← All services

69 European companies

BaaS platforms

Banking as a Service platforms provide licensed banking infrastructure — accounts, payments, cards, and compliance — via APIs to non-bank companies who want to embed financial products without holding a banking licence themselves. BaaS is the infrastructure layer beneath embedded finance, enabling any software company to offer banking-like features to its customers.

Typically offered by

European fintech companies offering BaaS platforms

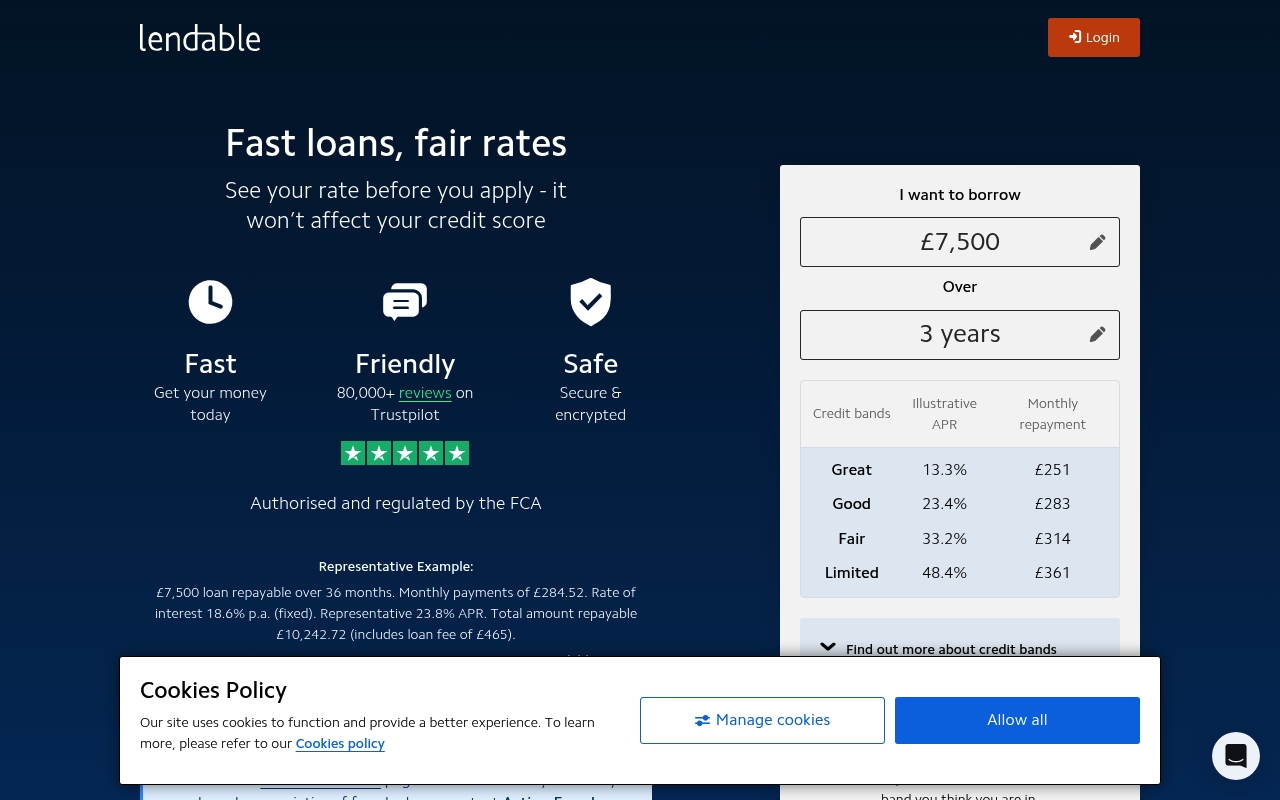

Lendable

Financial Infrastructure🇬🇧 United Kingdom

Lendable sits at the intersection of institutional finance and algorithmic credit. It's a platform that connects alternative lenders—think peer-to-peer platforms, fintechs, and non-bank lenders—with institutional capital markets. Rather than originating loans itself, Lendable acts as a market infrastructure layer, securitizing consumer and SME loan portfolios and selling them to institutional investors hungry for yield in an era of low rates.

The company essentially democratized access to capital markets for non-traditional lenders. Before Lendable, a mid-sized P2P lender or online SME lender couldn't easily tap into the deep-pocketed institutional buyers that banks routinely access. Lendable changed that by building the plumbing—origination APIs, portfolio management tools, and securitization infrastructure—that lets alternative lenders scale without warehousing risk on their own balance sheets.

In the European fintech landscape, Lendable represents a specific but growing category: the infrastructure play that enables other fintechs to thrive. It's not a consumer app; it's the backbone that lets consumer-facing lenders actually fund their ambitions. The platform has processed billions in loan assets and works with some of Europe's most recognizable fintech names.

Lendable's role in the broader ecosystem is that of a bridge—connecting the new world of distributed lending with the old world of institutional capital. It's quietly important infrastructure, the kind of thing that doesn't grab headlines but fundamentally reshapes how credit flows.

Founded 2013

Checkout.com

Embedded Finance🇬🇧 United Kingdom

Checkout.com is a global payments infrastructure company that builds the plumbing beneath the surface of e-commerce. While most payment processors still operate like legacy banking rails, Checkout.com has constructed a single API that connects directly to card networks, acquiring banks, and alternative payment methods—eliminating the middlemen that slow everything down. The platform processes payments in over 150 currencies across 195 countries, handling everything from straightforward card transactions to complex multi-currency settlements for merchants operating at scale.

What sets it apart in Europe and beyond is its refusal to be a typical payment gateway: instead of asking merchants to adapt to the network, Checkout.com adapts the network to the merchant. Founded in 2012 by Guillermo Gutiérrez García-Ceballos, the company has grown from a London-based startup into a critical piece of infrastructure for enterprises, fintechs, and marketplaces that need orchestration at the transaction level. It competes with traditional acquirers and modern payment platforms by combining the reliability of legacy banking with the speed and flexibility developers expect.

In the fragmented European payments landscape, Checkout.com has become indispensable for companies that refuse to compromise on latency, coverage, or control. The company represents a fundamental shift in how payments should work: less about choosing between payment methods and more about making payments invisible.

Founded 2012

Omnius

Financial Infrastructure🇩🇪 Germany

Omnius is a European fintech infrastructure player that builds the plumbing for digital finance. Rather than launching consumer apps or chasing trends, the company focuses on giving financial institutions and fintech operators the core technology to move faster. The platform handles payment processing, account management, and the underlying APIs that let banks and non-banks operate at scale without reinventing the wheel.

What distinguishes Omnius in a crowded infrastructure market is its pragmatic approach to complexity. European banks still manage legacy core systems alongside new digital channels—a messy, expensive reality most fintech companies ignore. Omnius doesn't fight that; it sits in the middle, connecting old and new, and abstracts the chaos away from the business logic above it.

The company targets institutions that need to modernize faster than their technology stacks allow. That includes challenger banks that need banking-as-a-service foundations, traditional banks building new digital channels, and fintech companies that want to scale without owning every layer. It's unsexy infrastructure work—the kind that doesn't generate headlines but quietly powers the financial services layer that consumers interact with.

In the European fintech stack, Omnius occupies a critical but overlooked position: the vendor that lets faster companies stay fast, and slower ones move at all.

Nexi

Financial Infrastructure🇮🇹 Italy

Nexi is Italy's largest payment services operator, controlling the infrastructure that moves money across the country's retail and corporate sectors. Founded in 2013 through a merger of two major Italian payment processors, it manages card transactions, merchant acquiring, and digital payment rails for banks, retailers, and businesses across Europe.

The company operates across the full payments stack—from traditional POS terminals and card networks to modern API-based solutions and instant payment systems. Unlike most fintech startups, Nexi doesn't target consumers directly. Instead, it powers the payment backbone for Italian and European financial institutions and retailers, processing tens of billions in transactions annually. Its business model sits at the intersection of traditional payment infrastructure and modern open banking, positioning it as a critical node in Europe's shift toward real-time payments and embedded finance.

Nexi's role is unglamorous but essential: it's the plumbing that makes modern commerce work, handling everything from contactless cards to mobile wallets to cross-border transfers. In the broader European fintech landscape, it represents the "boring" but profitable core—the infrastructure layer that fintechs themselves depend on to function.

Founded 2013

Solaris

Financial Infrastructure🇩🇪 Germany

Solaris is a Berlin-based fintech infrastructure platform that lets financial institutions and fintechs launch their own digital banking products without building tech from scratch. Rather than wrestling with legacy core banking systems, clients plug into Solaris's cloud-native API layer to issue cards, manage accounts, and process payments at speed.

The company operates in the shadows of most consumer apps—you won't see the Solaris logo in an app store—but its backbone runs through dozens of European fintechs, neobanks, and traditional financial institutions. Think of it as the plumbing that powers other people's banking ambitions.

Solaris dominates a specific niche: the BaaS (Banking-as-a-Service) and embedded finance layer for Europe. While competitors like Thought Machine and Temenos chase enterprise banking overhauls, Solaris stays focused on the modern fintech workflow. Its modular design appeals to companies that need speed and flexibility, not a 10-year implementation project.

In a market crowded with infrastructure plays, Solaris has become essential plumbing for European digital banking. It sits at the intersection of regulatory compliance, technical simplicity, and startup ambition—precisely where the next wave of European fintech is being built.

Founded 2015

MoonPay

Embedded Finance🇬🇧 United Kingdom

MoonPay sits at the intersection of crypto and traditional finance, offering on and off-ramps that let people move money between their bank account and crypto wallets with minimal friction. Founded in 2018, the London-based company has quietly become one of Europe's most important infrastructure plays in the emerging crypto economy, handling billions in transactions across more than 150 countries.

What sets MoonPay apart is its unglamorous but essential positioning: it's not trying to be a crypto exchange or a trading platform. Instead, it's the plumbing layer that makes crypto accessible to ordinary people. You buy crypto through MoonPay the same way you'd buy a digital service—seamless, compliant, and fast. The company operates with full EU regulation, holding licenses across multiple jurisdictions while maintaining the kind of compliance rigor that traditional banks expect. MoonPay's API-first approach means startups, wallets, and even traditional fintech apps can embed crypto purchasing directly into their user experience. This white-label capability has attracted partnerships with everyone from music platforms to gaming studios. The company has raised substantial funding and is valued at over a billion dollars, a testament to how critical crypto infrastructure has become. In a market obsessed with trading speculation and yield farming, MoonPay represents something more fundamental: the normalization of crypto as a payment asset class. It's doing for cryptocurrency what Stripe did for online payments—removing the technical and regulatory barriers that kept it confined to specialists.

Founded 2018

Belvo

Embedded Finance🇪🇸 Spain

Belvo is a fintech infrastructure company that lets developers tap into Latin American banking data without building a single integration. The platform connects to thousands of banks and financial institutions across Mexico, Brazil, Colombia, and Peru, unlocking account balances, transaction histories, and identity information through a single API. Rather than forcing developers to chase down fragmented banking systems, Belvo standardizes chaotic regional financial infrastructure into clean, predictable data flows. Its core insight is simple: Latin American fintech is drowning in bank connectivity work when it should be building products. Belvo solves that. The platform serves fintechs, neobanks, and traditional financial institutions looking to modernize lending decisions, open banking integrations, and embedded finance experiences. Think of it as the connective tissue between fractured regional banking systems and the apps that need to run on top of them. By abstracting away the complexity of working with hundreds of different bank APIs and connection methods, Belvo has become the standard for financial data aggregation in a region where banking infrastructure is anything but standardized. It's the kind of boring-but-essential infrastructure that powers smarter lending, faster onboarding, and new financial products across Latin America.

Founded 2019

Mambu

Financial Infrastructure🇩🇪 Germany

Mambu is a cloud-native banking software platform that lets financial institutions and fintechs launch and operate lending and deposit products without building from scratch. Rather than forcing customers into rigid legacy systems, Mambu provides composable banking infrastructure—modular APIs and pre-built components that work together or stand alone, depending on what you actually need.

The company sits at the intersection of two fintech realities: traditional banks are drowning in outdated core systems that can't keep pace with market demands, while new lenders and neobanks need speed without sacrificing compliance or scale. Mambu's approach is to be the operating system underneath, handling the heavy lifting of loan origination, deposit management, portfolio servicing, and regulatory reporting while letting clients focus on customer experience and product innovation.

What makes Mambu different from other core banking platforms is its emphasis on velocity. Institutions deploy in weeks rather than years. The platform is genuinely modular—you can pick the lending module, the deposit module, or both, and layer in third-party services through APIs. This flexibility has resonated with everyone from African microfinance networks to European challenger banks to enterprise lenders managing complex credit products.

Mambu is now a critical piece of infrastructure in the emerging markets fintech ecosystem, particularly across Africa and Asia, where it powers lending operations for hundreds of financial institutions. In Europe, it's carved out space among mid-market and challenger banks looking to avoid the capital expenditure and technical debt of legacy systems. The company represents a broader shift in fintech: away from end-to-end platforms that claim to do everything, toward specialized infrastructure that does one thing—backend financial operations—exceptionally well.

Founded 2011

Paynetics

Embedded Finance🇧🇬 Bulgaria

Paynetics operates at the intersection of payment infrastructure and embedded finance, building the plumbing that lets fintechs and traditional companies accept, process, and manage payments without wrestling with legacy banking systems. The Bulgarian-founded company has positioned itself as a critical middleware layer—connecting merchants, fintech platforms, and financial institutions through a unified API. Rather than forcing clients into proprietary ecosystems, Paynetics emphasizes flexibility and interoperability, allowing partners to plug into multiple acquiring networks, payment gateways, and settlement rails from a single integration point. This approach has resonated particularly with regional players across Europe seeking alternatives to Western-dominated payment processors.

The company's strength lies not in flashy consumer-facing products but in unglamorous, essential infrastructure: payment orchestration that routes transactions intelligently, card issuing APIs that power embedded finance plays, and acquiring services that work across markets where local nuance matters. For fintech founders building in Central and Eastern Europe or scaling across fragmented European payment corridors, Paynetics removes the friction of navigating dozens of local processors and compliance regimes. Its expansion into treasury and FX services suggests ambitions beyond pure payments—positioning itself as a platform for companies managing cross-border complexity. In an industry dominated by American giants and large European incumbents, Paynetics represents a rare example of a challenger emerging from the region's underestimated fintech ecosystem, proving that critical infrastructure doesn't always require Silicon Valley pedigree.

Founded 2013

Blockchain.com

Financial Infrastructure🇬🇧 United Kingdom

Blockchain.com is one of the oldest and most-visited crypto infrastructure platforms in the world, operating as a bridge between traditional finance and digital assets. The company runs a full-stack crypto ecosystem—a blockchain explorer that millions use to track transactions, a self-custody wallet that puts users in control of their private keys, and a suite of institutional-grade services for serious players. Where most crypto platforms treat blockchain as a trading venue, Blockchain.com treats it as infrastructure. The platform serves retail users seeking transparency and control, developers building on-chain applications, and institutions entering crypto with proper compliance frameworks. The company has maintained a distinctly crypto-native stance while gradually building enterprise services that acknowledge regulatory reality. Its wallet remains one of the most downloaded in the space, offering both simplicity for newcomers and advanced features for power users. Blockchain.com sits at an interesting inflection point in fintech—old enough to have survived multiple market cycles, serious enough to work with regulators, yet still fundamentally aligned with decentralized principles. The platform's role in the broader landscape is foundational: it enables crypto participation across the entire user spectrum, from curious individuals to multinational corporations managing digital asset reserves.

Founded 2011

Token

Financial Infrastructure🇬🇧 United Kingdom

Token is a London-based open banking platform that sits at the intersection of infrastructure and consumer experience, making API-driven financial connectivity feel less like plumbing and more like a natural part of how money moves. Rather than asking users to log into their banks manually or hand over passwords, Token handles account aggregation and payment initiation through direct bank connections—the infrastructure most fintech apps and traditional banks should have built themselves but didn't.

The company's core insight is that open banking is only useful if it actually works across borders, across device types, and across the chaos of fragmented financial systems. Token's platform standardizes this mess, letting fintechs, banks, and payment companies offer seamless experiences without getting bogged down in regional variations or legacy bank APIs that still feel like they were written in 2003.

What sets Token apart in the European market is its focus on developer experience without sacrificing enterprise-grade security and compliance. While competitors offer raw API access or clunky consent flows, Token treats the entire interaction—from user authentication to transaction confirmation—as a product problem, not just a technical one. They're essentially the connective tissue that lets modern financial products actually work at scale.

Token's role in fintech infrastructure means it powers an invisible layer: the moment you authorize a payment or link an account in an app that "just works," Token's orchestration is likely running underneath. That's the kind of foundational utility the ecosystem desperately needs.

Founded 2014

BVNK

Financial Infrastructure🇬🇧 United Kingdom

BVNK is a digital asset infrastructure company built for the institutional world. Founded to bridge traditional finance and crypto, it provides custody, settlement, and liquidity services for digital assets across multiple blockchain networks. Rather than positioning itself as a trading platform or exchange, BVNK operates as plumbing—a behind-the-scenes infrastructure layer that lets banks, payment processors, and fintech companies add digital asset capabilities to their existing systems. The platform handles the technical and regulatory complexity that kept institutions out of crypto, offering institutional-grade security and compliance tooling alongside access to decentralized finance. In a market flooded with retail-focused crypto products, BVNK targets the institutional infrastructure gap. It serves as the counterparty settlement layer and liquidity provider for financial institutions that want to offer digital assets without building their own custody and execution infrastructure. The company counts major payment networks and banking infrastructure providers among its early customers, positioning itself as the connective tissue between traditional finance rails and blockchain networks. BVNK reflects a maturation in crypto infrastructure—less about speculation and retail adoption, more about institutional plumbing that will quietly power the next generation of financial services.

Founded 2021

Showing 12 of 69 companies. View all in the directory →