← All services

30 European companies

data enrichment

Data enrichment enhances raw financial data with additional context — converting transaction strings into clean merchant names and categories, adding firmographic data to company records, or appending risk signals to customer profiles. Enriched data produces better underwriting decisions, more accurate financial categorisation, and more useful financial products than raw transaction records alone.

Typically offered by

European fintech companies offering data enrichment

Tink

Embedded Finance🇸🇪 Sweden

Daniel Kjellén and Fredrik Hedberg didn't set out to build infrastructure. Tink started in Stockholm in 2012 as a consumer personal finance app — an attempt to give Swedish bank customers a cleaner view of their money across multiple accounts. It was a reasonable idea that ran into an unreasonable obstacle: getting reliable, consistent data out of European banks was extraordinarily hard. The technical problem turned out to be more interesting than the consumer product. In 2018 they pivoted, shifted focus entirely to the B2B layer, and started selling the very infrastructure they'd been forced to build for themselves.

That pivot proved prescient. The EU's PSD2 directive, which came into full effect in 2019, legally required banks to open their data to authorised third parties — creating the regulatory foundation that open banking platforms needed to operate at scale. Tink had spent years building exactly those bank connections. When the regulation arrived, the company was ready.

The platform Kjellén and Hedberg built connects to more than 3,400 banks and financial institutions across Europe, reaching over 250 million bank customers. Through a single API integration, banks, fintechs, and merchants can access aggregated account data, initiate payments directly from customer bank accounts, verify account ownership, and enrich transaction data — without maintaining their own connections to hundreds of separate banking systems with different technical standards and update schedules. Clients include Klarna, PayPal, NatWest, ABN AMRO, and BNP Paribas Fortis.

In March 2022, Visa completed the acquisition of Tink for €1.8 billion — one of the largest European fintech acquisitions of that year, and a clear signal of how seriously the global payments industry had come to take open banking infrastructure. Visa's strategic rationale was straightforward: it had failed to acquire Plaid, the US equivalent, after an antitrust challenge, and needed a European open banking capability. Tink gave it 500 employees, 18 European markets, and relationships with over 300 banks and fintechs built over a decade.

The founders stayed on as CEO and CTO through the transition, continuing to run Tink as a standalone Visa subsidiary from Stockholm. Both departed in 2025 — Kjellén and Hedberg announced they were building Freda, a new AI-driven legal and compliance technology startup, with the pair describing Tink as "now in better hands than ever." Francois Tornier, Visa's VP of Open Banking, took over as CEO. The product roadmap has continued under Visa ownership, including a 2024 expansion of Tink's open banking platform into the US market.

Founded 2012

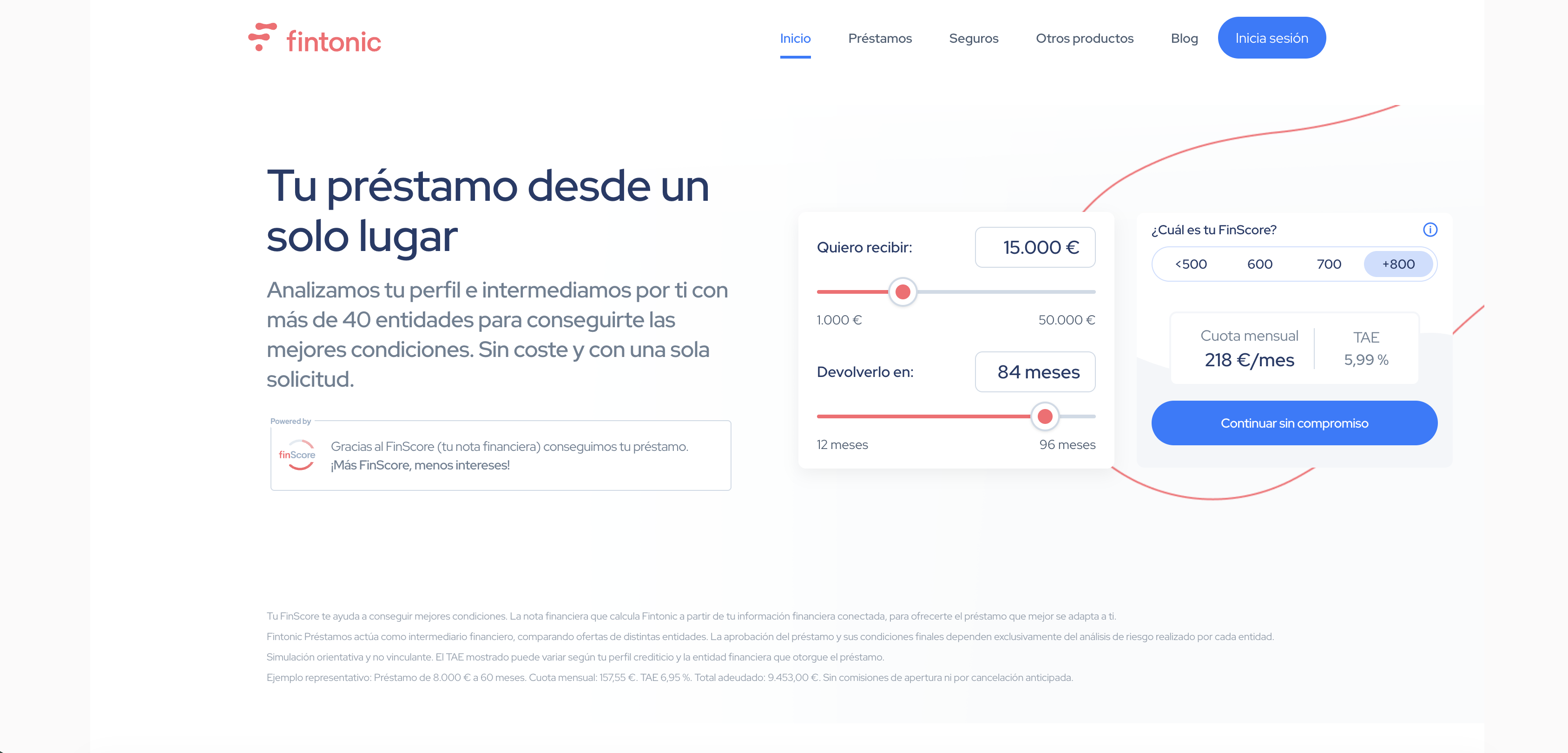

Fintonic

Open Banking🇪🇸 Spain

Fintonic is a Spanish fintech that has spent the better part of a decade helping everyday Europeans understand what they're actually spending money on. Rather than reinvent banking from scratch, it acts as a layer on top of your existing accounts—aggregating transactions, categorizing expenses, and surfacing insights that most banks still bury in PDF statements. The app feels less like financial software and more like a personal finance companion that speaks plain language. You link your bank accounts, and Fintonic does the unglamorous work: tracking subscriptions you forgot about, highlighting spending patterns, flagging unusual transactions. It's deliberately unglamorous work, because the real value sits in simplicity. What sets Fintonic apart in a crowded personal finance space is its focus on the European user. The platform understands local banking infrastructure, multi-currency households, and the specific pain points of cross-border living. It's not trying to be your investment platform or your savings app or your lending provider—it's trying to be the one thing most people actually need: clarity on money that's already moving. For a generation that finds traditional banking UX infuriating, Fintonic occupies the pragmatic middle ground: minimal, useful, and genuinely designed for how Europeans actually manage money.

Founded 2011

OpenWrks

RegTech🇬🇧 United Kingdom

OpenWrks was the UK's first FCA regulated AIS Open Banking platform. In 2020 OpenWrks was acquired by Tink.

Credit decisions have historically been made on backward-looking data — credit files that reflect what happened years ago rather than what a person's financial life looks like today. OpenWrks was founded in London in 2017 to change that with open banking data. Its platform uses transaction data from bank accounts to generate real-time financial insights — income verification, affordability assessments, and cash flow analytics — that lenders, debt advisors, and financial services companies can use to make better decisions about the people they serve. The focus on affordability and debt support is deliberate — OpenWrks has built particular depth in the debt advice sector, providing tools that help debt charities and money guidance services understand their clients' financial situations with precision and speed that paper-based assessments cannot match. Its work with the Money and Pensions Service and other UK debt support organisations reflects a commitment to using open banking data for financial inclusion rather than purely commercial lending optimisation. In the open banking ecosystem, where most data applications focus on acquisition and credit origination, OpenWrks' orientation toward debt support and financial wellbeing is a distinctive positioning that has built genuine trust with the organisations that serve financially vulnerable people.

Founded 2017

Belvo

Embedded Finance🇪🇸 Spain

Belvo is a fintech infrastructure company that lets developers tap into Latin American banking data without building a single integration. The platform connects to thousands of banks and financial institutions across Mexico, Brazil, Colombia, and Peru, unlocking account balances, transaction histories, and identity information through a single API. Rather than forcing developers to chase down fragmented banking systems, Belvo standardizes chaotic regional financial infrastructure into clean, predictable data flows. Its core insight is simple: Latin American fintech is drowning in bank connectivity work when it should be building products. Belvo solves that. The platform serves fintechs, neobanks, and traditional financial institutions looking to modernize lending decisions, open banking integrations, and embedded finance experiences. Think of it as the connective tissue between fractured regional banking systems and the apps that need to run on top of them. By abstracting away the complexity of working with hundreds of different bank APIs and connection methods, Belvo has become the standard for financial data aggregation in a region where banking infrastructure is anything but standardized. It's the kind of boring-but-essential infrastructure that powers smarter lending, faster onboarding, and new financial products across Latin America.

Founded 2019

Enable Banking

Financial Infrastructure🇫🇮 Finland

Enable Banking is an open banking infrastructure platform that simplifies how financial institutions and fintech companies connect to bank APIs across Europe. Rather than building custom integrations for dozens of different banking networks, companies tap into Enable Banking's unified layer—a single API that handles the complexity of connecting to thousands of European banks with varying technical standards and regulatory requirements.

The platform abstracts away the fragmentation that has made open banking adoption slower than it should be. While PSD2 and other regulations opened up bank data and payments, the actual implementation remains messy: each bank interprets the standards differently, each has its own API quirks, and each requires separate integration work. Enable Banking eliminates that friction.

Their core value sits in the infrastructure layer—they're infrastructure for infrastructure. Fintechs use it to access account data, initiate payments, and verify customer identity across European banks without maintaining individual relationships with each one. Banks use it to expose their APIs in a standardized way without rebuilding their legacy systems.

In a market where most open banking plays focus on consumer-facing applications, Enable Banking takes the plumbing approach. They're to open banking what Stripe is to payments: making the invisible layers work so others can build on top of them. This positions them as a critical enabler for the entire European fintech ecosystem rather than a consumer-facing application.

Founded 2018

TrueLayer

Financial Infrastructure🇬🇧 United Kingdom

TrueLayer is a payments and open banking infrastructure platform that lets fintech companies, payment processors, and traditional banks access real-time financial data and initiate payments directly from consumer bank accounts across Europe. Rather than building APIs from scratch or waiting months for bank integrations, developers plug into TrueLayer's unified network and immediately get access to payment initiation, account aggregation, and transaction data from thousands of financial institutions.

The company operates as a critical middleware layer in European fintech. While most payment infrastructure still relies on cards or legacy rails, TrueLayer routes transactions through bank-grade open banking rails, making transfers faster, cheaper, and less friction-heavy. Its API-first approach means a startup launching in five countries gets the same clean integration experience as an enterprise player.

In the competitive open banking space, TrueLayer stands out through breadth of coverage and developer experience. The platform supports payments in 17+ European countries and has built integrations with hundreds of banks—not through partnerships alone, but through technical depth in handling regional quirks and regulatory complexity. Its customer base spans neobanks like Wise and Revolut, major payment processors, and traditional banks replatforming their operations.

TrueLayer essentially democratized access to Europe's banking infrastructure at a moment when open banking regulations made that access possible but still technically demanding. For any fintech building on the continent, it's become a foundational piece of modern payment architecture.

Founded 2016

Moneyhub

Wealth🇬🇧 United Kingdom

Open banking's promise — that financial data, properly used, can help people make better decisions — has been articulated by hundreds of companies. Moneyhub has spent longer than most actually delivering it. Founded in Bristol in 2014, it built one of the UK's first and most comprehensive open banking platforms, aggregating financial accounts, pension data, and property values into a unified financial picture that gives users — and the institutions serving them — a genuinely complete view of financial health. Its B2B platform powers the open banking and financial wellness features of major UK employers, financial advice firms, and pension providers, white-labelling its data aggregation and analytics capabilities under their brands. The pensions integration is particularly significant — Moneyhub connects to pension providers alongside bank accounts, giving users visibility into their retirement savings alongside their current financial position. That breadth of financial data coverage — beyond the current account focus of most open banking platforms — is a genuine differentiator. In the UK open banking ecosystem, where the FCA's consumer duty requirements are pushing financial institutions to demonstrate they understand their customers' broader financial circumstances, Moneyhub's comprehensive data view is becoming infrastructure rather than a nice-to-have.

Founded 2014

Token

Financial Infrastructure🇬🇧 United Kingdom

Token is a London-based open banking platform that sits at the intersection of infrastructure and consumer experience, making API-driven financial connectivity feel less like plumbing and more like a natural part of how money moves. Rather than asking users to log into their banks manually or hand over passwords, Token handles account aggregation and payment initiation through direct bank connections—the infrastructure most fintech apps and traditional banks should have built themselves but didn't.

The company's core insight is that open banking is only useful if it actually works across borders, across device types, and across the chaos of fragmented financial systems. Token's platform standardizes this mess, letting fintechs, banks, and payment companies offer seamless experiences without getting bogged down in regional variations or legacy bank APIs that still feel like they were written in 2003.

What sets Token apart in the European market is its focus on developer experience without sacrificing enterprise-grade security and compliance. While competitors offer raw API access or clunky consent flows, Token treats the entire interaction—from user authentication to transaction confirmation—as a product problem, not just a technical one. They're essentially the connective tissue that lets modern financial products actually work at scale.

Token's role in fintech infrastructure means it powers an invisible layer: the moment you authorize a payment or link an account in an app that "just works," Token's orchestration is likely running underneath. That's the kind of foundational utility the ecosystem desperately needs.

Founded 2014

Inxy

Financial Infrastructure🇵🇱 Poland

Inxy is a European open banking platform that lets businesses tap into customer financial data through APIs, turning fragmented banking relationships into a single source of truth. Rather than asking customers to manually upload statements or reconnect accounts every few months, Inxy maintains a live, permission-based link to real bank data—making it effortless for fintechs, lenders, and SaaS platforms to build smarter underwriting, risk assessment, and financial insights on top of their core products. The platform sits squarely in the infrastructure layer, designed for teams building financial experiences rather than consumers managing their own money. What sets Inxy apart in a crowded open banking space is its focus on simplicity and reliability. While competitors often require technical gymnastics or lengthy integrations, Inxy's API is direct and frictionless. It handles the complexity of PSD2 compliance, account connectivity, and data standardization behind the scenes. The result: lenders can make faster, more informed decisions; embedded finance platforms can offer instant credit lines; accounting tools can automatically reconcile transactions. Inxy is fundamentally changing how financial data moves between banks and the applications that need it most, making it an essential building block for modern European fintech.

Founded 2020

Linxo

Open Banking🇫🇷 France

Linxo is a European personal finance platform that aggregates bank accounts, credit cards, and investments across multiple institutions into a single dashboard. Rather than asking users to switch banks entirely, the app pulls live data from existing accounts—a model that respects the European's pragmatic relationship with their primary bank while offering the insights and control they actually want. The company positions itself as the financial operating system for everyday money management, not a replacement for banking itself.

What sets Linxo apart in a crowded personal finance space is its focus on actionable intelligence. Beyond simple balance-checking, the platform categorizes spending automatically, alerts users to unusual transactions, and helps track progress toward financial goals—all without the paternalistic tone of many budgeting apps. It works across France, Spain, Germany, Italy, and Belgium, making it one of the few genuinely pan-European plays in a category often dominated by single-market apps.

Linxo has built its infrastructure on open banking standards, leveraging PSD2 APIs to connect securely to banking institutions rather than relying on screen-scraping. This approach gives it a technical moat while also keeping it aligned with regulatory trends. The company targets digitally-native adults who want visibility into their finances without the friction of traditional banking interfaces.

In the broader fintech landscape, Linxo represents a specific bet: that most people won't abandon their bank, but they will absolutely pay for—or accept advertising within—a tool that makes that bank easier to use. It's less disruptive than a neobank, more practical than an investment app, and more design-forward than legacy personal finance software.

Founded 2015

Anyfin

Lending🇸🇪 Sweden

Anyfin sits at the intersection of fintech and banking infrastructure, solving a problem most people don't know they have: buried in their financial life are loans and credit products scattered across multiple institutions, often at unfavorable terms. The Stockholm-based platform aggregates these fragmented debts and refinances them into a single, optimized package—think of it as a financial consolidation layer that actually works. Rather than building another neobank or another loan origination system, Anyfin focuses on the underserved middle ground: helping customers reclaim control of debt they already have, often saving thousands in the process.

The company positions itself as a counterweight to the traditional banking industry's opacity around refinancing, where customers rarely know whether they're getting a fair deal. What sets Anyfin apart in the crowded Nordic fintech scene is its technology-first approach to credit decisioning and underwriting, combined with a genuine mission to democratize access to better loan terms. It operates across multiple Scandinavian markets and has built partnerships with traditional financial institutions who recognize that Anyfin's platform actually drives better customer outcomes rather than cannibalizing their business. The company represents a new breed of fintech that doesn't try to replace banks—it intelligently sits between customers and the banking system, extracting value through transparency and automation in an industry built on opacity.

Founded 2017

BVNK

Financial Infrastructure🇬🇧 United Kingdom

BVNK is a digital asset infrastructure company built for the institutional world. Founded to bridge traditional finance and crypto, it provides custody, settlement, and liquidity services for digital assets across multiple blockchain networks. Rather than positioning itself as a trading platform or exchange, BVNK operates as plumbing—a behind-the-scenes infrastructure layer that lets banks, payment processors, and fintech companies add digital asset capabilities to their existing systems. The platform handles the technical and regulatory complexity that kept institutions out of crypto, offering institutional-grade security and compliance tooling alongside access to decentralized finance. In a market flooded with retail-focused crypto products, BVNK targets the institutional infrastructure gap. It serves as the counterparty settlement layer and liquidity provider for financial institutions that want to offer digital assets without building their own custody and execution infrastructure. The company counts major payment networks and banking infrastructure providers among its early customers, positioning itself as the connective tissue between traditional finance rails and blockchain networks. BVNK reflects a maturation in crypto infrastructure—less about speculation and retail adoption, more about institutional plumbing that will quietly power the next generation of financial services.

Founded 2021

Showing 12 of 30 companies. View all in the directory →