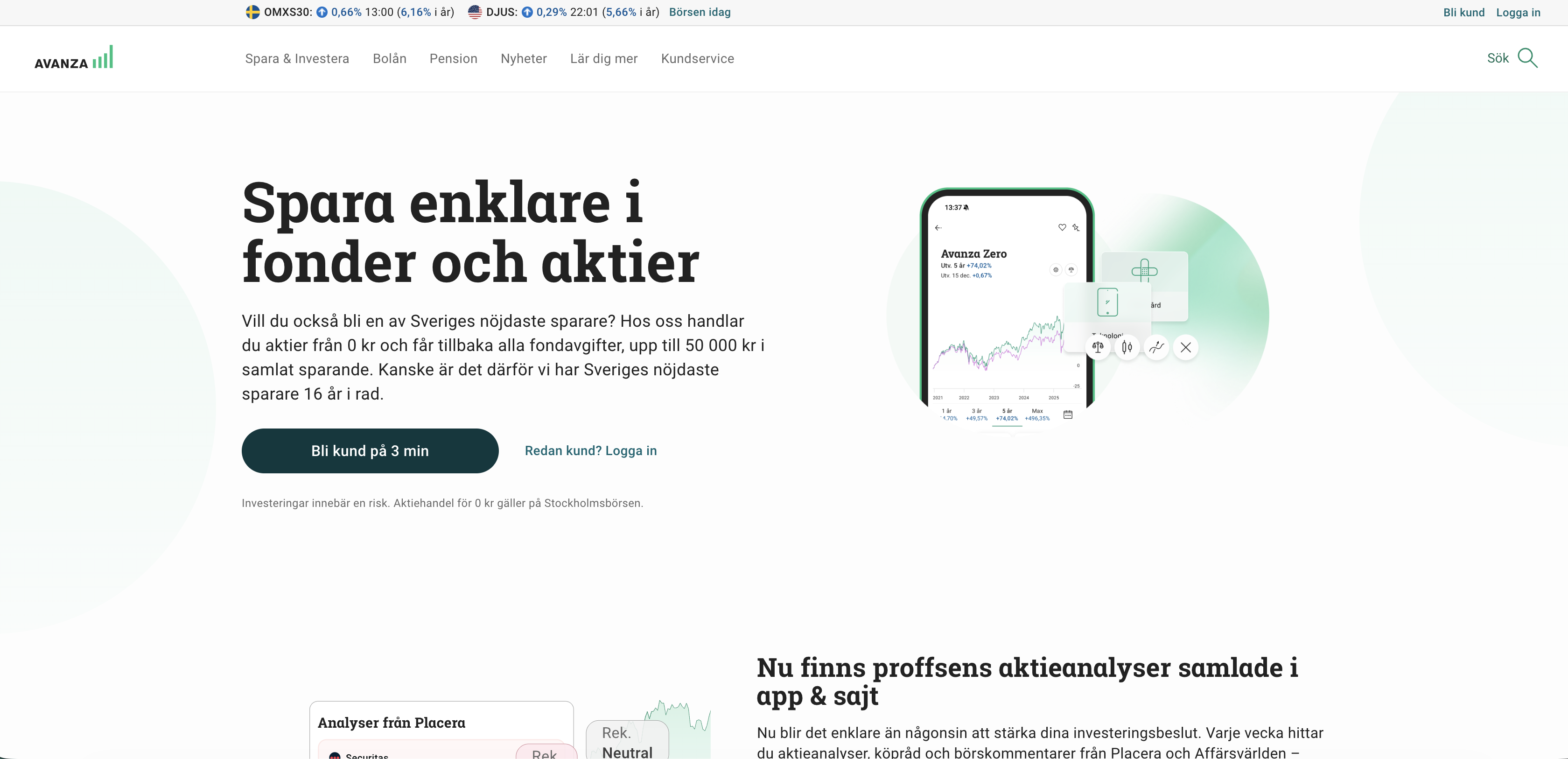

Avanza

Wealth🇸🇪 Sweden

Avanza is Sweden's largest independent online brokerage, a no-frills investment platform that democratized stock trading for Swedish retail investors two decades ago. What started as a scrappy alternative to traditional banks has become the go-to app for millennials and Gen Z who want to trade, invest, and save without paying legacy banking fees. The platform strips away unnecessary complexity—no advisors, no jargon, just direct market access at transparent prices. Avanza operates in that interesting middle ground between a neobank and a pure trading platform. It offers savings accounts, pension accounts, and investment accounts with a sharp focus on user experience and low costs. The company has built a cultural following in Sweden, becoming almost synonymous with retail investing for a generation that views traditional brokers as relics. Beyond just equities and funds, Avanza has expanded into savings products, retirement planning, and financial education—positioning itself as a genuine financial companion rather than just a transaction layer. Its dominance in the Nordic market reflects a broader European shift toward direct-to-consumer investment platforms that compete on transparency, speed, and mobile-first design. Avanza exemplifies how fintech can win by doing one thing exceptionally well and then expanding thoughtfully into adjacent categories. The company's influence extends beyond Sweden into a broader shift in how younger Europeans think about investing: without gatekeepers, without unnecessary fees, and entirely on their own terms.

Founded 1999

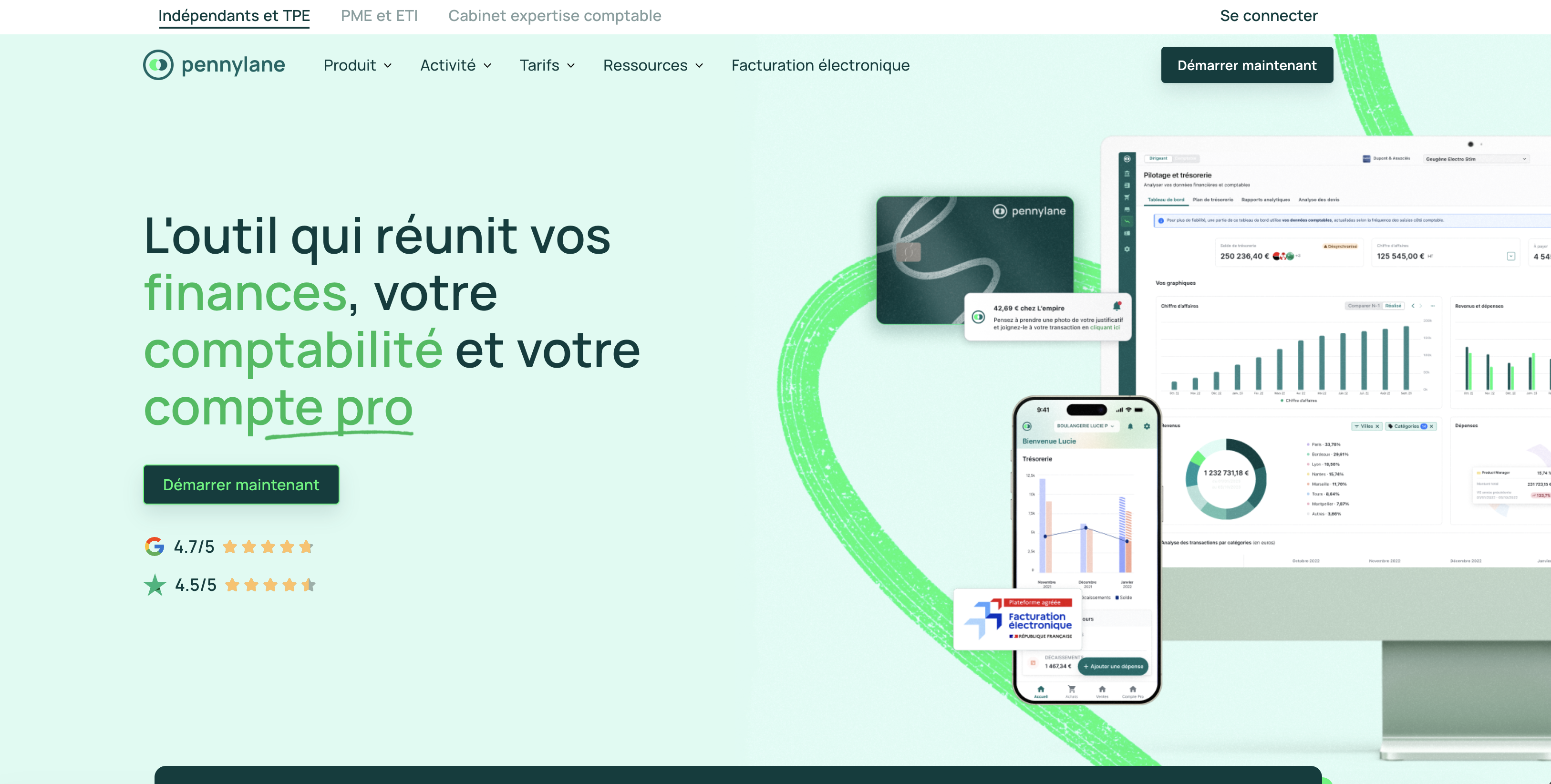

Pennylane

Digital Banking🇫🇷 France

Pennylane is a French fintech that bundles accounting, invoicing, and banking into one platform built for freelancers and small businesses. Rather than piecing together separate tools, users get a unified workspace where transactions sync automatically, expenses categorize themselves, and tax calculations happen in the background. The company positions itself against the fragmented mess of legacy accounting software and generic banking solutions, betting that SMEs want a single interface that actually understands their cashflow.

What sets Pennylane apart in Europe's crowded SME finance space is its focus on simplicity without sacrificing depth. While competitors often target either accountants or business owners, Pennylane aims at the owner-operator who wants to understand their numbers without hiring bookkeeping help. The platform connects directly to bank feeds and invoice data, pulling everything into a dashboard that feels less like traditional accounting software and more like a modern finance app.

Pennylane represents a shift in how European SMEs are expected to manage money. Rather than quarterly accountant visits and spreadsheet chaos, the company argues that modern businesses should have real-time visibility into their finances. It's part of a broader movement to make financial operations software actually enjoyable to use, not just tolerable.

Founded 2018

OneFor

Lending🇬🇧 United Kingdom

OneFor is a European fintech platform that reimagines how SMEs access and manage working capital. Rather than treating finance as a transactional afterthought, OneFor embeds cash flow tools, invoice financing, and dynamic credit solutions directly into the workflows where small business owners actually work. The platform pulls together accounts data, payment history, and real-time transaction flows to offer instant access to capital without the friction of traditional bank applications.

What sets OneFor apart is its positioning as a cash flow operating system rather than just another lending product. It serves companies that traditional banks have largely abandoned—the messy middle of European small business—by automating the visibility and accessibility of working capital. While legacy banks still demand spreadsheets and weeks of underwriting, OneFor delivers decisions in hours using behavioral data and API connections to accounting software.

The company operates across Western Europe with particular traction in the UK and Nordics, building a loyal following among founders who've grown tired of juggling multiple finance tools. Its integration-first approach means OneFor sits comfortably alongside existing business software stacks, making it feel less like switching banks and more like upgrading your CFO's toolkit. In a crowded SME finance space, OneFor's bet is that speed, transparency, and embedded simplicity will ultimately win over traditional lending relationships.

Founded 2020

Bankin

Digital Banking🇫🇷 France

Bankin is a French fintech that connects you to your money across multiple banks through a single app. Rather than juggling five different banking apps, Bankin aggregates all your accounts—checking, savings, investments, crypto—into one place where you can see your full financial picture. The company doesn't hold your money or replace your banks; it's an overlay that reads your data securely and gives you control over what happens next. What sets Bankin apart is its focus on switching: unlike most aggregators that just show you balances, Bankin helps you move money between banks, find better rates, and actually leave a bank if you want to. It's positioned somewhere between a personal finance dashboard and a financial comparison tool, but with genuine switching capability baked in. The app works across Europe, though strongest in France and the Nordics, and has built a loyal base of power users who genuinely use it to manage their money rather than just peek at their balance. In a landscape crowded with robo-advisors and neobanks offering me-too features, Bankin solves a more mundane but more urgent problem: most people still bank with multiple institutions and hate managing them. The company has positioned itself as the glue holding fragmented European banking together, and that simplicity—aggregation plus switching—gives it a unique role in the open banking revolution.

Founded 2013

Xero

Financial Infrastructure🇩🇪 Germany

Xero has spent the last fifteen years building the accounting software that most small business owners actually want to use. It's cloud-first, beautifully designed, and treats compliance as something that happens in the background rather than a chore. The platform connects directly to your bank account, automatically categorizes transactions, and integrates with hundreds of payroll, invoicing, and inventory tools—turning what used to be a quarterly nightmare into something you barely think about.

Founded 2006

FinFrog

Digital Banking🇫🇷 France

FinFrog is a French neobank designed for the Instagram generation—a mobile-first challenger that strips away the pretense of traditional banking and treats financial management like a social experience. Rather than positioning itself as a replacement for your main bank, FinFrog positions as the fun account you actually use, complete with spending analytics that actually make sense and a card that feels like an extension of your lifestyle rather than a financial obligation.

The platform focuses on real-time spending visibility, automated savings mechanisms, and a philosophy that younger Europeans shouldn't have to tolerate clunky interfaces or hidden fees just to manage their money. It's built on the premise that financial literacy and engagement happen through friction-free, mobile-native experiences, not through apps bolted onto legacy systems.

Within the European challenger banking landscape, FinFrog carves out space by leaning heavily into design and user experience clarity rather than attempting to be everything at once. While competitors chase feature bloat, FinFrog has maintained focus on core banking and budgeting fundamentals executed at a level that feels genuinely differentiated.

As part of the broader shift toward mobile-first financial services in continental Europe, FinFrog represents the next wave of neobanks that treat banking as a utility that should be boring, fast, and actually yours—no corporate messaging, no pretense, just money that works.

Founded 2018

Meniga

Digital Banking🇮🇸 Iceland

Personal finance management has been fragmented for years—users juggle multiple accounts across different banks, struggle to categorize expenses, and lose sight of their actual spending patterns. Meniga built the operating system for that chaos, connecting directly to banks across Europe and beyond to give people a unified view of their financial life.

The company aggregates account data from thousands of financial institutions, automatically categorizes transactions, and surfaces actionable insights through intuitive mobile and web interfaces. Rather than forcing users to manually log expenses or switch banks, Meniga meets them where their money already is. The platform learns spending habits over time and can flag anomalies, suggest savings opportunities, and help families coordinate finances in one place.

While most fintech startups chase headlines with flashy features, Meniga has stayed disciplined on the unglamorous work of data plumbing and user experience. It's become the backend for other financial services—banks, brokers, and insurers across the region use Meniga's APIs and white-label solutions to power their own personal finance tools, rather than building from scratch.

The company operates quietly but pervasively across Northern Europe and beyond, having grown from a Reykjavik startup into a critical piece of financial infrastructure for millions of users and dozens of institutional partners. In an era of financial fragmentation, Meniga is the connective tissue.

Founded 2009

Hype

Digital Banking🇮🇹 Italy

Hype is Italy's answer to the mobile banking revolution, a neobank that has spent nearly a decade proving that digital-first doesn't mean stripped-down. Rather than chase global scale with generic features, Hype has built a hyperlocal following by understanding what young Italians actually want from their money: instant transfers, cashback rewards, zero monthly fees, and a sleek app that doesn't feel like it was designed by a committee of compliance officers.

The platform operates as a digital-only current account backed by actual IBAN credentials, so it's not playing at banking—it's the real thing, licensed and regulated. Users get a contactless Mastercard, push-notification alerts for every transaction, and the kind of interface that makes traditional banking feel positively medieval by comparison. Hype's cashback ecosystem is its signature move, offering percentage returns on spending across partner merchants, which transforms the app from a mere account holder into a lifestyle spending companion.

In a market where European neobanks have largely converged around identical feature sets, Hype has chosen to go deep rather than broad, cementing itself as the default neobank for Italian millennials and Gen Z. It's proof that you don't need hundreds of millions in funding or ambitions to be present in every time zone to build something genuinely meaningful. The company represents a particular kind of fintech success: profitable, focused, and beloved by its core audience rather than chased by venture capitalists.

Hype demonstrates that the future of banking in Europe isn't about creating one global super-app, but rather a network of fiercely intelligent regional players, each optimized for the specific financial behaviors and preferences of their home market.

Founded 2014

Chip

Digital Banking🇬🇧 United Kingdom

Chip is a savings app that treats your money like it's on autopilot. Rather than asking you to manually set aside cash each month, Chip uses machine learning to analyze your spending patterns and automatically moves small amounts into a separate savings pot whenever it detects you can afford it. Think of it as a financial safety net that works in the background—no willpower required, just consistent, painless saving. The app integrates with your main bank account and learns your habits over time, adjusting how much it saves as your circumstances change. It's designed for people who want to build a financial cushion but struggle with the discipline of traditional budgeting. Chip democratizes financial discipline by removing the human friction from saving. Most savings apps ask you to commit upfront or rely on manual contributions; Chip does the thinking for you. The platform has become a trusted companion for UK consumers looking to pad their emergency fund without the guilt of underspending or oversaving. In the broader fintech landscape, Chip represents a shift toward behavioral finance—using technology and psychology to nudge people toward better financial habits rather than relying on willpower alone.

Founded 2016

Showing 12 of 16 companies. View all in the directory →