← All services

21 European companies

core banking

Core banking platforms are the central systems managing a bank's fundamental operations — account management, transaction processing, customer records, product configuration, and regulatory reporting. Modern cloud-native core banking software like Mambu and Thought Machine provides banks with flexible infrastructure that supports rapid product development without the constraints of legacy systems built decades ago.

Typically offered by

European fintech companies offering core banking

BVNK

Financial Infrastructure🇬🇧 United Kingdom

BVNK is a digital asset infrastructure company built for the institutional world. Founded to bridge traditional finance and crypto, it provides custody, settlement, and liquidity services for digital assets across multiple blockchain networks. Rather than positioning itself as a trading platform or exchange, BVNK operates as plumbing—a behind-the-scenes infrastructure layer that lets banks, payment processors, and fintech companies add digital asset capabilities to their existing systems. The platform handles the technical and regulatory complexity that kept institutions out of crypto, offering institutional-grade security and compliance tooling alongside access to decentralized finance. In a market flooded with retail-focused crypto products, BVNK targets the institutional infrastructure gap. It serves as the counterparty settlement layer and liquidity provider for financial institutions that want to offer digital assets without building their own custody and execution infrastructure. The company counts major payment networks and banking infrastructure providers among its early customers, positioning itself as the connective tissue between traditional finance rails and blockchain networks. BVNK reflects a maturation in crypto infrastructure—less about speculation and retail adoption, more about institutional plumbing that will quietly power the next generation of financial services.

Founded 2021

Omnius

Financial Infrastructure🇩🇪 Germany

Omnius is a European fintech infrastructure player that builds the plumbing for digital finance. Rather than launching consumer apps or chasing trends, the company focuses on giving financial institutions and fintech operators the core technology to move faster. The platform handles payment processing, account management, and the underlying APIs that let banks and non-banks operate at scale without reinventing the wheel.

What distinguishes Omnius in a crowded infrastructure market is its pragmatic approach to complexity. European banks still manage legacy core systems alongside new digital channels—a messy, expensive reality most fintech companies ignore. Omnius doesn't fight that; it sits in the middle, connecting old and new, and abstracts the chaos away from the business logic above it.

The company targets institutions that need to modernize faster than their technology stacks allow. That includes challenger banks that need banking-as-a-service foundations, traditional banks building new digital channels, and fintech companies that want to scale without owning every layer. It's unsexy infrastructure work—the kind that doesn't generate headlines but quietly powers the financial services layer that consumers interact with.

In the European fintech stack, Omnius occupies a critical but overlooked position: the vendor that lets faster companies stay fast, and slower ones move at all.

Nexi

Financial Infrastructure🇮🇹 Italy

Nexi is Italy's largest payment services operator, controlling the infrastructure that moves money across the country's retail and corporate sectors. Founded in 2013 through a merger of two major Italian payment processors, it manages card transactions, merchant acquiring, and digital payment rails for banks, retailers, and businesses across Europe.

The company operates across the full payments stack—from traditional POS terminals and card networks to modern API-based solutions and instant payment systems. Unlike most fintech startups, Nexi doesn't target consumers directly. Instead, it powers the payment backbone for Italian and European financial institutions and retailers, processing tens of billions in transactions annually. Its business model sits at the intersection of traditional payment infrastructure and modern open banking, positioning it as a critical node in Europe's shift toward real-time payments and embedded finance.

Nexi's role is unglamorous but essential: it's the plumbing that makes modern commerce work, handling everything from contactless cards to mobile wallets to cross-border transfers. In the broader European fintech landscape, it represents the "boring" but profitable core—the infrastructure layer that fintechs themselves depend on to function.

Founded 2013

Solaris

Financial Infrastructure🇩🇪 Germany

Solaris is a Berlin-based fintech infrastructure platform that lets financial institutions and fintechs launch their own digital banking products without building tech from scratch. Rather than wrestling with legacy core banking systems, clients plug into Solaris's cloud-native API layer to issue cards, manage accounts, and process payments at speed.

The company operates in the shadows of most consumer apps—you won't see the Solaris logo in an app store—but its backbone runs through dozens of European fintechs, neobanks, and traditional financial institutions. Think of it as the plumbing that powers other people's banking ambitions.

Solaris dominates a specific niche: the BaaS (Banking-as-a-Service) and embedded finance layer for Europe. While competitors like Thought Machine and Temenos chase enterprise banking overhauls, Solaris stays focused on the modern fintech workflow. Its modular design appeals to companies that need speed and flexibility, not a 10-year implementation project.

In a market crowded with infrastructure plays, Solaris has become essential plumbing for European digital banking. It sits at the intersection of regulatory compliance, technical simplicity, and startup ambition—precisely where the next wave of European fintech is being built.

Founded 2015

Mambu

Financial Infrastructure🇩🇪 Germany

Mambu is a cloud-native banking software platform that lets financial institutions and fintechs launch and operate lending and deposit products without building from scratch. Rather than forcing customers into rigid legacy systems, Mambu provides composable banking infrastructure—modular APIs and pre-built components that work together or stand alone, depending on what you actually need.

The company sits at the intersection of two fintech realities: traditional banks are drowning in outdated core systems that can't keep pace with market demands, while new lenders and neobanks need speed without sacrificing compliance or scale. Mambu's approach is to be the operating system underneath, handling the heavy lifting of loan origination, deposit management, portfolio servicing, and regulatory reporting while letting clients focus on customer experience and product innovation.

What makes Mambu different from other core banking platforms is its emphasis on velocity. Institutions deploy in weeks rather than years. The platform is genuinely modular—you can pick the lending module, the deposit module, or both, and layer in third-party services through APIs. This flexibility has resonated with everyone from African microfinance networks to European challenger banks to enterprise lenders managing complex credit products.

Mambu is now a critical piece of infrastructure in the emerging markets fintech ecosystem, particularly across Africa and Asia, where it powers lending operations for hundreds of financial institutions. In Europe, it's carved out space among mid-market and challenger banks looking to avoid the capital expenditure and technical debt of legacy systems. The company represents a broader shift in fintech: away from end-to-end platforms that claim to do everything, toward specialized infrastructure that does one thing—backend financial operations—exceptionally well.

Founded 2011

Thought Machine

Financial Infrastructure🇬🇧 United Kingdom

Thought Machine builds the operating system for modern banking. Its Vault platform is a cloud-native core banking system that replaces the legacy infrastructure most banks still depend on—the kind that was written when personal computers were novel and the internet was optional. Rather than patching decades-old mainframes with band-aids, Vault lets banks modernize from the ground up, moving away from monolithic systems toward modular architecture that can actually adapt to change. The platform serves as the nervous system for digital banking, payment processing, and lending at scale, handling everything from transactions to regulatory compliance in real time. Thought Machine competes directly against vendors like Temenos and Finastra, but with a fundamentally different philosophy: born in the cloud, designed for APIs, built for speed. The company works with tier-one banks and ambitious challengers alike, essentially selling them the technical freedom to compete in fintech's pace rather than their legacy system's glacial timeline. In the broader European fintech ecosystem, Thought Machine represents the infrastructure layer that makes everything else possible—without modern core banking, the rest of the fintech revolution stays locked in legacy constraints.

Founded 2014

Tieto

Financial Infrastructure🇫🇮 Finland

Tieto operates in the murky middle ground between traditional IT services and fintech infrastructure, building the unsexy-but-essential systems that European financial institutions actually run on. The company provides core banking platforms, payment systems, and digital banking solutions to banks and financial services firms across the Nordic and European markets. Where most fintech captures headlines with consumer apps, Tieto stays disciplined in the B2B infrastructure game—modernizing legacy systems, managing complex regulatory requirements, and keeping payments flowing. Its positioning reflects a particular Nordic pragmatism: less about disruption, more about making banking systems reliable, scalable, and compliant. In a landscape crowded with flashy consumer fintechs, Tieto represents the unglamorous but critical plumbing layer that enables everyone else to operate. The company remains one of Europe's largest fintech infrastructure players, though its parent company structure and steady-handed approach means it rarely commands the venture attention of younger competitors.

Founded 1969

Wallester

Embedded Finance🇪🇪 Estonia

Wallester is a European fintech infrastructure company that makes it simple for other businesses to issue, manage, and distribute payment cards at scale. Rather than wrestling with legacy banking systems and complex integrations, companies use Wallester's APIs and platforms to embed card programs directly into their own products—think neobanks, fintechs, and platforms that need white-label card solutions without the operational overhead. The company handles the technical plumbing: card issuance, real-time transaction processing, compliance, and customer-facing controls, all delivered through clean, developer-friendly APIs. Wallester operates across multiple European markets and works with everyone from emerging challenger banks to established financial institutions looking to modernize their card infrastructure. What sets Wallester apart is its focus on removing friction from the card-issuing process. Most issuers are bound to cumbersome core banking relationships or have to build entirely custom solutions. Wallester sits in the middle, offering a turnkey platform that scales with demand without forcing companies to reinvent core banking. It's become a quiet backbone for European fintechs that need cards fast, reliably, and without the bureaucracy. The company represents a broader trend in fintech infrastructure: the unbundling of banking services into modular, API-first components that let smaller players compete with traditional incumbents.

Founded 2019

finleap

Embedded Finance🇩🇪 Germany

finleap is Berlin's answer to a question the European fintech scene keeps asking: how do you build world-class financial companies at scale? Rather than chase unicorn valuations, finleap builds them. The holding company operates as a fintech factory, incubating and scaling financial startups from day one with institutional backing, operational expertise, and a network that spans regulators, banks, and investors across the continent.

What sets finleap apart is the architecture itself. It's not an accelerator or a VC fund—it's a purpose-built engine for creating and nurturing fintech companies. Each portfolio company gets access to finleap's infrastructure, compliance playbooks, and go-to-market templates, which compresses timelines and eliminates the friction that typically derails early-stage fintechs. The model works: companies like Wayfair-backed Finn, B2B payments platform Foxpay, and lending marketplace Evala have all emerged from the finleap stable.

Internally, finleap operates across payments, lending, wealth, and embedded finance—categories where the European market remains genuinely underpenetrated compared to the US. The company's thesis is straightforward: identify white space in financial services, build products faster than traditional banks can move, and create defensible market positions through technology and user experience. It's less about disruption theater and more about pragmatic value creation.

Finleap sits at an interesting intersection in the European fintech landscape: large enough to command resources and regulatory relationships, independent enough to move quickly, and structured in a way that lets founders maintain autonomy while tapping institutional muscle. For a continent that produces good fintech companies but struggles with scaling, finleap represents a new playbook.

Founded 2014

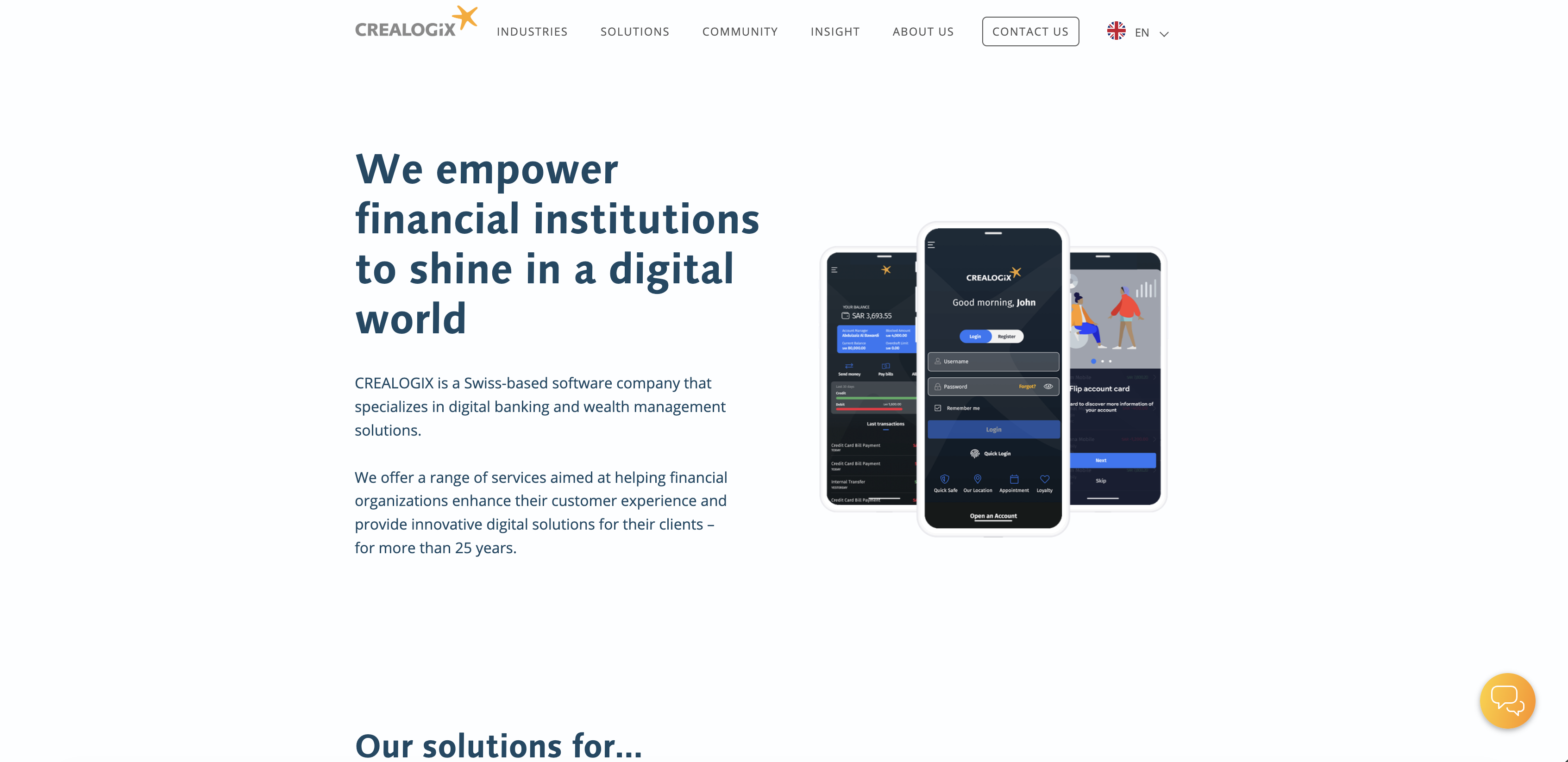

Crealogix

Financial Infrastructure🇨🇭 Switzerland

Crealogix is a Swiss fintech company that builds digital banking platforms for financial institutions across Europe. Rather than starting from scratch, banks and wealth managers plug into Crealogix's modular software suite to modernize their customer experience—covering everything from retail and corporate banking interfaces to wealth management portals and mobile apps.

The company operates as an infrastructure play in the digital transformation space. Its platforms run on a microservices architecture, letting financial institutions pick and choose the components they need rather than ripping out legacy systems entirely. This approach has gained traction with mid-market and enterprise banks looking to compete with neobanks without the cost of a complete rebuild.

Crealogix sits in a pragmatic middle ground between traditional banking software vendors and modern fintech disruptors. It's not trying to be a bank itself; instead, it partners with incumbents and increasingly with smaller financial institutions across German-speaking Europe and beyond. The company's strength lies in understanding both the technical demands of modern digital banking and the regulatory complexity that traditional banks navigate daily.

In the evolving European fintech landscape, Crealogix represents the infrastructure generation—the companies enabling the banking industry's digital transition rather than replacing it entirely.

Founded 1999

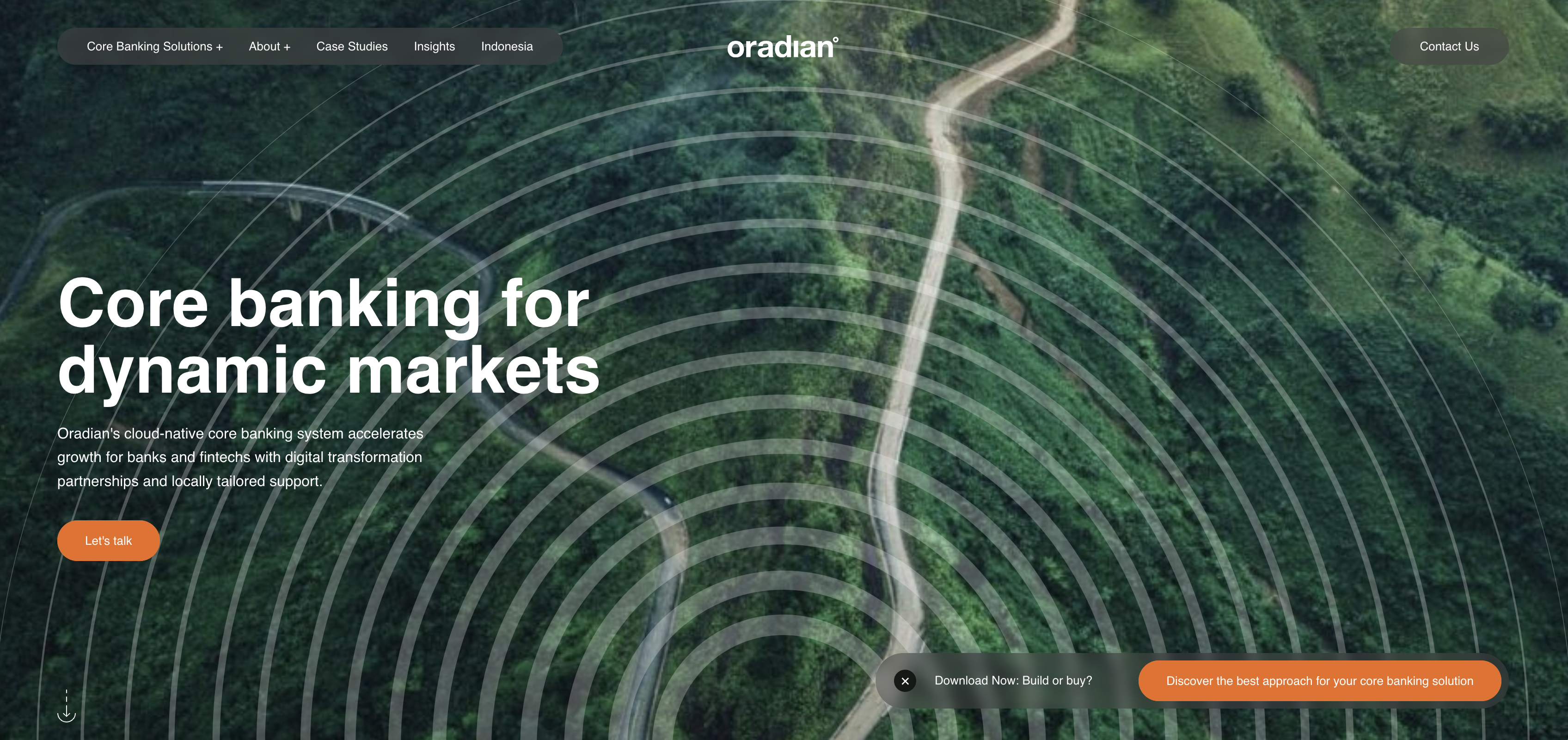

Oradian

Financial Infrastructure🇭🇷 Croatia

Microfinance institutions and banks operating in emerging markets have technology needs that the major core banking platforms haven't traditionally served well — they need cloud-deployed infrastructure that runs reliably with intermittent connectivity, supports the specific products and workflows of microfinance, and is priced for institutions that operate at scale but with thinner margins than developed-market banks. Oradian was founded in Zagreb in 2012 to build that core banking platform, deploying its cloud-native banking infrastructure to microfinance institutions, credit unions, and emerging market banks across Africa, Southeast Asia, and Latin America. The Croatian engineering base combined with deep expertise in emerging market banking operations gave Oradian a positioning that few core banking competitors could replicate — modern cloud architecture combined with genuine understanding of how microfinance institutions actually work. Oradian has deployed its platform to hundreds of financial institutions across multiple emerging market regions, processing billions in transactions for institutions serving millions of customers who would otherwise be excluded from formal financial services. In the broader European fintech landscape, Oradian represents the category of European technology built explicitly for emerging market deployment — a model that has produced some of the more interesting and impactful fintech outcomes by addressing markets where the underlying need is substantial and where European technology engineering can deliver disproportionate value.

Founded 2012

FintechOS

Financial Infrastructure🇷🇴 Romania

Banking software has historically been built around the idea that each financial product needs its own dedicated system — a current account platform, a separate mortgage system, another for credit cards, another for investments. The result is a fragmented technology landscape that prevents banks from delivering the unified experience customers actually want. FintechOS was founded in Bucharest in 2017 to challenge that model with a digital-first platform that lets financial institutions build, launch, and operate any financial product on a single configurable infrastructure. Its platform combines core banking capabilities with low-code product configuration, letting banks design customer journeys, launch new products, and modify existing ones without the multi-year IT projects that define traditional banking transformation. FintechOS has attracted backing from major investors including Earlybird and Draper Esprit, and serves banks and insurance companies across Europe and beyond. The Romanian base is significant — Bucharest has emerged as one of the more important Central European fintech hubs, and FintechOS has built one of the most credible product-led companies to come from that ecosystem. In the European banking infrastructure market, where the largest players are global enterprise software companies, FintechOS represents a generation of platform-native banking technology built for a different kind of bank.

Founded 2017

Showing 12 of 21 companies. View all in the directory →