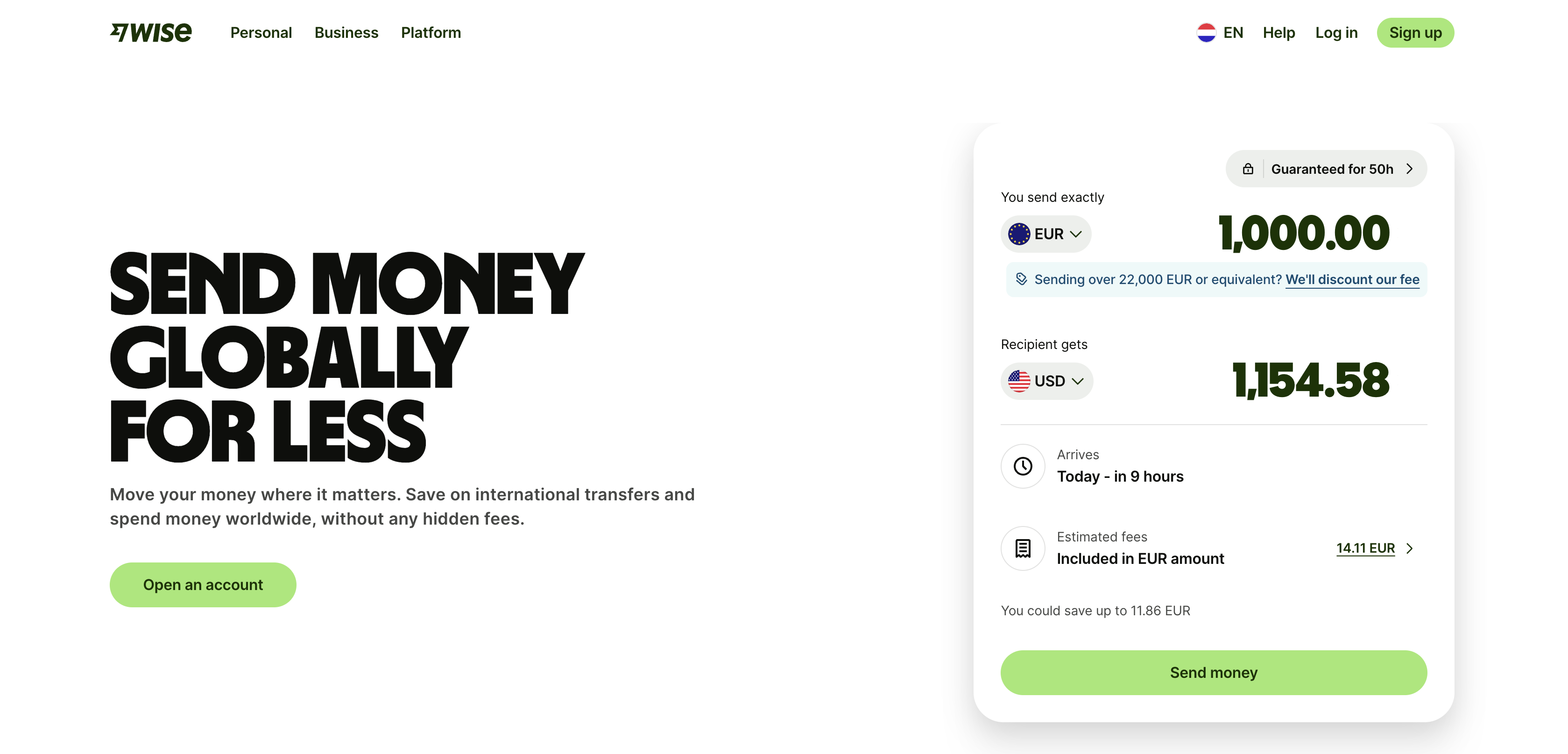

London is the undisputed centre of European fintech, and the numbers support the claim. The UK has produced more fintech unicorns than any other European country — Revolut, Wise, Monzo, Starling, Checkout.com, GoCardless, Funding Circle, and dozens more — and London's concentration of financial services talent, venture capital, and regulatory infrastructure has created a self-reinforcing ecosystem that other European cities have been trying to replicate for a decade.

The Financial Conduct Authority's regulatory sandbox, launched in 2016, gave the UK a first-mover advantage in fintech regulation that shaped how regulators across Europe subsequently approached innovation. The FCA's willingness to engage with new business models — issuing e-money licences to neobanks, authorising open banking initiatives, and developing a specific regime for crypto assets — created the conditions for companies to build and scale regulated financial products in the UK before expanding internationally.

Post-Brexit, the UK has retained its position as Europe's leading fintech hub despite losing passporting rights that previously allowed UK-authorised firms to operate across the EU without additional licensing. Most significant UK fintechs have established EU entities — typically in Ireland, Lithuania, or the Netherlands — to serve European customers, while maintaining London as their operational headquarters. The UK's fintech sector continues to attract more venture capital investment than any other European country, with the ecosystem now mature enough to produce its own serial founders and institutional investors.

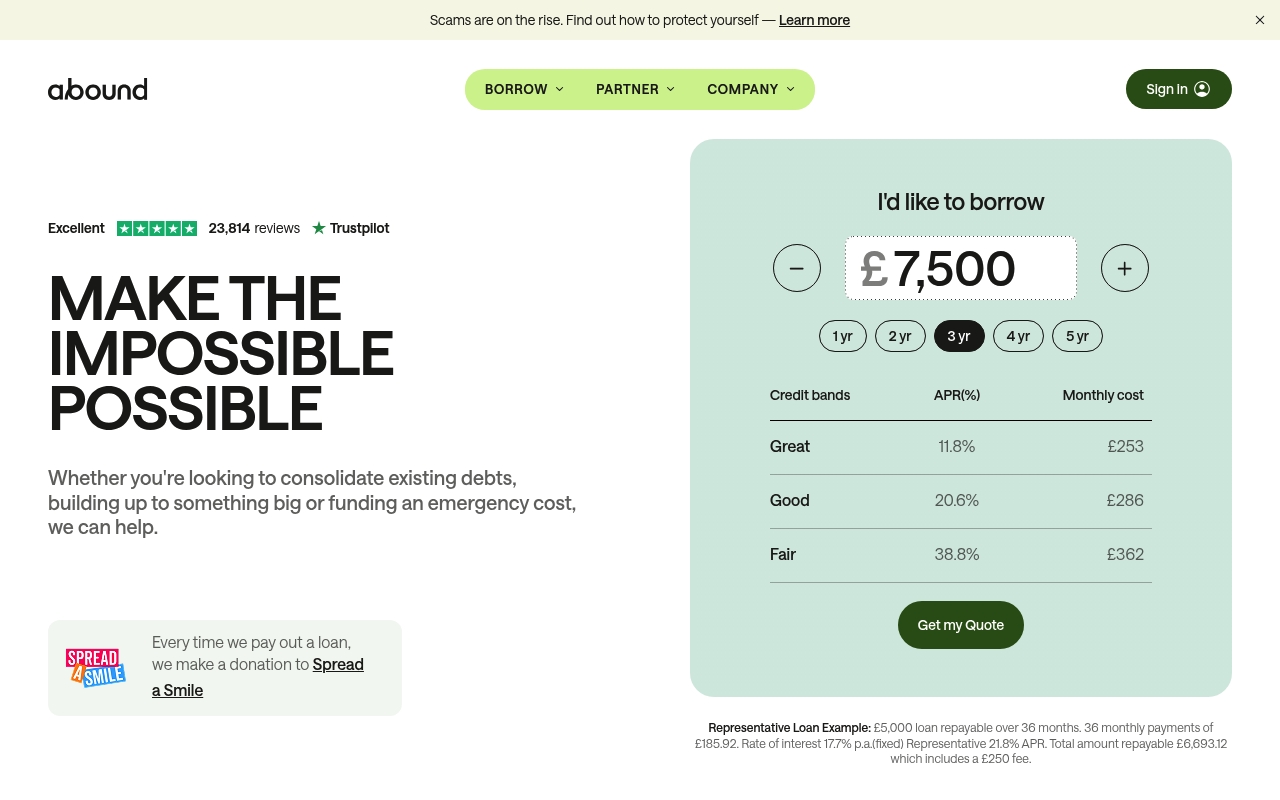

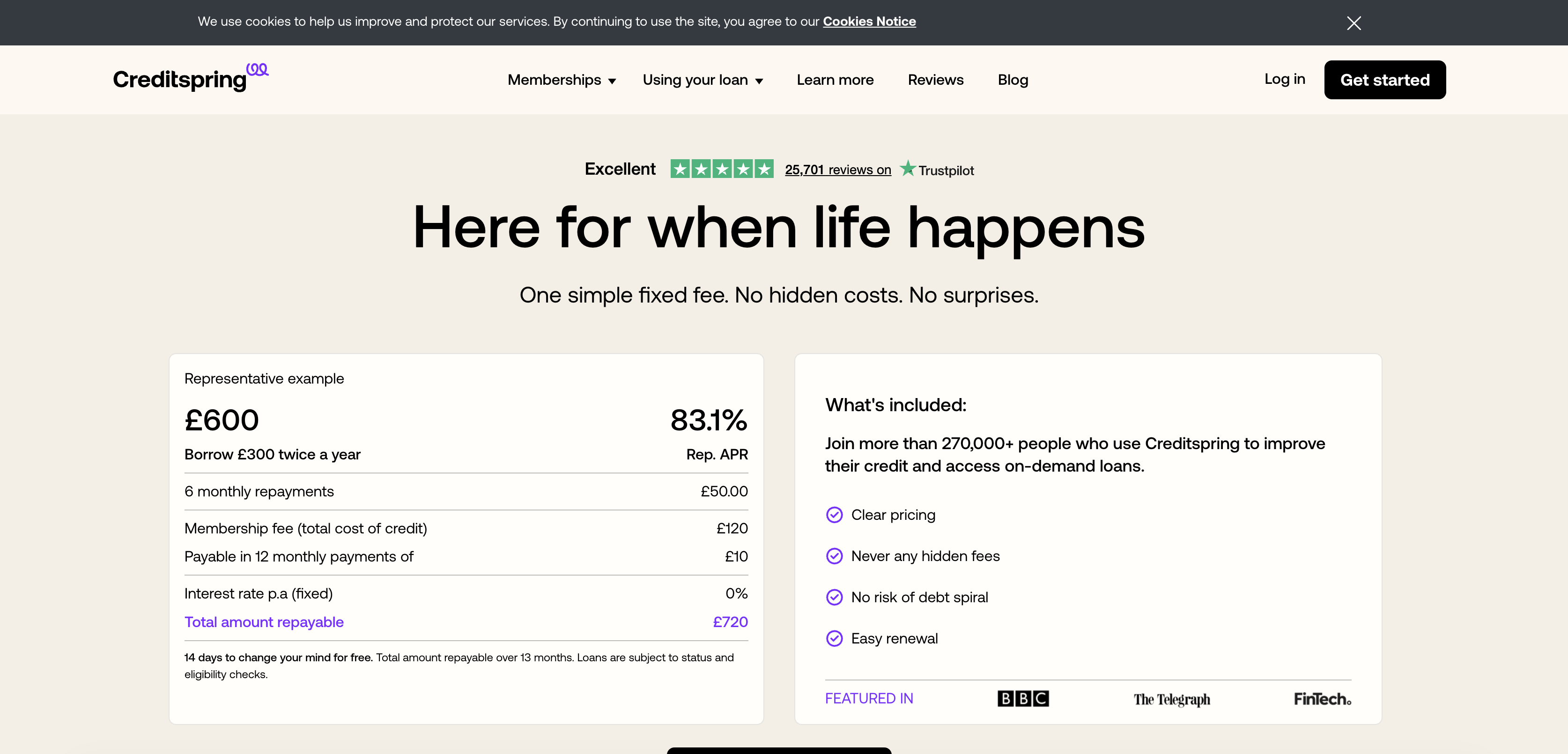

Fintech companies based in United Kingdom