← All services

20 European companies

white-label banking

White-label banking allows banks, fintechs, and non-financial companies to offer banking products under their own brand, powered by a third-party provider's infrastructure and licence. A retailer can offer a branded bank account backed by a BaaS partner. A software company can offer a branded business account to its customers. White-labelling separates the customer relationship and brand from the underlying regulated banking infrastructure.

Typically offered by

European fintech companies offering white-label banking

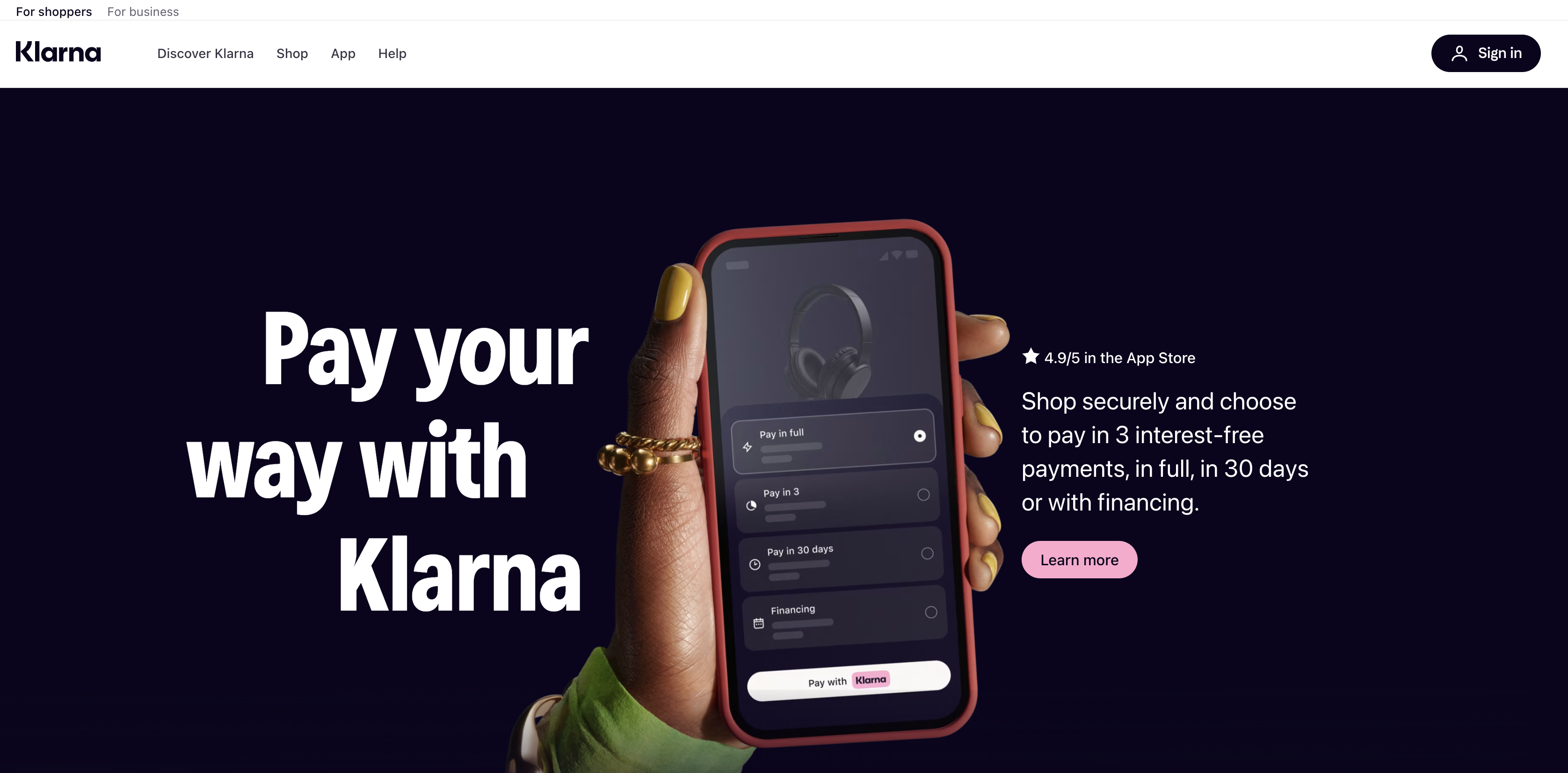

Klarna

Embedded Finance🇸🇪 Sweden

Three Stockholm School of Economics students pitched an idea at a university entrepreneurship competition in 2005: let shoppers receive goods before they pay, and put the credit risk on the merchant side. The pitch finished last. They built it anyway.

Sebastian Siemiatkowski, Niklas Adalberth, and Victor Jacobsson launched what was originally called Kreditor, later renamed Klarna, and spent the next two decades turning that rejected idea into one of Europe's most recognised fintech brands. The core insight held up: millions of people would rather split a purchase into three instalments than reach for a credit card, and merchants would pay for the privilege of offering that option because it reduces cart abandonment and increases average order values.

Klarna grew from a Swedish checkout button into something considerably more complex. It now holds a banking licence in Sweden, offers savings accounts, issues its own card, and operates across more than 45 markets with around 93 million active consumers and 675,000 merchant partners at the end of 2024. The US, which Klarna entered in 2015, has become its largest market by revenue, a fact the company underlined by listing on the New York Stock Exchange in September 2025 under the ticker KLAR, raising $1.37 billion at IPO.

The financial trajectory has been bumpy. Klarna reported net income of $21 million in 2024, a return to profitability after a bruising 2022 that included an 85% valuation cut and significant layoffs that reduced headcount from over 7,000 to around 3,400. What survived the restructuring was a leaner company with $2.81 billion in revenue and a clearer strategic direction: AI. Klarna's partnership with OpenAI produced a customer service assistant it claims handles the equivalent of 700 full-time agents, and generative AI now manages roughly two-thirds of customer chats.

The honest assessment of where Klarna sits today: it's no longer purely a BNPL provider and it's not quite a bank. It's somewhere in between, a consumer finance platform that knows more about your shopping behaviour than your bank does, and is betting that's worth a lot.

Founded 2005

Younited Credit

Lending🇫🇷 France

Younited Credit sits at the intersection of consumer lending and fintech, offering personal loans to borrowers across Europe who want speed and transparency instead of the bureaucratic friction of traditional banks. Founded in 2011, the company has evolved from a peer-to-peer lending marketplace into a full-stack credit platform that sources, prices, and services loans for both retail customers and institutional partners.

The core product is straightforward: quick online approval (often minutes), competitive rates based on real underwriting, and a streamlined digital experience that feels more like ordering something on your phone than sitting in a bank branch. What distinguishes Younited from the crowded European consumer lending space is its scale and sophistication. Rather than just operating a marketplace, the company has built proprietary credit scoring models, automated servicing infrastructure, and a diversified funding model that includes institutional investors, warehouse financing, and securitization. This means Younited isn't dependent on peer-to-peer investors or a single funding source—it can grow independently. The platform operates across multiple European markets and has become a quiet infrastructure player for consumer credit, processing loans for direct borrowers while also powering lending for third parties through white-label partnerships. In an era when legacy banks still treat personal lending like a commodity and fintechs are scrambling to prove unit economics, Younited represents the pragmatic middle ground: technology-first underwriting and customer experience wrapped around a business model that actually scales profitably.

Founded 2011

Belvo

Embedded Finance🇪🇸 Spain

Belvo is a fintech infrastructure company that lets developers tap into Latin American banking data without building a single integration. The platform connects to thousands of banks and financial institutions across Mexico, Brazil, Colombia, and Peru, unlocking account balances, transaction histories, and identity information through a single API. Rather than forcing developers to chase down fragmented banking systems, Belvo standardizes chaotic regional financial infrastructure into clean, predictable data flows. Its core insight is simple: Latin American fintech is drowning in bank connectivity work when it should be building products. Belvo solves that. The platform serves fintechs, neobanks, and traditional financial institutions looking to modernize lending decisions, open banking integrations, and embedded finance experiences. Think of it as the connective tissue between fractured regional banking systems and the apps that need to run on top of them. By abstracting away the complexity of working with hundreds of different bank APIs and connection methods, Belvo has become the standard for financial data aggregation in a region where banking infrastructure is anything but standardized. It's the kind of boring-but-essential infrastructure that powers smarter lending, faster onboarding, and new financial products across Latin America.

Founded 2019

Coverflex

Digital Banking🇵🇹 Portugal

Coverflex is rewriting how freelancers and gig workers access financial security in Europe. Instead of the traditional employment model, the platform bundles flexible work with genuine benefits—health insurance, pension contributions, and paid leave—creating a middle path between employment and total independence.

The company essentially flips the script on gig economy precarity. Workers stay independent contractors but gain access to protections that were previously locked behind 9-to-5 employment. Employers get a simpler way to hire flexible talent without managing traditional payroll complexity. It's a fundamentally different architecture for modern work.

Coverflex operates across multiple European markets and has built a B2B2C model where companies use the platform to offer benefits to their contractor workforce. The business combines insurance brokerage, financial services coordination, and workplace infrastructure into one interface.

In a landscape where gig work remains fragmented and precarious, Coverflex sits at the intersection of fintech and HR tech, solving a genuine gap in how Europe's growing contingent workforce accesses security and stability.

Founded 2020

Swile

Embedded Finance🇫🇷 France

Swile tackles the unglamorous but essential problem of employee benefits administration—turning what's typically a bureaucratic nightmare into something that actually works for modern companies. The Paris-based platform bundles meal vouchers, transportation allowances, childcare support, and wellness benefits into a single card and app that employees actually want to use.

Instead of juggling multiple vendor relationships and paper trails, HR teams get one interface to manage everything. Employees scan a card or phone at participating restaurants, shops, and gyms, earning tax-advantaged benefits while employers simplify their compliance burden. It's the kind of boring-but-essential infrastructure that scales across Europe—Swile operates in France, Spain, Italy, and beyond.

What sets Swile apart in the crowded benefits space is its focus on the entire employee lifecycle rather than just one vertical. While competitors obsess over meal vouchers or mobility, Swile positions itself as a comprehensive benefits platform. The company raised significant Series B funding and expanded aggressively across continental Europe, proving that there's real appetite for consolidation here.

Swile represents a broader shift in how European companies think about compensation: less about salary alone, more about total employee experience. By digitizing what was once entirely analog, Swile has become an essential piece of HR infrastructure for mid-market and enterprise employers across the region.

Founded 2016

Enable Banking

Financial Infrastructure🇫🇮 Finland

Enable Banking is an open banking infrastructure platform that simplifies how financial institutions and fintech companies connect to bank APIs across Europe. Rather than building custom integrations for dozens of different banking networks, companies tap into Enable Banking's unified layer—a single API that handles the complexity of connecting to thousands of European banks with varying technical standards and regulatory requirements.

The platform abstracts away the fragmentation that has made open banking adoption slower than it should be. While PSD2 and other regulations opened up bank data and payments, the actual implementation remains messy: each bank interprets the standards differently, each has its own API quirks, and each requires separate integration work. Enable Banking eliminates that friction.

Their core value sits in the infrastructure layer—they're infrastructure for infrastructure. Fintechs use it to access account data, initiate payments, and verify customer identity across European banks without maintaining individual relationships with each one. Banks use it to expose their APIs in a standardized way without rebuilding their legacy systems.

In a market where most open banking plays focus on consumer-facing applications, Enable Banking takes the plumbing approach. They're to open banking what Stripe is to payments: making the invisible layers work so others can build on top of them. This positions them as a critical enabler for the entire European fintech ecosystem rather than a consumer-facing application.

Founded 2018

Rapyd

Embedded Finance🇬🇧 United Kingdom

Rapyd is a global fintech infrastructure company that lets businesses accept payments and move money across 170+ countries without needing local banking relationships. Rather than forcing companies to navigate fragmented payment ecosystems country by country, Rapyd abstracts away the complexity—providing a single API that connects to local payment methods, wallets, and bank accounts everywhere from Southeast Asia to Latin America. The platform handles the unglamorous but essential work: acquiring local licenses, managing compliance, and integrating with hyperlocal payment rails so a startup in Berlin can charge a customer in Lagos as easily as one in London. For merchants and platforms operating globally, this means ditching the spreadsheet of payment processors and compliance frameworks. Instead of cobbling together 15 different providers to cover emerging markets, they get one dashboard, one contract, one API. Rapyd has positioned itself as the plumbing for the next wave of global commerce—the infrastructure layer that makes it possible for any business to think globally from day one, not after they've scaled. In a fintech landscape dominated by Western-centric payment networks, Rapyd's bet on true geographic diversity and local payment methods feels like a deliberate counterweight, making it an essential piece of the infrastructure for companies serious about serving the rest of the world.

Founded 2018

Worldpay

Embedded Finance🇬🇧 United Kingdom

Worldpay is one of Europe's most established payment infrastructure plays, handling transactions at the backbone of commerce across the continent. The company processes payments for retailers, e-commerce merchants, and financial institutions, sitting at the critical intersection where customer intent becomes settled value. Rather than chasing consumer attention, Worldpay operates in the plumbing layer—orchestrating card payments, merchant acquiring, and real-time settlement across borders with the quiet efficiency of infrastructure that's been stress-tested for decades. It's the kind of company most Europeans have never heard of but rely on every time they buy something online or in-store. What sets Worldpay apart in a crowded acquiring space is its scale and geographic reach. While newer fintech challengers chase flashy use cases, Worldpay manages the unglamorous work of connecting merchants to banks, processing disputes, and maintaining 99.9% uptime across payment rails that move billions. The company has evolved from a pure processor into a platform, offering tools for payment orchestration, subscription billing, and omnichannel commerce support. Its strength lies not in disruption but in resilience and reach—it powers payments for everything from corner shops to multinational retailers. In the European fintech ecosystem, Worldpay represents institutional financial infrastructure: old enough to be trusted, large enough to absorb regulatory change, and integrated deeply enough that replacing it would be prohibitively complex for most businesses.

Founded 1989

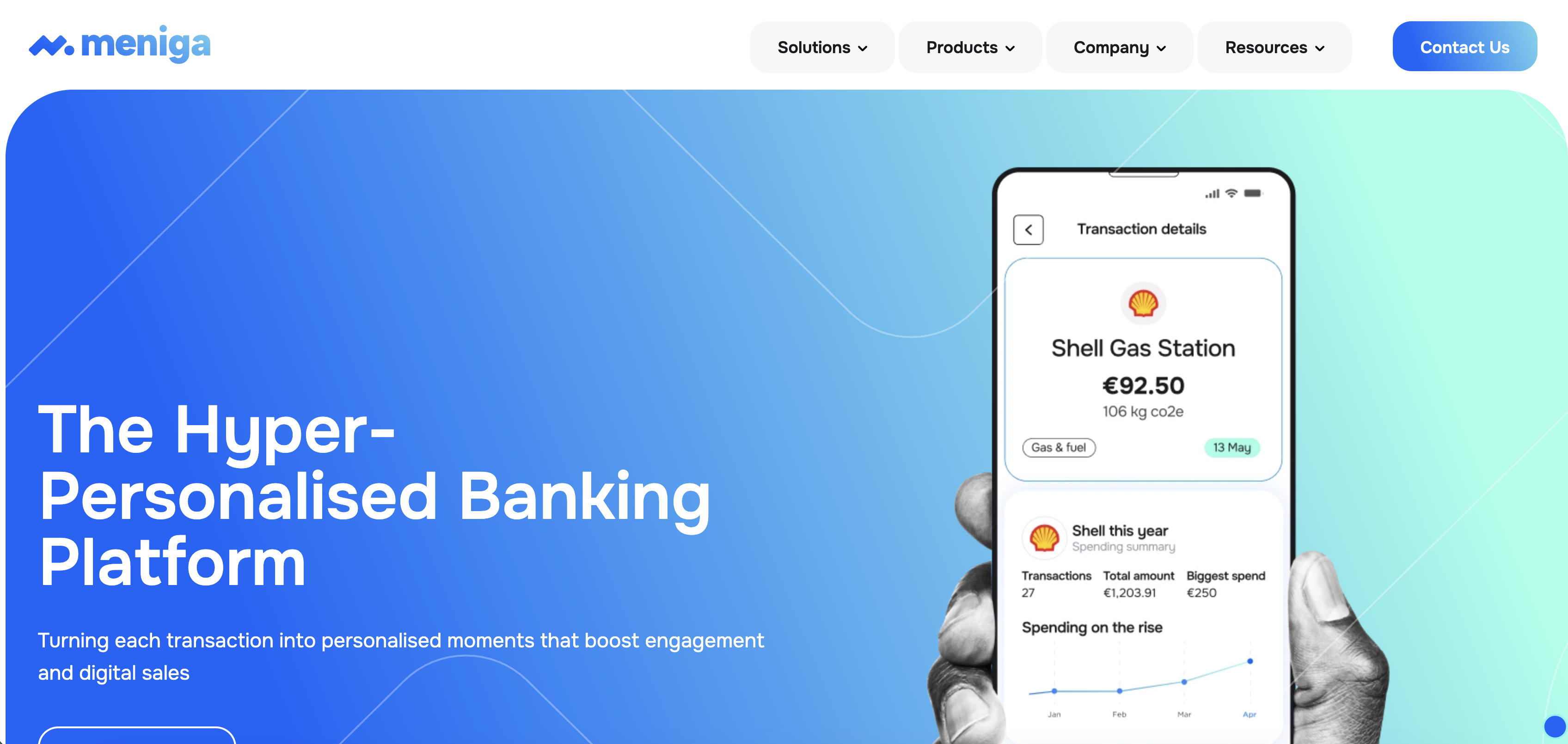

Meniga

Digital Banking🇮🇸 Iceland

Personal finance management has been fragmented for years—users juggle multiple accounts across different banks, struggle to categorize expenses, and lose sight of their actual spending patterns. Meniga built the operating system for that chaos, connecting directly to banks across Europe and beyond to give people a unified view of their financial life.

The company aggregates account data from thousands of financial institutions, automatically categorizes transactions, and surfaces actionable insights through intuitive mobile and web interfaces. Rather than forcing users to manually log expenses or switch banks, Meniga meets them where their money already is. The platform learns spending habits over time and can flag anomalies, suggest savings opportunities, and help families coordinate finances in one place.

While most fintech startups chase headlines with flashy features, Meniga has stayed disciplined on the unglamorous work of data plumbing and user experience. It's become the backend for other financial services—banks, brokers, and insurers across the region use Meniga's APIs and white-label solutions to power their own personal finance tools, rather than building from scratch.

The company operates quietly but pervasively across Northern Europe and beyond, having grown from a Reykjavik startup into a critical piece of financial infrastructure for millions of users and dozens of institutional partners. In an era of financial fragmentation, Meniga is the connective tissue.

Founded 2009

Wallester

Embedded Finance🇪🇪 Estonia

Wallester is a European fintech infrastructure company that makes it simple for other businesses to issue, manage, and distribute payment cards at scale. Rather than wrestling with legacy banking systems and complex integrations, companies use Wallester's APIs and platforms to embed card programs directly into their own products—think neobanks, fintechs, and platforms that need white-label card solutions without the operational overhead. The company handles the technical plumbing: card issuance, real-time transaction processing, compliance, and customer-facing controls, all delivered through clean, developer-friendly APIs. Wallester operates across multiple European markets and works with everyone from emerging challenger banks to established financial institutions looking to modernize their card infrastructure. What sets Wallester apart is its focus on removing friction from the card-issuing process. Most issuers are bound to cumbersome core banking relationships or have to build entirely custom solutions. Wallester sits in the middle, offering a turnkey platform that scales with demand without forcing companies to reinvent core banking. It's become a quiet backbone for European fintechs that need cards fast, reliably, and without the bureaucracy. The company represents a broader trend in fintech infrastructure: the unbundling of banking services into modular, API-first components that let smaller players compete with traditional incumbents.

Founded 2019

finleap

Embedded Finance🇩🇪 Germany

finleap is Berlin's answer to a question the European fintech scene keeps asking: how do you build world-class financial companies at scale? Rather than chase unicorn valuations, finleap builds them. The holding company operates as a fintech factory, incubating and scaling financial startups from day one with institutional backing, operational expertise, and a network that spans regulators, banks, and investors across the continent.

What sets finleap apart is the architecture itself. It's not an accelerator or a VC fund—it's a purpose-built engine for creating and nurturing fintech companies. Each portfolio company gets access to finleap's infrastructure, compliance playbooks, and go-to-market templates, which compresses timelines and eliminates the friction that typically derails early-stage fintechs. The model works: companies like Wayfair-backed Finn, B2B payments platform Foxpay, and lending marketplace Evala have all emerged from the finleap stable.

Internally, finleap operates across payments, lending, wealth, and embedded finance—categories where the European market remains genuinely underpenetrated compared to the US. The company's thesis is straightforward: identify white space in financial services, build products faster than traditional banks can move, and create defensible market positions through technology and user experience. It's less about disruption theater and more about pragmatic value creation.

Finleap sits at an interesting intersection in the European fintech landscape: large enough to command resources and regulatory relationships, independent enough to move quickly, and structured in a way that lets founders maintain autonomy while tapping institutional muscle. For a continent that produces good fintech companies but struggles with scaling, finleap represents a new playbook.

Founded 2014

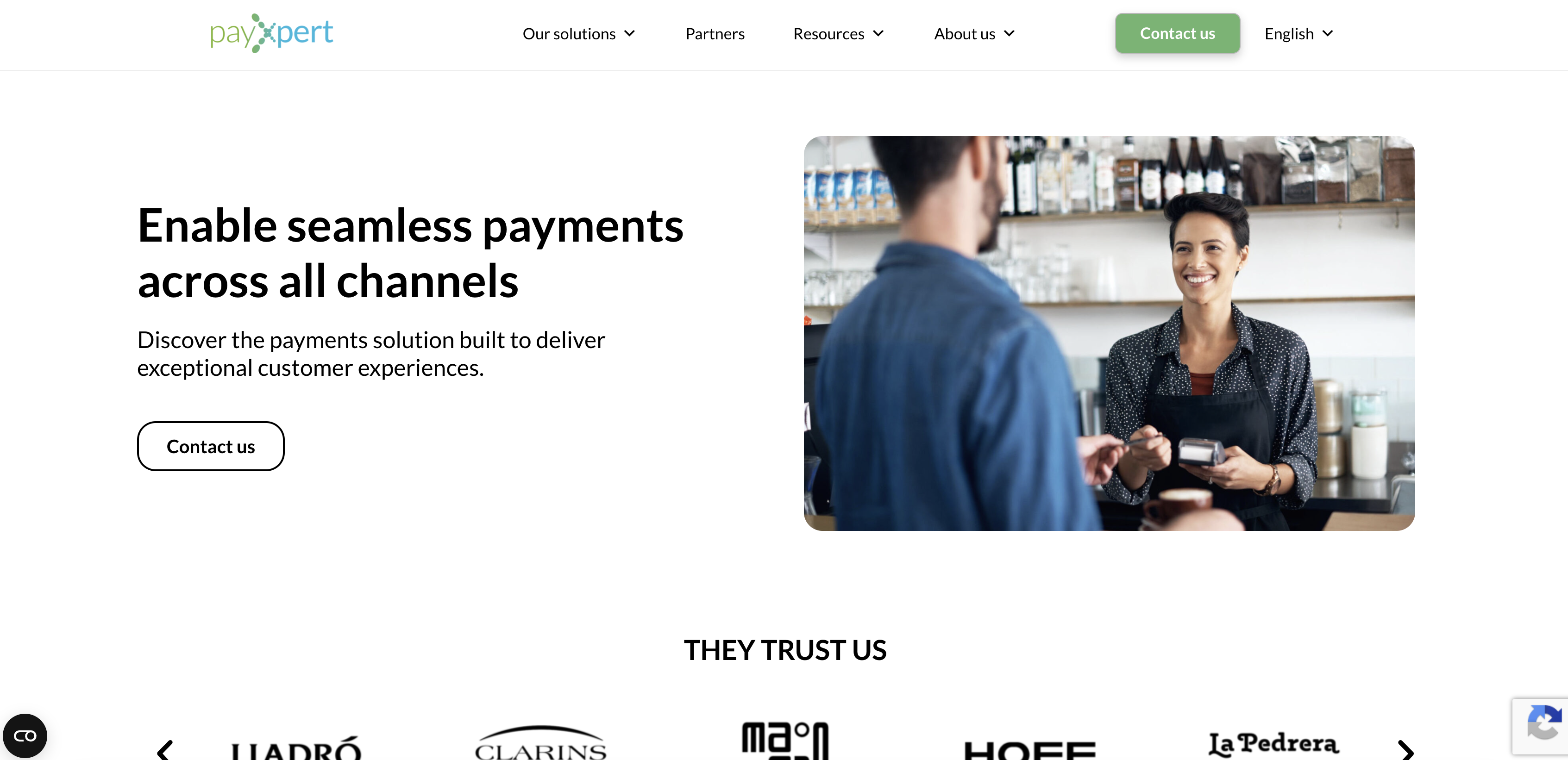

Payxpert

Financial Infrastructure🇱🇺 Luxembourg

Payxpert operates in the unglamorous but essential world of payment processing—the infrastructure that keeps European commerce humming. Founded to solve the messy reality of multi-currency, multi-channel payments, Payxpert provides acquiring and payment gateway services that handle everything from card transactions to alternative payment methods. What sets them apart is their focus on complex merchants: online platforms, travel companies, and e-retailers that can't afford technical friction or settlement delays. Rather than chasing consumer fintech glory, Payxpert built a backbone. They offer white-label solutions and direct merchant acquiring across multiple geographies, meaning they're invisible to most people but indispensable to the businesses they serve. In a market crowded with payment startups obsessed with frictionless checkout, Payxpert quietly handles the hard part: making sure money actually arrives where it's supposed to, reliably and at scale. They're the kind of company that doesn't trend on Twitter but keeps European e-commerce running.

Founded 2008

Showing 12 of 20 companies. View all in the directory →