← All services

64 European companies

loan origination

Loan origination platforms manage the end-to-end process of creating a new loan — from initial application and credit assessment through underwriting, approval, documentation, and disbursement. Digital loan origination has compressed timelines from weeks to hours for many loan types by automating data collection, credit decisioning, and document generation, while maintaining the compliance standards that regulated lending requires.

Typically offered by

European fintech companies offering loan origination

Monzo

Wealth🇬🇧 United Kingdom

The founding team that built Monzo had all worked together before — at Starling Bank, another challenger bank startup that didn't survive its internal conflicts. Tom Blomfield, Gary Dolman, Jonas Huckestein, Jason Bates, and Paul Rippon left Starling together in 2015 and started again. The product they built was initially a prepaid card — a coral-coloured piece of plastic that became one of the most recognisable objects in British fintech — before becoming a fully licensed current account in 2017.

The early user community was unusual for a bank. Monzo ran community forums, published public blog posts about its engineering decisions, and invited customers into beta programmes for new features. When it broke the world record for the fastest crowdfunding raise in 2016 — £1 million in 96 seconds — it wasn't just raising money; it was building an identity. People felt ownership of the product in a way that no high street bank had ever managed to create. That emotional connection became a genuine competitive advantage.

The product has matured considerably since then. Monzo now offers current accounts, joint accounts, savings pots, personal loans, overdrafts, and investment products, all wrapped in the real-time notification experience and transaction categorisation that made its early reputation. Revenue reached £1.23 billion in 2024, up 40% year on year, with net income of £95 million — the second consecutive year of profitability after years of growth-first losses. The customer base reached 12.1 million by end of 2024, making Monzo the UK's largest digital bank by customer count. Customer deposits stood at £16.6 billion.

The business is still private — the much-discussed IPO has not yet happened, and internal disagreements about where to list (the former CEO TS Anil favoured the US, the board preferred London) contributed to Anil's departure in October 2025. Diana Layfield took over as CEO with a mandate focused on international expansion before any public listing. The company is valued at approximately $5.9 billion following a 2024 secondary sale backed by Alphabet's GIC and StepStone.

In December 2025 Monzo announced it had agreed to acquire Habito, the digital mortgage broker, pending regulatory approval — a move that extends the product into one of the last major financial products it didn't yet offer. With 3,821 employees and a loan book growing rapidly, Monzo has evolved from a prepaid card experiment into a bank with genuine scale and a growing claim on being the primary financial account for a generation of UK consumers.

Founded 2015

Funding Circle

Lending🇬🇧 United Kingdom

Funding Circle sits at the intersection of institutional capital and small business ambition. The platform connects SMEs with investors—funds, banks, and individuals—who want returns tied to real economic activity rather than abstract asset classes. It's fundamentally a marketplace, but one that's spent years learning how to assess credit risk at scale, price loans competitively, and move money across borders without the friction traditional finance demands.

The company operates across multiple geographies, though Europe remains central to its strategy. It handles everything from loan origination and underwriting through to servicing and portfolio management, meaning it's built real infrastructure rather than just matching borrowers to lenders. This matters because it allows institutional investors to actually understand what they're funding.

Funding Circle competes in a space where traditional banks have historically been absent—the mid-market lending gap where a £50,000 loan isn't big enough for a relationship manager but too important for a business to ignore. Alternative lenders have crowded this space, but Funding Circle's institutional backing and regulatory maturity give it a structural advantage. It's moved from pure peer-to-peer model toward a more hybrid approach, partnering with regulated lenders to expand reach while maintaining its marketplace credibility.

The company represents a fundamental rethinking of how capital reaches productive SMEs—not through gatekeepers, but through platforms that make risk transparent and pricing efficient.

Founded 2010

Mambu

Financial Infrastructure🇩🇪 Germany

Mambu is a cloud-native banking software platform that lets financial institutions and fintechs launch and operate lending and deposit products without building from scratch. Rather than forcing customers into rigid legacy systems, Mambu provides composable banking infrastructure—modular APIs and pre-built components that work together or stand alone, depending on what you actually need.

The company sits at the intersection of two fintech realities: traditional banks are drowning in outdated core systems that can't keep pace with market demands, while new lenders and neobanks need speed without sacrificing compliance or scale. Mambu's approach is to be the operating system underneath, handling the heavy lifting of loan origination, deposit management, portfolio servicing, and regulatory reporting while letting clients focus on customer experience and product innovation.

What makes Mambu different from other core banking platforms is its emphasis on velocity. Institutions deploy in weeks rather than years. The platform is genuinely modular—you can pick the lending module, the deposit module, or both, and layer in third-party services through APIs. This flexibility has resonated with everyone from African microfinance networks to European challenger banks to enterprise lenders managing complex credit products.

Mambu is now a critical piece of infrastructure in the emerging markets fintech ecosystem, particularly across Africa and Asia, where it powers lending operations for hundreds of financial institutions. In Europe, it's carved out space among mid-market and challenger banks looking to avoid the capital expenditure and technical debt of legacy systems. The company represents a broader shift in fintech: away from end-to-end platforms that claim to do everything, toward specialized infrastructure that does one thing—backend financial operations—exceptionally well.

Founded 2011

Younited Credit

Lending🇫🇷 France

Younited Credit sits at the intersection of consumer lending and fintech, offering personal loans to borrowers across Europe who want speed and transparency instead of the bureaucratic friction of traditional banks. Founded in 2011, the company has evolved from a peer-to-peer lending marketplace into a full-stack credit platform that sources, prices, and services loans for both retail customers and institutional partners.

The core product is straightforward: quick online approval (often minutes), competitive rates based on real underwriting, and a streamlined digital experience that feels more like ordering something on your phone than sitting in a bank branch. What distinguishes Younited from the crowded European consumer lending space is its scale and sophistication. Rather than just operating a marketplace, the company has built proprietary credit scoring models, automated servicing infrastructure, and a diversified funding model that includes institutional investors, warehouse financing, and securitization. This means Younited isn't dependent on peer-to-peer investors or a single funding source—it can grow independently. The platform operates across multiple European markets and has become a quiet infrastructure player for consumer credit, processing loans for direct borrowers while also powering lending for third parties through white-label partnerships. In an era when legacy banks still treat personal lending like a commodity and fintechs are scrambling to prove unit economics, Younited represents the pragmatic middle ground: technology-first underwriting and customer experience wrapped around a business model that actually scales profitably.

Founded 2011

auxmoney

Lending🇩🇪 Germany

auxmoney sits at the intersection of peer-to-peer lending and digital financial inclusion. The Berlin-based platform connects individual investors with borrowers seeking personal loans, sidestepping traditional bank gatekeeping through algorithmic credit assessment and a streamlined approval process.

Since 2007, it has built one of Europe's more mature alternative lending marketplaces, processing billions in credit and establishing itself as a credible counterweight to institutional finance for everyday lending needs. What sets auxmoney apart in the crowded P2P lending space is its focus on accessibility: borrowers who might struggle with conventional bank criteria can access capital, while investors gain exposure to diversified consumer credit without the friction of direct lending management. The platform automates origination, servicing, and investor payouts, handling the operational complexity that keeps most people out of direct lending. auxmoney doesn't pretend to be a bank—it's unapologetically a marketplace, transparent about risk and returns in ways traditional lenders rarely are.

In a European fintech landscape increasingly dominated by neobanks and payment startups, auxmoney represents a quieter but steadier category: the infrastructure that lets capital find borrowers efficiently. Its longevity and scale demonstrate that P2P lending, despite early hype and inevitable casualties, has become infrastructure for people and investors outside the conventional banking circle.

Founded 2007

Belvo

Embedded Finance🇪🇸 Spain

Belvo is a fintech infrastructure company that lets developers tap into Latin American banking data without building a single integration. The platform connects to thousands of banks and financial institutions across Mexico, Brazil, Colombia, and Peru, unlocking account balances, transaction histories, and identity information through a single API. Rather than forcing developers to chase down fragmented banking systems, Belvo standardizes chaotic regional financial infrastructure into clean, predictable data flows. Its core insight is simple: Latin American fintech is drowning in bank connectivity work when it should be building products. Belvo solves that. The platform serves fintechs, neobanks, and traditional financial institutions looking to modernize lending decisions, open banking integrations, and embedded finance experiences. Think of it as the connective tissue between fractured regional banking systems and the apps that need to run on top of them. By abstracting away the complexity of working with hundreds of different bank APIs and connection methods, Belvo has become the standard for financial data aggregation in a region where banking infrastructure is anything but standardized. It's the kind of boring-but-essential infrastructure that powers smarter lending, faster onboarding, and new financial products across Latin America.

Founded 2019

Credit Spring

Lending🇬🇧 United Kingdom

Credit Spring is a UK-based fintech that treats financial distress like a health problem—one that deserves diagnosis and treatment, not judgment. Rather than simply offering credit, the company combines short-term loans with financial coaching and debt management tools, recognizing that a quick cash injection without context is often a band-aid on a bigger problem. The platform helps borrowers understand their spending patterns and rebuild their financial foundation, not just patch a temporary shortfall. It's a provocative stance in a market crowded with BNPL and payday lenders that rarely ask why someone needs money in the first place. Credit Spring targets people in the credit-vulnerable segment—those with poor or limited credit histories who'd normally be shut out of mainstream lending. Instead of algorithmic rejection, the company uses alternative data and behavioral insights to assess creditworthiness beyond traditional scoring. For users, this means faster access to reasonable credit at transparent rates. For the market, it signals a shift toward lending that acknowledges financial fragility as a temporary state, not a permanent condition. The company represents a broader move within fintech to attach financial wellness services to credit products, treating lending as an entry point to deeper financial health rather than a transaction.

Founded 2016

Partasio

Wealth🇨🇭 Switzerland

Most people think of art as something you hang on a wall, not something you add to a portfolio. That’s exactly the gap Partasio is trying to close.

Based in Switzerland, Partasio sits at the intersection of finance and culture, turning blue-chip art into a structured investment product. Instead of buying a single painting for millions, investors can access curated portfolios of museum-grade works—fractionalized, packaged, and managed like a financial asset.

At its core, the model is simple but powerful. Partasio builds portfolios of 4–6 high-end artworks from globally established artists, typically sourced off-market through private networks. Each portfolio is placed into a single-purpose vehicle, and investors buy into it through bankable certificates—complete with a Swiss ISIN—making it look and behave more like a traditional financial instrument than an art purchase.

The pitch isn’t just about access—it’s about diversification. Blue-chip art has historically shown low correlation with traditional asset classes like equities or real estate, making it attractive for investors looking to balance risk. But until recently, that market was largely reserved for ultra-wealthy collectors. Partasio lowers that barrier, with minimum investments starting around CHF 30,000.

What makes the platform stand out is how it blends private equity logic with the art world. Portfolios are actively managed over a multi-year horizon, with returns realized when the artworks are sold—typically within three to seven years. The company’s incentives are aligned with investors, earning performance fees only when profits are generated.

It’s part of a broader shift in fintech toward alternative assets—where everything from real estate to art is becoming more accessible, structured, and digital. But Partasio leans into something slightly different. It doesn’t try to reinvent art. It simply builds a financial layer around it.

In a market that’s historically opaque and exclusive, that alone is enough to make it stand out.

Founded 2022

EstateGuru

Real Estate Finance🇪🇪 Estonia

Real estate-backed lending across European markets has been one of the more durable categories within marketplace lending, partly because the underlying collateral provides recovery infrastructure that unsecured consumer lending lacks. EstateGuru was founded in Tallinn in 2014 to build a Pan-European platform connecting retail and institutional investors with property developers and real estate businesses needing project financing. The platform operates across multiple European markets, originating loans secured against real estate and offering investors the ability to diversify across geographies and loan types. EstateGuru has funded over a billion euros in real estate-backed loans since inception, making it one of the largest property-focused marketplace lending platforms in Europe. The model has proven more resilient through market cycles than unsecured consumer P2P lending — when borrowers default, the underlying real estate collateral provides recovery options that consumer loans don't have. The company has navigated the broader maturation of European marketplace lending while maintaining the property-secured focus that distinguishes it from generalist platforms. In the European alternative real estate finance landscape, EstateGuru represents one of the more substantial cross-border marketplace operators — building genuine geographic diversification rather than the single-market focus that characterises most regional property finance platforms.

Founded 2014

Inbank

Digital Banking🇪🇪 Estonia

Specialised banking for consumer credit — focused on lending products distributed through merchant partnerships rather than building general-purpose retail banking — is a model with deeper European roots than the venture-backed BNPL conversation suggests. Inbank was founded in Tallinn in 2011 as a specialist lender focused on point-of-sale consumer credit, partnering with retailers across Estonia and the broader Baltic and Central European region to offer instalment finance at the moment of purchase. The company received a full Estonian banking licence and has built operations across Estonia, Latvia, Lithuania, Poland, and the Czech Republic, expanding from a domestic specialist into a Pan-European consumer finance bank. Inbank is publicly listed on the Nasdaq Tallinn exchange — one of the few publicly traded Baltic fintechs — giving it both the regulatory standing of a licensed bank and the funding access of a public company. Its product range covers point-of-sale finance, BNPL, and consumer deposit products, with merchant partnerships across automotive, electronics, home improvement, and other categories where consumers commonly finance purchases. In the European specialist consumer banking landscape, Inbank represents one of the more successful examples of a focused operator scaling across borders while maintaining the operational discipline of a regulated bank.

Founded 2011

NeoFinance

Lending🇱🇹 Lithuania

Lithuanian peer-to-peer lending built one of the more substantial European markets for marketplace consumer credit, with multiple platforms competing for both borrowers and investors in a country that has cultivated a regulatory environment supportive of fintech experimentation. NeoFinance was founded in Vilnius in 2014 as one of those Lithuanian P2P pioneers, connecting Lithuanian and international investors with creditworthy local borrowers seeking personal loans. The platform's domestic focus gave it credit data depth in the Lithuanian market that pan-European platforms didn't match, while its EU passport allowed it to attract investor capital from across Europe. NeoFinance has expanded its operations and product range while navigating the maturation of European P2P lending — including the regulatory tightening that brought retail crowdfunding under the European Crowdfunding Service Provider Regulation framework. In the Lithuanian P2P landscape, NeoFinance represents one of the longer-running platforms operating with a domestic borrower focus and a Pan-European investor base — a combination that has proven more sustainable than purely cross-border models that lacked deep credit knowledge of any single market.

Founded 2014

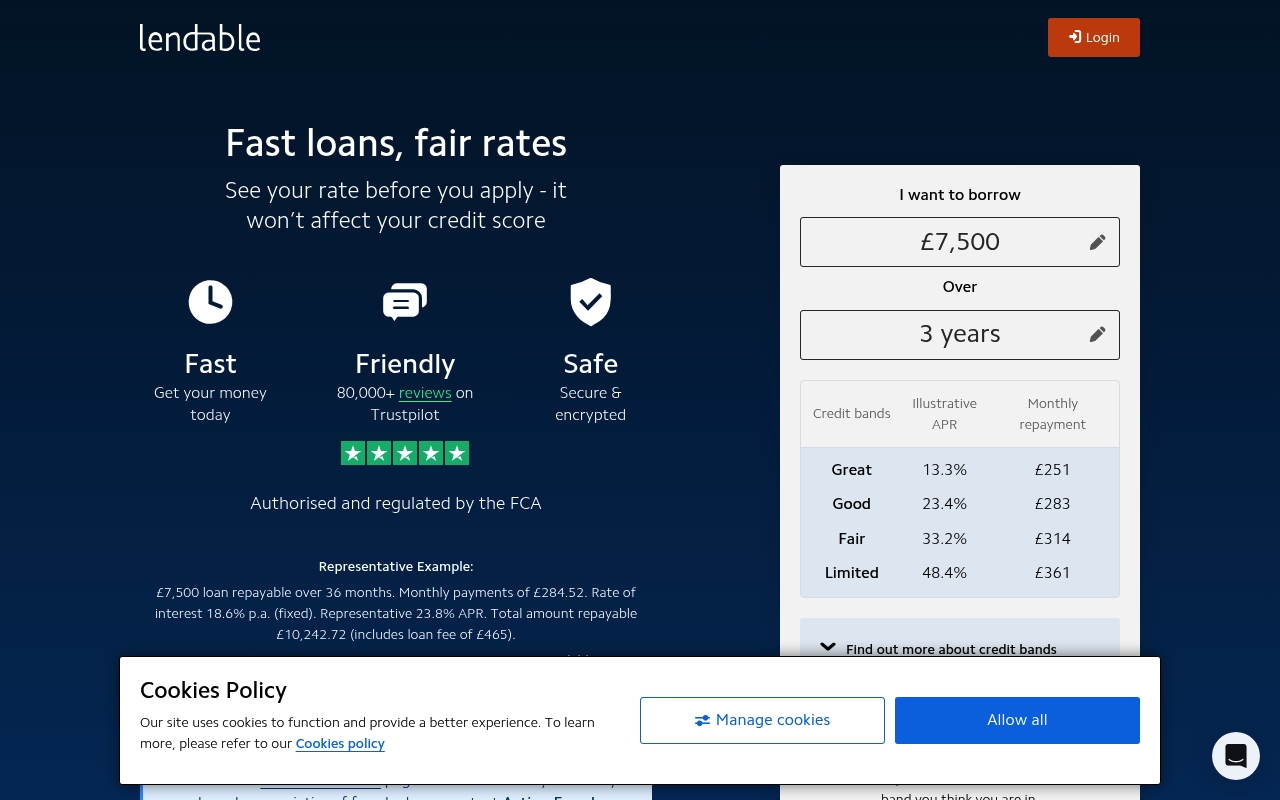

Lendable

Financial Infrastructure🇬🇧 United Kingdom

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates.

The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets.

In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names.

Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

Founded 2013

Showing 12 of 64 companies. View all in the directory →